MF3d

Thesis

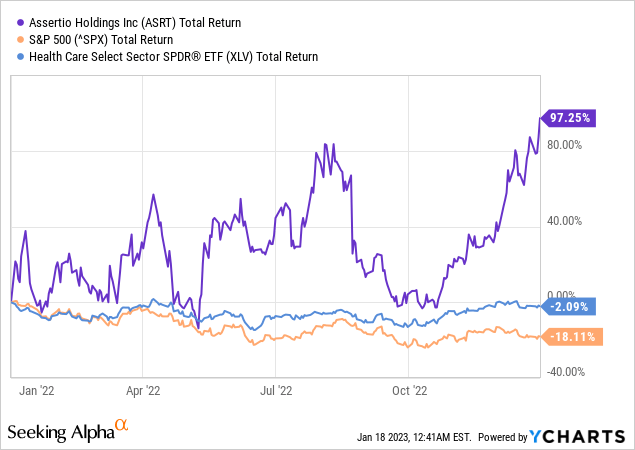

I have long noticed Assertio Holdings, Inc. (NASDAQ:ASRT) and the phenomenal growth this stock has shown throughout 2022 – especially when compared to the S&P 500 Index (SPX) and the Healthcare sector (XLV), of which this stock is a part:

After taking a closer look at this company, I conclude that its low valuation multiples are not just a temporary/cyclical phenomenon and that the potential to generate FCF should continue for the foreseeable future. Therefore, ASRT is still undervalued enough to be considered for buying at current levels or as part of a covered call strategy.

Why Do I think So?

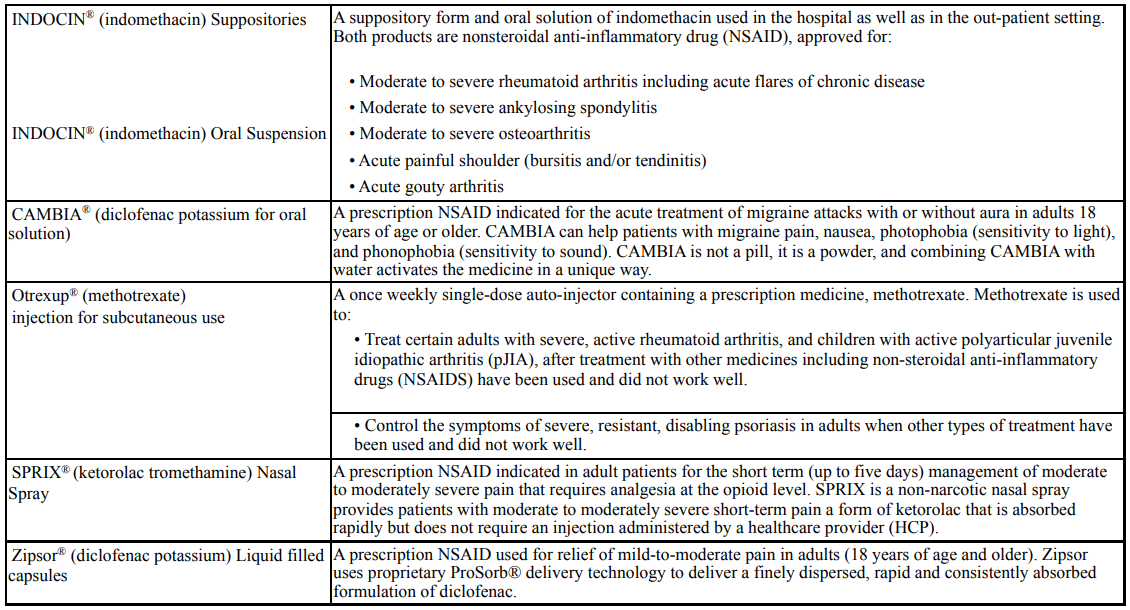

Assertio Holdings is a $200-million market cap commercial pharmaceutical company offering differentiated products to patients. It manages the whole business operations within one reportable segment while substantially all of the revenues come from product sales in the U.S., according to the latest 10-Q filing. ASRT’s primary selling products include the following variety of nonsteroidal anti-inflammatory drugs (“NSAID”):

ASRT’s latest 10-Q filing ASRT’s latest 10-Q filing

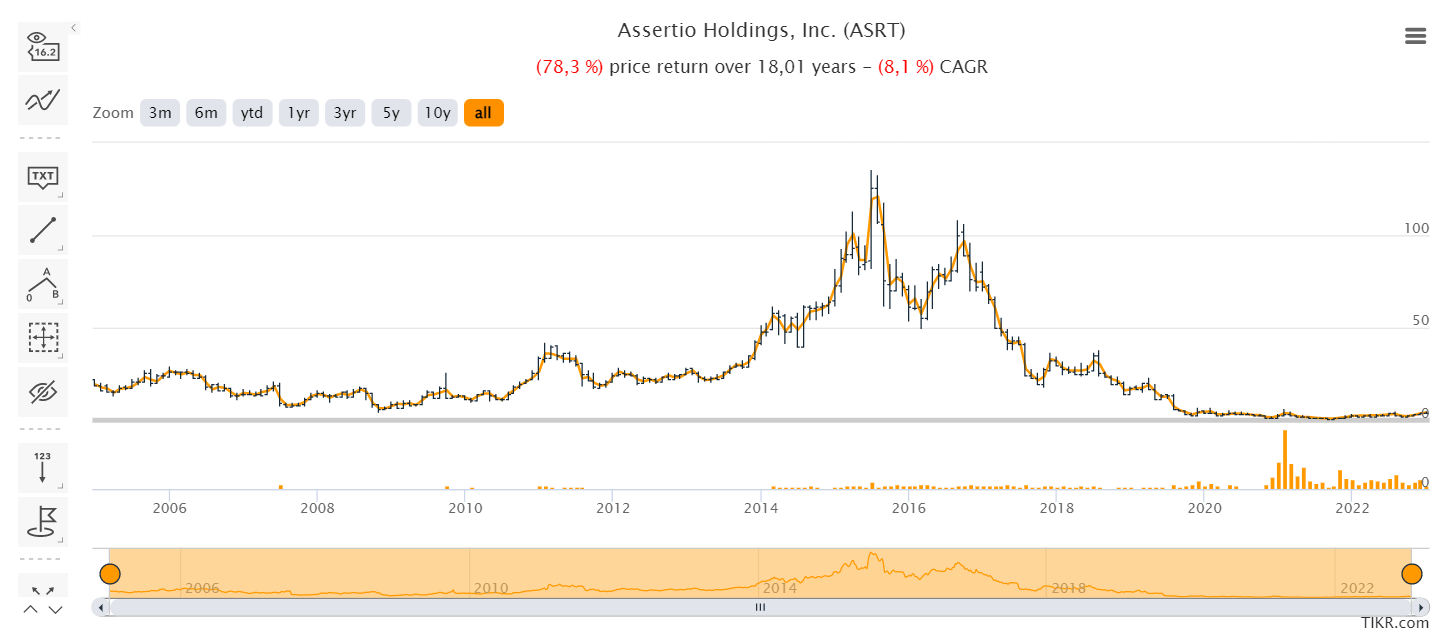

As SA fellow contributor Jeremy Blum noted back in early 2022, Assertio was a stock left for dead after the disastrous acquisition of opioid NUCYNTA in 2015. Therefore, if we move the chart back more than a year, we see its terrible performance since the IPO debut date (January 2005):

TIKR Terminal, ASRT

A year after acquiring the rights to the opioid drug Nucynta, ASRT posted revenue of $29.75 per share and FCF of $4.09 per share at its operational peak [in terms of sales figures] in 2016 – when the stock price stood at more than $100.

A year later [2017], after the company was already involved in the investigation conducted by Sen. Claire McCaskil against the sale and marketing of opioid-based drugs, the company sold its license for the drug to Collegium Pharmaceutical (COLL) in exchange for an upfront payment of $10 million, at least $135 million in royalties per year for a four-year period, and a double-digit percentage royalty on net sales exceeding $235 million, as well as ongoing double-digit royalties after the initial 4-year agreement expires [based on SA fellow Edmund Ingham’s 2021 article].

But getting rid of the debt proved too much for the company, and ASRT eventually sold all rights to Nucynta for an upfront payment of $375 million to buy out most of its the outstanding debt. Management decided to use the remaining liquidity to acquire Zyla Life Sciences in March 2020 – giving ASRT Zyla’s INDOCIN products, which are now the company’s flagship products.

Then followed a series of management reshuffles – it was necessary to somehow reduce the company’s cost base. This led to ASRT becoming a penny stock by mid-2021 and taking on a new challenge – being able to list on NASDAQ.

Ultimately, the company was left with 2 of its legacy assets (Cambia and Zipsor in the table above) and assets after the Zyla acquisition. They all generated revenue, but there were profitability issues – the company could not fully break even on EBIT, especially in 2020 (when cost-cutting measures were needed).

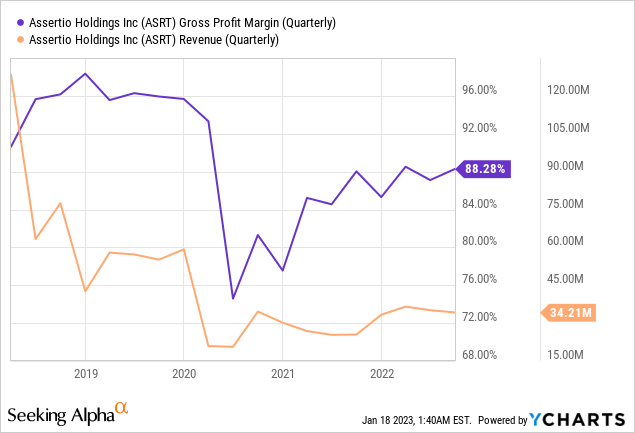

The pivot came in late 2020, when CEO Daniel Peisert switched to an online sales model and got rid of unnecessary staff. Sales did not decline as a result, but actually grew, while gross profit margins began to recover significantly. This momentum continued over the next 2 years – as of Q3 2022, ASRT has a gross profit margin of > 88%, which is hundreds of basis points higher than it was in mid-2020:

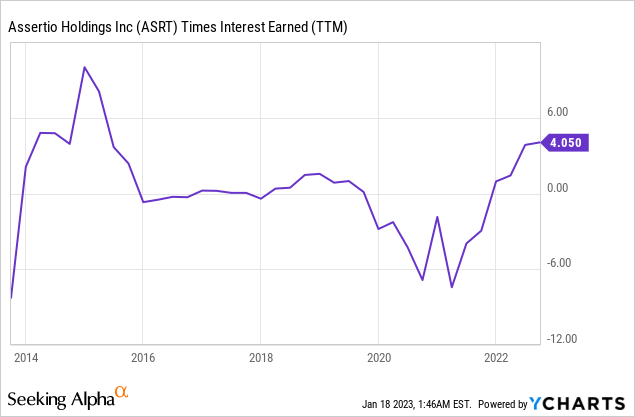

Assertio returned to operating profitability (EBIT margin of 12.67%) in March 2021, and since then the margin expansion has only strengthened, reaching 30.26% in Q3 2022. Interest expense has fallen steadily and now stands at a comfortable 6% of total revenue – an improvement of 380 basis points in just 1 year. Thus, today Assertio can once again be described as a creditworthy company with very low credit risk – this is reflected in the dynamics of the times-interest-earned [TTM] ratio, which has returned to the historical values of the company’s “past greatness”.

The restructuring appears to be complete – the CEO said at the last earnings call that Assertio’s new commercial platform should now move to growth with improved profitability.

As of the end of Q3 2022, the company had $64.8 million in cash and ST investments on its balance sheet, representing more than 35% of total market capitalization. Management sees many opportunities for future M&A transactions such as the one ASRT completed with the acquisition of an exclusive license to the Sympazan intellectual property from Aquestive for an upfront payment of $9.0 million.

We think the M&A environment is very robust and buyer friendly right now which the Sympazan transaction exemplifies. We’re able to acquire that asset for $15 million, including the milestone for the new patent. In the trailing 12 months ended September 30, Aquestive recorded $9.9 million in net sales. We’ve acquired an asset that is growing. We’ll soon have patent protection to 2039 and has gross profit margins very close to our corporate average for 1.5x trailing revenues. The refinancing was especially timely in this environment as this M&A environment continues to ripen and we now have the cash resources and balance sheet to add more products to the portfolio.

Source: CEO’s words, Q3 2022 earnings call [emphasis added by the author]

Assertio has a fairly diversified lineup of end-markets, each of which is a) growing quite well and b) of a size that may provide ASRT with a multiple of its current revenues.

| Metric/Market | Rheumatoid Arthritis | Migraine Drug | Pain Relief Medication |

| Research Agency | Market Research Future | Delvensight | Emergen Research |

| CAGR, % | 4.20% | 10.96% | 4.50% |

| Forecasted years | 2022 – 2030 | 2022 – 2032 | 2021 – 2030 |

| Market size, $B – final year | $85.9 | $21.85 | $79.68 |

Source: Author’s selection and calculations

From today’s perspective, I see no clear reason to believe that ASRT will return to its unprofitable years – there simply are not enough catalysts for that. Based on this assumption about the sustainability of current profitability, we can attempt to value the stock using a variety of valuation methods. Let us start with the DCF.

I expect last quarter’s top line growth (+10.39%, YoY) to continue through FY2023, but then slow to a modest 6% by E2026. I do this intentionally to keep my model conservative.

I expect the EBITDA and EBIT margins achieved to be maintained in FY2023 and even improve slightly from E2024 to E2026. The ratio of D&A to total revenue will fall to 25% in E2024 and remain at this level until the final forecast period.

I change the forecast ratios for working capital slightly compared to recent historical data to introduce a little variability into my model. CAPEX as a percentage of revenue has historically been below 1% – I expect CAPEX to remain slightly above historical averages.

To calculate WACC, I use the following inputs:

- risk-free rate of 3.5%;

- cost of debt of 15% (remember, ASRT is a small-cap pharma stock);

- market risk premium of 6%;

- tax rate of 20%.

The resulting WACC is 13%, which in my opinion is consistent with logic and even a little higher than the percentage given by Gurufocus [10.91%].

If ASRT’s FCFF grow by only 2% [Gordon’s g-rate] in the post-forecast period, the implied value per share is $6.3 per share, 65.8% above yesterday’s closing price.

If ASRT trades at 8 times EV/EBITDA in 2026 (slightly below the sector average), then the company’s fair value today is $237.7 million – 30.2% above the company’s current capitalization.

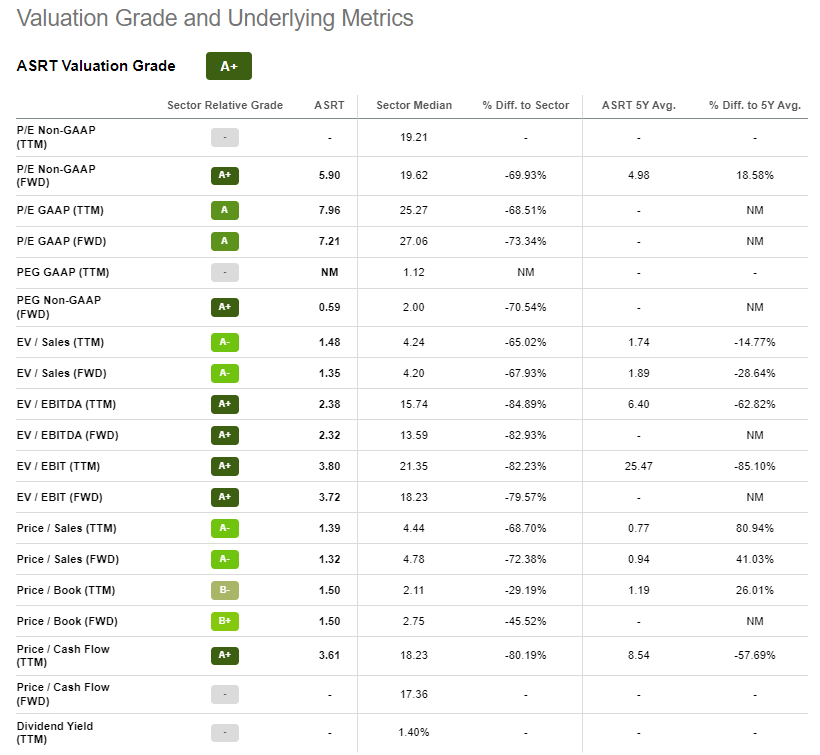

As for the relative valuation, here Assertio also looks too cheap to pass by.

Seeking Alpha, ASRT

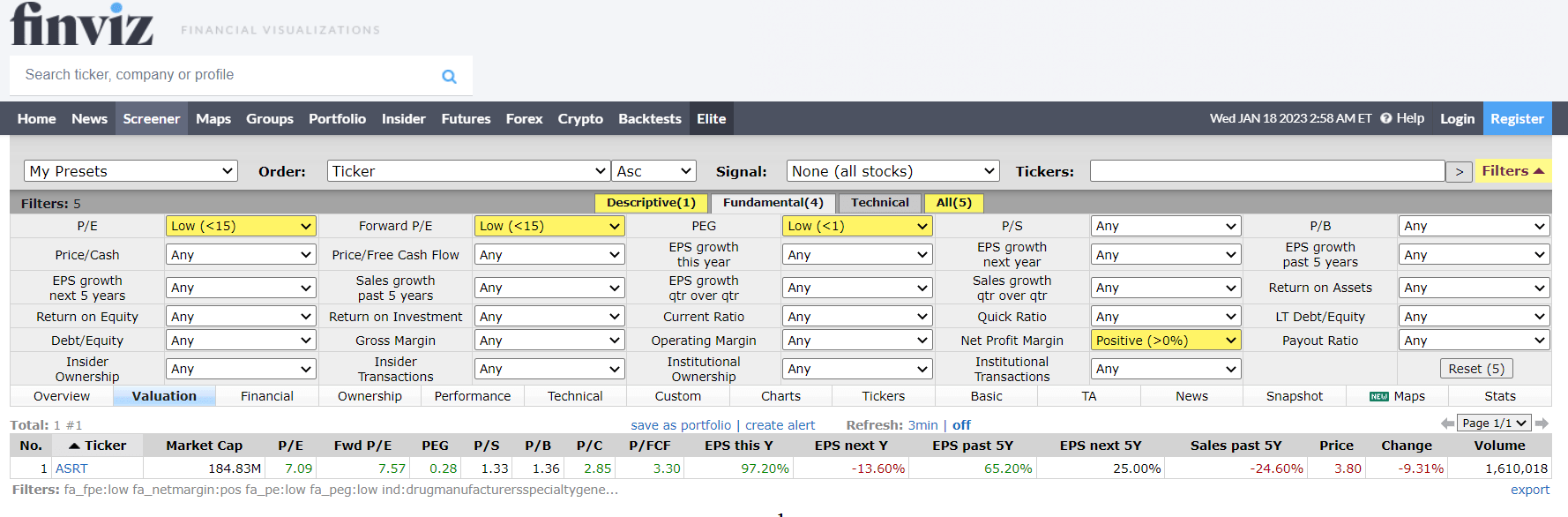

Assertio screens on FinViz as the only drug company [Specialty & General] with a PEG of less than 1x, a P/E and a forward P/E of less than 15x with a positive bottom line margin:

FinViz, author’s inputs

That is why I am talking about a still quite comfortable level of undervaluation for potential investors.

Bottom Line

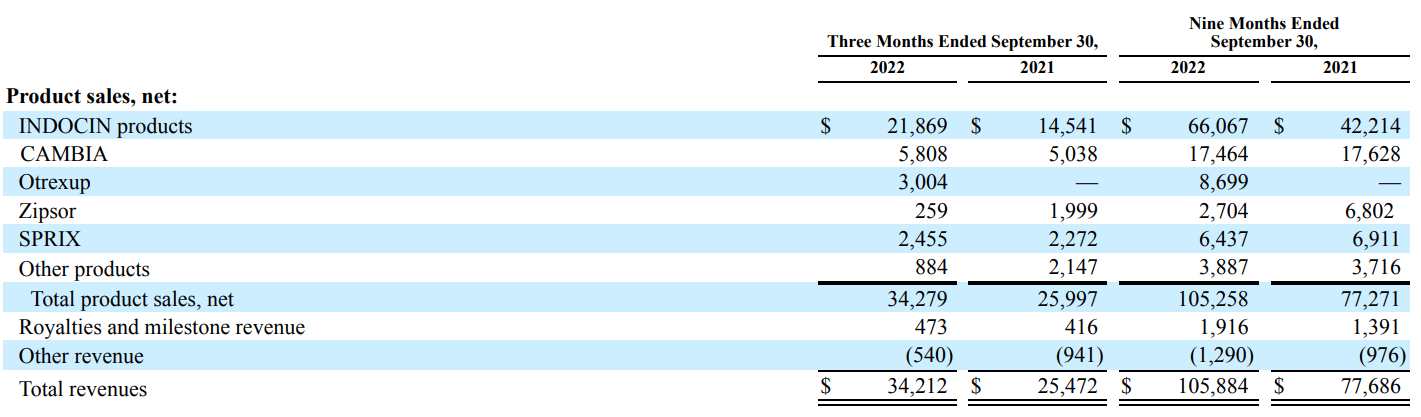

Before buying ASRT stock, everyone should be aware of the risks involved. First, the company is not immune to new litigation at some point in the future. Second, about 64% of the company’s total revenue comes from the sale of INDOCIN products – so the company’s real diversification is much less than its nominal one.

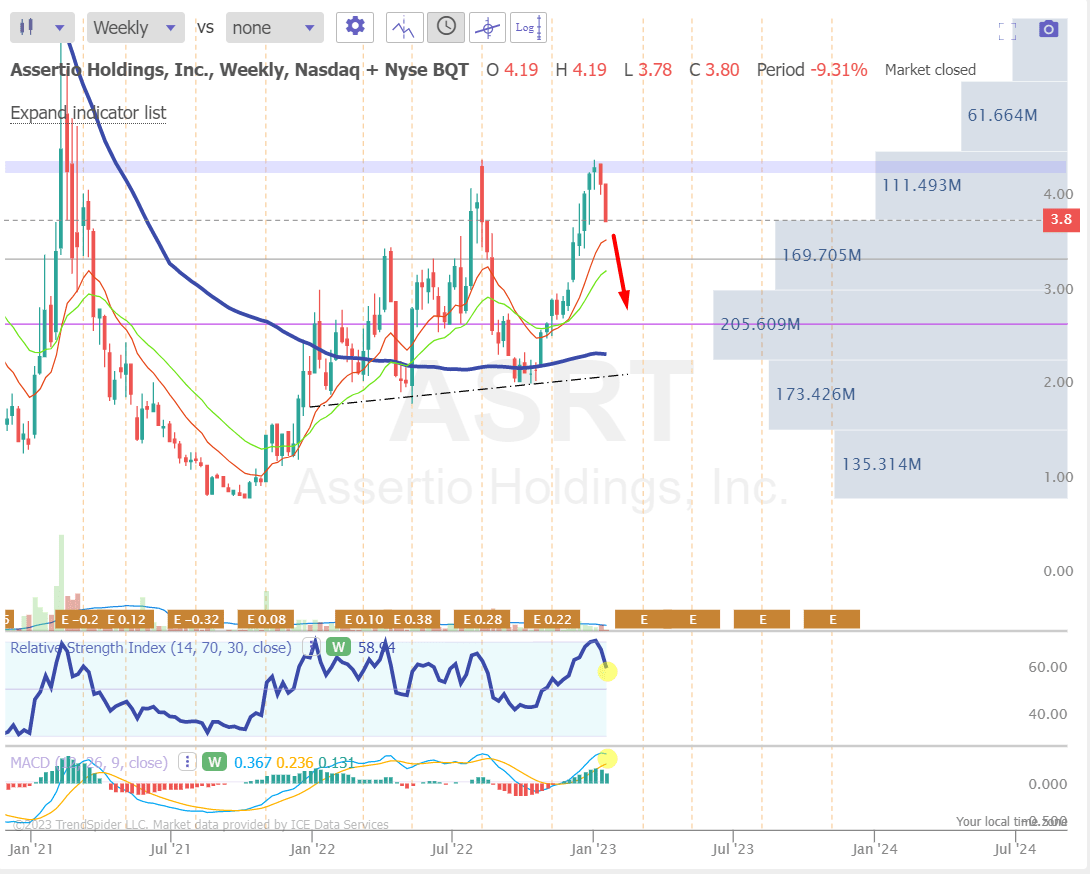

Third, ASRT is technically struggling to grow. On January 17, the stock fell more than 9% and bounced off its strong resistance level. This pullback has just begun, as shown by the weekly chart and the mean reversion seen on it:

TrendSpider, ASRT, author’s notes

This price action is ideally overlaid by seasonality, which has too little data for statistical significance, but nevertheless predicts a continuation of the decline [for the next week]:

TrendSpider, ASRT’s seasonality [4 years of data]![TrendSpider, ASRT's seasonality [4 years of data]](https://static.seekingalpha.com/uploads/2023/1/18/49513514-16740294801929314_origin.png)

However, the further ASRT falls and the longer its idiosyncratic risks do not materialize, the more attractive it becomes. My DCF model shows an upside potential of 30% to 60% in the medium term under fairly conservative assumptions. It is very likely that the actual potential is even higher. Therefore, I recommend you put ASRT on your watch list and consider buying this stock via a covered call or dollar cost averaging.

Thanks for reading!

Be the first to comment