gorodenkoff

Investment Thesis

Atlas Air Worldwide (NASDAQ:AAWW) conducts its business in aviation services and the outsourcing of aircraft. The company is experiencing solid demand for assets and services due to sustaining shifts in consumer demand for long-term dedicated airlifts. AAWW has recently entered into long-term dry lease & AMCI agreements which I believe can accelerate the company’s growth and can add to the revenues of the company and profits significantly. It can also help the company to attract new customers, and further increase their areas of operations.

About AAWW

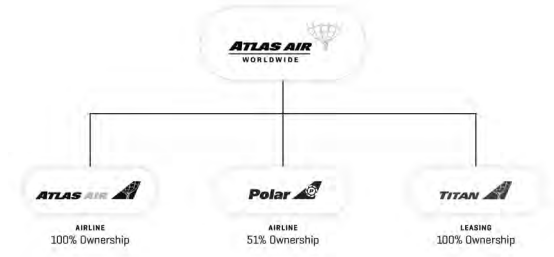

Atlas Air Worldwide deals in providing outsourced aircraft and other aviation operating services. The company has 51% economic interest and 75% voting rights in Polar Air Cargo Worldwide. It is also the parent company of multiple wholly owned subsidiaries, collectively referred to as Titan, which deals in dry leasing services. The company operates a fleet of 747 freighters, which is considered to be the world’s largest fleet. It provides customers with a wide variety of 747, 777, 767, and 737 aircraft. These aircraft are used for international, regional & domestic cargo and passenger operations. The company’s customer base includes express delivery providers, charter brokers, e-commerce retailers, freight forwarders, the U.S Military Air Mobility Command (AMC), direct shippers, manufacturers, airlines, sports teams, and private charter customers. It operates and provides services in Asia, Australia, Africa, the Middle East, Europe, North America, and South America. The company conducts business in two operating and reportable segments: Airline Operations and Dry Leasing. The Airline Operations segment generally delivers cargo aircraft outsourcing services on an ACMI (aircraft, crew, maintenance, and insurance), CMI (crew, maintenance, and insurance), and charter basis to its customers. This segment generates guaranteed minimum revenues through long-term charter contract deals at predetermined rates and levels of operations, which further helps minimize the risk of price fluctuations. The company earns 96% of its revenue from the Airline Operations segment. The Dry leasing segment deals in providing engines and aircraft to customers. This segment’s business is operated and managed by Titan, a cargo aircraft dry lessor. Titan also deals in aviation-related technical services and passenger-to-freighter conversions. The Dry leasing segment generates 4% of the company’s total revenue.

Atlas Air Company Structure (Annual Report of Atlas Air Worldwide)

Financial Trend

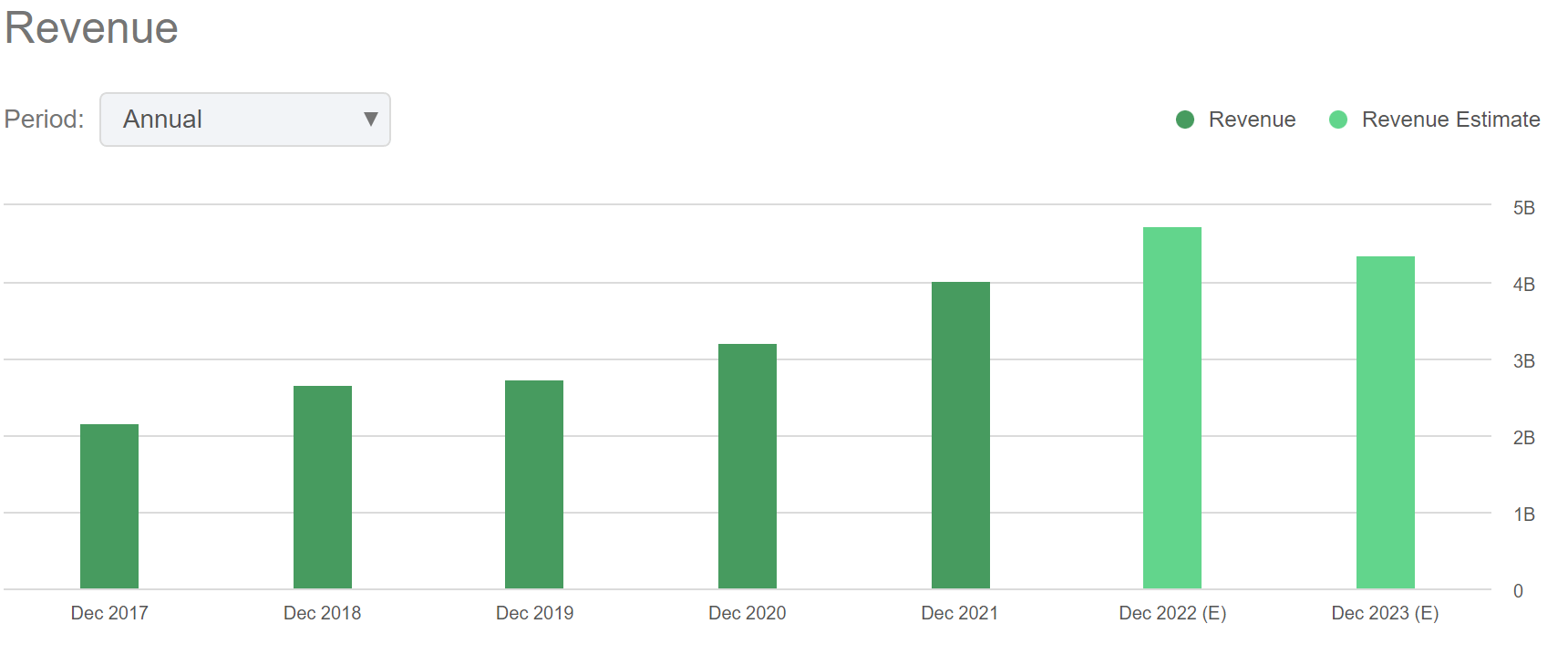

Revenue Trend (Seeking Alpha)

As we can see in the above chart, the company has maintained stable growth in the last five years. The revenue has grown from $2.16 billion in FY2017 to $4.03 billion in FY2021 resulting in a solid 5-year CAGR of 13.28%. The aviation services market and outsourcing of aircraft have observed a significant demand after the pandemic. Even AAWW has experienced substantial growth after the pandemic. The company has reported revenue growth of 25.54% YoY compared to the revenue of FY2020. I think the strong revenue growth might continue in the coming years as the company is experiencing solid demand for assets and services due to sustaining shifts in consumer demand for long-term dedicated airlifts. The company plans to increase the flying amount that the company performs under long-term agreements with cheap rates, which can help the company to attract new customers.

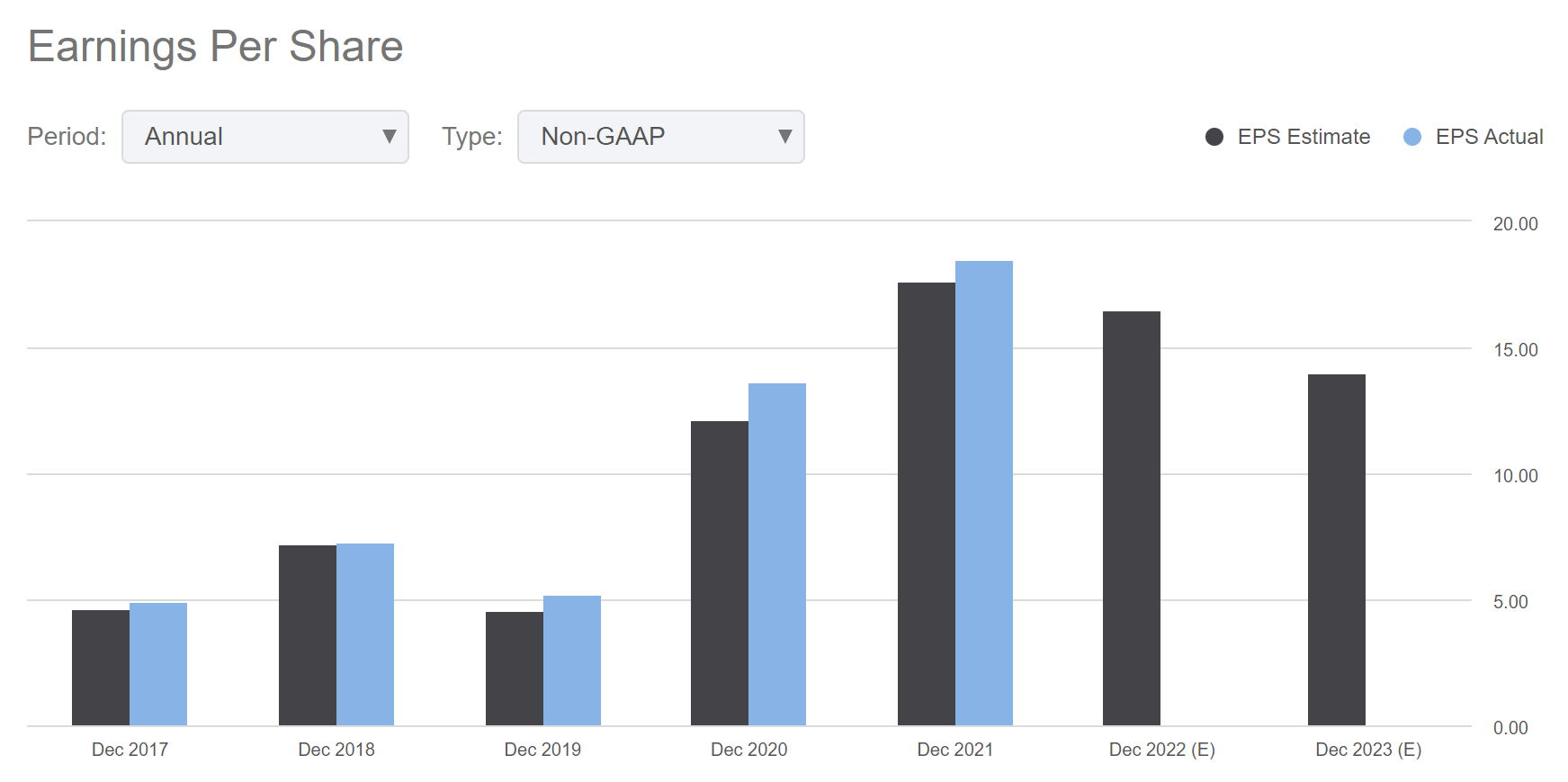

EPS Trend (Seeking Alpha)

Also, the company has experienced strong EPS growth in the past five years. The EPS has grown from $4.93 in FY2017 to $18.51 in FY2021 resulting in a 5-year CAGR of 30.29%. The EPS growth has significantly surpassed the revenue growth, which indicates the company’s solid operating and financial leverage. After considering all these factors, I believe we can expect strong EPS growth in the coming years. Therefore, I estimate the EPS for FY2023 to be $16.51.

Long-Term Dry Lease Agreement

The aviation services market and outsourcing of aircraft have observed a significant demand after the pandemic. Even AAWW is experiencing and benefiting from rising demand in the market. The company has entered into two agreements of dry-lease and AMCI Placements. The first agreement was announced recently by Titan Aircraft Investment which is a joint venture between Titan Aviation Holdings and Bain Capital Credit with Ethiopian Airlines Group. Ethiopian Airlines is an airline business operating in Africa. As per the agreement, the company will place three Boeing 767-300ER converted freighter aircraft on long-term dry leases with Ethiopian Airlines. The delivery of two aircraft is expected to occur later this year, and the third aircraft is scheduled to deliver next year.

I believe this agreement can significantly benefit the company as it will increase its freighter fleet to 10 aircraft, which can ultimately help the company to generate more revenues through these additional three aircraft. I think this deal can create a stable revenue stream for the AAWW as the agreement is long-term. The second agreement announced by the company is a long-term ACMI (aircraft, crew, maintenance, and insurance) agreement made between its subsidiary Atlas Air, Inc and MSC Mediterranean Shipping Company. MSC mainly deals in the transportation and logistics business. According to this agreement, AAWW will operate and manage MSC’s four new Boeing 777-200 freighters globally. The first delivery as per this agreement will be executed in the last quarter of this year. The 777-200 will facilitate dedicated aircraft capacity to cater to the rapidly growing customer demand, which can boost the revenue and earnings of the company significantly. I think the company can attract more such customers in the coming years as it provides fuel efficiency and noise reduction factors. Hence, I believe the investors can expect these agreements to be made for the long term, which significantly reduces the company’s risk in scenarios of adverse global conditions and helps it maintain its guaranteed minimum revenue.

What is the Main Risk Faced by AAWW?

Rising Fuel Prices

The price and availability of aircraft fuel can be volatile and negatively affect the company’s performance. The company’s direct exposure to the fuel risk is limited, mitigated by price adjustments, including long-term charter contract deals. The company does not make fuel expenditures while providing ACMI and CMI services, whereas, in the Dry Leasing business segment, the fuel cost is passed on to the customers. Although if the fuel price increases, customers can reduce the volume and usage of cargo shipments or find less costly shipment alternatives, which can affect the company’s sales volume, further contracting its profit margins. Geopolitical uncertainties can affect the supply of fuel, which can affect the company’s financial operations negatively.

Valuation

The company has recently announced two agreements of long-term dry leasing and AMCI placements which I believe can generate more revenues and accelerate the company’s growth in the long term. After considering all the above factors, I am estimating EPS of $16.51 for FY2023, giving the forward P/E ratio of 6.09x. After comparing the forward P/E ratio of 6.09x with the sector median of 15.15x, I think the company is undervalued. As we know, fuel prices are currently rising due to the Russia-Ukraine war and rising inflation which can contract the company’s profit margins. But I believe the shift in consumer demand for long-term dedicated airlifts can counter the impact of rising fuel prices. After considering all these factors, I estimate that the company can trade at a P/E ratio of 10x, which gives the target price of $165.10, representing a 64% upside from the current share price of $100.70.

Conclusion

AAWW is experiencing solid demand for assets and services due to sustaining shift in consumer demand for long-term dedicated airlifts. Also, the company has recently entered into two dry-leasing and AMCI agreements, which can significantly benefit it in generating more leasing revenues and accelerating its growth. AAWW is exposed to the risk of changes in fuel prices which can reduce its customer base. Currently, fuel prices are rising due to the Russia-Ukraine war and increasing inflation. But the shift in consumer demand for long-term dedicated airlifts can counter the impact of rising fuel prices. After considering all these factors, I assign a buy rating to AAWW.

Be the first to comment