RealPeopleGroup/iStock via Getty Images

Overview

Arko Corp. (NASDAQ:ARKO) has 18% downside. I am not advocating to short the company but to stay neutral since the short-term headwinds could possibly turn into tailwinds if fuel margin surges again due to macro factors that are outside of management control.

ARKO has demonstrated its ability to conduct value accretive M&As to grow the business as well as consolidate the industry. I believe the habit of visiting is here to stay, and with more introduction of food product to capture a larger share of wallet will drive further growth – which is what ARKO is doing.

I believe the right time to enter the stock is after valuation has re-rated further downwards and near-term headwinds are cleared.

Business description

ARKO through its subsidiary, GPM Investments LLC, is an independent convenience store (c-store) operator in the US and is the sixth largest ranked by store count.

More consumers patronizing c-stores

The convenience store industry is experiencing a continuous trend of companies focusing on expanding and bettering their in-store foodservice options. Convenience stores that provide food options like these may see an uptick in business from customers, because it is convenient. This could translate to higher revenue from the sale of both food and non-food items, as well as more people stopping in to fill up their cars. Currently, GPM provides a selection of hot and fresh foods, as well as pizza and other prepared foods, as part of its foodservice offering.

As opposed to developing its own in-house food service, GPM has traditionally relied on food franchises and in-store delis to attract customers. Due to its low market share in the proprietary foodservice sector, There is potential for GPM to expand its foodservice offerings and improve its profit margins by increasing its market share in the proprietary foodservice sector, given the shift in consumer preferences.

I also believe that investment in innovative digital tools to cater to customers’ ever-changing dining habits, such as contactless checkout and food delivery, will fuel the business’s expansion and increase its profits. This is based on my belief that consumers these days are digital savvy and prefer to interact with restaurants the employ latest technology.

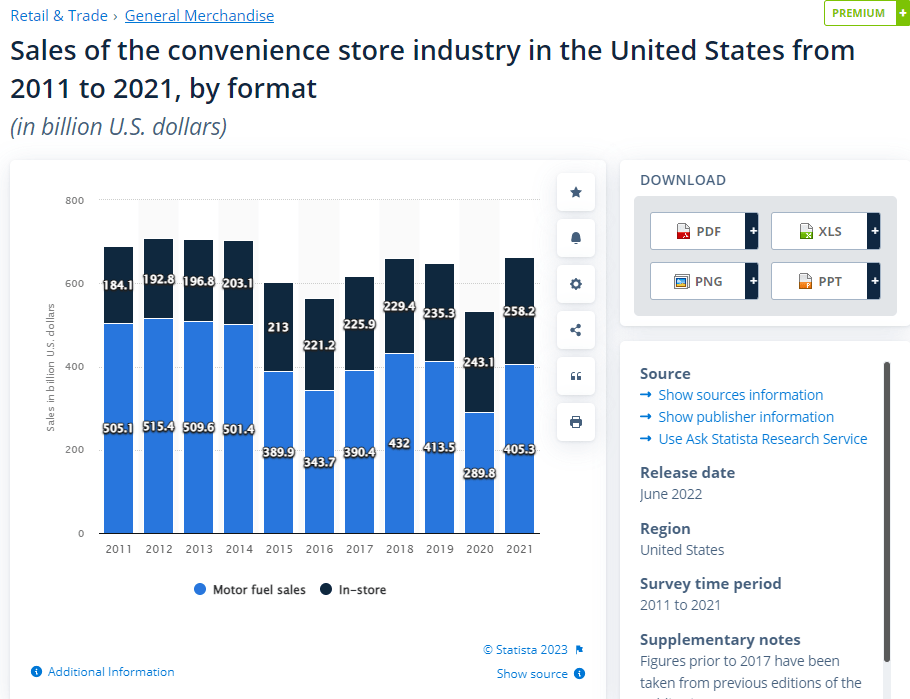

Resilient business model and industry

As evidenced by their classification as essential businesses during state-wide shutdowns caused by the COVID-19 pandemic, c-store in the United States has shown remarkable resilience in the face of economic downturns. Historical data corroborate this, showing that in-store sales have been remarkably robust over the last decade.

Statistsa

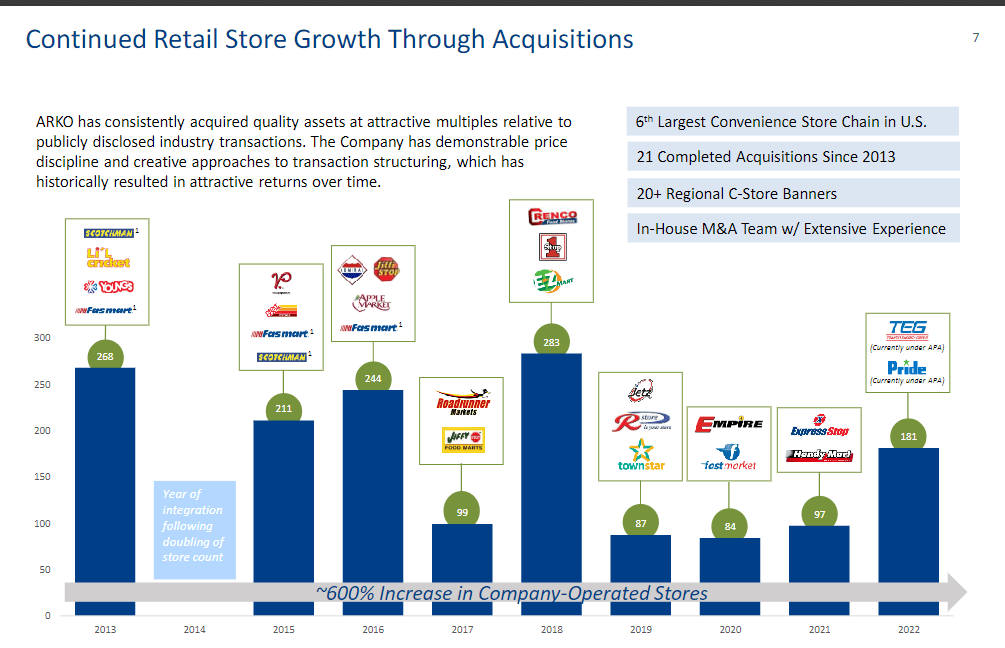

Fragmented industry means plenty of opportunities to acquire

In the highly fragmented c-store industry, GPM is a major and active consolidator. Through more than a dozen acquisitions over the past eight years, GPM has greatly expanded its store count.

3Q22 earnings

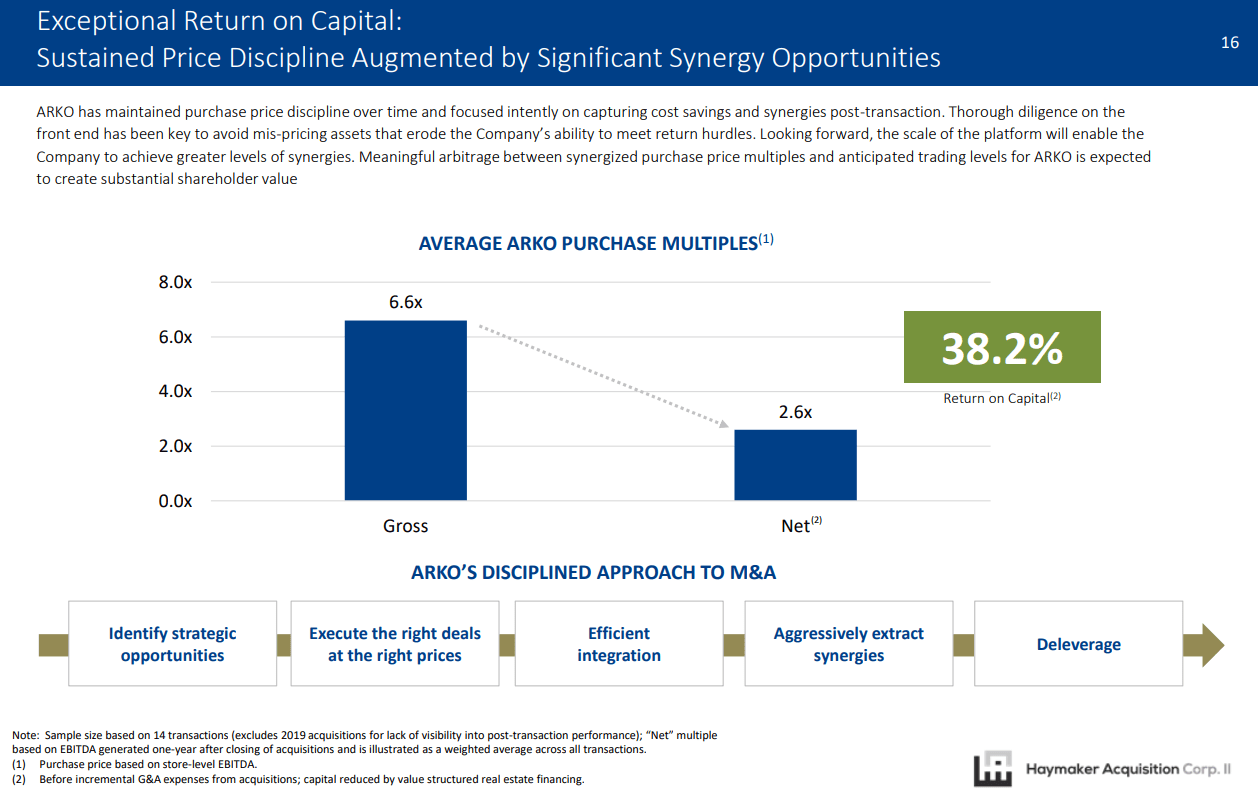

As a seasoned acquirer, GPM has proven time and again that it can achieve outstanding ROC, and significantly boost acquired brands performance after integration, thanks to its operational prowess and scale. I believe that GPM has achieved success in part due to its ability to maintain a strong market position through its scale advantage, allowing it to become a dominant player in the industry and a preferred acquirer.

SPAC deck

The top ten convenience store retailers in the United States make up less than 25% of the total store base, indicating that the industry is still very fragmented. Casey’s General Stores is the third largest chain in the United States, but it only has a small fraction of the stores compared to the top two. The vast majority of convenience stores are owned and operated by small, regional chains with a limited number of stores. Hence, I believe the market is poised for ARKO and other large players to continue consolidating the market through mergers and acquisitions.

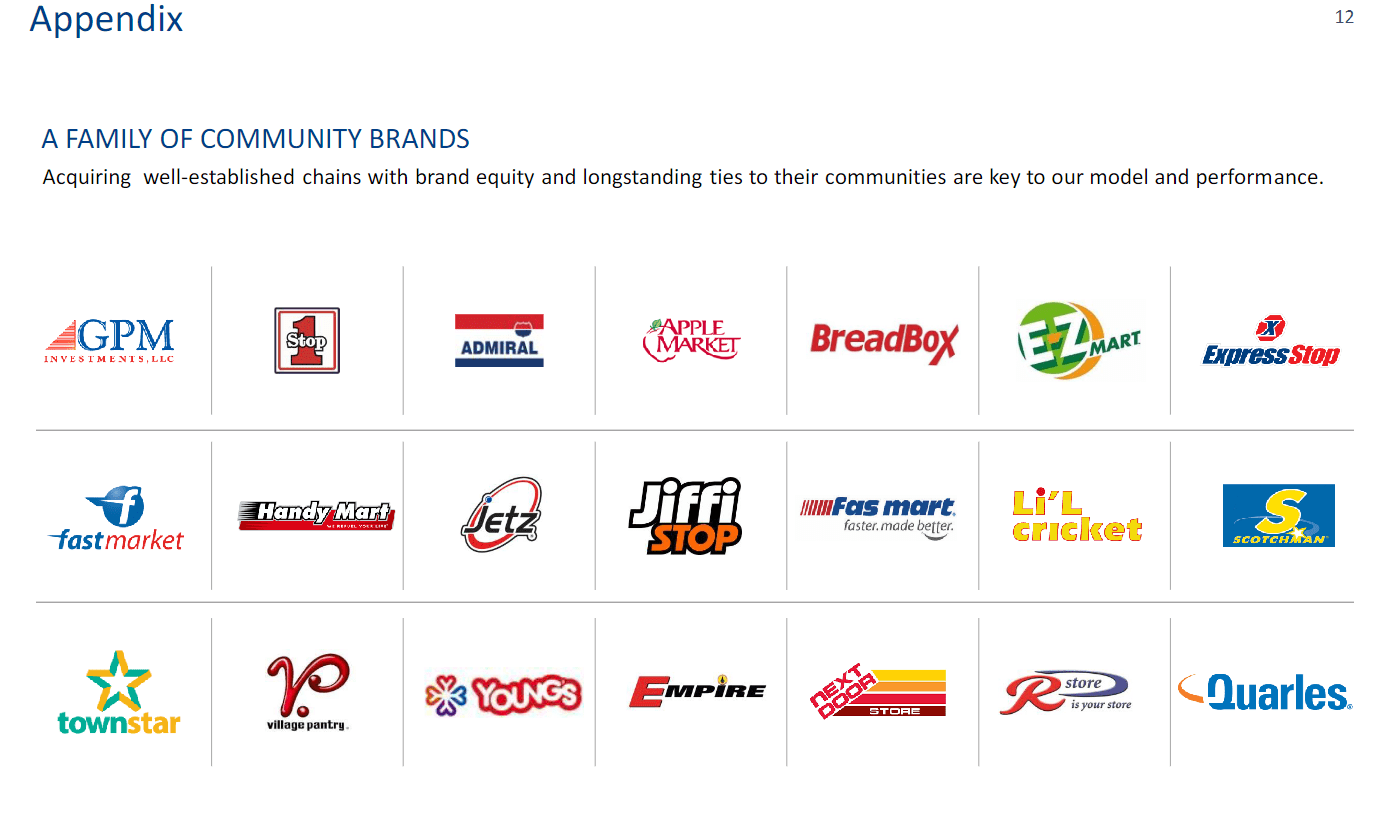

As of 3Q22, GPM had its stores operating under 21 different regional brand names. GPM has traditionally not rebranded a chain of stores after an acquisition, capitalizing on the patronage already established by the local name. I think this is a brilliant plan because it capitalizes so well on the already-established brand equity in its store banner portfolio. Rebuilding the brand, on the other hand, necessitates spending a lot of money on things like rebranding and renovations, in addition to a lot of time and effort. In addition, the brands GPM has acquired have each been around for at least half a century, making them well-known in the communities where they have operated for so long. Furthermore, all of GPM’s store brands benefit greatly from the company’s size, corporate infrastructure, and centralized advertising initiatives. This scale benefit grows from a virtuous cycle as the more brands/stores consolidates. For instance, it gains better negotiating power against suppliers, and also able to spread HQ administrative cost across a wider base of brands.

3Q22 earnings

Retail and wholesale

GPM’s acquisition of Empire is evidence of the company’s management team’s expertise in the field. With the help of this purchase, GPM was able to increase the size of its wholesale business by securing contracts with previously unaffiliated operators. As a result, its cash flow profile will be bolstered and diversified by its combination of retail and wholesale fuel portfolios. In my opinion, GPM’s model, which incorporates both convenience store retail and wholesale fuel distribution, will generate more predictable and varied revenue streams.

This would provide a competitive edge against competitors. is that GPM is able to reduce fuel margin variability through bulk purchasing of fuel, unlike many smaller c-store operators. In addition, the wholesale fuel business offers strategic flexibility to GPM, as it allows the company to potentially change the ownership model of underperforming company-owned sites by transferring them to consignment or lessee-dealer trade channels.

Forecast

The underlying secular trends for ARKO are positive. However, I believe near-term growth is going to be slowdown as I expect fuel prices to come down. This would have an impact on margins as well. While I believe ARKO margins should be cushioned by its retail and wholesale strategy, it retracts to pre-covid levels.

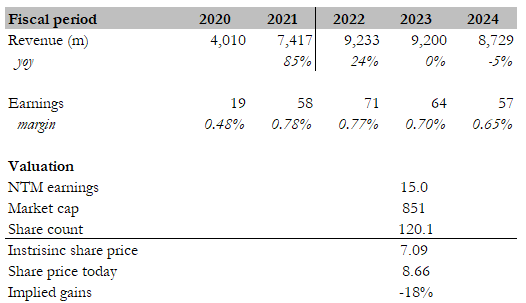

ARKO is currently trading at 15 times forward earnings. Given the expected near-term headwinds, I do not see any reason why valuation would re-rate upwards. With these assumptions, I believe ARKO is worth around $7.09 in FY23, or 18% less.

Author’s estimates

Key risks

Exposure to fuel price volatility

Retail fuel margins per gallon sold have a major impact on ARKO’s business. While I anticipate both total fuel sales volumes and fuel margins to be fairly stable over time, fuel margins are highly volatile and subject to change depending on a number of factors.

Past acquisitions record may not be reflective of the future

Even though ARKO has been successful at implementing its acquisition strategy over the past few years, this trend may not be sustainable. My concern is that management will stick with this growth-boosting strategy even if the deal is not financially beneficial.

Competition

As I was saying before, there are a lot of little players in this industry. This is great news for mergers and acquisitions, but it also means that the competition is relatively easy to enter. Everybody can open a convenience store and challenge ARKO if they have enough money and a good spot to put it.

Conclusion

The industry is experiencing a trend of companies expanding and improving their in-store foodservice options, which may lead to an increase in revenue from both food and non-food items. GPM has the opportunity to increase its foodservice offerings to capture this trend. Also, the highly fragmented c-store industry presents opportunities for GPM to continue consolidating the market through mergers and acquisitions, as it has proven to be a successful acquirer in the past.

I believe investors should wait till valuation gets cheaper before investing.

Be the first to comment