In July, I wrote an article titled “Archer-Daniels-Midland (NYSE:ADM): The Right Way To Add Agriculture (Dividends)”. Back then, I highlighted why I was bullish on the company given market fundamentals and why the company is a great way to benefit from long-term growth in the industry through dividends. Since then, the stock has risen 11%, outperforming the S&P 500 by almost 10 points despite market weakness. In this article, I will reiterate my bullish call by using market fundamentals and the company’s own progress. Given the company’s strong performance and low yield, it’s important to assess the risk/reward, which may seem mildly unfavorable due to the low dividend yield. However, the company is doing a great job improving its business, which makes the valuation quite attractive.

So, without further ado, let us dive into the details!

ADM Hit A Homer – Financially Speaking

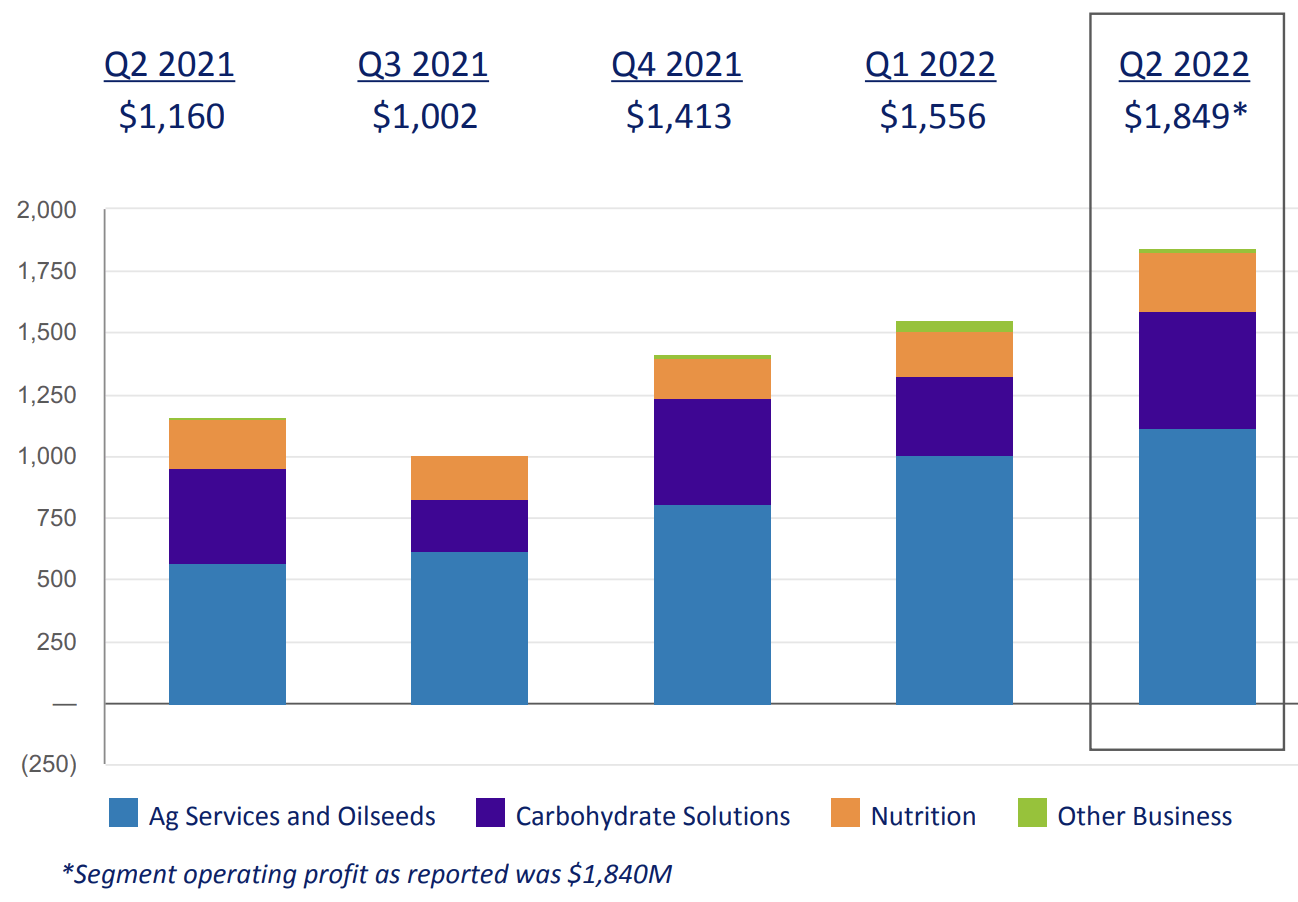

The chart below speaks volumes. In 2Q21, Archer-Daniels generated $1.8 billion in operating profit. As usual, most of it came from its agriculture services and oilseeds business. However, the most important thing is that the company did “only” $1.2 billion in operating profit in the prior-year quarter.

Archer-Daniels-Midland

However, before we dive into these numbers, let me quickly reiterate what ADM is all about for the readers who are new to this agricultural giant. After all, I think that even if people don’t trade or invest in ADM shares, knowing what ADM is all about is very important.

As I wrote in my last ADM article (I updated the numbers):

ADM is an extremely complex company engaged in all key aspects of the global food supply chain. This Chicago-based company was founded in 1902 and employs close to 40,000 employees. With a market cap of roughly $47.5 billion, it’s the largest company in the farm products industry.

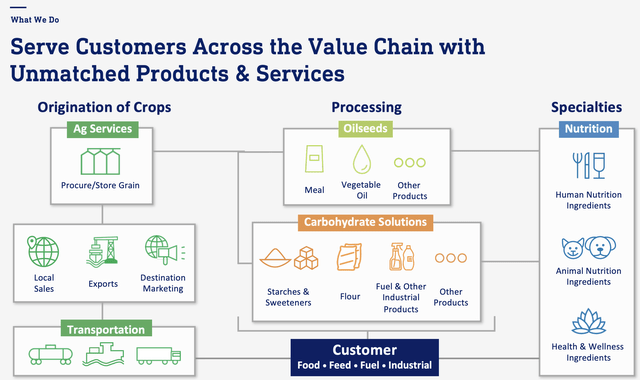

ADM operates a number of business segments.

Ag Services & Oilseeds (79% of 2021 sales)

Carbohydrate Solutions (13%)

Nutrition (8%)

Other (Negligible)

Ag services and oilseeds include operations that take place at the start of the food supply chain. These operations are related to the origination, merchandising, transportation, and storage of agricultural raw materials, and the crushing and further processing of oilseeds (soybeans, cottonseed, sunflower seed, canola, rapeseed, etc.). These products are used food, feed, energy, and industrial feedstock. This includes renewable diesel and more or less everything that comes to mind when thinking of food.

On top of that, the company owns the largest ethanol plants in the United States.

[…] The overview below shows the company’s business segments.

Archer-Daniels-Midland

As the first chart of this article suggests, the company is back on track, exploiting a very strong agricultural bull case. Its 2Q22 earnings were blowout earnings. Adjusted EPS came in at $2.15, a whopping $0.43 higher than expected. Revenues jumped by 19% to $27.3 billion. That’s $2.4 billion higher than expected.

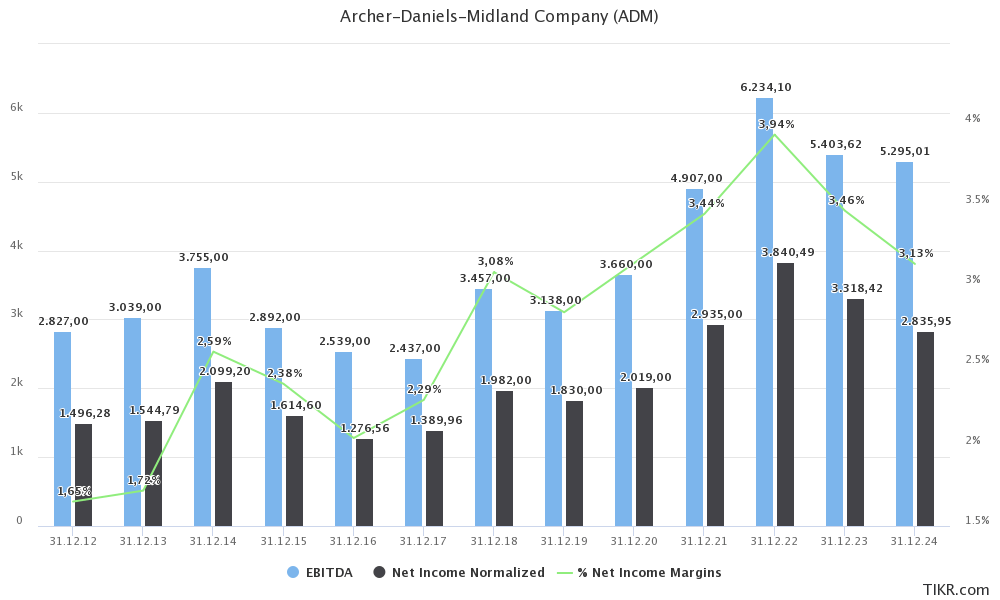

As the chart below shows, the start of the inflationary agricultural bull market in 2020 has pushed ADM to a whole new level of profitability. This year, net income is expected to reach $3.8 billion with a net income margin close to 4.0%.

TIKR

The company also saw a steep increase in its adjusted return on invested capital, which rose from 8.7% in 2Q21 to 11.6% in the most recent quarter.

On top of higher sales, the company benefited from modernization projects like its Minnesota corn facility in Marshall, which is unlocking significant new value through automation, new control systems, and advanced analytics. The company is seeing double-digit returns on investments made to streamline its labor and capital-intensive operations.

With regard to agricultural developments, the company sees strong export volumes thanks to high global demand. While the rate of growth is set to slow, I expect global agriculture tailwinds to be persistent. The other day, Bloomberg ran an article, citing long-term food problems, which are still mounting around the world. According to the article:

Everywhere you look, nations are grappling with a vast range of food ailments.

In the US, bakers are being squeezed by the worst ever flour inflation. In the UK, the price of an English breakfast is getting out of reach for more and more people. And in Europe, tomato growers and beer brewers are facing shutdowns and production cutbacks as the region’s energy crisis spills over beyond the utilities and energy-intensive sectors.

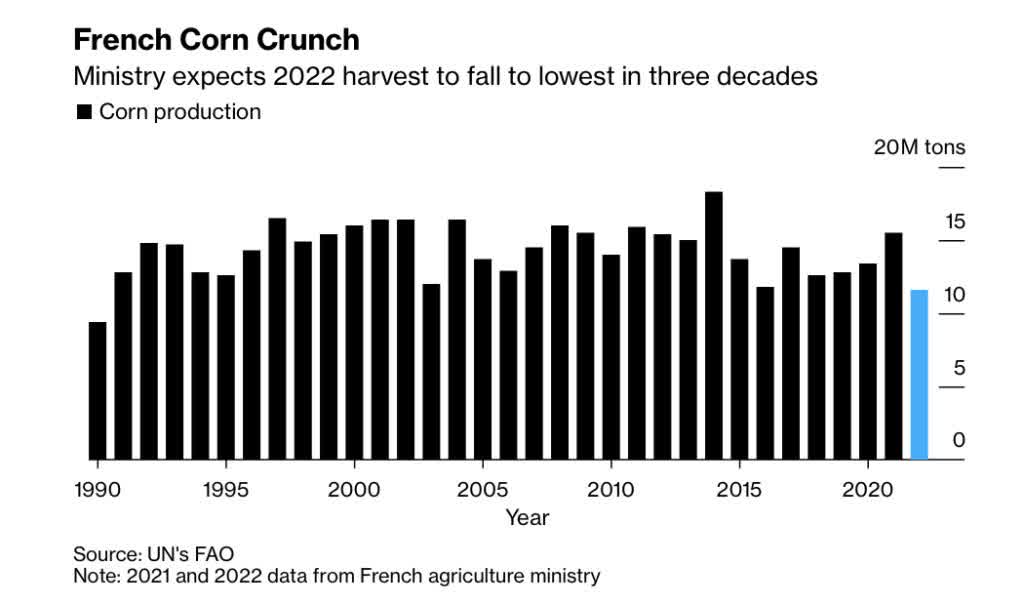

Moreover, we’re now in a situation where we could see another year of La Nina, a weather phenomenon that will (could more than likely) pressure crop production in key growing areas in Southern America, Europe, Asia, and North America. Although I expect North America to remain in a good spot due to really favorable growing areas.

France, for example, is seeing the first corn crop in more than three decades, which is a good benchmark for the dire situation in Europe right now.

Bloomberg

According to the same article:

The price of everything from a cup of coffee to the coal used in steelmaking is impacted by the weather. It’s all but guaranteed the world will see another year of weather disasters that destroy homes, ruin crops, disrupt shipping and threaten lives. Another year of La Nina means the world is hurtling toward $1 trillion in damages by the time 2023 wraps up.

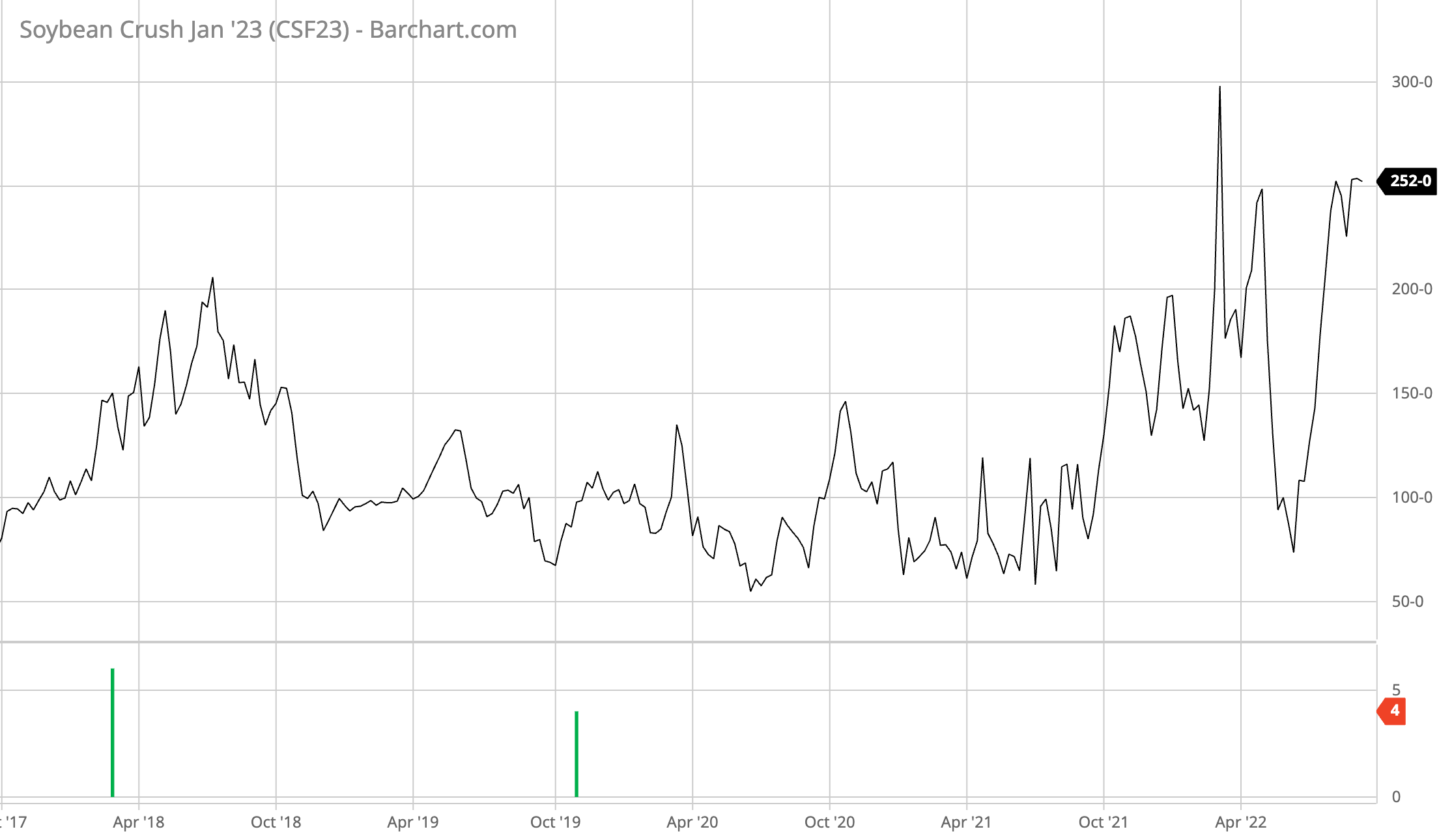

It also needs to be said that the company’s operations benefit from strong crush margins. Crush margins are the margins it gets on operations like turning soybeans into soybean meal and soybean oil. After all, that’s not something farmers do. Companies like ADM buy grains and turn this into value-added products. If i.e., soybean oil and soybean meal futures outperform the price of soybeans it pays to farmers, ADM makes more money.

Using soybean crush futures, we see that futures are indeed at elevated levels, more than double what they were prior to the pandemic.

Barchart (Soybean Crush Jan 2023)

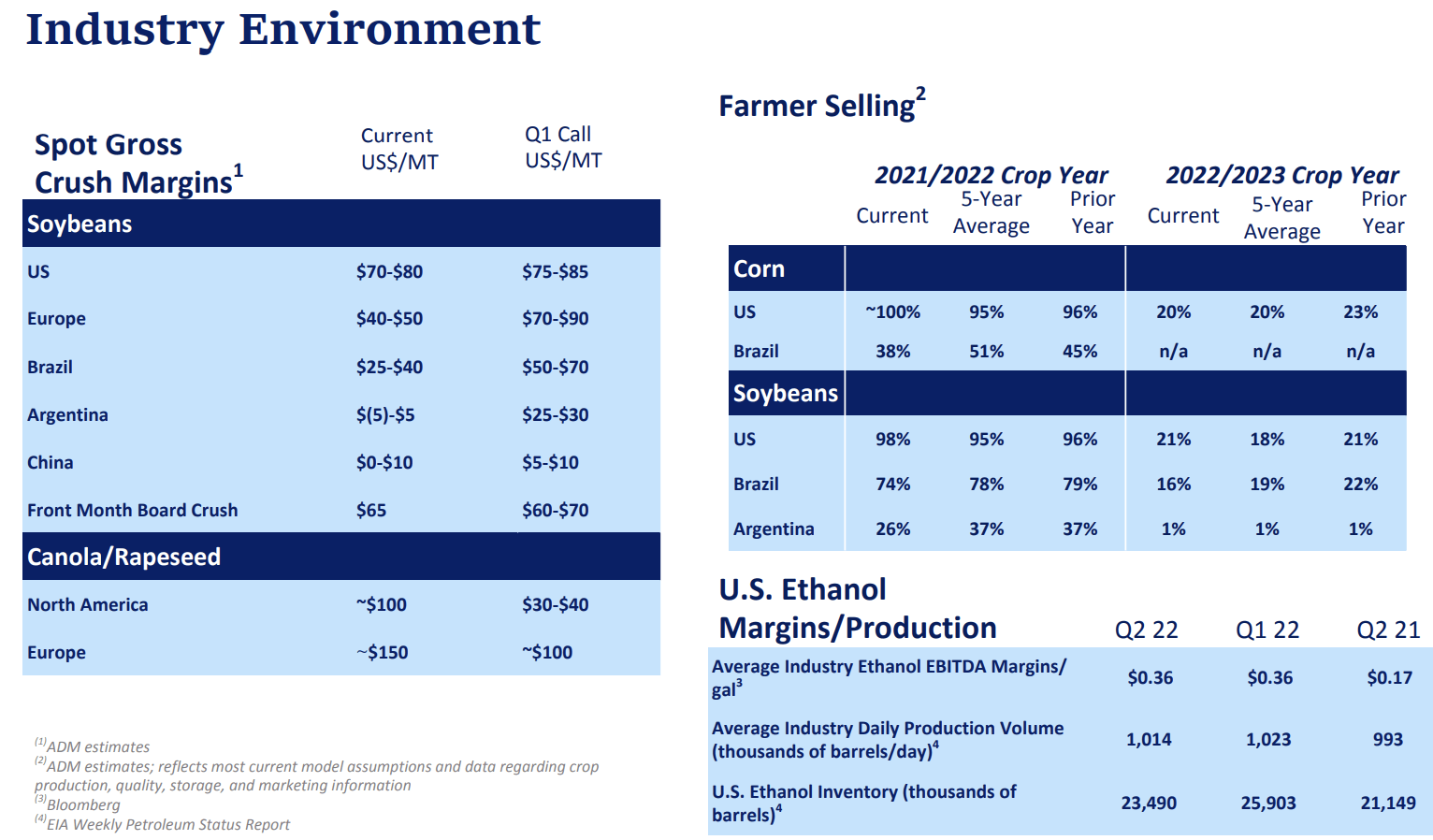

The company’s own numbers as shown below confirm this. Both crush margins and ethanol margins are very strong. Given higher demand, the company is in a good spot to deliver elevated earnings on a long-term basis.

Archer-Daniels-Midland

With regard to the company’s outlook:

[…] North American crush margins should be constructive. As soybean meal remains a very efficient and cost-effective protein substitute for even wheat as wheat prices, even though they’ve come up, they’re still relatively expensive. So soybean meal remains an important feed for all types of protein and especially for poultry, and you’ve seen the number of poultry rising. So we’re constructive for crush margins in North America.

And even with biodiesel as well, that’s also providing another avenue to support crush margins even in Europe. So crush margin outlook for the back half is strong in terms of the fundamentals that I highlighted.

What About The Valuation?

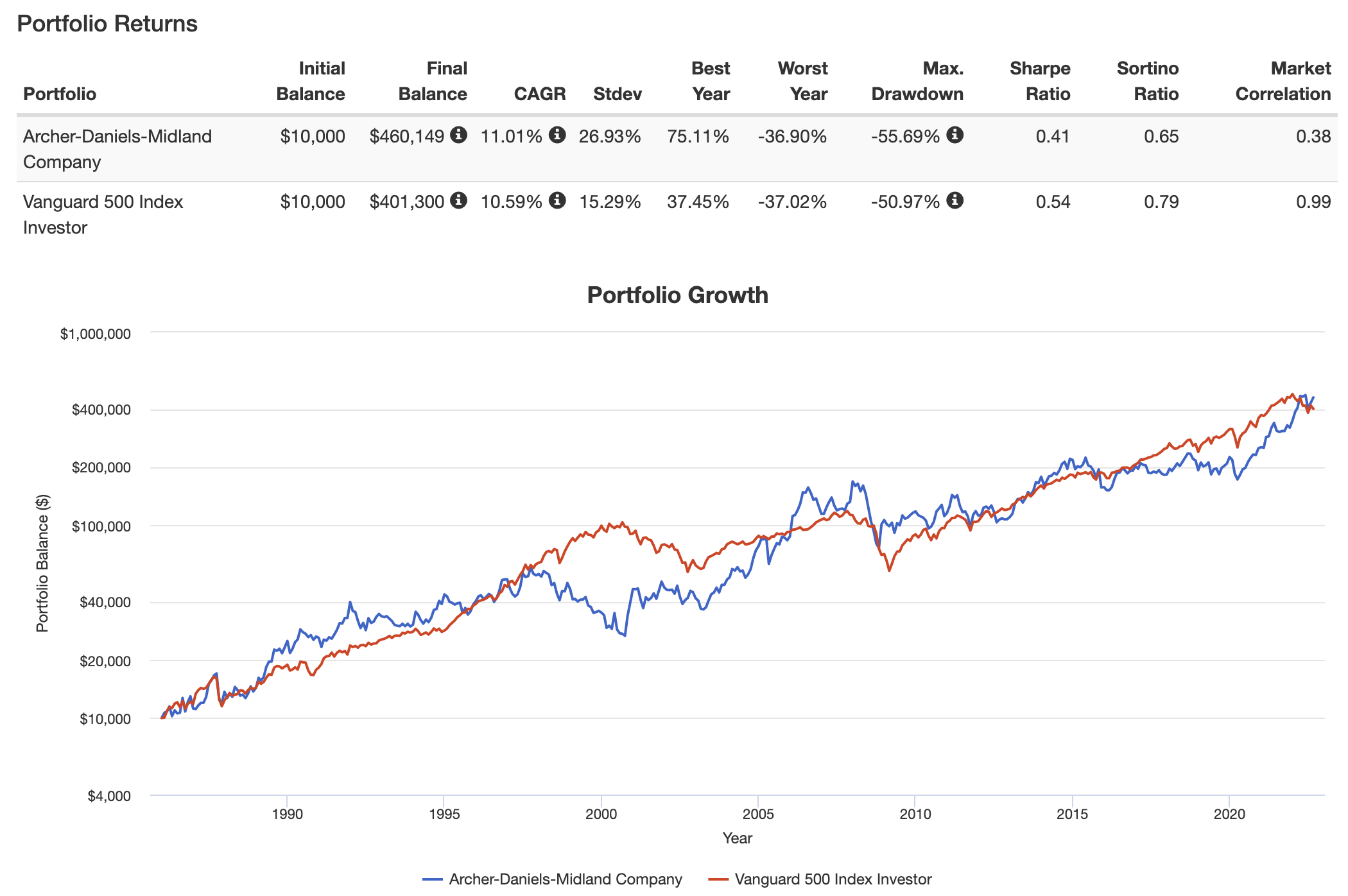

Archer-Daniels-Midland has a low correlation with the market. Going back to 1986, the company has a 0.38 correlation, which is rather low. What’s interesting is that during this period, ADM shares have performed really well. An investment in ADM was “slightly” more profitable than an investment in the S&P 500. While the S&P 500 was rising quite consistently, ADM shares got most of their gains from three major upswings with prolonged sideways trends in between.

We’re currently in one of these uptrends for the first time since the early 2000s as the market has shifted from “growth” to “value” stocks due to high inflation, high commodity prices, and everything related to this.

Portfolio Visualizer

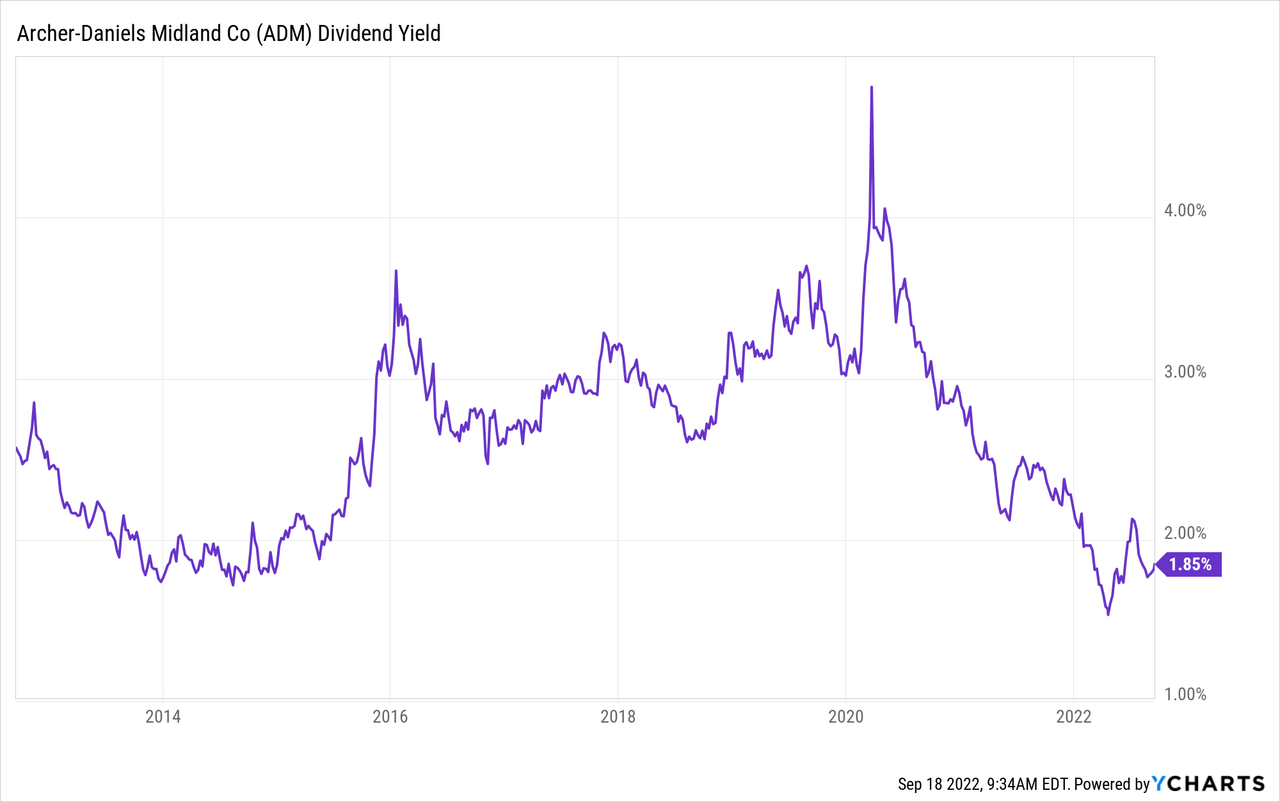

Given these developments, it’s important to refrain from buying into overvaluation. Especially because ADM shares are yielding less than 2% again. That’s not a lot for most dividend investors, especially not when dealing with slow-growing (in general) stocks.

ADM has been paying dividends for 90 years with 40 years of consecutive growth. The company hiked dividends by 8% this year. The current dividend is $0.40 per share per quarter. That’s $1.60 per year or 1.9% of the company’s stock price.

This yield is one of the lowest in years. It’s even below 2014 levels before commodities came down crashing.

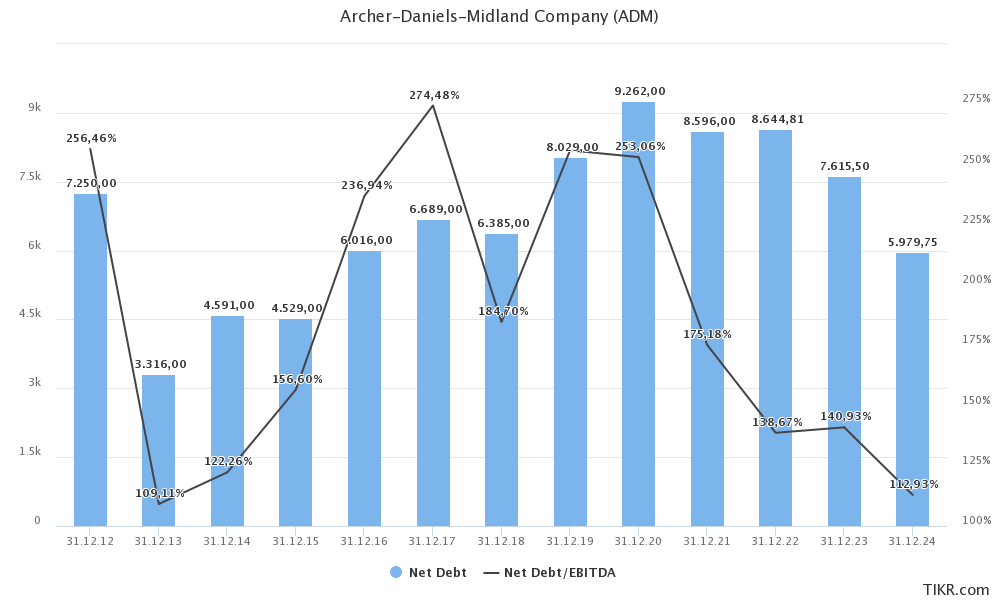

One thing that helps the company’s valuation tremendously is accelerating cash generation. Pre-working capital changes, the company generated $3.2 billion in operating cash flow in the six months ending June 30. That’s up from $2.2 billion in the prior-year period. This helps to bring down the net debt load to less than $6.0 billion in 2024 (expected).

TIKR

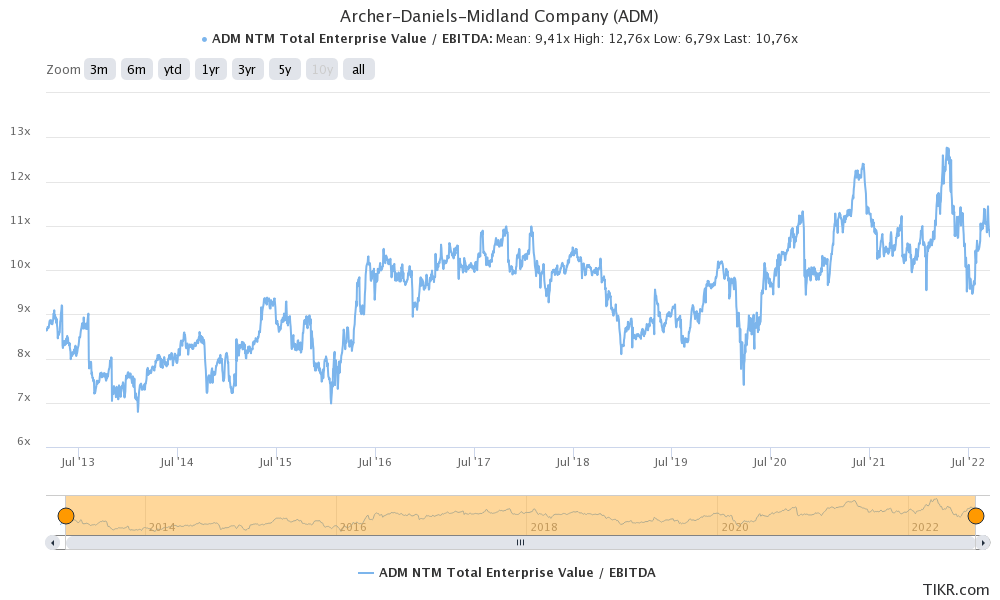

This matters as it lowers the implied enterprise value. Right now the company has an implied enterprise value of $55.4 billion consisting of its $47.5 billion market cap, $7.6 billion in 2023E net debt, and $300 million in minority interest. That’s 10.3x 2023E EBITDA of $5.4 billion.

That’s a very fair valuation and not at all overvalued as the dividend yield may suggest.

TIKR

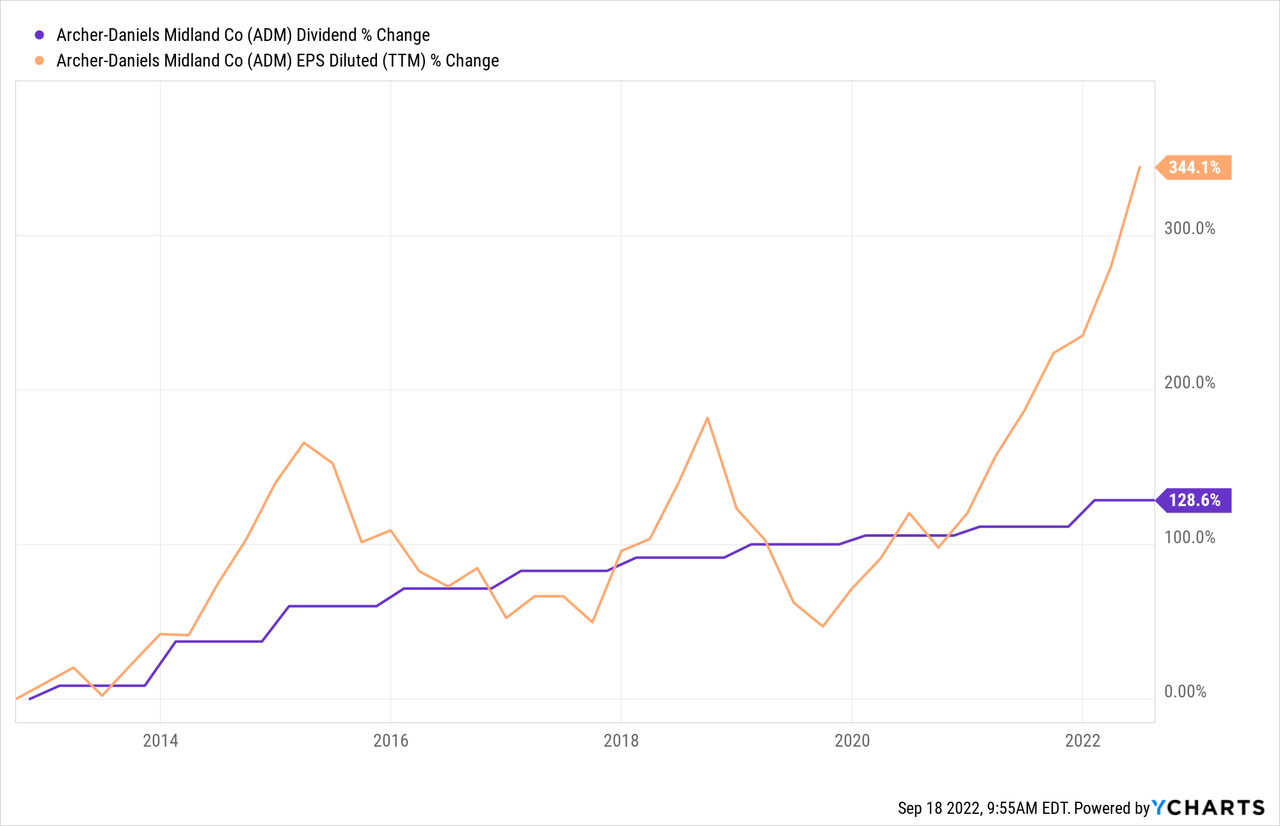

Based on this context, I’m using the chart below to make two points. First of all, look at how cyclical ADM’s EPS growth is. Inflationary cycles boost EPS growth while the opposite of that has a significant slowing effect on EPS. While dividend growth is consistent, EPS (and related financial indicators) are currently outperforming dividend growth – by a mile. Over the past 10 years, dividend growth was 130% (not too bad!) while EPS grew by 344%. This explains why the dividend yield looks “low” while the stock itself is far from overvalued.

In my last article (before the recent rally), I wrote that investors overreacted. It was followed by a surge back to value stocks – especially the ones benefiting from agriculture tailwinds.

Given these longer-term tailwinds and the company’s valuation, I remain bullish and believe that ADM has room to run another 10% before I would become cautious.

Takeaway

The agriculture bull market continues. Global demand for crops is as high as ever while the war in Ukraine, high energy prices, fertilizer shortages, and droughts pressure the supply. This is helping ADM as it benefits from high export demand while it also feels the tailwinds from strong crush margins and business improvements to enhance operations.

While the dividend yield has come down due to subdued (historic) dividend growth, the company is not overvalued. I believe that the company has at least 10% more upside to a “fair” valuation with a high likelihood of long-term outperformance over the S&P 500 as long as the inflationary agriculture bull market lasts.

However, I would not buy a large position (relatively speaking) as the valuation isn’t attractive enough for that – especially because the stock is relatively slow-growing, which makes bigger discounts important before buying large stakes.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment