Geber86

Every investment brings with it some form of risk. This is without exception. But some investments bring more risk than others. Last year, one company that I pointed to as a riskier play, but one that would make sense for many value-oriented investors, was ARC Document Solutions (NYSE:ARC), an enterprise focused on providing digital printing services and products. At the time, the company had been exhibiting significant weakness, much of which was related to the COVID-19 pandemic, but not all. But the firm was showing some signs of stabilizing and shares were trading at very cheap levels. All combined, this made me feel a bit bullish about the company. But now that some time has passed, it’s time to see whether or not the company still makes for a very good play moving forward.

The turnaround is real

Back in early June of 2022, I found myself interested in the operations of ARC Document Solutions. At that time, I recognized how the company had struggled over the prior few years, including in the time leading up to the COVID-19 pandemic. But we were starting to see at that time a turnaround that, if sustained, could lead to attractive value creation for investors. Add on top of this how cheap shares of the company were, and I found myself drawn to the firm. Ultimately, I rated the company a ‘buy’, specifying that it might make for a very good prospect for those who don’t mind the risk that comes with a turnaround. Since then, the business has done quite well for itself from a share price perspective. While the S&P 500 is down 1.9%, shares of ARC Document Solutions have generated upside for investors of 14.2%.

Author – SEC EDGAR Data

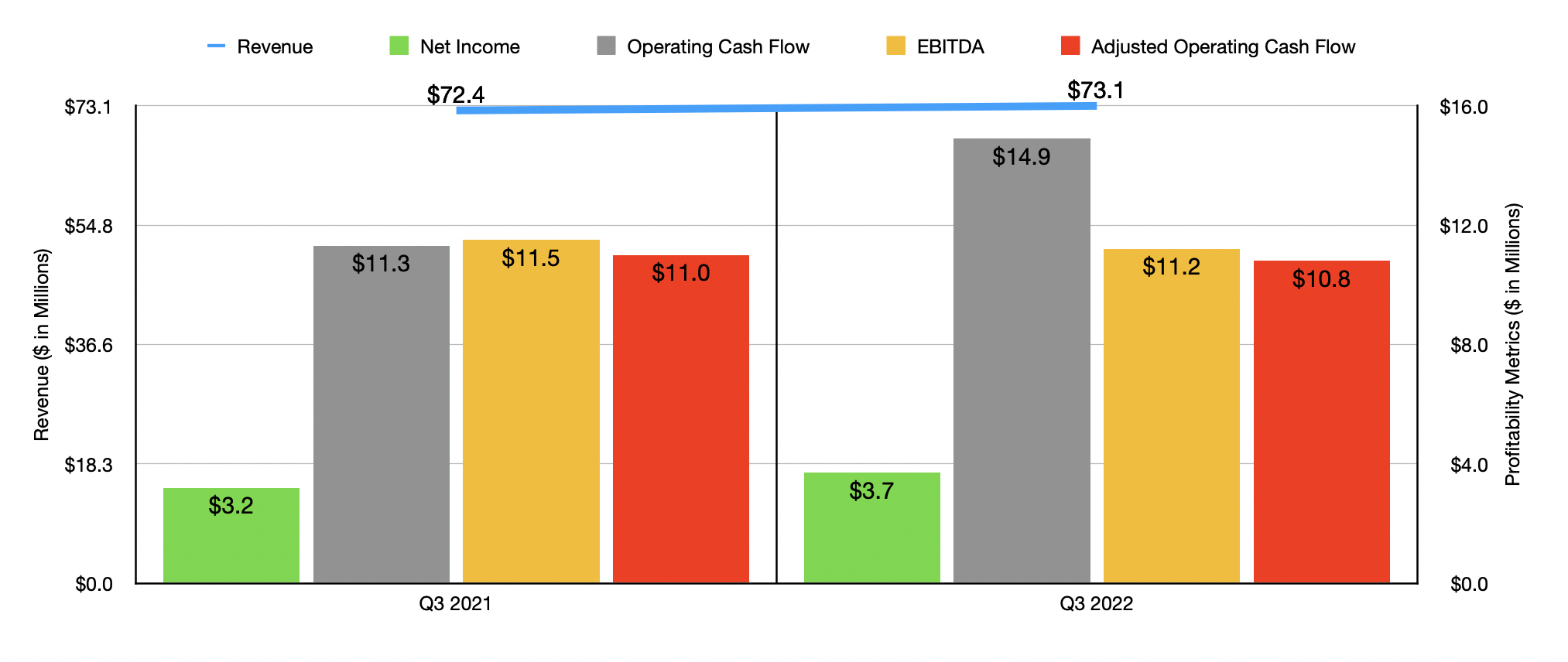

This return disparity seems to be a reward for the company proving that its operations are truly turning the corner. To see what I mean, I’d like to point to the data provided for the company’s third quarter of its 2022 fiscal year. During that time, revenue came in at $73.1 million. That’s about 1% higher than the $72.4 million generated one year earlier. Management attributed this increase in revenue to the expansion and diversification of its customer base and the selling of additional services to existing customers. On a percentage basis, the greatest growth for the company came from its Scanning and Digital Imaging operations, with sales up 17.3% thanks to growing demand for paper-to-digital document conversions used in day-to-day business operations and the creation of digital archives to replace long-term warehoused paper document storage. The company also experienced a 5% increase in its MPS operations, with an increase of on-site printing volume caused by a return from work-from-home employees to the job site helped the company immensely.

Author – SEC EDGAR Data

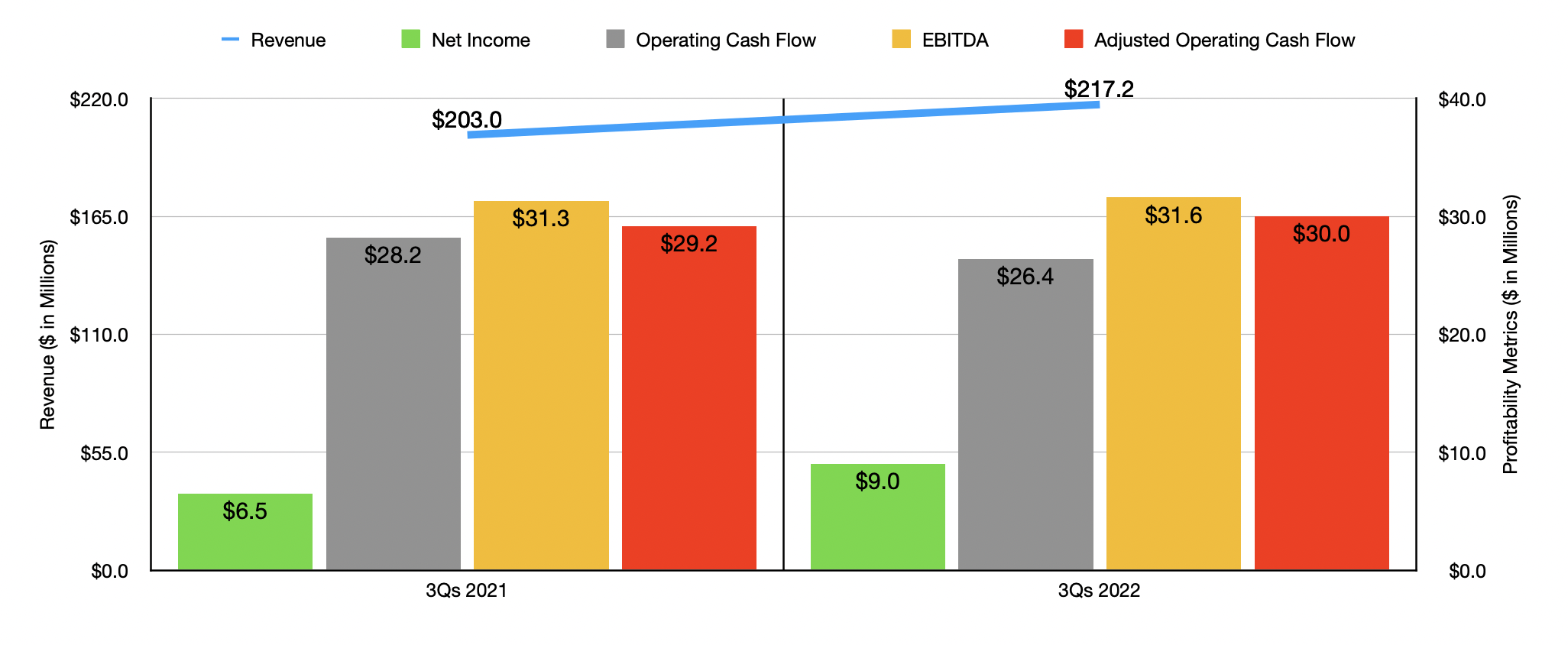

This increase in revenue brought with it improved profitability. Net income rose from $3.2 million to $3.7 million. Operating cash flow popped up from $11.3 million to $14.9 million. Though it is important to note that if we adjust for changes in working capital, it would have decreased modestly from $11 million to $10.8 million. Meanwhile, EBITDA for the company ticked down modestly from $11.5 million to $11.2 million. Results for the first nine months of 2022 as a whole look even better. Sales of $217.2 million came in 7% higher than the $203 million reported one year earlier. Profits jumped from $6.5 million to $9 million. In this case, operating cash flow for the company did worsen, falling from $28.2 million to $26.4 million. But if we adjust for changes in working capital, it would have risen from $29.2 million to $30 million. And finally, EBITDA for the enterprise expanded from $31.3 million to $31.6 million.

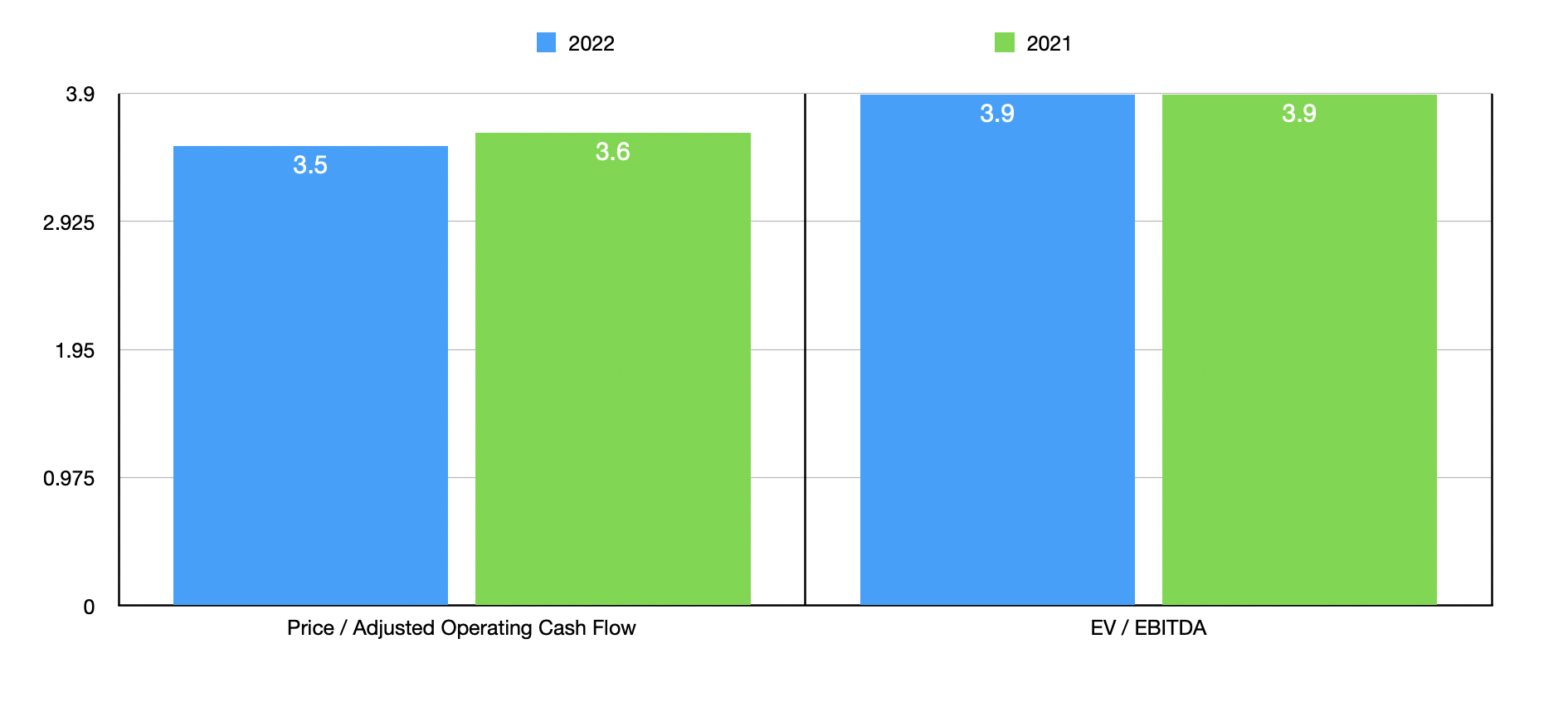

Sadly, management has not provided any guidance when it comes to the 2022 fiscal year in its entirety. But if we annualized results experienced so far for the year, we would expect adjusted operating cash flow of $40.2 million and EBITDA totaling $42.1 million. These numbers are actually not much higher than the $39.1 million and $41.7 million, respectively, that the firm generated during its 2021 fiscal year. Using these figures though, we can easily value the enterprise. On a price to adjusted operating cash flow basis, the multiple currently comes in at 3.5. This is down a notch from the 3.6 reading that we get using data from 2021. Meanwhile, the EV to EBITDA multiple for the company should be 3.9. This matches the 3.9 reading that we get using data from the year prior.

Author – SEC EDGAR Data

These are incredibly low multiples that are further enhanced when you consider just how cheap the company is compared to similar firms. I looked at five similar companies and, using the price to operating cash flow approach, I ended up with a range of between 4.9 and 323.5. Using the EV to EBITDA approach, the range was from 3.8 to 15.1. In the first case, ARC Document Solutions was the cheapest of the group, while in the second there was only one firm cheaper. It’s also worth noting that the company has a very low amount of debt right now. Net of cash on its books, the company’s debt stands at around $18.2 million. This means that the company could easily pay off its net debt in a fairly short period of time if so desired.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| ARC Document Solutions | 3.5 | 3.9 |

| Atento S.A. (ATTO) | 4.9 | 7.5 |

| Virco Mfg. Corp (VIRC) | 323.5 | 6.6 |

| ACCO Brands (ACCO) | 5.6 | 9.4 |

| Kimball International (KBAL) | 163.3 |

15.1 |

| NL Industries (NL) | 17.7 |

3.8 |

Takeaway

Operationally speaking, ARC Document Solutions may not be the greatest company on the market. The company still carries with it some risk since it’s still fairly early in its turnaround. But based on all the data I can see, the picture becomes more appealing every day and shares are still trading at remarkably low levels even after seeing a nice amount of appreciation relative to the broader market. Because of these factors, I’ve decided to keep the ‘buy’ rating I assigned the stock previously. This rating reflects my view that share price performance should outperform the S&P 500 for the foreseeable future absent any major developments transpiring.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment