PonyWang

Applied Materials (NASDAQ:AMAT) has the industry’s broadest and most enabling portfolio of materials engineering solutions used to produce almost every type of chip and advanced display in the world. Its customers include manufacturers of semiconductor chips, liquid crystal display (LCD) and organic light-emitting diode (OLED) displays, and other electronic devices. As such, AMAT is in a terrific position to benefit from the growth of the semiconductor industry. Despite this, shares are trading at a relatively low valuation, one that we believe is too low for this industry leader. We believe the company is being treated by the market as a commodity player in the cyclical Wafer Fabrication Equipment (WFE) industry, but Applied Materials is becoming a leader in some of the most advanced technologies that few competitors can match, and the company is gaining significant pricing power and growth opportunities.

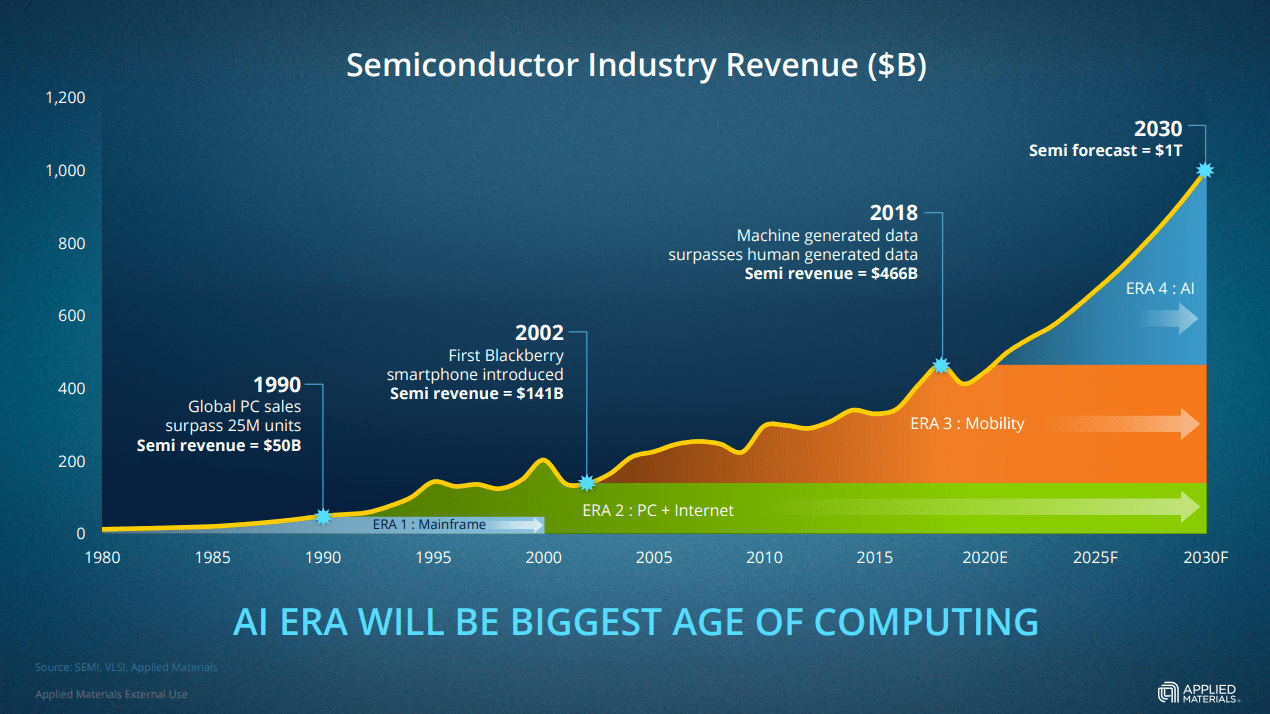

There is also the enormous growth that is being forecasted for the semiconductor industry, which is expected to reach ~1 trillion dollars by 2030. For this to become a reality the industry will need to purchase a lot of WFE equipment, and importantly, much more sophisticated equipment as the industry starts being confronted with physical limitations to shrinking and has had to increasingly rely on more advanced circuitry.

