Anastasia Koroleva/iStock via Getty Images

Introduction

ASX Ltd. (OTCPK:ASXFF) (OTCPK:ASXFY) is the operator of the Australian Stock Exchange (‘ASX’), Australia’s largest securities market. Exchange operators usually have very high margins and tend to be monopolists (there are smaller exchanges but those haven’t really threatened the large market share of the main operators like ASX).

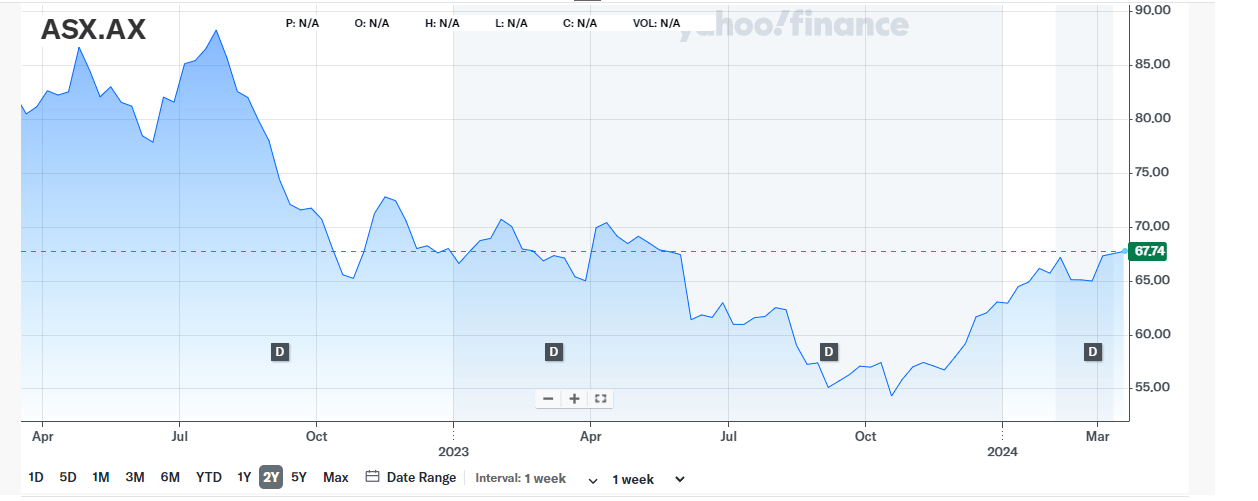

Yahoo Finance

ASX Ltd. is listed on its own exchange, the ASX. It’s trading with ASX as its ticker symbol (which makes it pretty easy to remember). The ASX listing for sure is the most liquid listing as the average daily volume is almost 400,000 shares. I will use the Australian Dollar as base currency throughout this article.

Running an exchange is a high-margin business

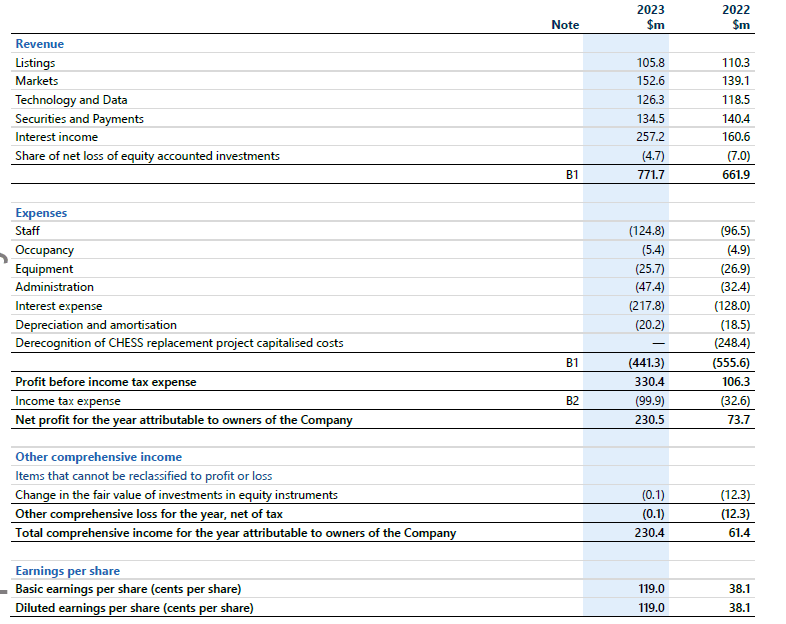

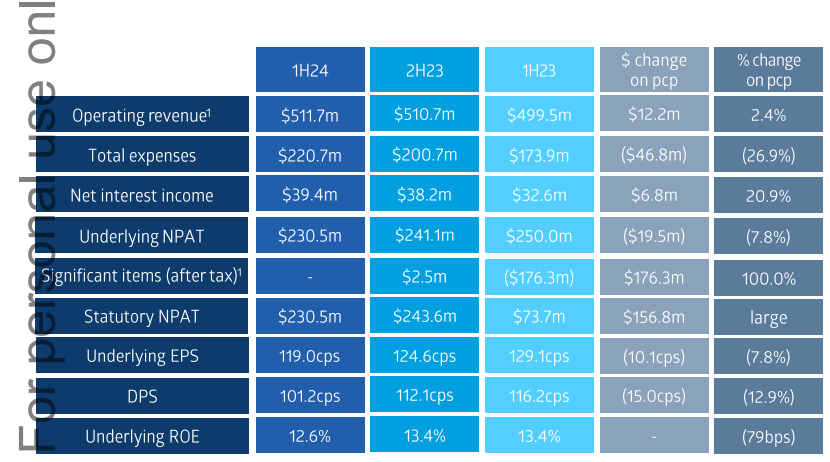

There’s one thing that isn’t even a point of discussion: If you’re an operator of an exchange, your operating margins tend to be quite strong. That’s also the case for the ASX. Whereas the total revenue generated in the first half of the financial year (ASX’s financial year ends in June) was A$772M, the pre-tax income came in at A$330M as you can see below on the income statement.

ASX Investor Relations

While that already is a very respectable margin of in excess of 40%, let’s not forget this also includes the low-margin net interest income. The A$257M in interest income is included in the revenue while the almost A$218M in interest expenses represents almost half of all operating expenses. With a margin of less than 20%, this part of the business is actually dragging the margins down.

If I would exclude the net interest income from the equation and just focus on the “services,” ASX generated approximately A$292M in pre-tax income on a revenue of A$515M. This represents a margin of almost 57%.

ASX Investor Relations

As ASX paid almost 100M AUD in interest expenses, the company’s bottom line showed a net profit of just over A$230M which resulted in an EPS of A$1.19 per share. While that’s more than three times higher than the H1 2023 EPS, let’s not forget the 2023 results were very negatively impacted by an A$248M derecognition of capitalized project costs. This means that on an adjusted basis, the H1 2023 net profit would have been slightly higher than the H1 2024 results.

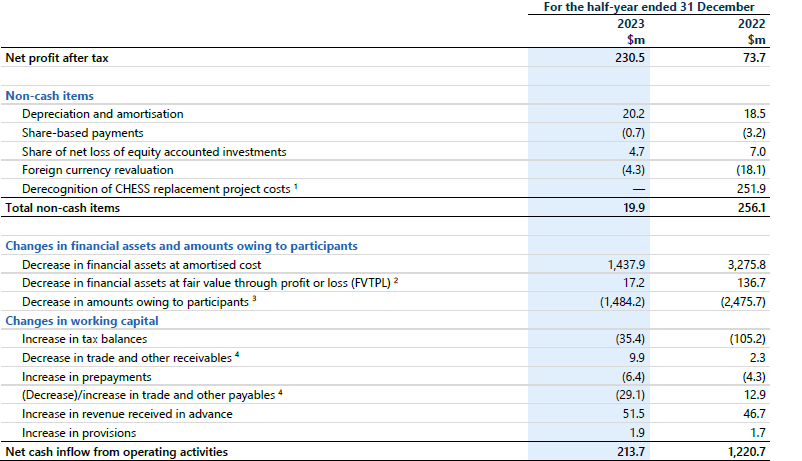

As the stock is currently trading at approximately A$66/share, ASX is trading at almost 30 times earnings. That’s why I wanted to check the company’s cash flow statement as well, hoping I would see a better cash flow metric as the earnings multiple is too high for me to get really interested in the stock.

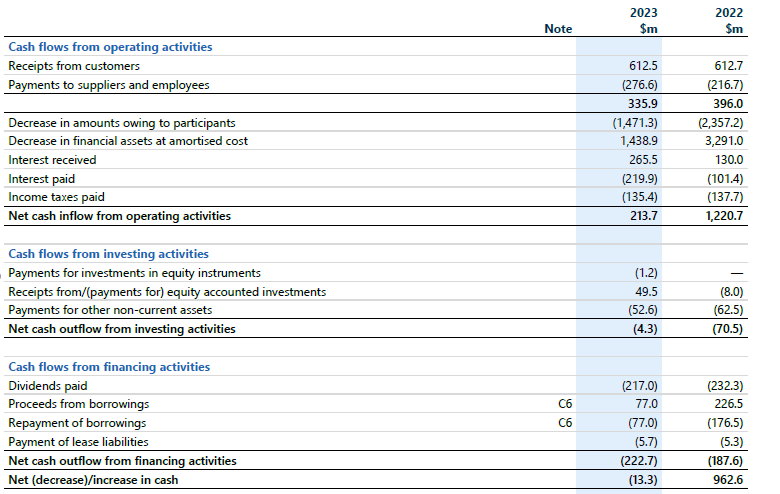

The company reported an operating cash flow of A$214M but this included A$135M in cash tax payments although only A$100M was due. On the other hand, we should deduct A$6M in lease payments.

ASX Investor Relations

This means the underlying operating cash flow generated by ASX was approximately A$244M. The total capex was approximately A$53M which means the underlying free cash flow was approximately A$191M. That’s lower than the reported net income. That difference is caused by a few different elements. First of all, ASX’s income statement included a positive (but non-cash) FX change of A$4.3M, a working capital investment of A$7.6M while the total amount of capex + lease payments of approximately A$58M represents approximately three times the total depreciation and amortization.

ASX Investor Relations

On an underlying basis, this means the net free cash flow was approximately A$199M and approximately A$240M if you would use a normalized capex.

The company acknowledges its operating expenses are quite elevated and it refers to the regulatory commitments and modernizing its technology. The total operating expenses will be lower in the second half of the year but the total capex will likely increase as ASX reconfirmed its full-year capex guidance of A$110-140M. Although the balance sheet is very strong, ASX will issue an A$200-300M bond in the current semester. It will be interesting to see the terms of a debt issue as it looks like the company will have to offer a coupon that might be higher than its free cash flow yield. I wouldn’t mind being a creditor of ASX but the bond offering might very well be institutional-only so I am not holding my breath.

Investment thesis

Although I appreciate the company’s push for modernization, looking at the analyst estimates, the stock is currently trading at approximately 26 times the anticipated FY 2025 earnings while the consensus EV/EBITDA multiple is almost 18. Other exchange operators like Euronext (OTCPK:EUXTF) and Nasdaq (NDAQ) are trading at earnings multiples of 15 and 24, respectively, while their EV/EBITDA multiples are 10.5 and 15.

I did write put options on ASX late last year, but those all had strike prices around A$50, which is closer to what I wouldn’t mind paying for an exchange operator like ASX. At the current valuation, the stock is a “hold” at best.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment