ktsimage

General Overview

Lithium is a specialty battery mineral central to the electrification of global energy. Traditionally priced through over-the-counter long-term contracts between buyer and seller, as demand has soared, end users such as electric vehicle original equipment manufacturers have lobbied for greater transparency.

Data from 2019 indicates how small the size of the market was compared to gold ($170B), copper ($155B), aluminum ($165B), and iron ore ($137B). Six years ago, the world’s leading lithium battery players produced just 29GWh of batteries.

By the end of the decade, it is expected that production increases to 1049GWh, albeit a 35x increase. The biggest players in the industry by that time are likely to be Chinese battery giant CATL, Korean industrialist LG Chem, and US EV icon Tesla (TSLA).

It remains one of the biggest growth commodities and one garnering increasing producer interest. That is why our outlook remains bullish for Australian lithium miner Allkem (OTCPK:OROCF) – its portfolio of assets, beefed up balance sheet and comprehensive coverage of the lithium value chain places it appropriately to reap lithium’s rewards.

Yet not all lithium is equal with grade and impurity impacting prices. Spodumene concentrate contains a range of impurities such as iron oxide, manganese oxide, and magnesium oxide.

Lithium carbonate has greater technical and battery applications along with Lithium hydroxide which is mainly consumed in the production of cathode materials for lithium-ion batteries.

Gangfeng Lithium Co Ltd. and Albemarle have maintained production leadership in the industry, followed by Livent Corporation and SQM. Significant new capacity is planned to keep pace with the ongoing electrification of the automobile industry.

