Deagreez/iStock via Getty Images

Ares Management (NYSE:ARES) has been on my radar for some time, given its durable income stream and high dividend growth. While I believe its long-term growth thesis is intact, it’s also important to recognize that everything is relative, especially in this market, where many stocks remain on sale. In this article, I highlight ARES’ recent quarterly results and evaluate whether if it’s currently a buy or hold, so let’s get started.

Why ARES?

Ares Management is a worldwide asset manager that’s been in business for 25 years, with over 2,300 employees spread across over 45 offices around the globe. Its three main lines of business include Credit, Private Equity, and Real Estate, and is the external manager for well-regarded investment companies such as commercial mortgage REIT Ares Commercial Real Estate (ACRE) and the largest BDC by asset size, Ares Capital (ARCC).

ARES just announced strong third quarter results, with over 20% YoY growth in assets under management, management fees, and fee related earnings, demonstrating the strength of its business model even as equity markets faced plenty of turmoil in the quarter. It appears that investors appreciate the lower volatility of ARES’ investment vehicles, as it raised an impressive $44 billion of new gross capital commitments so far this year and has $90 billion of available capital with a strong forward pipeline.

Moreover, ARES hasn’t experienced significant redemptions, with 88% of its AUM and 95% of its management fees being from either long-dated funds or perpetual capital vehicles with no set end date. This enables management to be patient investors and while waiting for opportune times (economic downturns) to make investments.

ARES is also somewhat shielded from economic downturns due to the fact that over half of its AUM is tied to credit investments, which sit at the top half of the capital stack. The remainder of the asset mix is set up for more upside participation with inflation, as noted during the recent earnings call:

Across the rest of our asset mix, we believe that our growing AUM and real assets with investments in real estate sectors with strong rent growth and an infrastructure assets that have built-in inflation escalators will be well-positioned to perform in the current market environment. We also believe that our private equity business is also differentiated with its focus on resilient, less cyclical, higher growth industries along with its flexible capital strategy of deploying assets across debt and equity in distressed and other opportunistic assets.

Turning to deployment, the current market environment is providing opportunities for us to continue to take market-share and be a consistent capital provider when other traditional providers and public sources are retrenching. Our significant dry powder and the flexibility of our strategy has enabled us to provide a variety of capital solutions to private companies or to play in liquid markets as relative value shifts.

ARES also carries a strong BBB+ rated balance sheet and pays a well-covered 3.2% dividend yield with a 5-year dividend CAGR of 20%. While ARES has many demonstrable positive attributes, it appears that the market also recognizes this, as it’s again trading towards the top end of its 52-week trading range. At the current price of $76.89 with forward PE of 23.8, the market is already baking in strong double digit returns in the near future.

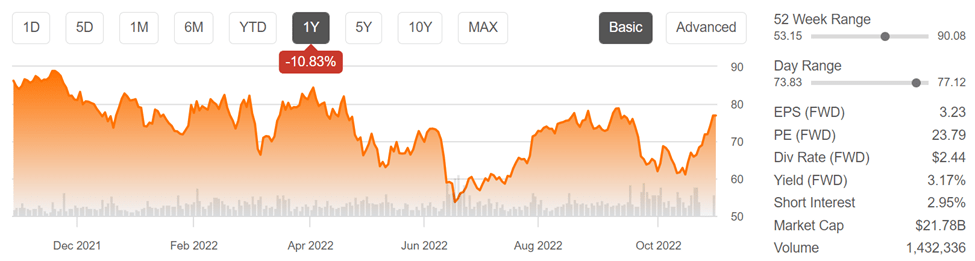

With the recent rebound in equity markets, investors may turn away from private alternative investments and back towards equities. Plus, near-term uncertainties around the economy may again drive ARES stock back down again, as can be seen in ARES’ trading pattern over the past 12 months.

ARES Stock (Seeking Alpha)

That’s why I view ARES-managed Ares Capital (ARCC) as being a better choice at the moment. ARCC is the largest BDC by asset size and is benefiting from rising interest rates. It recently bumped up its dividend by 12% and currently yields 9.8%. The new $0.48 per quarter dividend rate is covered by adjusted EPS of $0.50 during Q3.

ARCC also trades at just a modest premium to NAV at a price to NAV of 1.056. Some of this premium is due to NAV per share declining by just 1% in the recent quarter due to unrealized losses, and I would expect for these losses to recover after the economic picture brightens.

Investor Takeaway

ARES may be a wonderful alternative investment manager, but the market has also picked up on its quality, as it’s now trading at the top end of its 52-week range. While ARES may be a good investment in a normal economy, there are simply plenty of bargain priced alternatives at the moment. One such opportunity is ARCC (managed by ARES), which I view as a more attractive choice at the moment for income and potentially high total returns.

Be the first to comment