martin-dm

Investment Thesis

Block (SQ), formerly Square, is a payments platform aimed at small businesses and has recently added a peer-to-peer digital banking app and now offers crypto and stock trading. Coinbase Global (COIN) provides infrastructure for the U.S. crypto economy and has over 100 million verified active users. DraftKings (DKNG) offers users multi-channel sports betting and gaming technologies in 17 countries.

These are three examples of the types of companies Cathie Wood targets with the ARK Fintech Innovation ETF (NYSEARCA:ARKF), which just recently broke even since its launch in February 2019. I believe that while ARKF offers tremendous upside potential, the thematic focus is more of a marketing gimmick that overshadows what this fund is: a high beta fund full of non-profitable stocks that requires an overly optimistic market to succeed. To support my thesis that ARKF isn’t worth owning, I’ll provide historical returns for 20 other thematic innovation funds and analyze how non-profitable and profitable stocks performed over 20+ years. In addition, I will contrast ARKF’s fundamentals with the Global X FinTech Thematic ETF (FINX), another leading Fintech ETF with over $600 million in assets under management.

ETF Overview

Strategy, Top Holdings, and Sector Exposures

ARK Invest’s website describes ARKF as an actively-managed ETF selecting companies it deems to be engaged in the theme of Fintech innovation, meeting one of the following two criteria:

- derives a significant portion of its revenue or market value from the theme of Fintech innovation

- has stated its primary business to be in products and services focused on the theme of Fintech innovation

Segments cited include Transaction Innovations, Blockchain Technology, Risk Transformation, Frictionless Funding Platforms, Custom Facing Platforms, and New Intermediaries. ARKF charges a 0.75% annual fee and, as of July 31, 2022, has net assets of $936.4 million. Typically, the ETF holds between 35 and 55 securities, but Wood’s approach is to focus on the highest conviction names in light of the market downturn, so there are currently only 30, excluding cash and equivalents. The top 20 are below, which total 91.96%.

