Marco Bello

Investment Thesis

We informed investors in a May article that applying a Hold rating on ARK Innovation ETF (NYSEARCA:ARKK) was appropriate as we needed to parse its bottoming process.

We are pleased to inform investors that ARKK had already formed its long-term bottom in May, even as the macroeconomic headwinds have worsened since then. Furthermore, the Fed is committed to maintaining its hawkish stance, as Powell hardened his inflation-fighting credentials.

Despite that, we believe the market is anticipating the possibility that the cadence of the “unusually large” rate hikes could give way to lower hikes moving forward. Critical commodity prices have also fallen way below their March highs. Also, port congestion has been easing progressively, leading to a marked fall in global freight rates over the past three months.

Therefore, we believe that the Fed’s hawkish rhetoric and rapid rate hikes have proved effective as a signaling tool to the market. Moreover, given the underlying strength seen in the US economy, some economists and strategists remain confident that a hard landing or full-blown recession can be avoided.

As a result, we surmise that the backdrop for speculative growth stocks is getting increasingly accommodative. Notwithstanding, ARK Invest CEO/CIO Cathie Wood’s investing decisions seem questionable at times, as we discussed in our previous article.

However, we believe exposure in ARKK offers investors an opportunity to participate broadly in speculative growth stocks without the need to take underlying exposure. As a result, investors could focus their attention on more predictable growth stocks in their portfolios and let Cathie Wood’s team do the heavy lifting in managing the speculative aspect of their portfolios.

Accordingly, we revise our rating on ARKK from Hold to Buy.

Speculative Growth Stocks Need A Less Hawkish Fed

We know the argument against speculative growth stocks. These long-duration symbols, with relatively weak profitability and high valuations, have lost their luster since early 2021. However, we surmise the battering seen in ARKK and its underlying stocks has also reflected the value compression as investors fled toward quality names.

Furthermore, investors had justifiably pointed out that the Fed’s hawkish stance is unfavorable for speculative growth stocks. Powell strengthened his inflation-fighting credentials at Jackson Hole as the market firmly priced in a 75 bps rate hike (86% probability as of September 9) at the upcoming September FOMC meeting. Furthermore, the Fed’s James Bullard weighed in on a 75 bps preference and suggested that the market consider a hawkish Fed for longer than it’s currently expecting. He accentuated:

While the consumer price index may show progress when it’s reported next week, I wouldn’t let one data point sort of dictate what we are going to do at this meeting. So I am leaning more strongly toward 75 at this point. I have felt Wall Street is underpricing the idea that inflation may just be relatively high, and it may take quite a while to bring [it] back to 2%. This would mean interest rates have to be higher for longer. That’s a scenario that is not garnering enough attention in today’s market pricing. – Bloomberg

Bullard has a point, and that remains the most significant risk to our thesis. Bloomberg reported that economists had reduced their inflation forecasts through 2023, signaling their optimism that the Fed’s tools should prove effective. Notably, these economists lowered their projections for YoY growth in the Fed’s preferred gauge, the personal consumption expenditures (PCE). The revised consensus estimates indicate a reduction of 0.1 to 0.2 percentage points for each quarter. The estimates suggest that the PCE should average 2.4% by Q1’24.

Therefore, it’s critical for investors to assess whether the market is right in its prognosis that the Fed’s hawkish stance could quickly bring down the elevated inflation rates. A near-term peak in the Fed’s position could pave the way for the medium-term recovery of speculative growth stocks. Investors should also remember that the market is forward-looking. Therefore, we might not need to wait until the Fed dials down its hawkish tone before ARKK recovers further.

We also believe the constructive price action in bond yields, and ARKK suggests that these economists could be right.

ARKK’s Bottom Is In Line With The Top In The 10Y Yield

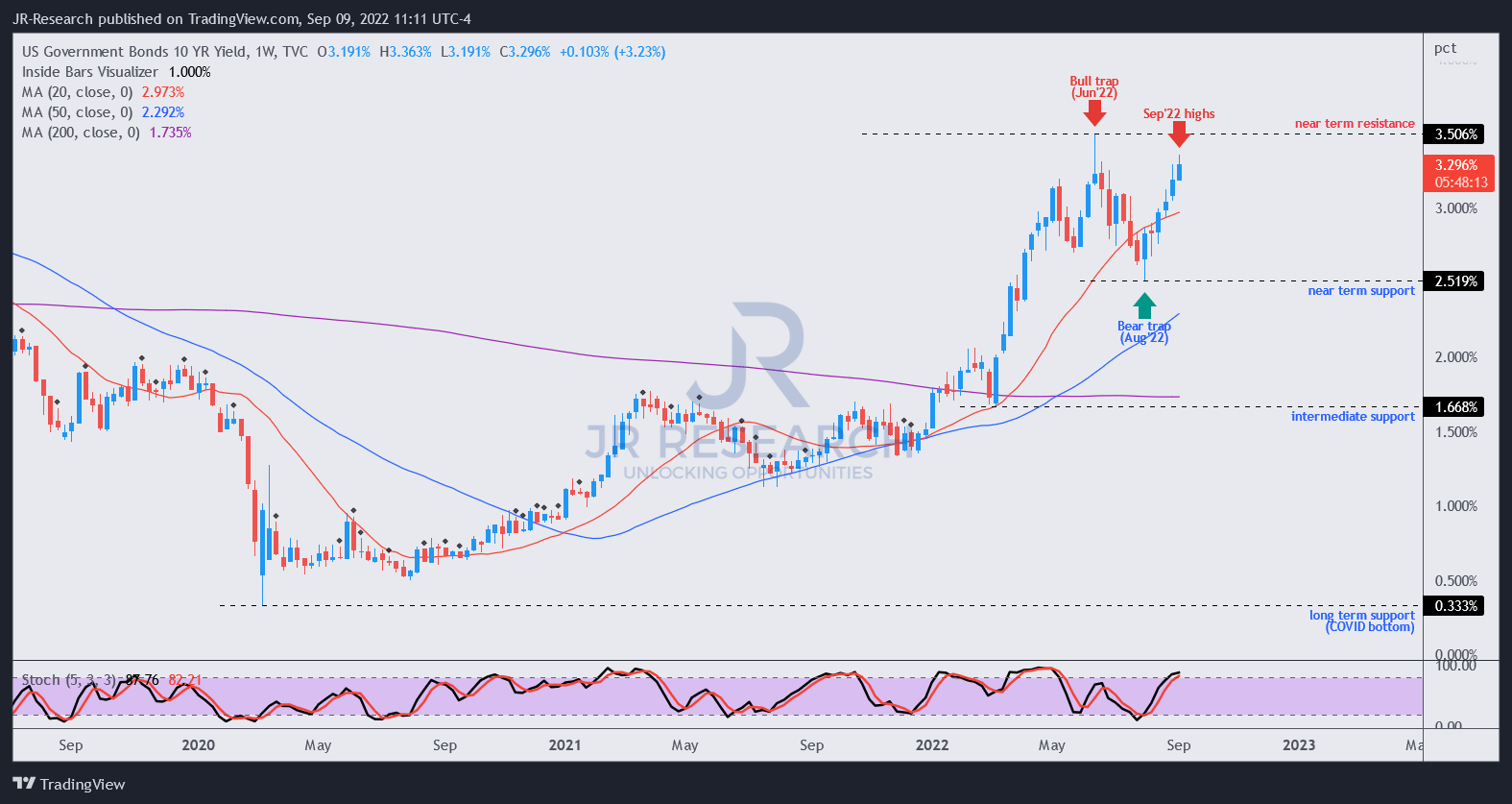

10Y yield price chart (weekly) (TradingView)

As seen above, the 10Y yield has likely topped out in June by a validated bull trap (indicating that the market rejected further upward momentum decisively). Interestingly, it also formed a bottom in early August, well ahead of the recent August highs seen in the SPDR S&P 500 ETF (SPY). We also updated members of our service in early August that the bond market’s price action could suggest a pullback in the equity markets, despite the robust summer rally in the SPY through August.

Hence, the pullback in the SPY didn’t surprise us. However, note that the 10Y yield’s rapid surge toward its recent highs has been met with selling pressure. We surmise that it is unlikely to sustain much further upward momentum, consistent with the price action seen at the SPY’s current levels.

Therefore, we are confident that the market has likely priced in peak Fed hawkishness, with yields expected to fall further moving ahead. As a result, a more benign environment in bond yields is constructive for a robust recovery in speculative stocks.

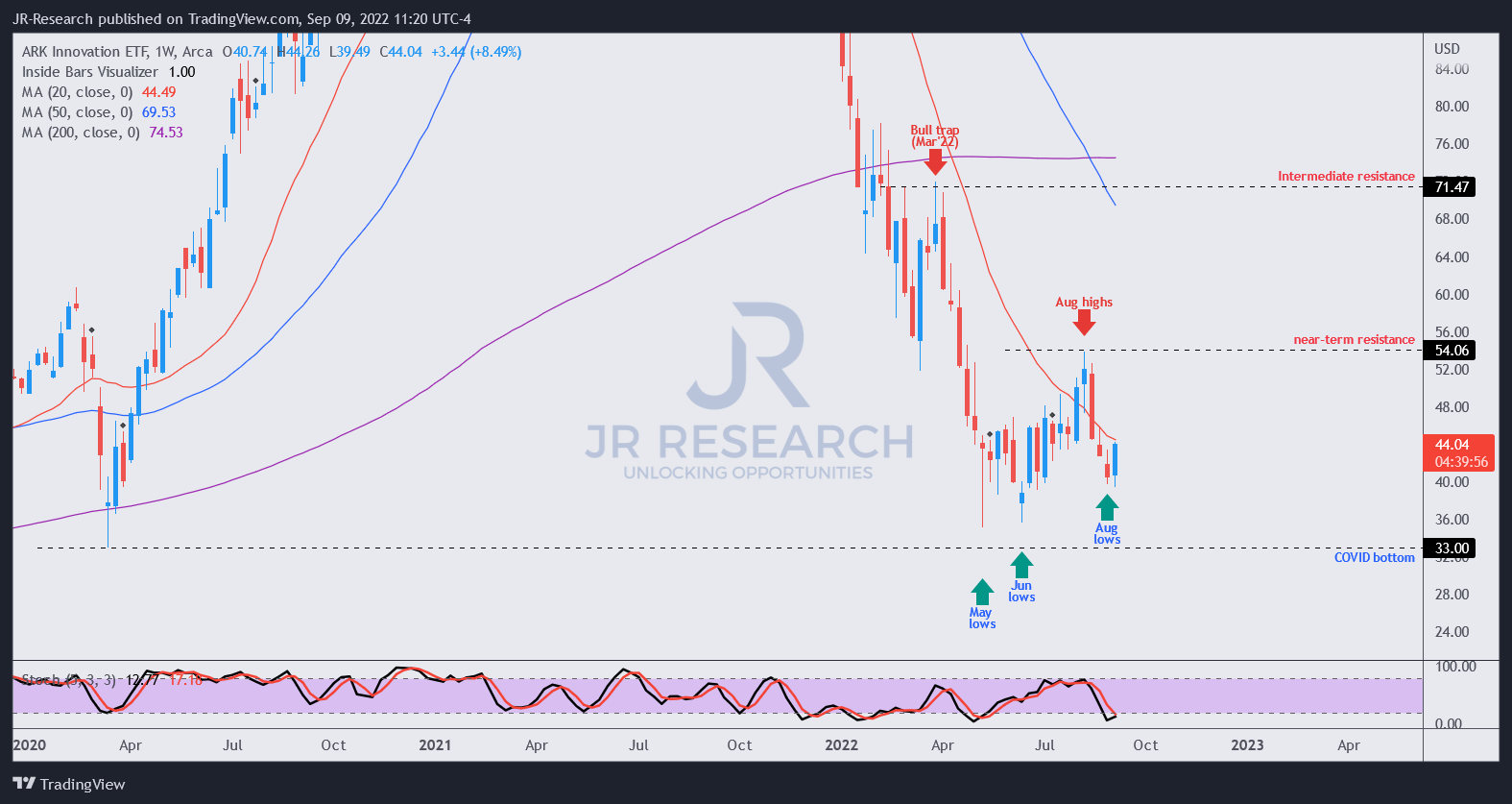

ARKK price chart (weekly) (TradingView)

In addition, we gleaned that ARKK has continued to base constructively over the past three months after its discernible May lows. Therefore, we postulate that the pullback from its August highs represented a healthy retracement, as its momentum is also oversold. Hence, ARKK needs to demonstrate resilient buying support, which is critical to spurring a recovery of its medium-term bullish bias.

Investors are urged to parse ARKK’s ability to retake its 20-week moving average (red line). We believe that ARKK’s accumulation phase with support close to its May lows suggests it’s on track to regaining control of its critical 20-week moving average decisively. Moreover, the recovery of it would likely stoke further buying sentiments, suggesting that the selling downside has been exhausted.

Therefore, we are confident that the underlying market momentum and macro indicators suggest that our thesis of ARKK bottoming out decisively is credible.

Is ARKK ETF A Buy, Sell, Or Hold?

While some of Wood’s past investing decisions were questionable, we believe her recent commentary on the impact of the Fed’s rate hikes is in line with what we observed in the market.

Wood’s recent commentary highlighted that “inflation is turning into deflation,” given the Fed’s aggressive stance to combat inflation. Fundstrat’s recent commentary also backed up her insights. It articulated that “inflation is starting to drop like a rock rather than a feather, leading to outright deflation in some areas of the economy.”

While Wall Street strategists are less aggressive in their posture, even JPMorgan (JPM) is increasingly confident that the market’s June lows would not be re-tested. It accentuated that it “still (sees) the prospect that continued evidence of peaking inflation data in the August CPI report can feed into improving sentiment for risky markets, which in turn can keep the market from fully re-testing the 3,636 June low.”

Coupled with constructive price action seen in ARKK, we are confident that we have seen the worst for ARKK.

As such, we revise our rating on ARKK from Hold to Buy.

Be the first to comment