Editor’s note: Seeking Alpha is proud to welcome InSight Analytics as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

D. Lentz

Sky-high input prices caused by inflationary pressure took some industry players by surprise, while created opportunities for others such as Arconic Corporation (NYSE:ARNC) to tune into the tailwind. The company is a leading global manufacturer of aluminum downstream products for ground transportation, aerospace, construction, industrial and packaging applications. The firm’s operating segments include Rolled Products, Extrusions and Building and Construction Systems. Earlier in the year, the company was hit by elevated input prices, while falling economic indicators added up to the stock trading at a low valuation of 0.4x to Sales and 5.4x to EBITDA forward multiples.

While the energy crisis caused lower demand and higher costs in Europe, the company’s strategic verticals in North America remain resilient. I believe that Arconic could benefit from more favorable macro landscape, since most of its 21 production facilities are located in the US, and the lightweighting megatrend in automotive and aerospace, which is set to drive increased demand for rolled and extruded products. Let’s follow up to down to work it out why I’m bullish on this stock.

Impact of European energy turmoil and green transition

The worldwide flat-rolled products market is expected to rise on stable demand from the energy revolution and decarburization. Global industrialization, rapid urbanization and replacement of conventional metals with aluminum alloys will provide for solid growth in demand for the ”winged metal”. But the positive trends may not affect everyone, especially those businesses in the regions that are suffering relatively more from negative spillovers of the COVID-induced crisis and the ongoing hostilities in Ukraine.

Namely, European industrial companies are grappling with a combination of headwinds that don’t seem to go away anytime soon. Foremost among these problems are high energy prices, which forced the shutdown of some industrial production following Russia’s invasion of Ukraine. There is also the rising cost of achieving Europe’s green ambitions. This makes it difficult for companies when they face competition from countries with more and cheaper energy supplies.

Despite natural gas prices falling since end-August peaks, that shouldn’t be implicitly taken as good news. The depressed demand for energy in Europe is due to the fact that many factories are reducing their production owing to the high operational costs. Although an unusually warm October and forecasts of a mild winter have pushed prices down to €120/MWh, this is still around 6x of what companies overseas are paying. If Energy prices remain so high, this will make the industry players less competitive compared to manufacturers in the US, where there is an abundance of cheap shale energy. Moreover, reopening an aluminum smelter could cost up to €400 million and is unlikely given Europe’s uncertain economic outlook.

Concerning the energy transition, it will be a powerful growth driver in most base metals’ markets, which already include widespread uses. Aluminum is a key component of tomorrow’s technologies, from electro mobility, solar modules, wind turbines, electrical grids and batteries to aerospace and satellites. The high circularity feature of aluminum enables further decarburization due to significant reduction in GHG emissions and energy compared to primary production, and will exponentially increase the demand for aluminum products for the green transition.

Company overview and recent developments

Arconic came into being in 2016 as a result of corporate restructuring. Back then, Alcoa separated its bauxite, alumina, and aluminum operation into a new unit (with the same name). The remaining company continued operations in aluminum rolling, aluminum plate, precision casting, aerospace and industrial fasteners, and was renamed Arconic. Afterwards, in 2020 the company (Arconic) spun off its rolling products business into a separate unit, keeping its name, while the engineered products and forgings business remained in the existing company and changed its name to Howmet Aerospace.

Arconic has sold its Russian business (Samara production plant named Arconic SMZ) for $230 million. This was obviously not a good bargain, as in 2021, the revenue of Aronic SMZ amounted to $968 million, where the share of Samara plant in the total revenue of Arconic was 16%. The deal was closed after obtaining all necessary permits, as the company’s funds held in Russia were not available due to legal proceedings initiated by the Federal Antimonopoly Service of Russia. But, according to the current macroeconomic and political conditions, the deal appears to be a damage limitation.

As its core, Arconic is dependent on aluminum price volatility. The recent situation in the global aluminum market price seems to be not just a short-term surge as a result of the pandemic.

Aluminum price (USD/mt) (tradingeconomics.com)

Although the prices decreased to $2,400/mt levels since hitting record levels of over $3,500/mt in March 2022, the long-term nature remained and may appear now. Let me explain. The policy of the vast majority of countries in the world, aimed to reduce greenhouse gas emissions, encourages the consumption of raw materials necessary for the development of low-carbon technologies. Aluminum is not an exception, and as we mentioned above the metal is broadly used in solar panels, wind farms, electric vehicles and their infrastructure. The green trends will also lead to a reduction in production capacity using coal-fired electricity to power aluminum electrolysis, which could force aluminum in short supply. Thus, I believe the above may lead to a further increase in aluminum prices.

Financials

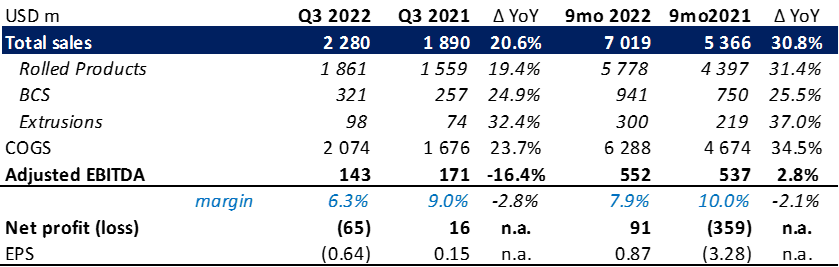

Arconic reported Q3 2022 revenue of $2.28 billion, up 20.6% year-over-year (YoY) mainly on favorable product pricing. Segment-wise, the positive performance was attributable to the Rolled Products business line, which accounted for 81.6% of the revenue mix, and marked 19.4% growth compared to year-ago quarter despite operational challenges and production outages. Building&Construction (B&CS) Systems and Extrusions business segments also registered double-digit growth of 24.9% and 32.4% compared to the respective quarter last year, and delivered a combine $419 million to the top-line.

Financial results in Q3 2022 (company reports)

Breakdown by end-markets revealed that volumes to the aerospace industry outperformed, showing off a 53% YoY surge, followed by sales to the packaging industry with a strong 24.6% YoY rise, as the can sheet operation at the Tennessee rolling mill increased up to the full capacity run rate levels. However, third-quarter adjusted EBITDA came 16.4% short YoY to $143 million where margin contracted 280bp to 6.3%. Bottomline, the company ended Q3 with a net loss of $65 million, or ($0.64) per share, compared to a net profit of $16 million, or $0.15 per share a year ago. Note, that third quarter of 2022 includes an after-tax, non-cash asset impairment charge of $70 million related to the Extrusions segment business review.

9-month revenue reached $7.02 billion, rising by 30.8% over the same period in 2021. Adjusted EBITDA for the period amounted to $552 million, still 2.8% higher YoY on solid H1 results. This brought net income for the nine months ended 30 September to $91 million, or $0.87 per share, compared to a net loss of $359 million, or ($3.28) per share in a year-ago period.

With the last quarter report Arconic updated its 2022 outlook to the downside, and now expects adjusted EBITDA to come in a $700-730 million range due to challenges at the Lancaster facility related to equipment upgrades. The company is also expecting $150 million free cash flow in 2022 due to significant reduction in pension contributions.

Long-term catalysts

The flagship here is the automotive industry, as the amount of aluminum used in car parts is rising every year. The growing demand for aluminum by the industry will be primarily associated with the need to lighten the design of the car as much as possible in order to increase its efficiency. Another promising area for the growth of the aluminum application is the development of high-speed railways.

The growth in aluminum consumption will also be associated with the development of electrical engineering and construction projects. The increase in the former would be driven by the spread of alternative energy projects and, in the latter, by the spread of green building standards and energy-saving technologies.

When it comes to aerospace, the demand for aluminum alloys for the industry should remain strong due to rapidly growing application of composite materials, underpinned by passenger traffic and build rates recovery.

Valuation

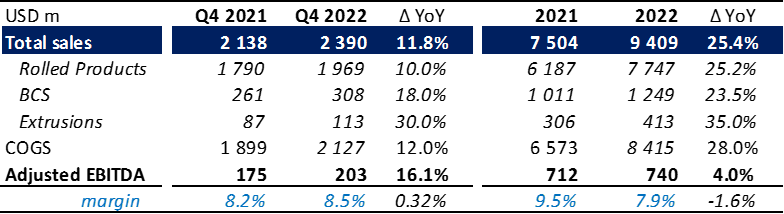

For reasons of determining a fair price of Arconic, I applied a comparable valuation approach. Taking into account the company’s outlook for 2022, my expectations for the fourth-quarter Net Sales and EBITDA, as well as full year readings are as follows:

Forecasts for Q4 and 2022 full year (company reports; personal estimates)

I assumed 25.2% sales growth in 2022 for the Rolled Products segment to be driven mainly by Ground Transportation end-market demand, as supply chain problems are alleviated, underpinned by strong demand in Aerospace, as major OEMs continue to ramp up production. Additionally, the operational challenges at Tennessee and Davenport facilities, which limited rolled production in the last two quarters, are resolved and should contribute to the segment’s performance. I also assume B&CS and Extrusions segments to register 23.5% and 35% increase. With the above expectations, total sales should be $9.4 billion and mark 25.4% growth in 2022. With an expected 28% COGS expansion, I estimated full-year EBITDA to stand at $740 million on a margin of 7.9%.

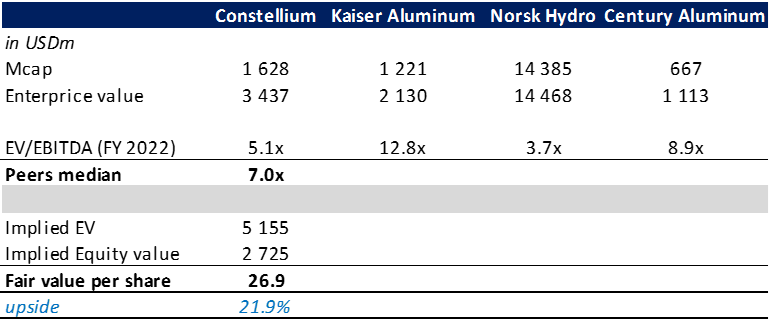

To the aforesaid EBITDA forecast, I decided to apply sector EV/EBITDA forward trading multiple, derived from Arconic’s main comps represented by Constellium (CSTM), Kaiser Aluminum (KALU), Norsk Hydro (OTCQX:NHYDY) and Century Aluminum (CENX).

Peers comparison valuation (seekingalpha data; company reports; author’s own estimates)

Summarizing the table above, ARNC is currently trading at a prominent discount to the peers median EV/EBITDA of 7.0x. Applying the latter multiple, the implied enterprise value should be $5.2 billion. With net of IB Debt and pension-related liabilities, the implied equity value per share should be close to $27 with potential of 22% to the upside. The way up would be backed by a new share buyback program of up to $200 million approved recently and set to last for two years. I believe the valuation is quite conservative amid the secular growth drivers, which alongside management’s commitment merely puts upside risk on my estimates.

Risk factors

The main risk relevant to Arconic represent production outages, which weighed on the company’s operating performance in the second and third quarters of 2022. Additionally, stagnation in the key end-markets due to recession fears could restrain the company’s future cash flows, while aggravation of the military conflict in Eastern Europe and potential sanction on the Russian imports of the metal would be a further source of price volatility and distortion of global aluminum trade flows.

Conclusion

I consider Arconic as a very attractive investment opportunity owing to its strong balance sheet, free cash flow generating capacity, attractive valuation and secular tailwind in strategic verticals which have put the company in the right position to capitalize from an economic rebound and drive future growth. I expect the company to gain market share, as the challenges outlined earlier puts Arconic apart from its overseas competitors. I also see a downside in continued supply chain disruptions and high input inflation causing demand uncertainty. Long story short, even considering the risks, I assign a Buy rating on ARNC and believe the stock has a significant upside potential.

Be the first to comment