Applied Materials Investor Presentation

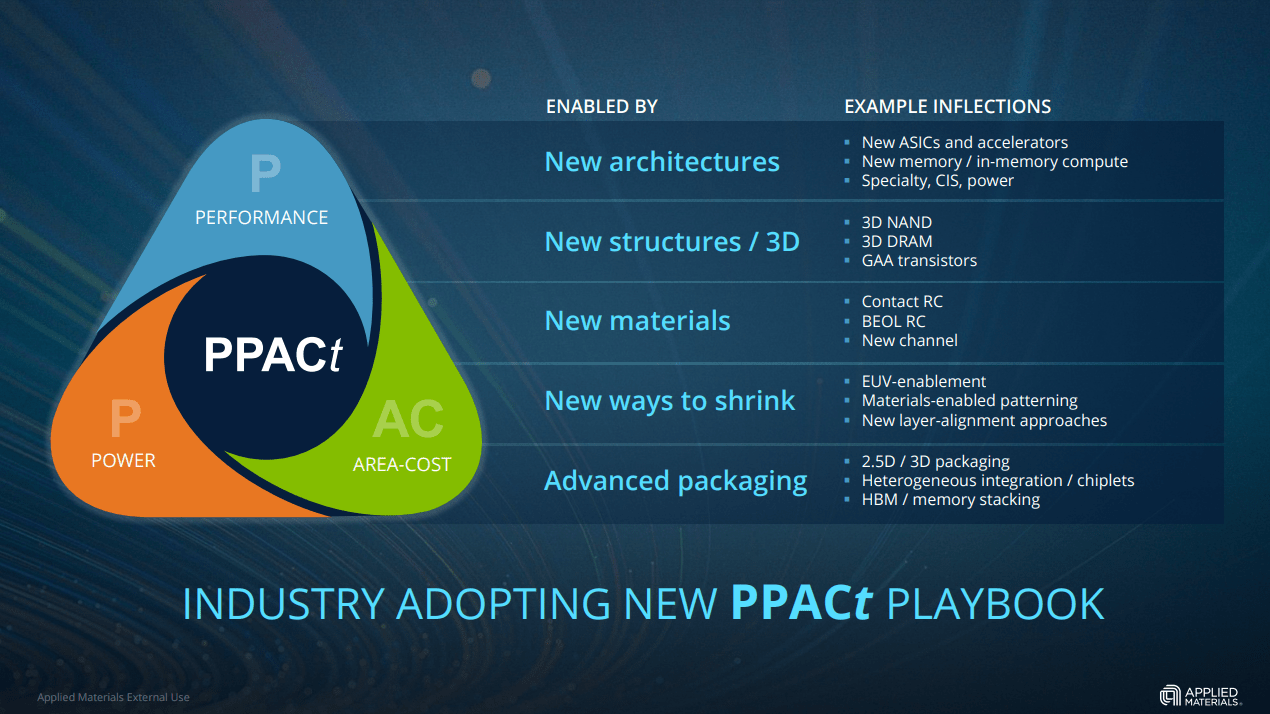

Also benefiting AMAT is its increasing focus on subscription style revenue. By 2024 it is expected that its customers will spend >$20 billion annually to manage Applied Materials’ installed base. There is also strong demand for subscription-like services to enable what AMAT calls PPACt acceleration. PPACt stands for lower power (P) consumption, higher performance ((P)), smaller size/area (A), lower cost (C), and faster time-to-market (T).