ARK Invest

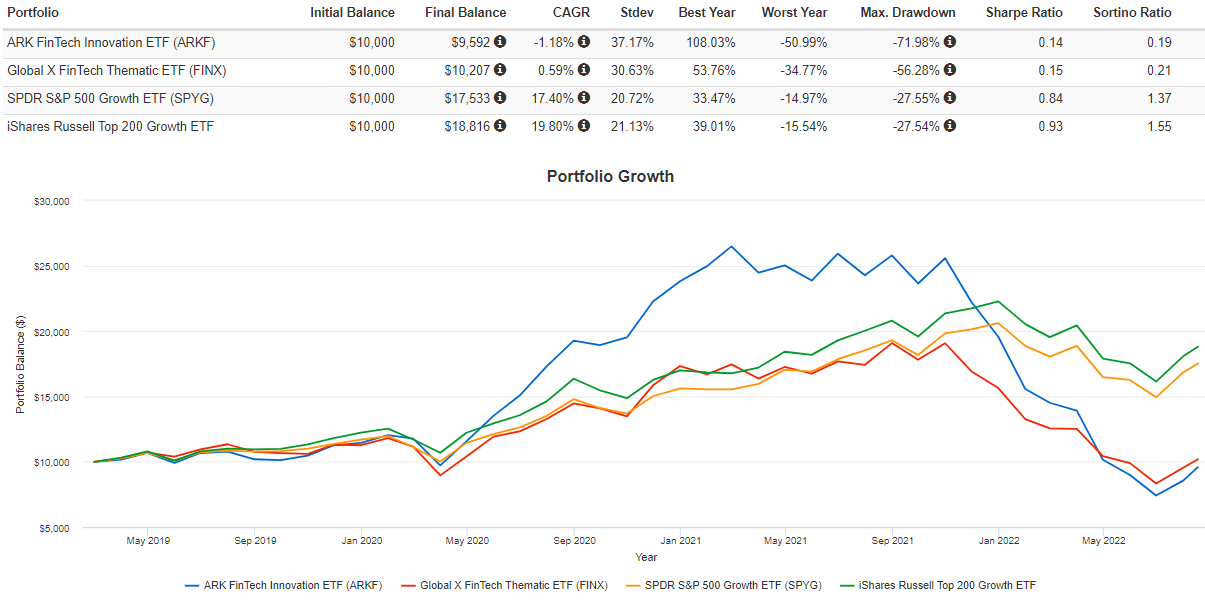

In addition to the names listed earlier, ARKF holds Shopify (SHOP), Twilio (TWLO), and Robinhood Markets (HOOD) are held in high concentrations. These three stocks are down approximately 75% over the last year, and I think they help illustrate the extreme risk investors take when they buy this fund. I often witness proponents of these types of funds scoff at pointing out short-term performance flaws, instead advocating for the bigger picture five or ten years later. However, that ignores the opportunity cost of not investing in other safer ETFs. One growth ETF I advocate for is the iShares Russell Top 200 Growth ETF (IWY), which is up 88% since March 2019 compared to a 4% loss for ARKF and has experienced about 43% less volatility.

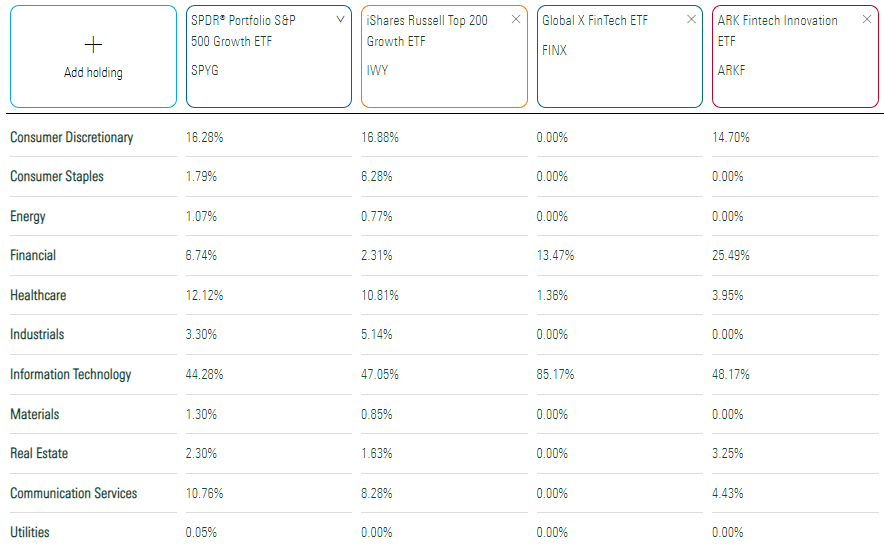

The following table highlights ARKF’s sector exposures compared to IWY, FINX, and the SPDR S&P 500 Growth ETF (SPYG). FINX is ARKF’s closest peer, also focusing on Fintech innovation, but has 65 holdings and passively tracks a rules-based Index with an expense ratio of 0.68%. You can see below that ARKF is more diversified on the sector level, while FINX has over 85% of its assets in the Technology sector.

Morningstar

Performance Analysis

The following graph highlights ARKF’s performance since March 2019 against the above three comparators. As shown, it’s down an annualized 1.18% (4.08% cumulative), but after including the partial-month returns from February 2019, it’s produced a slight 1.72% gain.

Portfolio Visualizer

“The Rise And Fall of ARKF” could have been a good headline for this article if the above chart is any indication. What was a relatively uneventful 2019 compared to its less-risky growth peers (IWY, SPYG), ARKF gained an astounding 108.03% in 2020. This wasn’t unique to ARKF, though. In my ETF Database, I track 34 non-single-sector-focused thematic-themed ETFs, 20 of which were launched before 2020. Look at how each performed in 2020, 2021, and 2022 YTD through August 17.

The Sunday Investor

The average 2020 gain was 82.83%, and 16/20 outperformed SPYG. Thematic investing was in style. I remember receiving documents from ETF providers calling for a new way of designing portfolios. Instead of traditional asset allocation among by sectors, it was suggested that investors construct portfolios capturing various themes using ETFs like ARKF. However, a quick look into the fundamentals of these funds’ constituents revealed the dangers of this strategy. Indeed, this sample group lost 2.46% in 2021 compared to a 32.01% gain for SPYG. They’re down another 22.59% in 2022 compared to a 14.97% loss for SPYG.

I quickly decided that thematic investing was primarily a marketing technique that encouraged investors to take on more risk than is appropriate and ignore fundamentals. Therefore, let’s look closer at ARKF’s fundamentals.

ARKF Fundamental Analysis

Descriptive Statistics

First, here are some quick statistics you might find helpful:

- Weighted-average two-year beta: 2.10

- Weighted-average market capitalization: $33.88 billion

- Companies that pay dividends: 3 (4.39% of total weight)

- Companies with negative operating cash flow: 8 (38.14% of total weight)

- Companies with negative net income: 18 (76.84% of total weight)

- Average price below 200-day moving average price: 22.66%

- Seeking Alpha Grades: Value (D), Growth ((C+)), Momentum ((C-)), Profitability (C), EPS Revision ((C-)), Quant (2.48/5)

- IWY Seeking Alpha Grades: Value ((D-)), Growth ((C-)), Momentum (B), Profitability (A), EPS Revision (C), Quant (3.37/5)

Historical Returns For Unprofitable Companies

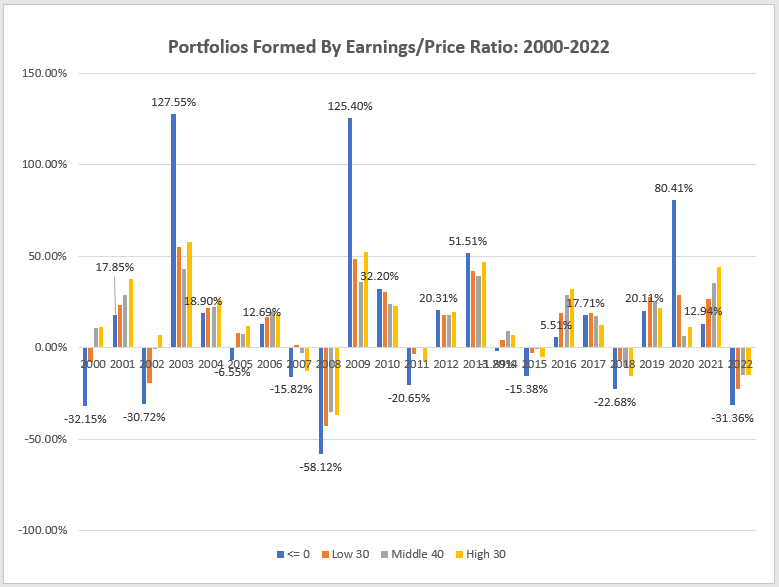

Not everyone values these metrics, but we can agree there’s a disconnect on profitability. This disconnect becomes essential when trying to understand the performance of an ETF like ARKF. The Kenneth French Data Library provides a wealth of information for portfolios formed on operating size, profitability, and valuations, among others. I chose to analyze the straightforward Portfolios Formed On Earnings/Price, which conveniently separates non-profitable stocks from profitable ones in the following four categories:

- <= 0: companies with negative earnings/price ratios (non-profitable)

- Low 30: the bottom 30% of companies with positive earnings/price ratios

- Middle 40: the middle 40% of companies with positive earnings/price ratios

- High 30: the top 30% of companies with positive earnings/price ratios

The graph summarizes the results for each category from 2000 onward for an equal-weight portfolio. I’ve also called out the data points for the unprofitable stocks (blue bars).

Chart: The Sunday Investor; Data: Kenneth French Data Library

As shown, the equal-weight portfolio of unprofitable stocks gained 80.41% in 2020, nearly matching the 82.83% average in the sample of thematic ETFs provided earlier. In 2013, the year preceding the launch of the ARK Innovation ETF (ARKK), the unprofitable portfolio gained 51.51% and likely provided a reason to create an ETF holding such stocks. That year, the First Trust NASDAQ Clean Edge Green Energy ETF (QCLN), one of the few thematic ETFs operating at the time, gained 93.91% compared to 32.60% for SPYG.

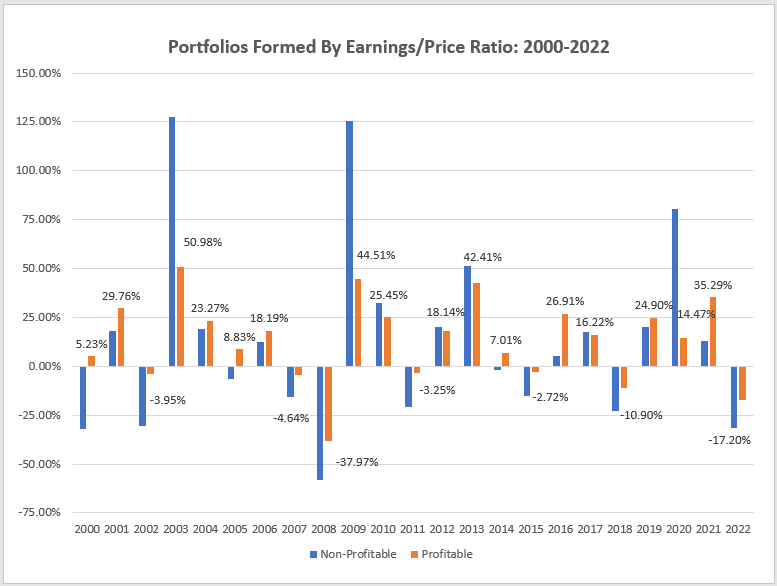

However, what’s most interesting is that in years when unprofitable stocks dominated (2003, 2009, 2020), the next year or two’s returns were always underwhelming compared to profitable stocks. Consider this simplified chart comparing the two, this time with data callouts for the profitable portfolio.

Chart: The Sunday Investor; Data: Kenneth French Data Library

As shown, there were only three years where the profitable portfolio lost more than 10%: 2008, 2018, and 2022. The unprofitable portfolio lost more than 10% in eight years. Furthermore, the average annual gain for the profitable portfolio was 13.52% compared to 13.38% for the unprofitable one. It begs the question: why take on the added risk? Portfolio managers who tell you to take the long view and think of where a stock might be in five or ten years are correct. Unfortunately for the proponents of thematic investing, the long view favors investors who insist on profits.

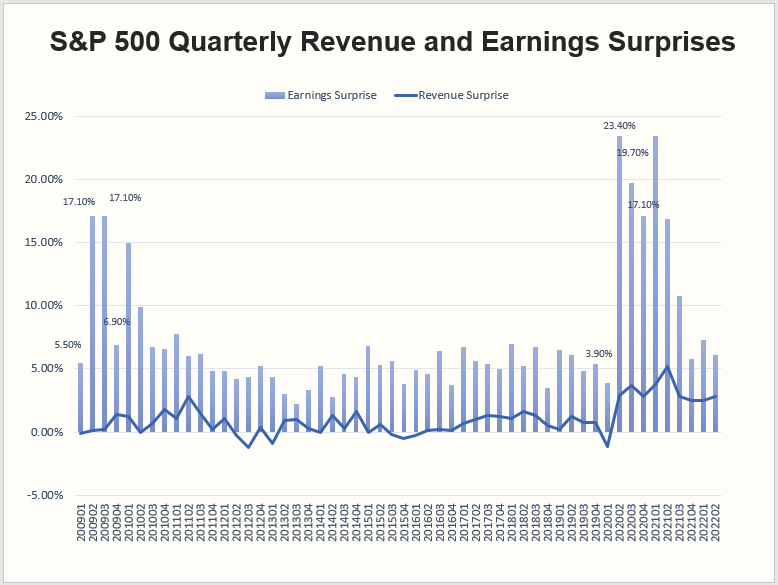

This leaves us with only short-term reasons to invest in unprofitable portfolios, hoping we can correctly anticipate a year like 2003, 2009, or 2020. It’s challenging, but looking at aggregate revenue and earnings surprises for the S&P 500 Index provides some clues. Notice the abnormally large quarterly earnings surprises in 2009 and 2020, reaching as high as 17.10% and 23.40%, respectively. The average since 2009 is 7.40%, and we’ve been below that for three straight quarters.

Chart: The Sunday Investor; Data: Yardeni Research

In my view, abnormal earnings surprises cause an excessive short-term movement in the price of a stock that tends to smooth out over the long term. The reverse is true, too. Recall the dot com bubble in the early 2000s, where unprofitable stocks lost a cumulative 44.60% from 2000-2002. The 127.55% rebound, one might argue, was inevitable. The same happened in 2008 when unprofitable stocks lost 58.12% but gained 125.40% in 2009. And it could very well be true again today. From January 2021 to June 2022, the unprofitable portfolio lags the profitable portfolio by 34.49%. That qualifies as abnormal to me, so I’m back to considering growth stocks again after about a year of favoring value.

Comparing ARKF with FINX

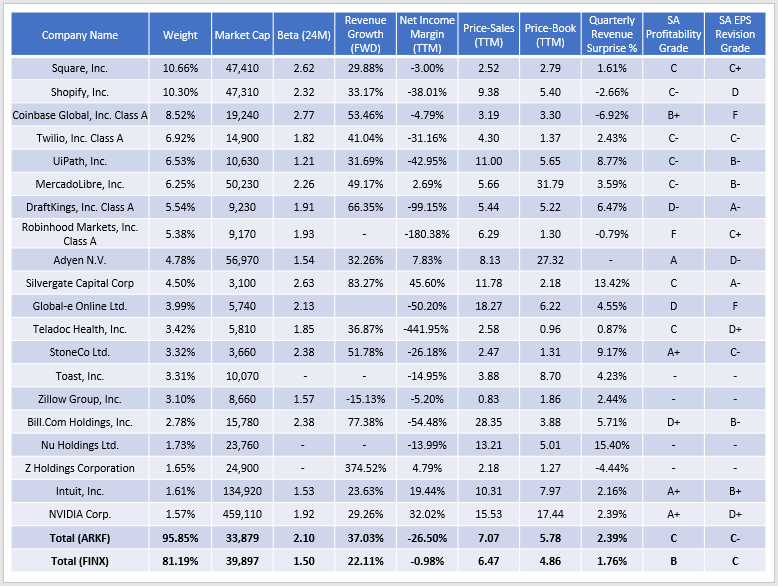

Finally, the following table compares selected fundamental metrics for ARKF with FINX. Please note that the weights listed are adjusted to exclude cash and three securities not in Seeking Alpha’s system: Discovery Ltd., Sea Ltd., and TCS Group Holdings. As a result, this analysis covers 94.16% of the ETF.

The Sunday Investor

This table demonstrates ARKF’s substantial growth potential, with many companies expected to grow sales by over 50% over the next year. However, many are still far from profitable, as the ETF has a weighted average -26.50% net income margin. FINX essentially breaks even at -0.98% and trades at lower price-sales (6.47 vs. 7.07) and price-book (4.86 vs. 5.78) ratios. Also, Seeking Alpha’s Profitability Grade confirms ARKFs is the less-profitable ETF. This grade is even worse than ARKK (C+), which is also less volatile (1.86 two-year beta), so ARKF may be poised for even more significant gains or losses, depending on your outlook.

Investment Recommendation

My issue with ARKF, and thematic ETFs in general, is that it is merely a collection of non-profitable, volatile stocks marketed in such a way to make the average investor believe it’s the way of the future. This article demonstrated that non-profitable stocks were hugely successful in the early 2000s and after the Great Financial Crisis. If ARKF existed back then, I’m confident it would have done exceptionally well, too. This article also proposed when extreme market sentiment occurs: after abnormally large earnings surprises. They coincide with the non-profitable portfolio’s most successful years. Still, with recent quarterly earnings surprises below the long-term average, I’m not seeing the necessary spark to make ARKF worth the risk.

To be clear, although speculative investing isn’t my approach, it doesn’t mean it can’t work. In fact, it worked very well in years like 2003, 2009, and 2020, and as long as the extreme volatility doesn’t bother you, there’s a solid chance you’ll end up well off in the long run. However, if you trust the thematic ETF managers who tell you to ignore the short-term noise and focus on the long-term, why not make it easier on yourself and insist on profitability first and foremost? Historical data shows that the average annual gain for an equal-weighted portfolio of profitable stocks was 13.52% vs. 13.38% for non-profitable stocks, with the added bonus of only losing more than 10% three times in over 20 years (compared to eight). That’s the most sensible approach and why I have plans to own this type of fund.

I hope you found this article helpful, even if you weren’t considering buying ARKF. Determining an ETF’s profitability is a great first step for any investor. As long as you remain reasonably well-diversified and don’t speculate too much, there’s no need to overcomplicate things with thematic ETFs. Thank you for reading, and I hope to answer any questions in the comments section below.

Be the first to comment