Gonzalo Marroquin/Getty Images Entertainment

Our view

ASOS (OTCPK:ASOMY) is a UK-based e-commerce player focusing on fashion and cosmetics and targeting the youth segment (20-somethings) globally. Ironically, the company is massively out of fashion when it comes to investors, with the value of its shares down by more than 80% since the peak in 2021.

There are a number of recent headwinds which have given investors reason to be wary. These include slowing revenue growth, supply chain issues, and reduced full-year profit expectations. Add to that wider economic uncertainty and a relatively high operating cost base and we can see why investors are concerned.

Whilst there are genuine signals of a more challenging trading environment ahead, we think that the issues will ultimately be short-to-medium term issues and that the extent of the current sell-off is unjustified.

In our view, the fundamentals of the business continue to be supportive of the long-term investment case. Our reasons for this include:

- continued improvement in non-financial KPIs customers, orders, and average order values in recent years;

- continued double-digit revenue growth in the US as it pursues international expansion as a key driver of growth, in spite of signs of a slowdown;

- leveraging brand recognition and customer access through the acquisition of Topshop brands and the partnership with Nordstrom (JWN) in the US; and

- a liquid balance sheet and low leverage which will provide flexibility to see out a period of difficult trading.

Whilst we do see difficult trading conditions as a real possibility in the coming months or even years, we think the risk/reward trade-off at the current price makes a compelling opportunity for patient, long-term investors.

Investment context

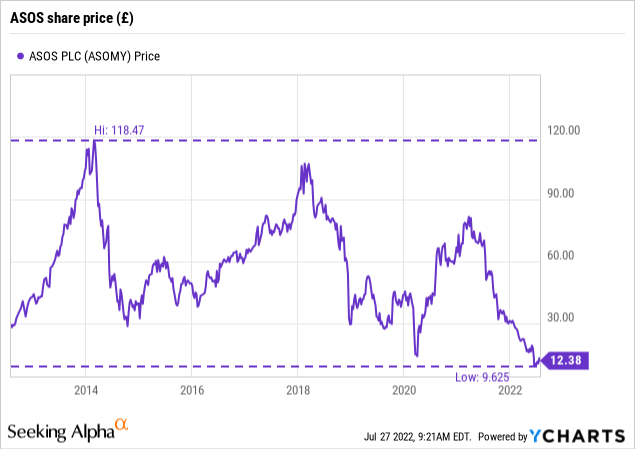

Since 2010, ASOS investors have seen the value of their investment decline by over 50% from peak-to-trough on three occasions. The most recent decline began in late 2021 before bottoming out in early 2022, with the price declining by more than 80% to around £8. Shares have rebounded by almost 30% since then, but at around £10 per share, it remains at levels not since 2021.

Company analysis

Growing revenues and profits

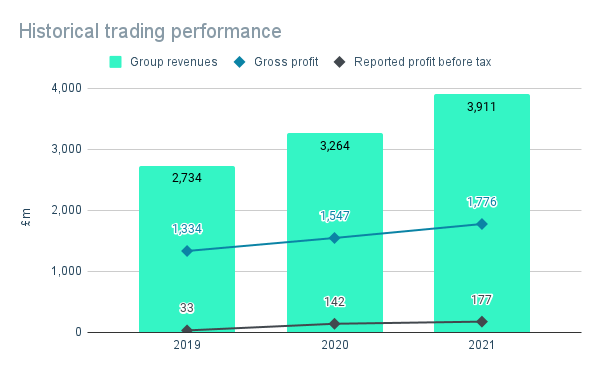

Author. Data from company reports

The volatile share price is not reflected in company’s trading performance. In fact, the company has demonstrated defiantly strong trading performance in recent years, with double-digit revenue growth and stable margins resulting in constantly increasing profits.

The strong performance in FY20 came in the face of unprecedented challenges brought on by Covid-19. Despite uncertain demand and supply disruptions, the company grew revenue by 20% and maintained gross margins in excess of 47%. Profits before tax (“PBT”) more than tripled to £142 million, albeit this included a Covid-related net benefit of £45 million, due to restrictions on product returns as a result of measures taken to contain the pandemic.

The growth story continued in FY21, with revenue up by a further c.20% and reported PBT up by 25% to £177 million. However, this also included a number of non-recurring costs and benefits such as the ongoing Covid tailwind and one-off costs related to the Topshop brands acquisition (see below). Excluding these, the company generated a PBT of £126 million, an increase of 30% from the prior year on a comparable basis.

Leveraging brand awareness

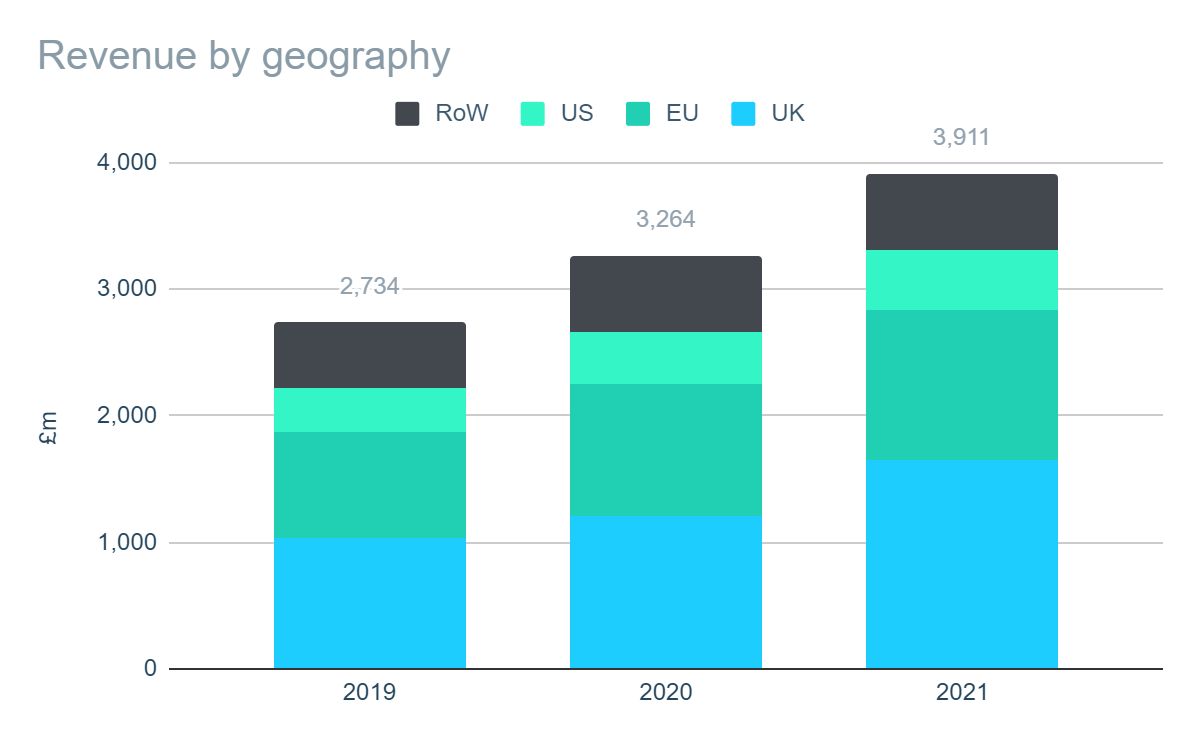

Author. Data from company reports

The company benefits from a global customer base, with more than 26 million active customers in over 200 markets. Despite the continued push for international growth, the UK continues to be its most significant market accounting for over 40% of sales. It has also been the most significant driver of growth in recent years, in both absolute and percentage terms.

Management hopes that growth, at home and abroad, will be accelerated by improving the company’s brand awareness – through both acquisition and partnership. In February 2021, the company acquired the Topshop brands from the failed Arcadia Group, for £286 million. The company hopes to leverage the existing brand recognition, which is particularly strong in the UK, US and Germany.

To further drive growth in North America, in 2021 the company entered a strategic partnership with Nordstrom, the US-based multi-channel retailer with more than 350 retail stores across North America. The partnership highlights the company’s steps to becoming a wholesaler as well as a retailer.

More, more, more

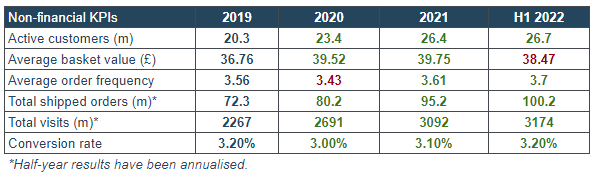

Author. Data from company reports

The positive momentum is not confined to the company’s financial performance, with the company’s non-financial KPIs (as selected by management) also showing continual improvement in recent years.

Since 2019, the company has almost continually attracted more customers, whore are willing to spend more on average, and are placing orders in increasing frequency. Even the H1 2022 results show continued improvement across almost all metrics, despite the headwinds faced by the company.

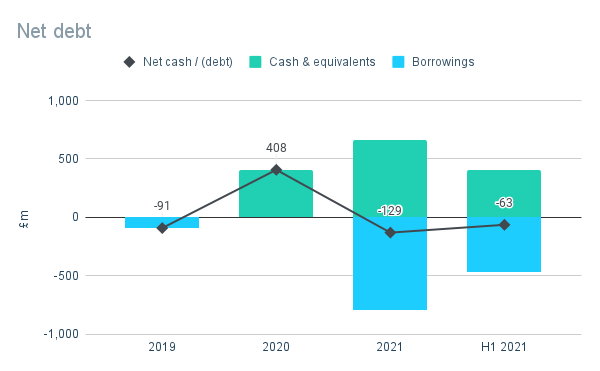

A lean and liquid balance sheet

Author. Data from company reports

The company has continually maintained a low level of net debt in recent years. In its half-year results for FY22, the company reported net debt of £63 million, representing leverage of around 0.5x EBIT for FY21.

Whilst this has been in part due to the company’s cash-generative operations, it also raised £239.4 million in net proceeds in April 2020 at the outset of the pandemic by way of a non-pre-emptive placing of ordinary shares i.e. a placing of new shares with a select number of institutional investors. The proceeds were used to clear the company’s limited existing debt and provide additional liquidity, should it be needed.

A year later, the company issued £500 million of convertible bonds with a coupon of 0.75% maturing in April 2026 as part of a refinancing program. The proceeds will mainly be used to fund the company’s global growth program but were also used to re-finance the acquisition of the Topshop brands. The initial conversion price was set at £79.65 per share, more than 6x above the current share price meaning conversion is unlikely to take place anytime soon.

The company also has ample liquidity with a Revolving Credit Facility of £350 million available in addition to its cash reserves of £407 million.

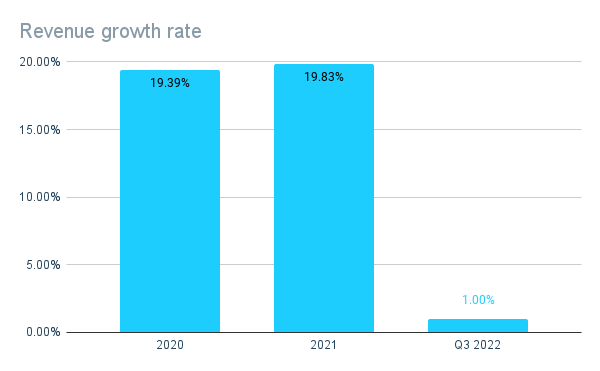

Signs of a slowdown

Author. Data from company reports

There were signs of a slowdown in the company’s Q3 trading update covering the 9 months ended 31 May 2022.

Group revenues for the 9 months ended 31 May 2022 were up 1% on the same period last year, a significant slowdown from the near 20% annual sales growth rates achieved in recent years. Management reported that whilst gross sales had increased, net sales had been impacted by the increased returns rate as the Covid-19 related benefit can finally be seen reversing.

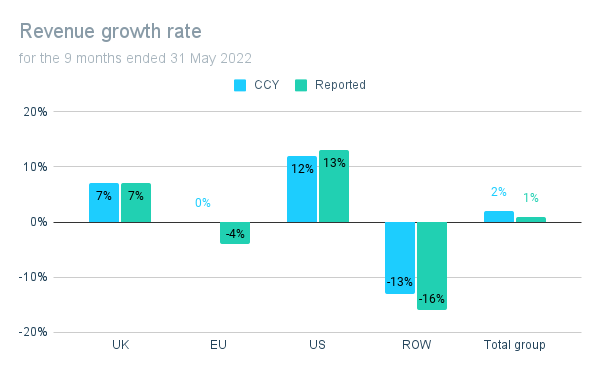

Author. Data from company reports

Despite the headline figures, things are not all bad and there are signs of continued progression across a number of areas.

The company continued its expansion in the US with double-digit sales growth, increasing by 12% in the same period last year. This is supported by the continued progression of the partnership with Nordstrom, with ASOS products available in more stores and an expanded product range available online.

And whilst sales in the EU and ROW were both down, this was in part due to adverse currency movements as well as the company’s decision to cease sales in Russia in response to the situation in Ukraine. Whilst these issues still ultimately hurt profitability, they do somewhat mitigate

Full year outlook downgraded

| FY22 guidance | Oct 2021 | Jun 2022 | Change |

| Revenue growth | 10% – 15% | 4% – 7% | Downgrade |

| Profit before tax (£ million) | £110 – £140 | £20 – £60 | Downgrade |

As part of the Q3 trading update, management also downgraded their guidance for the year to reflect uncertain consumer purchasing behavior and the potential continuation of higher return rates. Revenue growth is expected to be less than half the original guidance at 4%-7%, leading to PBT expectations being slashed to £20 million to £60 million.

As a result of lower profits and increased inventory levels, net debt is expected to increase to between £75 million-£125 million by year-end. At this level debt remains well within a manageable range even after factoring in lower earnings, representing leverage of 1.5x-2.5x estimated EBIT for FY22 (based on the lower end of management’s revenue growth estimate and the EBIT margin of 1.3% that the company achieved in H1 FY22).

Ambitious medium-term targets

The company continues to have medium-term targets of £7 billion of annual revenue and an EBIT margin of at least 4%, albeit the timeline to achieve these has been extended by a year to 2025/26.

Achieving these targets would mean almost doubling the size of the business compared to FY21 levels, equivalent to a CAGR of 15% – 20%. However, with a Total Addressable Market of £430 billion in the UK, US, Europe and core RoW territories, there is certainly room to grow, with company’s FY21 revenue representing less than a 1% market share.

Risks

We see the key risks to investors to include:

Inflation/economic conditions

The company is already reporting signs of slowing growth, adding that they believe this is before consumers have really started to feel the impact of inflation. Continued cost of living pressures could squeeze disposable incomes resulting in reduced demand.

Operational leverage

The company has high operating costs relative to sales resulting in relatively low operating margins, as highlighted by the 1.3% EBIT margin achieved in H1 FY22. As a result, the company’s profitability is sensitive to relatively small adverse changes in sales and/or costs. The impact of this risk will depend on the ability of management to reduce costs should a slow-down be experienced.

Fast-paced market

The company operates in a fast-paced market where consumer tastes and trends are subject to high levels of change leading to a risk that the company falls out of fashion. However, the breadth of the company’s product offering, its continued growth, and the positive trend in its non-financial KPIs suggest that it is able to continue to attract and retain customers.

Valuation

Our valuation approach centers around determining the true underlying earnings power of the business – or “owner earnings”. Whilst one should use ‘adjusted’ non-GAAP measures with caution, we believe that adjusted PBT represents a reasonable starting point in the case of ASOS.

As of 27 July 2022, the company’s shares trade at approximately £10 giving the company a total market cap of £1.03 billion. This represents a price-to-earnings multiple of 10x based on FY21 results. Based on management guidance for reduced profitability FY22, this increases to between 21x – 60x.

Nevertheless, we believe that the FY22 estimates reflect short-to-medium term headwinds which will ultimately subside and that the company’s longer-term prospects remain compelling. For that reason, we believe FY21 results are more representative of the company’s true underlying earnings power.

The company’s own medium-term plan is to achieve £7bn in revenue by 2024/25, with a minimum EBIT margin of 4%. Using this as a basis, we have estimated potential PBT to be in the region of £195m if these are achieved, reflecting a price-to-earnings multiple of just 5x versus the current valuation.

Should the company achieve its targets, we see the potential for a valuation in the region of £1.85 billion (based on an illustrative 10x earnings multiple). At this level, potential upside would be almost 90%, equivalent to a compound annual return of 24% if these targets are achieved by FY25. Even assuming these targets take two years longer than planned, it would still reward investors with a compound annual return of 14%.

Conclusion

Overall, we think the sell-off is overdone, and taking into account the relative risks and strengths, we assign a rating of “buy” at the current price.

Yes, there are signs of a slowdown, but it is important to view these in the context of strong sales growth in prior years and consistently strong fundamentals. A wider economic downturn remains a real possibility, but the company enters this period with a healthy balance sheet which will help see it through a difficult period.

Investors hoping for a quick rebound should stay away, but the fundamentals support the long-term investment case.

Be the first to comment