Applied Materials Investor Presentation

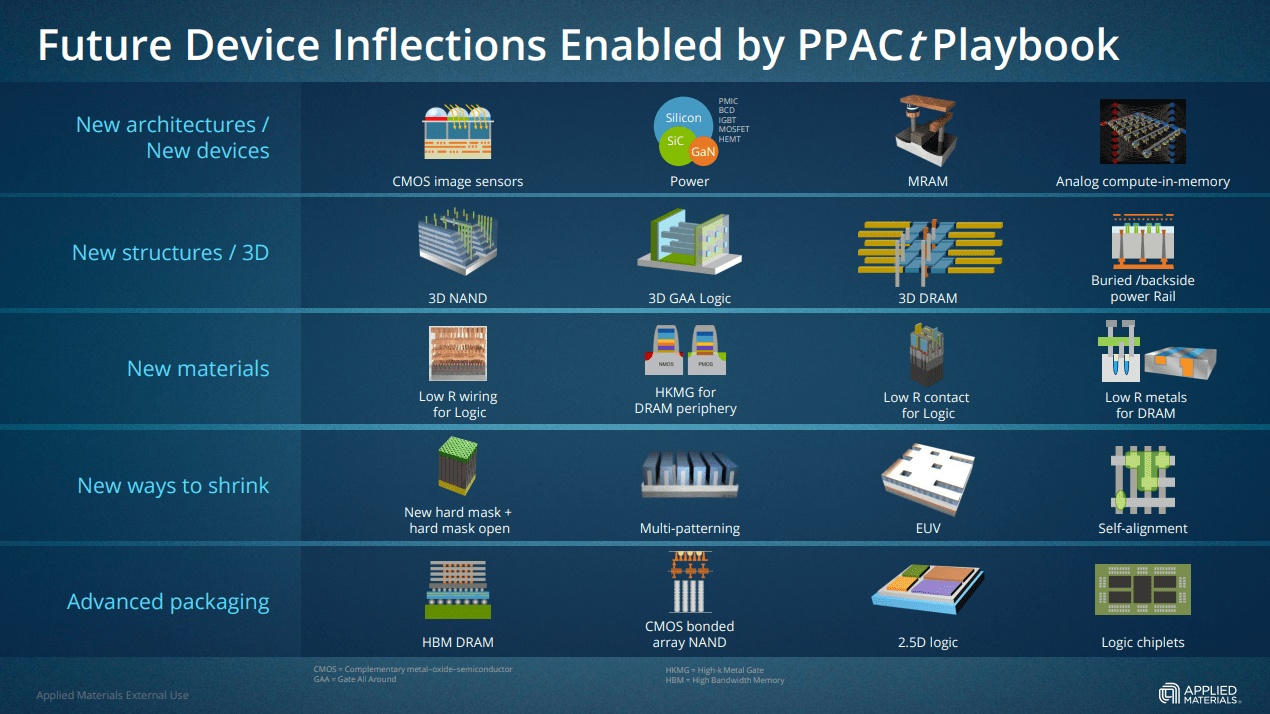

The key thing to understand about the future of the WFE industry is that the technology required to participate in a meaningful way is getting more and more complex. This means fewer players can afford to invest the necessary R&D dollars to keep up, reducing the playing field to fewer players. The slide below shows some of the technical solutions that have been needed to continue on the improvement path in the semiconductor industry. For AMAT this translates into a multi-billion dollar opportunity, with the company estimating that from 2020 to 2024 it can increase revenue with a CAGR of ~13%, while the WFE industry would only see a ~8-9% CAGR.

Applied Materials Investor Presentation

Financials

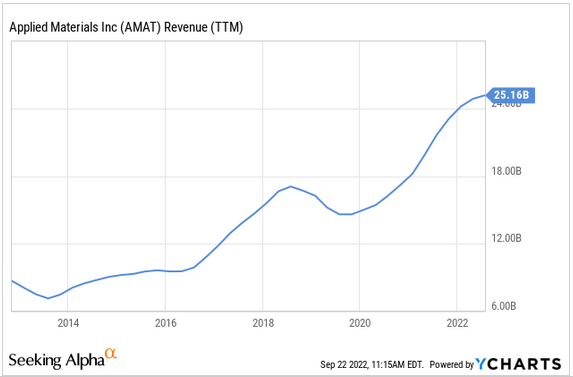

Despite the clear cyclicality, it is clear that the revenue trend is positive. The semiconductor manufacturing equipment market has been growing, and Applied Materials has been gaining share on top of that. Given the increased complexity of the equipment we expect companies that are willing to invest the R&D dollars to continue gaining share, and be able to justify higher prices for the equipment. As such we expect revenue to continue increasing for the next decade, in particular if the predictions of the semiconductor industry doubling by the end of the decade materialize.

YCharts

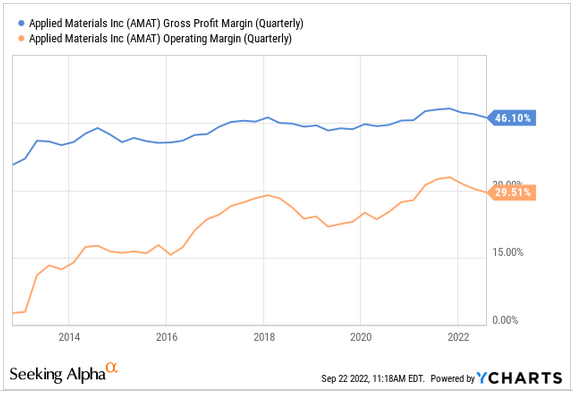

Investors should also give more respect to a company like AMAT, and not price it as a commodity player. Looking at its profit margins it is clear that this is a company with strong technological competitive advantages, and that these have been increasing the last few years, as reflected by increased operating margins.

YCharts

Growth

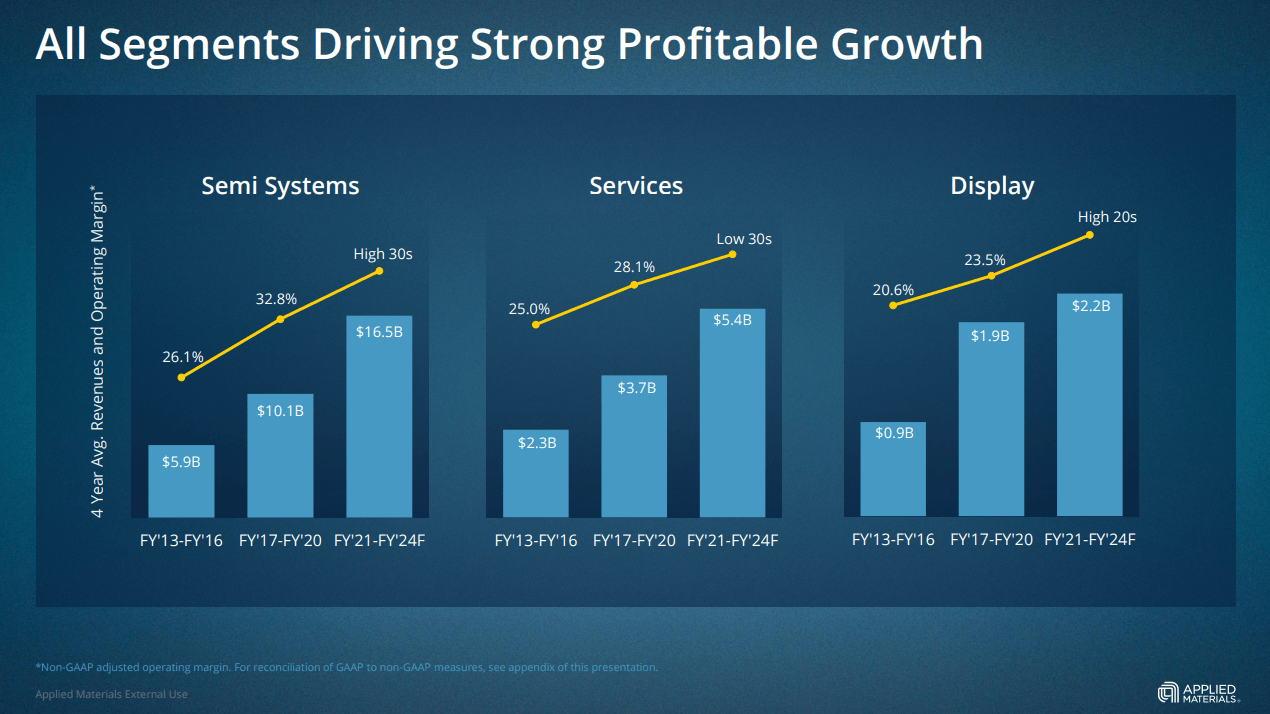

During its last investor day AMAT shared a slide where they predict higher operating margins for their three main businesses, as well as higher revenues. Especially for the Semi Systems business and the Services business.

Applied Materials Investor Presentation

Balance Sheet

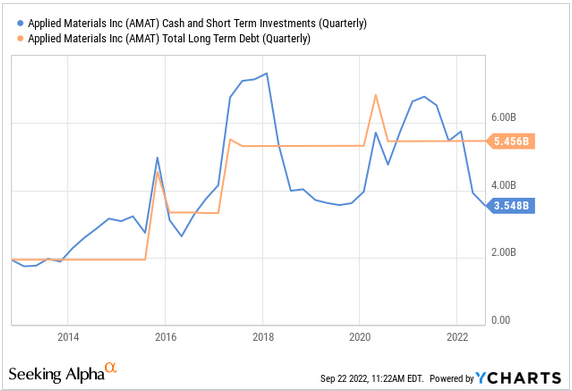

In addition to strong profitability AMAT has a very solid balance sheet, with more than $3.5 billion in cash and short-term investments that cover most of its long-term debt. The financial debt to EBITDA (TTM) is only 0.68x, we are therefore not the least worried about the safety or strength of the balance sheet.

YCharts

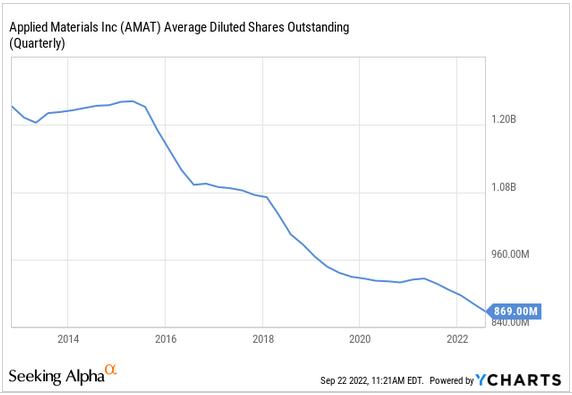

Stock Buybacks

While AMAT pays a dividend, it is through share repurchases that it has been mostly rewarding its shareholders. In the last ten years shares outstanding have decreased in a very meaningful way as can be seen in the graph below.

YCharts

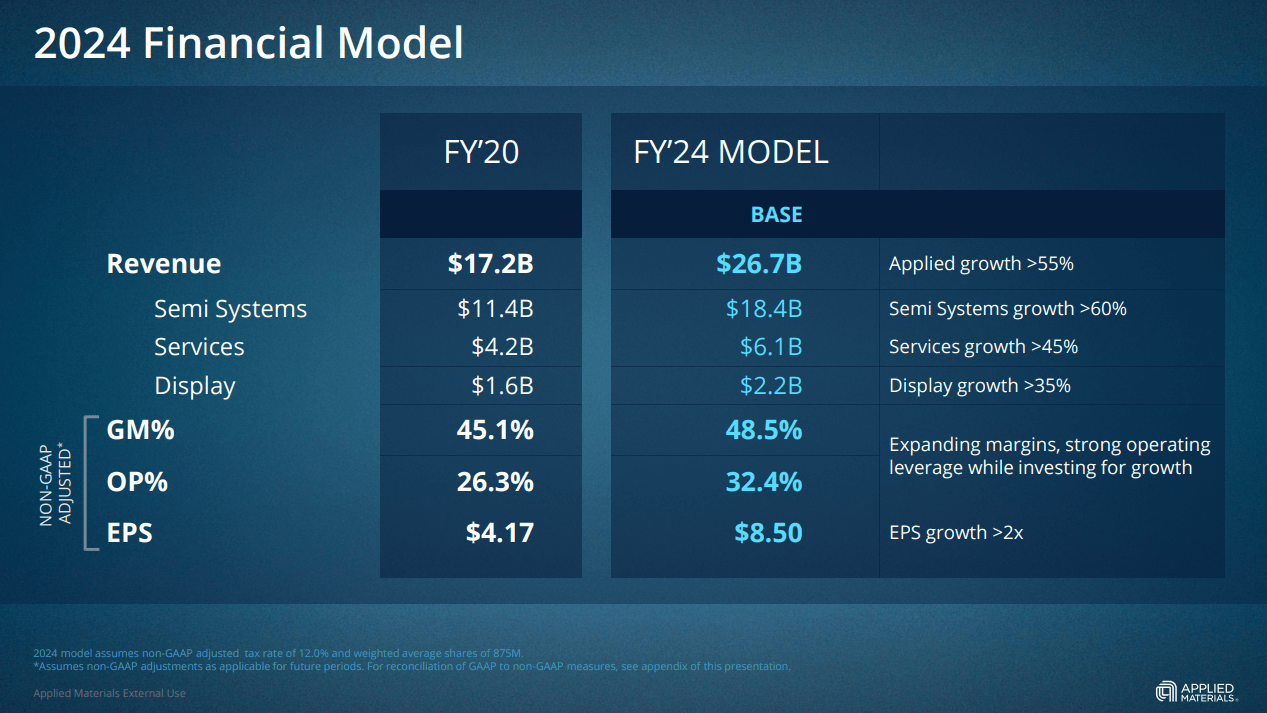

Valuation

Based on a recent share price of ~$85, and the company’s 2024 financial model, shares are trading at only ~10x the expected earnings for FY24. We believe this is conservative given that for the trailing twelve months normalized diluted EPS already reached $7.47. This is also the company’s base case, and for their High estimate they project an EPS that could potentially reach $10.

Applied Materials Investor Presentation

Risks

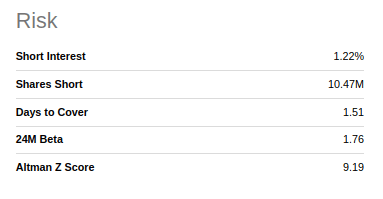

In the short term the main risk would be if the semiconductor industry enters a cyclical downturn. Longer-term we view the biggest risk that of technological disruption from a competitor, but this risk is mitigated by the billions of dollars that AMAT itself is spending in R&D to make sure it stays at the cutting-edge of technology.

From a financial point of view, we do not see much to get worried. The balance sheet is incredibly strong, the amount of shares outstanding sold short is very low, and the company’s Altman’s Z-Score is quite high.

Seeking Alpha

Conclusion

Applied Materials is doing better than its share price seems to suggest. It is a leader in markets with increasing technical complexity, and it is significantly outperforming its markets. Growth, and strong execution are driving significant margin expansion and earnings growth, while retaining a solid balance sheet. Despite the potential risk of a semiconductor down cycle coming, we believe shares have become too cheap, and don’t give enough credit to the strength of the company’s technological advantage.

Be the first to comment