Visual Capitalist

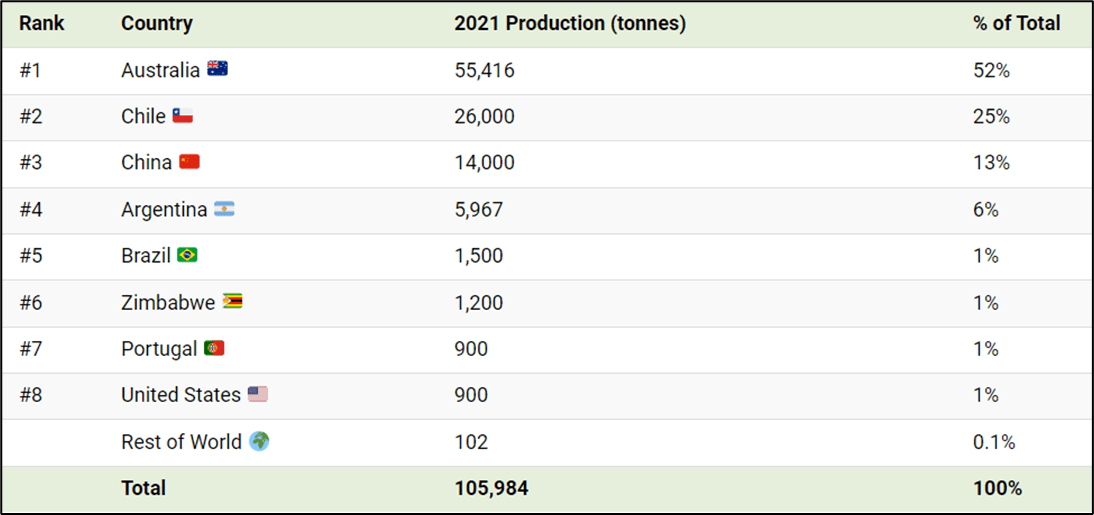

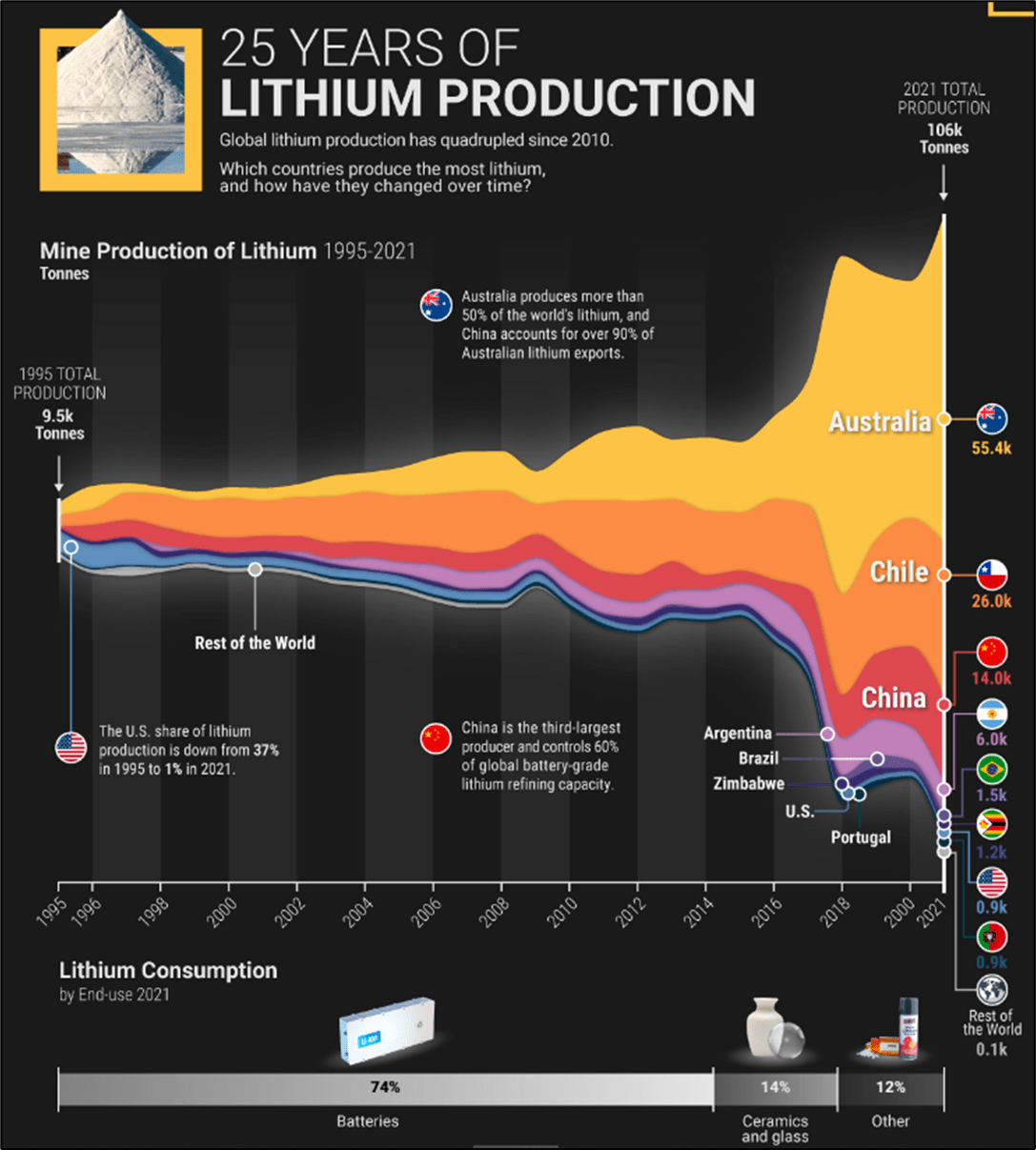

Australia presently dominates global lithium production.

Current Lithium Prices & Battery Production

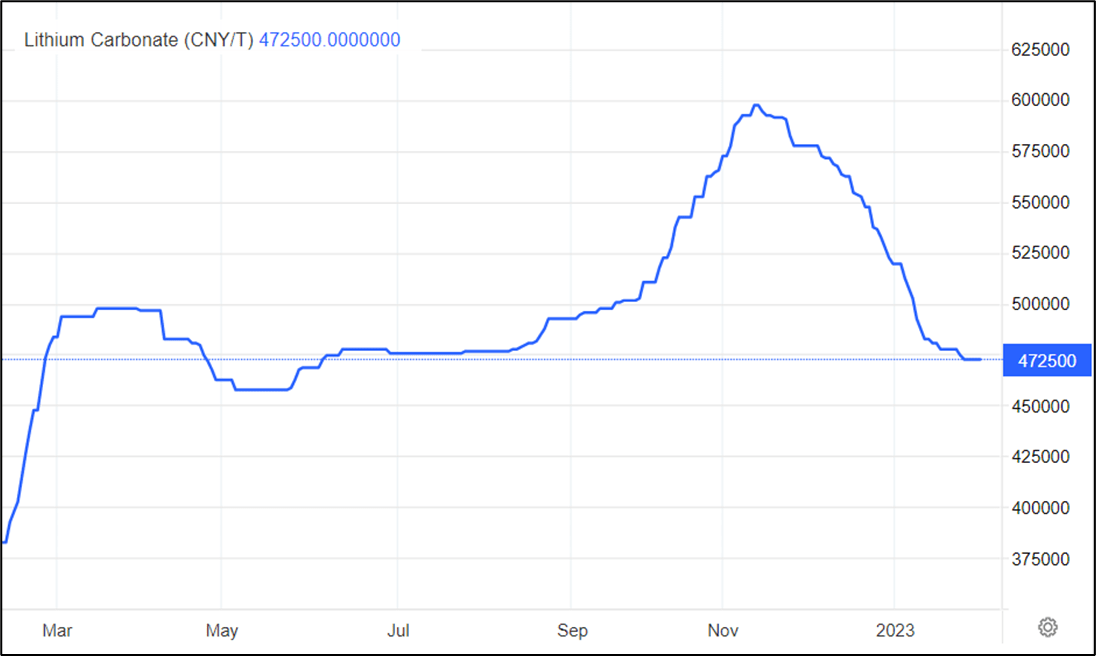

Lithium prices have recently rolled over from their 600,000 RMB/t end of year high posted in 2022. Since then, stronger supply expectations coupled with declining demand has produced a net negative effect for the battery mineral.

Major producer Australia is posting revisions on annual output, now forecast at 915,000 tons – that is still a +30% increase on last year’s volumes and tribute to the enduring demand for battery electric vehicles.

There are 2 major factors impacting benchmark prices – quality and grade of lithium dependent on source (mined hard rock deposits of pegmatites or liquid brines pumped from salars), and shipping costs and volumes.

Trading Economics

Lithium prices have declined since reaching an end of year peak in 2022.

Lithium batteries are comprised of cathode, electrolyte, and anode. As charging progresses, ions flow via electrolyte (often a lithium that provides conduction for flow of ions) from cathode to anode where they are stored.

The anode is a negatively charged electrode normally made of graphite. The cathode is a positively charged electrode made up a combination of cobalt, nickel, manganese, iron, and aluminum. During discharge, ions flow from the anode to the cathode and electrons are passed through the circuit, providing power to the vehicle.

Visual Capitalist

Australia dominates lithium production, accounting for a little over 50% of total world supply in 2021.

Company Introduction

Allkem Limited is an Australian specialty battery chemicals producer. Its core business is mineral extraction, production, and chemical processing of lithium and derived minerals.

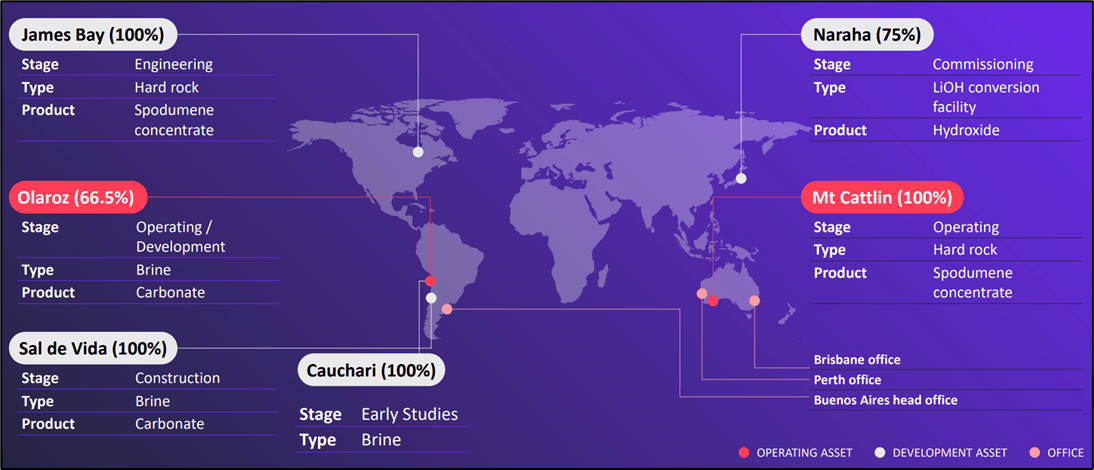

The company boasts a diversified set of assets including lithium brine operations in Latin America’s celebrated lithium triangle, a hard-rock pegmatite operation in Australia, and a lithium hydroxide conversion facility in Japan.

The company holds an important stake in the Olaroz Lithium Complex producing lithium carbonate some 3,900 meters above sea level in Northern Argentina. Additionally, the company’s wholly owned Sal de Vida project, presently under construction, will also boost lithium carbonate production. The James Bay Project in northern Quebec is a hard rock spodumene concentrate set-up presently under project engineering phase.

The firm’s Australian assets include the fully owned Mount Cattlin open pit mine and processing facility. Like James Bay, this prolific hard-rock pegmatite operation produces spodumene concentrate.

The 75% owned Naraha Lithium Hydroxide Plant, currently under commissioning, is engineered to convert primary grade lithium carbonate feedstock into battery grade lithium hydroxide destined for Asian battery manufacturers. Early studies are presently underway to understand feasibility of bringing another lithium brine play online at Cauchari.

Allkem Ltd.

Allkem is a major global lithium chemicals producer with industry leading lineage.

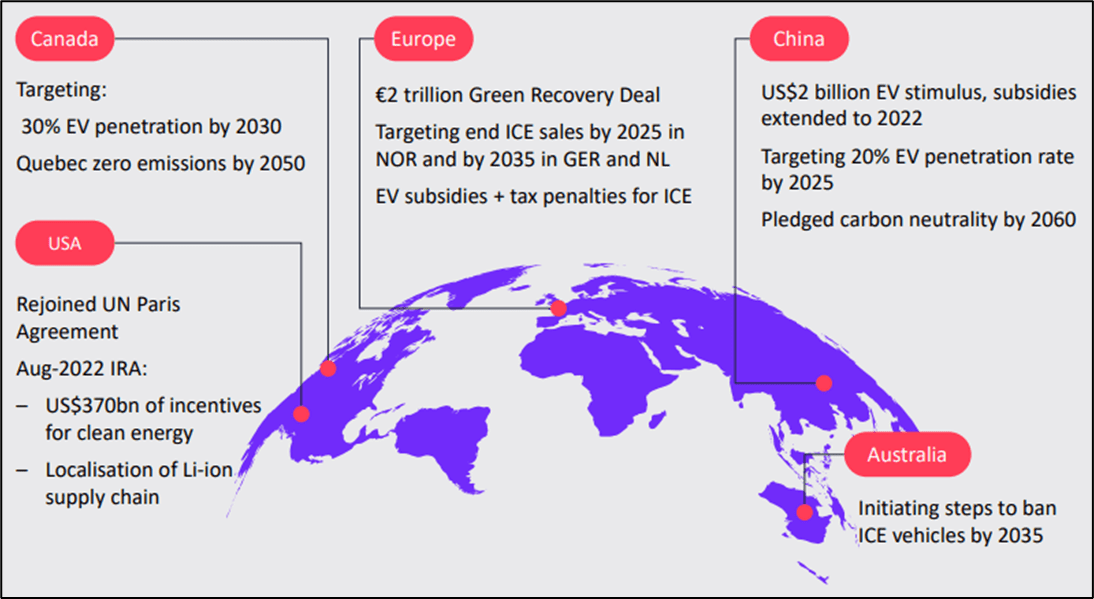

Allkem’s core business, production of battery grade lithium, is buoyed by initiatives undertaken by sovereign governments the world over. The United States recently passed the inflation reduction act, providing for tax breaks linked to battery electric vehicle ownership. An additional $380B in incentives for clean energy have been planned along with promotion of a domestic lithium-ion supply chain.

On the other side of the Atlantic, the European Union is following suit – its trillion-dollar Green Recovery Deal promotes an end to the internal combustion engine along with subsidies to promote electric vehicles.

The world’s biggest EV market, China has penned in US $2B of EV stimulus, extending subsidies and pledging carbon neutrality in the distant 2060. In summary, sweeping shifts are impacting the global transport industry.

Allkem Ltd.

Government sponsored stimulus deals are providing strong tailwinds for the global lithium industry.

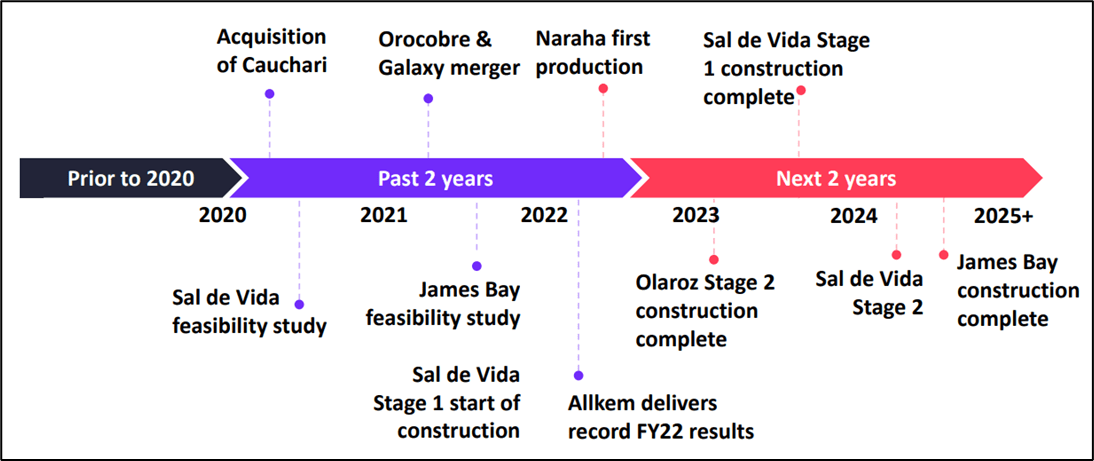

Despite some recent price headwinds, the company has been on a compelling growth trajectory fueled by acquisitions, mergers, licensing agreements, divestments, and carve-outs. Over the past 2 years, the firm has mutated via the Orocobre & Galaxy merger while strategically bringing online Sal de Vida, James Bay and the Naraha processing facility. Accordingly, the company showcases a balanced set of assets covering the lithium carbonate and spodumene value chains.

Allkem Ltd.

The company is building up scale and cash flows as it plans the next steps of its growth trajectory.

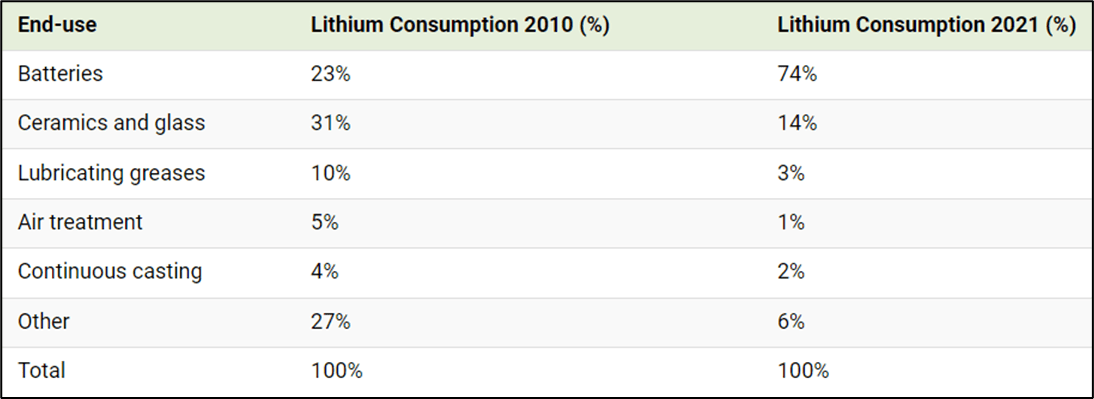

The business case for rapid expansion is supported by astronomical growth in lithium-ion battery production. Over the past decade, lithium consumption for battery manufacturing has accelerated threefold and looks primed to continue its meaningful growth trajectory in the years to come.

The battery mineral presents ideal qualities for battery production – energy density that is twice as much as Nickel metal hydride (NiMH) units, thermal stability, high specific power, low self-discharge performance, low weight, and recyclability.

Visual Capitalist

Lithium usage in battery production has skyrocketed over the past decade.

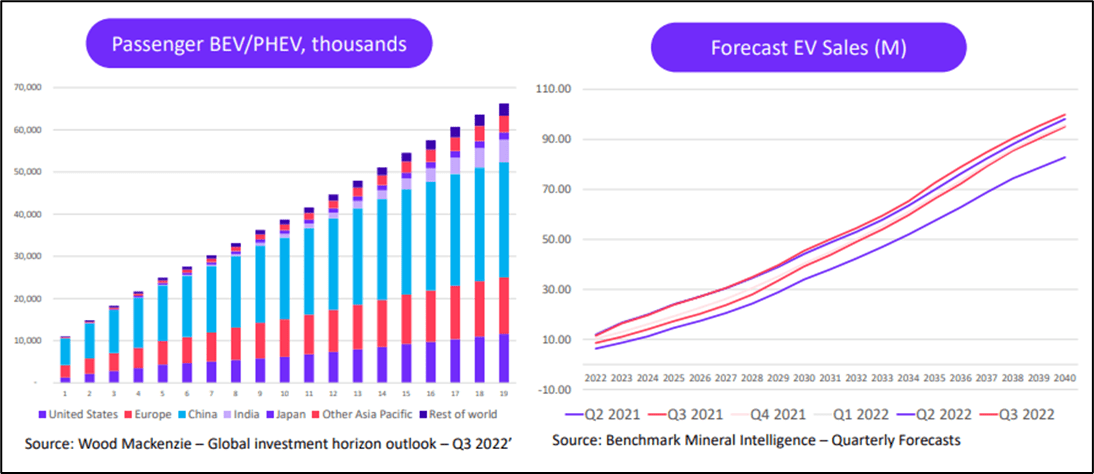

Several detailed studies into the future of battery electric vehicles show astronomical growth buoyed by government subsidies, tax breaks and policy shifts. EV Sales forecasts show roughly 40 million units will be sold by the end of the decade with China leading the drive. India and the Asia Pacific area are likely to be instrumental in delivering the EV growth story.

Allkem Ltd.

As per studies by Wood Mackenzie, electric vehicle sales continue to accelerate with China dominating.

Recent Quarterly Results

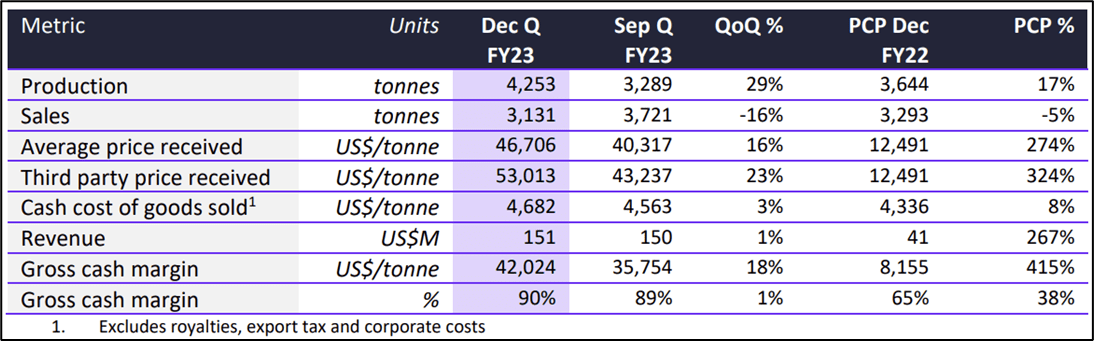

Recent quarterly results have augured a range of operational milestones – the Olaroz Lithium Facility posted record production of 4,253 tons LCE, an increase of 17%. Lithium carbonate sales ticked up, allowing the firm to generate $151M on the topline at a gross cash margin of 90%. Third party sales (excluding Naraha) average $53K/ton FOB, up approximately +20% since last quarter.

Mount Cattlin continued its growth trajectory, producing 16,404 dmt of spodumene, accounting for $83M in hard-rock sales. An additional $32M was generated from 53m715 dmt of low grade spodumene concentrate.

All in, the most recent quarterly results were promising and showed the firm well on course to meet its growth ambitions.

Allkem Ltd.

Recent production numbers continue to show positive progress

Key Financials

Allkem continues to generate substantial interest from the investing community. 47 exchange traded funds presently hold the equity, with US ETFs holding approximately $40M shares. The overall market value held by ETFs globally is about $350M. The stock is covered extensively by 19 analysts, most of whom post positive ratings – strong buy (4), buy (11), hold (2) with the remainder sell ratings (2).

The company currently trades at 8.7x forward price-to-earnings and has a market capitalization of just under $6B. The last few years have seen a radical acceleration of sales revenues, with postings of $84M sales (FY 2021) to $769M of sales (FY 2022) That is almost 10x in revenues in the space of 2 years.

EBITDA margins have almost tripled during the same period, from 25.51% (FY 2021) to 64.20% (FY 2022). Record earnings have followed suit with Allkem registering $305M in net income. Impressive numbers.

Cash has continued to surge – $258M (FY 2021) to $663M (FY 2022) while prudent capital allocation has helped maintain total debt around $350M. As additional project spending is committed, expect that to increase in an orderly, planned fashion.

Cash flow has been just as impressive with the company posting $441M in cash flow from operations in FY 2022. Promising numbers for a company trading at solely 9x forward.

While the balance sheet remains sturdy overall, it is worth highlighting $524M in goodwill generated by the firm’s acquisition spending spree. Any write down will have a direct impact on the income statement if it fails the annual impairment test.

Price to sales numbers, often favored for high growth low-to-zero income companies, is surprisingly low at 3.6x forward. All return metrics continue to point in the right direction – FY 2022 return on assets (+9.36%), return on equity (+17.72%), and return on total capital (+12.12%). Hard not to like to direction the firm is currently headed.

Risk

Despite best-in-class numbers, it is critical to recognize some of the risks facing the firm. China remains not only the world’s biggest importer of lithium but also the largest electric vehicle market globally. Tensions between China and the West continue to surface putting these markets at risk for an Australian lithium producer.

Tit for tat sanctions, specifically after attempts by the US to isolate China through sanctions on chipset equipment could come into play. Furthermore, the global economy is slowing – China’s economy has suffered 3 years of lock-down induced economic moderation showing little signs of a brisk recovery.

Electric vehicles which are part of the consumer discretionary space are already starting to see sales decline. In response, Tesla has started to lower prices igniting a price war among its OEM rivals.

Gangfeng Lithium is a fierce competitor that is exploring the world to ramp up production – it’s likely that it has certain protections and political lobbying power facing an increase of Australian lithium imports.

Main Takeaways

Allkem is a true testament to the strength of the Australian lithium industry. Its diversified portfolio over assets, covering hard-rock and brine deposits, combined with the development of processing firepower positions it aptly across the lithium value chain.

We have seen growth acceleration like rarely seen before with other battery minerals, impacting positively Allkem’s financials. Over $600M in the bank, manageable debt, eye-watering market growth, state sponsored subsidies putting a natural floor on prices, and prudent strategic investments see this firm trading solely at 9x forward PE and 3x price to sales.

At any rate that is a steal and underpins our long-term bullish thesis.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment