Ganna Zelinska

Dear Readers/followers,

Some things are only available to you if you’re internationally diversified and aware. In some cases, it might even be hard to find the full information on a company or its data in any other language than the native one. Such is the case, in part, with the business that we’re going to look at today – Aurubis (OTCPK:AIAGF).

I’ve made myself fairly known on Seeking Alpha for my investments in basic materials, including metals. Hydro (OTCQX:NHYDY) is a good example of this. My foray into copper has been announced when I looked at Southern Copper (SCCO) and other companies in the same space.

In this case, we’re looking at Aurubis, a German copper player.

I apologize in advance because much of the company material is only available in German – but I will do my best to provide explanations where necessary.

Aurubis – From A to Z

Aurubis is a German player in the field of metals – specifically, it’s much in Copper. The company works in processing of metal concentrates, recycling material, and its product business.

The company was formerly known as the Norddeutsche Affinerie AG and has ties to a history going back over 200 years. Since its founding, the company has hit milestones, such as providing over 50% of German copper, M&A’ing Belgian copper producer Cumerio, and being one of the current, most-relevant copper businesses in central Europe.

Aurubis is largely owned (just south of 30%) by German Steel company Salzgitter AG (OTCPK:SZGPY), which owns a total of 100+ subsidiaries in various parts of the metal segment.

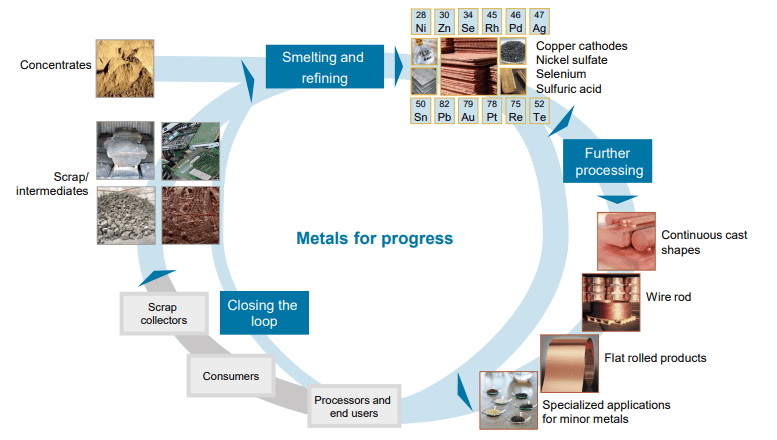

The core business idea of Aurubis is the production of copper cathodes from copper concentrates, various types of copper scrap and recyclable materials, and the like. The products are cast wire rod, shaped rod, rolled products, and strips as well as specialty wire made of copper and copper alloys. The company, due to its extreme expertise built over 240 years in the metallurgy segment, the company also processes precious metals.

While copper remains by far the focus of the company, Aurubis’s expertise is the processing and optimal utilization of complex concentrates and recycling raw materials to produce metals of the highest purity – and they do this across the board.

Aurubis IR (Aurubis IR)

You could call Aurubis a “sleeper” company, but that would only be true if it wasn’t known in Germany and Europe – and Aurubis is very well-known here. It was surprising to me to see the dearth of coverage that we have on the company on SA, and that’s what caused me to go in here.

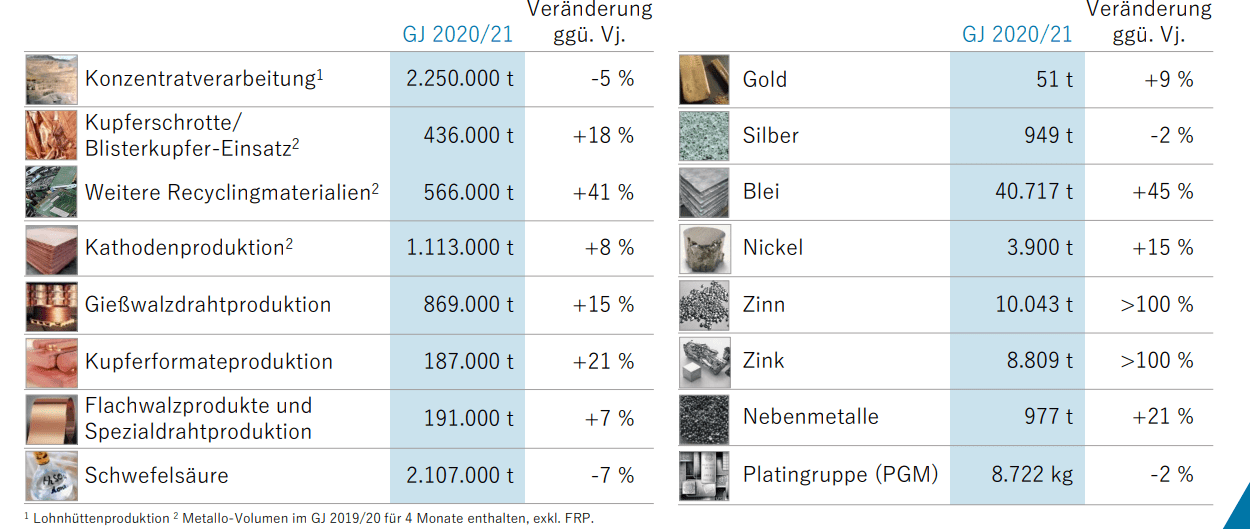

These are the volumes that the company processes.

Aurubis IR (Aurubis IR)

Most of these are self-explanatory, but the top areas (to the left) are concentrate processing, scrap input, Cathode production, cast wire rod output, shape output, flat products, and sulfuric acid. The company also, as you can see, works with Gold, Silver, Lead, Nickel, Tin, Zinc, Platinum, and “minor metals”.

The company is world-leading in copper scrap, flat rolled copper products, and specialty wire. It’s either top 5 in Europe/worldwide in every area you see on the left, with the exception of Sulfuric Acid, where other Basic materials company competes.

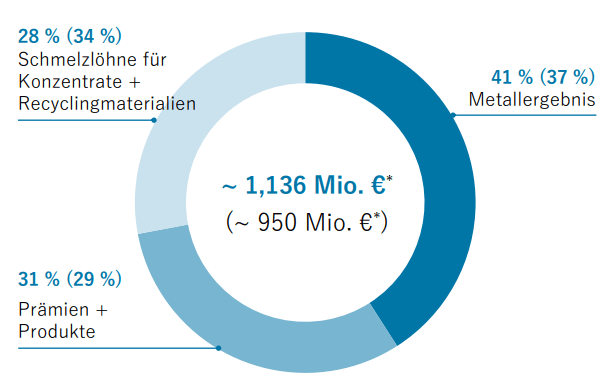

Aurubis was only marginally impacted by overall COVID-19 trends. The company didn’t see much in the way of service or production disruptions next to other companies, and the recent results confirm this. Operating profit is up YoY, ROCE is good and overall profit is excellent. Here is the company sales and gross margins, and this is on a 6M22 basis.

Aurubis IR (Aurubis IR)

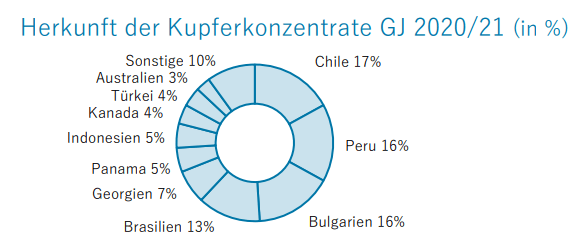

So it’s an appealing mix between smelting payments, metal profits and premiums, and products. Production, sourcing, and demand continue to be positive for Aurubis, and unlike many copper producers, Aurubis sources its concentrates from a wide variety of areas – less than 50% of South America, which is somewhat atypical.

Aurubis IR (Aurubis IR)

The company is sourcing more and more recycled materials, which, unlike the sourcing of concentrates, are coming 35% from Germany and 38% from the remaining western-European areas. In total, Aurubis sources over 75% of its recyclable input from Europe. It processes almost 1,000,000 annual tonnes of copper-containing recyclable materials. The way legislation is pushing to where recyclables from say, China is being limited, is completely changing the sourcing patterns in the industry here.

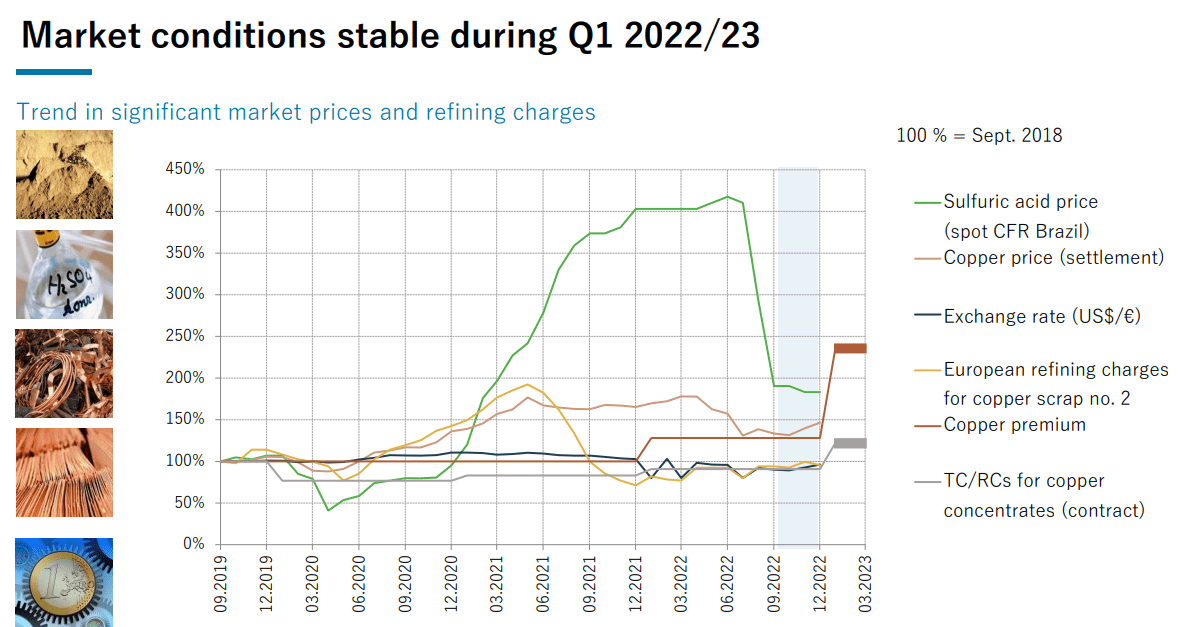

Also, the demand for the company’s other products remains extremely strong – Sulfuric Acid is needed for everything from fertilizers to other chemicals and mental, and spot pricing for the stuff is up significantly. For Aurubis, Sulfuric acid is a byproduct of the processing of copper concentrates at a rate of 1T concentrate to 1T Sulfuric Acid. In 20/21 alone, the company produced over 2.1M tonnes, and global demand for this is intimately tied to overall GDP/economic growth.

On high level, therefore, Aurubis is an expert company in the field of metallurgy, which has chosen copper as its primary field, but also processes a whole host of other metals. The company is ESG-compliant and with high environmental standards, making the company an attractive partner to raw material producers/miners.

Aurubis operations are spread over 20 nations, found not just in Europe, but NA as well, and as I’ve mentioned – it’s a market leader.

We do have the latest results for 2023 – Aurubis was able to, as of the date of writing this article, a realized operating EBIT of €125M, a superb ROCE of 16.3%, and a confirmed forecast range of upwards of half a billion in annual EBIT. The results, YoY, were negative due to changes in the spot price for Sulfuric acid and other trends…

Aurubis IR (Aurubis IR)

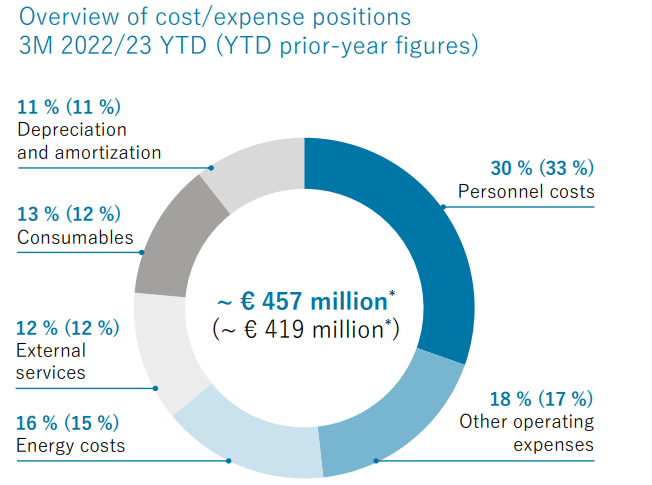

…but gross margins were good, nonetheless. In an operation like this, I also want to look at the expense mix, and this looks as follow for Aurubis.

Aurubis IR (Aurubis IR)

The company is not immune to these changes as you can see, with increases in consumables and naturally, energy. The company’s specifics for this quarter were in no way something that Aurubis themselves could have influenced, but rather is a product of the operating environments. Sales remained solid, and on a 3M YoY period, several of the company’s segments were positive.

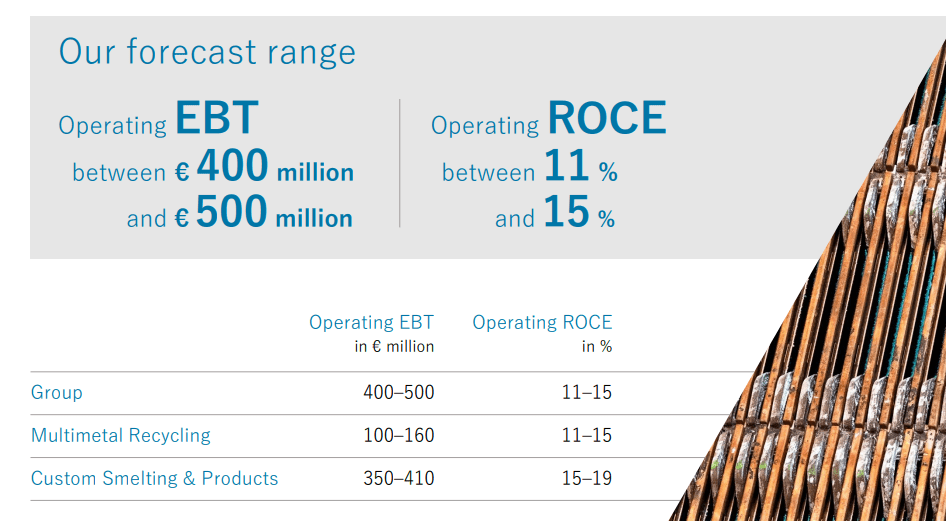

The 2023E assumptions include a reduced demand in the sulfuric acid segment, other than that, stable and strong demand for the company’s products across most market segments and customer segments.

Aurubis IR (Aurubis IR)

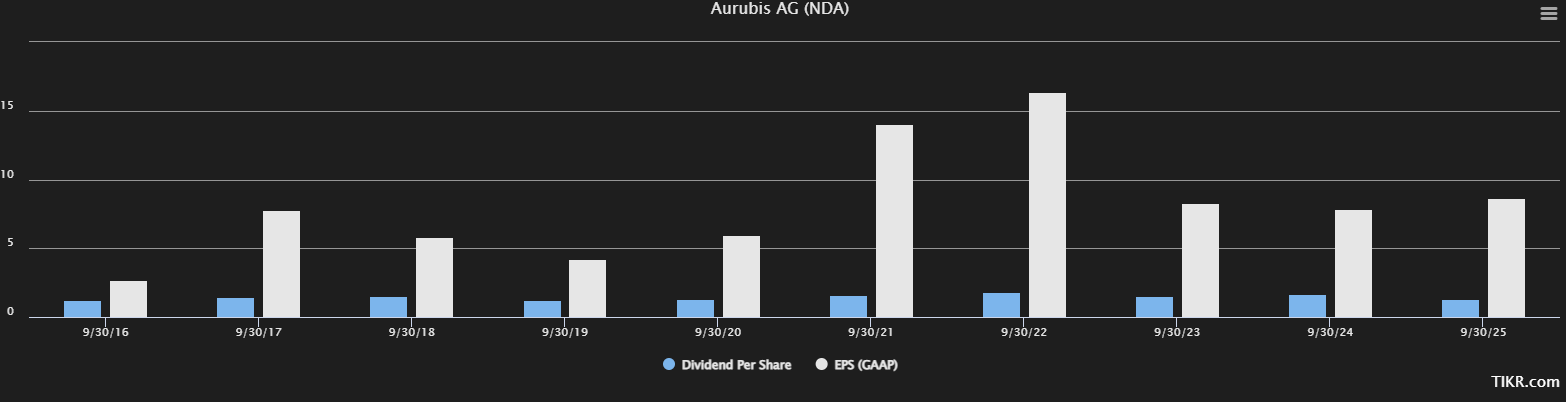

The company is also expanding its asset base, with a new facility in Richmond. The company’s growth strategy is based on a CapEx plan of €1B currently approved, with another half-billion in the works, including key growth projects like Richmond that’s expected to add around €170M worth of annual EBITDA to the company’s income, starting in 2026/2027, another €100M from planned strategic projects. The company is on an exciting trajectory for 2030, including scaling up legacy as well as going into areas like battery recycling. The company isn’t the most stable dividend payor but nonetheless has a decent tradition, especially considering COVID-19, with a currently proposed dividend of €1.8/share, which implies a yield of 1.84% here.

This leads us to the more unfortunate trends for the company here.

Aurubis Valuation

Aurubis is in an “unfortunate” valuation spike, which means that my trough-bought small position is up more than 44% in 6 months. The company’s native share currently trades at round €97.8/share, and that’s even declining a few percentage points today.

The company has a current market capitalization of €4.4B. The company has no relevant institutional credit rating worth mentioning. The native ticker trades under the symbol NDA on the German stock market. Peers are plentiful, depending on how you look. Aurubis doesn’t really mine as such, but peer comps put it on par with mining and metals companies, which include in no particular order, Freeport-McRoRan (FCX), Anglo American (OTCQX:AAUKF), Vale (VALE), Glencore, Rio Tinto (RIO), BHP (BHP) and others. Southern Copper is obviously also part of the list.

Where I have a problem with these comps is that many of them have incredible risk considerations, which I don’t really view Aurubis as having. That’s why when I see Aurubis trading significantly lower than most direct peers, like SCCO and FCX, I’m curious. Aurubis trades at revenue multiples of 0.23x – SCCO is at 6.5x, and FCX is at 3.25x. Same with P/E multiples – Aurubis is at 12x NTM, the other two at over 20x. Essentially, the market puts the company on the level with mining businesses, which I don’t view as being “correct”.

Take a look at forecasts – and know, just as with many other businesses in similar fields, the 2021-2022 fiscal were some great years for the businesses in this field, but these are unlikely to be repeated near term. Still, the normalization results look impressive on a forecast basis, and I don’t see any reason why they wouldn’t materialize at, or close to these levels.

Aurubis EPS/Dividends (TIKR.com)

Still, the current price for the company is problematic. Close to triple digits for the native is too much for the company with the unrealized growth vectors, as they currently are. I can see my way, from a bullish EBITDA/sales growth rate, with appropriate, 8-9% discount levels, to see a €60-€70/share PT. That part of the range is quite logical.

€80-€100 is a very different story, though.

7 analysts follow the native ticker NDA for S&P Global – out of those, only 2 have a “BUY” rating at this price, coming from a €56 low to a €132 high. This extreme spread, given the current €99/share price, is really to be explained by how uncertain the company’s growth vectors are, but macro above all is currently seeming. Analysts come to an average PT of around €93.5. Based on full normalization, I view this as being too positive for the company and where it should be trading.

I forecast based on a lower discount rate, a terminal growth rate of closer to 4-5% as opposed to 6-7%, and I impair the current by 10%, which leads me to an FV target of €80 – and that’s as high as I will go. I would prefer closer to €70, truth be told. The price targets we see from peer analysts here assume a too-high upside.

Aurubis is a great company, and I mean that. It’s one of the more interesting potentials in the entire space, and I wished I had bought more than watchlist when it was cheap. I do believe we’ll see another downturn for the pressured 2023E results that are likely to come, and when the first number in this company’s share price is a “7”, I will be ready with capital to act as necessary.

The yield isn’t the greatest, but it’s great enough, and likely to grow going forward.

So, all things now presented, here is my thesis for Aurubis that I’m working with from this, the initiatory article for the coverage of this business.

Thesis

- Aurubis is a market-leading German metallurgy company in the segment of copper, other non-ferrous metals, and precious metals, as well as the byproduct of Sulphuric Acid. The company has one of the most extensive expertise on the planet for this particular field, and it deserves more than the attention it’s getting here at this time.

- I own stock in Aurubis, and I’m up over 40% in less than 6 months. However, this company is currently overvalued, and I would say that you should not buy the company here.

- Instead, I say that Aurubis is a “BUY” at around €80/share or below for the common, and I would say “HOLD” at this time, but to keep a close eye on the business.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company doesn’t fulfill my valuation-related criteria. This makes it a “HOLD” here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment