St_Aurora72/iStock via Getty Images

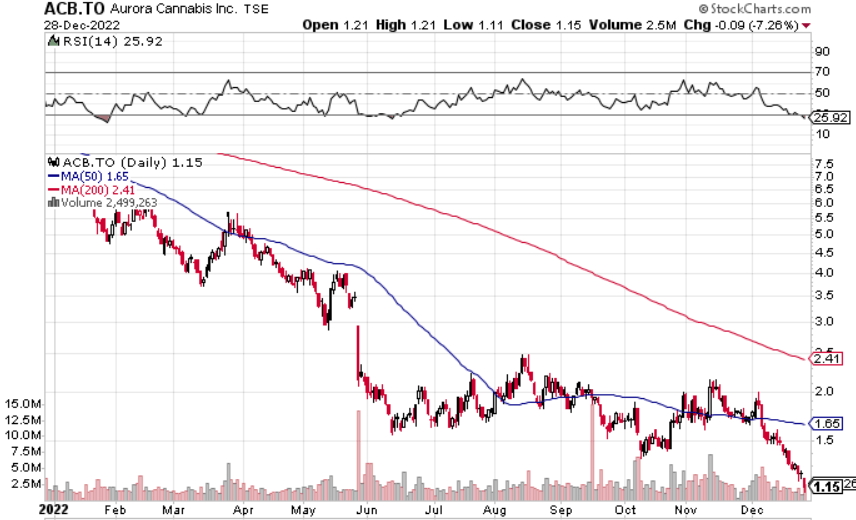

The rate of decline for the Aurora Cannabis Inc. (NASDAQ:ACB) stock price has slowed down in the second half of 2022. The last few weeks of the year unsurprisingly yielded more decreases as investors took advantage of tax loss harvesting. During all this the company has continued to execute on the plan to profitability that was created back in the summer of 2021. The latest update on that plan guides for positive Adjusted EBITDA by the end of the year, which leaves only a few days. Previous management has also provided similar guidance in the past that was never met so investors are understandably jaded. The latest management, however, has been fairly conservative in this positive guidance, and I feel the CEO Miguel Martin has finally right-sized the company and moved it past its inflection point.

stockcharts

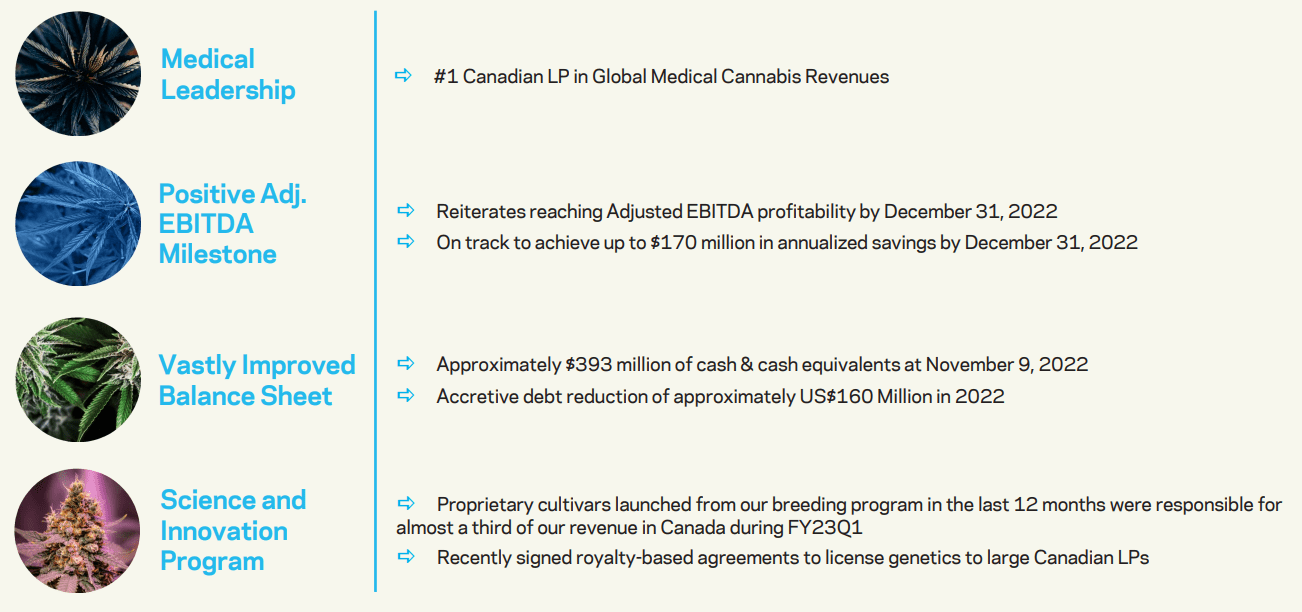

Achieving EBITDA Profitability By December 31, 2022

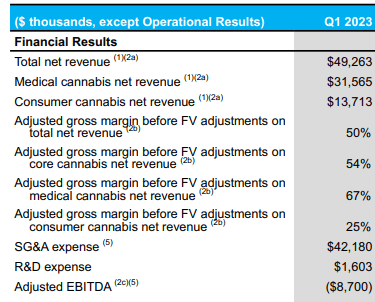

The company plans to achieve its milestone by cutting costs and focusing on high-margin revenue. Costs have been handled exceptionally well and the SG&A line has been declining for several quarters with it maintaining 4-year lows each time. About $150-$170 million in annualized savings will be realized by the end of the year. On the latest earnings call, the CFO announced SG&A and R&D excluding restructuring and other normalizing costs had come down to $33.4 million. The company is also said to be on track to bring that number below $30 million by the end of December.

Revenue had dipped in the previous quarter due to timing of shipments into certain international markets, an Ontario Cannabis Store cyberattack, and a strike in B.C. Those issues have been resolved and the company has guided that revenues will return to the Q4 level. The current quarter will also represent a full quarter contribution of revenue and positive adjusted EBITDA from Bevo compared with only 5 weeks previously which contributed $3.3 million.

Last quarter, the adjusted EBITDA loss came in at $8.7 million. With continued decreases in SG&A of at least $3.4 million, an increase of high-margin revenue, and greater contribution from Bevo it seems feasible that the company may actually reach their milestone of hitting positive adjusted EBITDA in the current quarter. The European revenue should also get a boost due to strength in the Euro over the past few months.

ACB FY2023 Q1 Report

Future Outlook

Achieving this specific profitability milestone will be a huge win for investors and is great for investor confidence, but it’s only one step. The company will still need to grow and drive shareholder value. I believe it can do this as it looks to accretive acquisitions and expanding its medical cannabis business internationally.

Over the past year, the company had also repurchased $235 million of its convertible senior notes, which resulted in an annual cash interest savings of $12.9 million. The company has one of the best balance sheets out of the Canadian LPs and can afford to invest in growth opportunities.

The biggest areas for growth will come from international markets. Aurora already is the medical market leader in Canada and continues to be one of the leaders in markets across Europe. Germany will likely allow for recreational cannabis sometime later in 2023. As Aurora already has a good relationship with the regulators through its work in the medical business it is well positioned to participate in the recreational side. France is another large market that may follow in Germany’s footsteps. Aurora is also the sole supplier of dry flower to the medical cannabis pilot program. Finally, the U.S. has been crawling towards federal legalization for some time now and more and more States have passed laws to legalize recreational use. I believe it will still take a lot of time for these markets to be realized and I don’t put much weight on them in the short term.

Q1 Supplemental Information

Risks

Rising inflation and interest rates have been a weight on the economy and fears of recessions are high. The cannabis business is thought to be less recession sensitive and sales actually did quite well during Covid. The medical segment that Aurora focuses on is also far more stable even in these turbulent times. The company is also diversified across several countries, although the majority of revenue still comes domestically.

Aurora Cannabis Inc. believes its cash on hand is sufficient to fund operations until the company is cash flow positive. We’ll need to wait to see if Aurora Cannabis truly reaches its goal of positive adjusted EBITDA this quarter but I believe the odds are good. Achieving that will likely result in a reassessment of the company’s value and will gain positive sentiment. Overall, I believe Aurora Cannabis Inc. stock has been severally oversold and now is a great time to buy.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment