Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on November 4th, 2022.

Earlier this year, the Board of Macquarie Global Infrastructure Total Return Fund (NYSE:MGU) approved the reorganization of the fund into Aberdeen Standard Global Infrastructure Income Fund (NYSE:ASGI). This is expected to close in the first quarter of 2023. Both closed-end funds (“CEFs”) need to approve the closing of this deal before it can happen.

Today, I wanted to look more at what could be changing or not changing about ASGI before the merger. It also remains an attractive fund overall for investors looking to increase global infrastructure exposure.

ASGI Basics

1-Year Z-score: -1.64

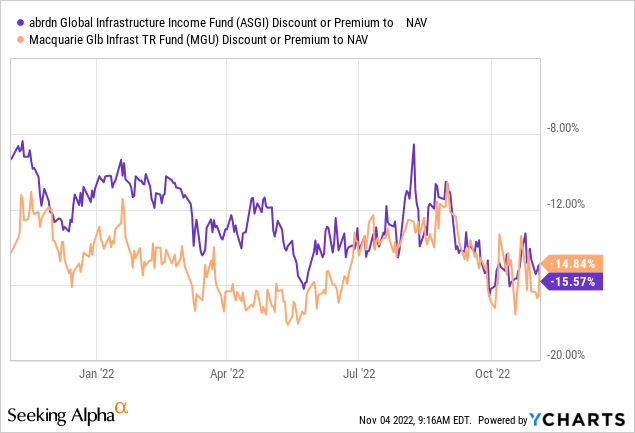

Discount: -15.57%

Distribution Yield: 8.73%

Expense Ratio: 1.73%

Leverage: N/A

Managed Assets: $173 million

Structure: Term (anticipated liquidation date around July 29th, 2035)

ASGI’s investment objective is “to seek to provide a high level of total return with an emphasis on current income.”

To achieve this objective, the investment strategy is quite simple. They will “invest in a portfolio of income-producing public and private infrastructure equity investments from around the world.” Interestingly, the most significant exposure in ASGI is to industrial stocks, making this fund a bit unique in the infrastructure space. However, utilities are right up there in terms of exposure.

MGU Basics

1-Year Z-score: -0.07

Discount: -14.84%

Distribution Yield: 7.29%

Expense Ratio: 1.82%

Leverage: 33.80%

Managed Assets: $467 million

Structure: Perpetual.

MGU has an investment objective to “provide investors with a high level of total return consisting of dividends and other income, and capital appreciation.” They intend to meet this objective by “investing at least 80 percent of its total assets in equity and equity-like securities issued by the U.S. and non-U.S. issuers that primarily own or operate infrastructure assets.”

They continue with “the Fund will also seek to manage its investment so that at least 25 percent of its distributions may qualify as tax-advantaged ‘qualified dividend income’ for U.S. federal tax income purposes.”

Performance And Portfolio Changes

With both ASGI and MGU at significant but similar discounts, there is not really a strong arbitrage opportunity to be made as a “backdoor” to enter ASGI. The main benefit here will be that ASGI will be a more sizeable fund. As it has below $200 million in AUM, ASGI is quite a small fund, so this is beneficial. Since the assets are similar, transferring over in-kind wouldn’t seem to disrupt the fund.

Ycharts

MGU is a leveraged fund. ASGI has operated – rather successfully in the current environment – without any leverage. MGU has performed best out of similar peers. Which is one thing that concerned me, because I was hoping ASGI would stay unleveraged. The good news is it turns out that MGU will be selling off around 30% of its portfolio prior to closing to pay back the leverage they have.

Q: Will there be any significant portfolio transitioning in connection with the Reorganization that impacts Fund shareholders?

A: It is anticipated that approximately 30% of the Acquired Fund’s holdings will be sold by the Acquired Fund before the closing of the Reorganization in order to pay back the Acquired Fund’s outstanding leverage.

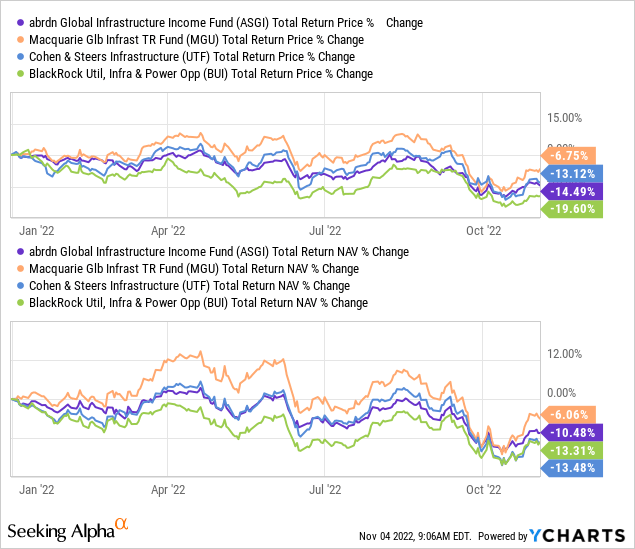

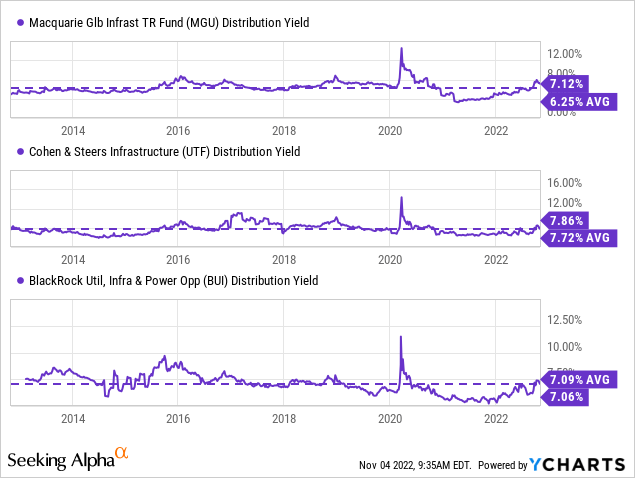

Here’s a look at the performance between some “peers.” However, it should be noted that all these funds have various and sometimes subtle differences, so they aren’t exactly the same. BlackRock Utilities, Infrastructure and Power (BUI), for example, utilizes no leverage but focuses on an options strategy. All four of these funds listed below do have an infrastructure and global focus, though.

Ycharts

One of the things that has helped MGU most is the heavier allocation to energy investments. Which is, yet again, another different tilt that makes the fund slightly different. ASGI does have some allocation to energy at around 7.6%, compared to MGU’s nearly 20% in energy infrastructure.

ASGI Management also anticipates that, following the merger, more of MGU’s assets will be sold off to realign the fund more into ASGI’s weightings. That should mean less energy and more industrial allocations.

Following the Reorganization, the Combined Fund expects to realign its portfolio in a manner consistent with its investment strategies and policies, which will be the same as the Fund’s strategies and policies. The Combined Fund may not be invested consistent with its investment strategies or abrdn Inc.’s investment approach while such realignment occurs. The realignment is anticipated to take approximately one week following the closing of the Reorganization, based on current market conditions and assuming that the Acquired Fund’s holdings are the same as they were on May 31, 2022.

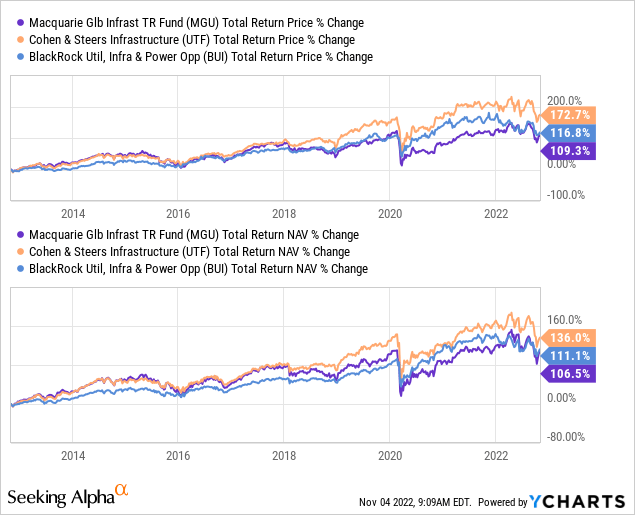

Over the longer term, this has hindered MGU’s performance. Particularly when looking at the performance in the COVID crash. I left ASGI off this longer-term look at total returns because it was only incepted in mid-2020.

Ycharts

The “special meeting” for ASGI will be on November 9th, 2022. Generally, these things are generally approved without issue. There really isn’t too much to decide since ASGI is essentially just gaining a larger base of capital. It isn’t like a company takeover where there is some sort of premium to the acquisition. Closed-end funds are merged on a NAV-for-NAV basis.

Distributions – Expected To Be Maintained

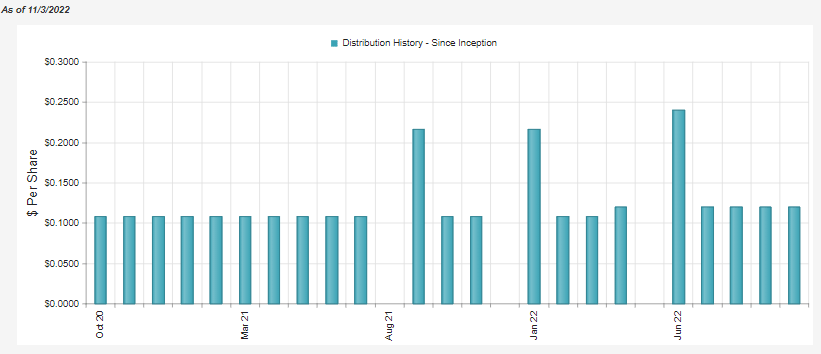

One of the main factors for considering a CEF is the fund’s payout. In this case, ASGI has paid out $0.12. This is expected to continue.

Q: Will the Reorganization impact Fund distributions to shareholders?

A: The Fund currently pays a monthly distribution of $0.12 per share. The Combined Fund expects to pay a monthly distribution of $0.12 per share, which is the same as the current monthly distribution of the Fund.

This is another one that generally goes without saying when a fund merges, they have typically kept the same payout. Again, since the fund’s assets have significant overlap, the income generation should be fairly similar, too.

Since ASGI’s launch, the fund has bumped up the monthly payout from the previous $0.1083 amount. The latest distribution rate comes to 8.73%, with a NAV yield of 7.37%.

ASGI Distribution History (CEFConnect)

MGU also bumped up its distribution earlier this year. As they are a much older fund, there have been several adjustments – both lower and higher – over the years. They had, for several years, run a relatively lower distribution yield compared to other funds, but this has become more elevated. This has made it more in line with the same peers we showed above.

Ycharts

Investors coming over from MGU will initially see a bump in their payout as they get shares of ASGI.

In looking at the coverage for ASGI, we covered that earlier this year. They haven’t reported a new report so that one remains the go-to for now. The new annual report should be coming in early December.

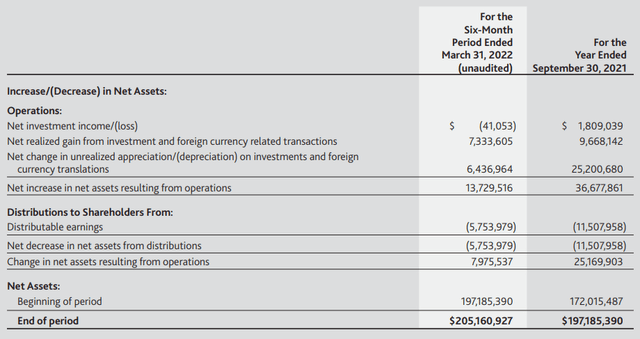

ASGI is particularly interesting when it comes to its coverage. They hadn’t produced any positive net investment income on the fund in the previous semi-annual report. This seems unusual because infrastructure companies are often associated with strong cash flows and payouts. That translates into CEFs holding these types of companies generating at least some NII.

Now, here’s the interesting part that most investors won’t like to see. They haven’t earned any net investment income in their last six-month report. NII is the dividends and interest received minus the expenses of the fund.

ASGI Semi-Annual Report (abrdn)

It isn’t odd to have an equity fund that earns most of the distribution to pay shareholders through capital gains. However, it is strange to see no NII for a fund with heavier exposure to utilities.

There are a few reasons for this, which leads me to believe it isn’t any concern. First of all, they’ve been able to grow the NAV, meaning they’ve been earning the distribution. That was quite easy for them, though, since they experienced basically a straight shot higher for the market for the first year after launch.

A second reason for the lack of NII is that the fund holds several larger positions in international names. International companies don’t generally put the same emphasis on regular dividends that U.S. companies do. Several of the names in ASGI’s portfolio pay semi-annual. The amounts are generally different for every payout too.

Finally, this is where the higher expense ratio comes to bite. That takes away from what NII there would be leftover for shareholders. Since it is higher than usual, that means a bigger chunk is taken away from shareholders.

Since that time, the NAV has fallen below the $20 inception NAV. This happened as the overall market headed lower, but also utilities have taken a hit more recently. This was after the utility sector was holding up relatively well.

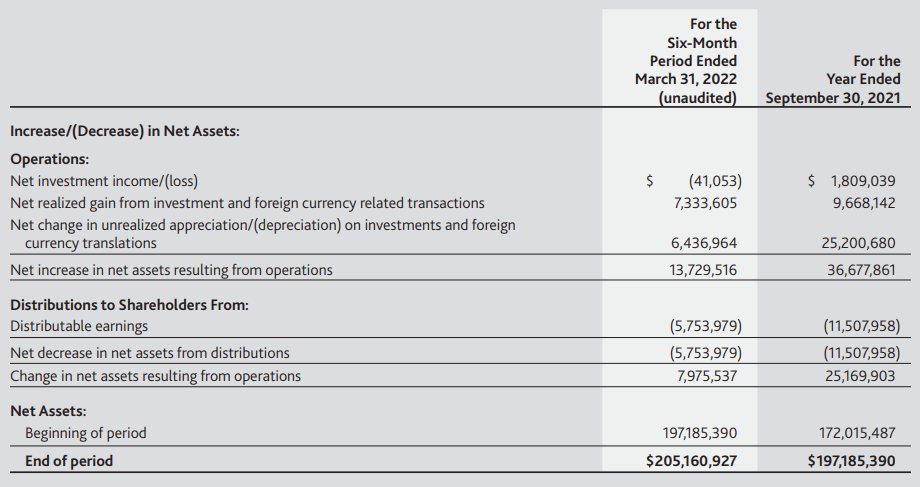

Additionally worth noting is that MGU has been able to provide NII. So it will definitely be interesting to see where NII falls after the merger. It will take some time for it to normalize as the portfolio is adjusted to fit the ASGI management preferences.

MGU Semi-Annual Report (Macquarie)

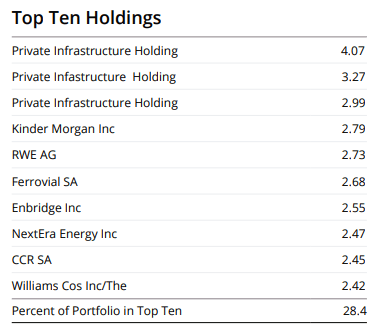

ASGI and MGU Top Holdings

As we know, both funds invest globally in various infrastructure plays. That’s what makes them similar. The largest component of ASGI’s portfolio is actually in private investments.

ASGI Top Ten (abrdn)

This is answered in the Q and A section of the special meeting announcement too. That ASGI will be reducing positions in MGU from their public allocation and investing further in private investments.

Sales and purchases of less liquid securities will take longer. Due to the increase in assets, and as a result of the relatively limited availability of infrastructure assets through private transactions (“Private Infrastructure Opportunities”), the Combined Fund will have a lower percentage of its total assets invested in Private Infrastructure Opportunities, and a higher percentage of its assets invested in publicly listed infrastructure issuers, following the closing of the Reorganization. The Combined Fund intends to make additional investments in Private Infrastructure Opportunities in accordance with its investment strategy following the Reorganization, which could take approximately 12 to 24 months. Based on the Acquired Fund’s holdings as of May 31, 2022, the Combined Fund expects to sell approximately 43% of the Acquired Fund’s portfolio following the closing of the Reorganization.

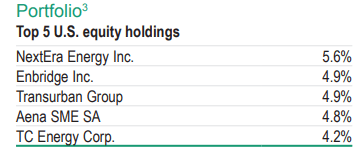

Here is a look at the top holdings for MGU at the end of June 30th, 2022.

MGU Top Five (Macquarie)

We can see that the two top holdings, NextEra Energy (NEE) and Enbridge (ENB), are included in the top positions of ASGI as well. That’s a significant amount of overlap right there. That could be why the fund anticipates selling approximately 43% of MGU’s portfolio, so they don’t become too concentrated in a select couple of holdings such as those two. Even if they are the best utility and pipeline plays in the world.

Conclusion

ASGI is set to become a larger fund starting in early 2023 after MGU merges into it. The portfolios are quite similar, but they still plan a fairly sizeable fund allocation once merged. Most notably, MGU is looking to deleverage before the merger, and ASGI will transition into a higher allocation of private investments. ASGI continues to look like an attractively discounted fund at this time.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment