yalcinsonat1/iStock Editorial via Getty Images

Apple (NASDAQ:AAPL) ended last week on a high as the market once again extrapolated a new product offering too far. The latest report has the tech giant working on a subscription plan for the iPhone and other hardware products, though similar monthly payment options already exist. My investment thesis remains Bearish on the stock with the market’s constant need to drum up reasons to pay rich prices for Apple despite a tough path for stock gains over the next few years.

Monthly Payments Aren’t New

Since the original launch of the iPhone back in 2007, consumers have rarely been forced to pay the full price of the costly smartphone upfront, or at all. From wireless carrier subsidies to monthly payment plans now and even Apple installment loans, people aren’t forking over $1,000+ at checkout or a cash register to acquire an iPhone.

According to Bloomberg, Apple is working on a subscription plan for iPhones and other hardware, iPads and Macs, charging a monthly fee. The company could bundle a hardware subscription possibly with other services discounted, such as Apple Music or Apple TV+.

While a subscription service for hardware would tie more consumers into Apple products over the long term and provide a direct connection to the consumer, users aren’t exactly clamoring for such an option. The tech giant would possibly be required to offer a bundled discount to offset wireless carrier discounts such as these from Verizon Communications (VZ) offering $800 off a second phone plus the costs to move from another carrier.

Source: Verizon

Remember, Apple isn’t trying to sell a $40/month wireless service to these iPhone owners against multiple competitors. The tech giant gets people to sign up for subscription services due to the value of the product, not discounts offered to sign up.

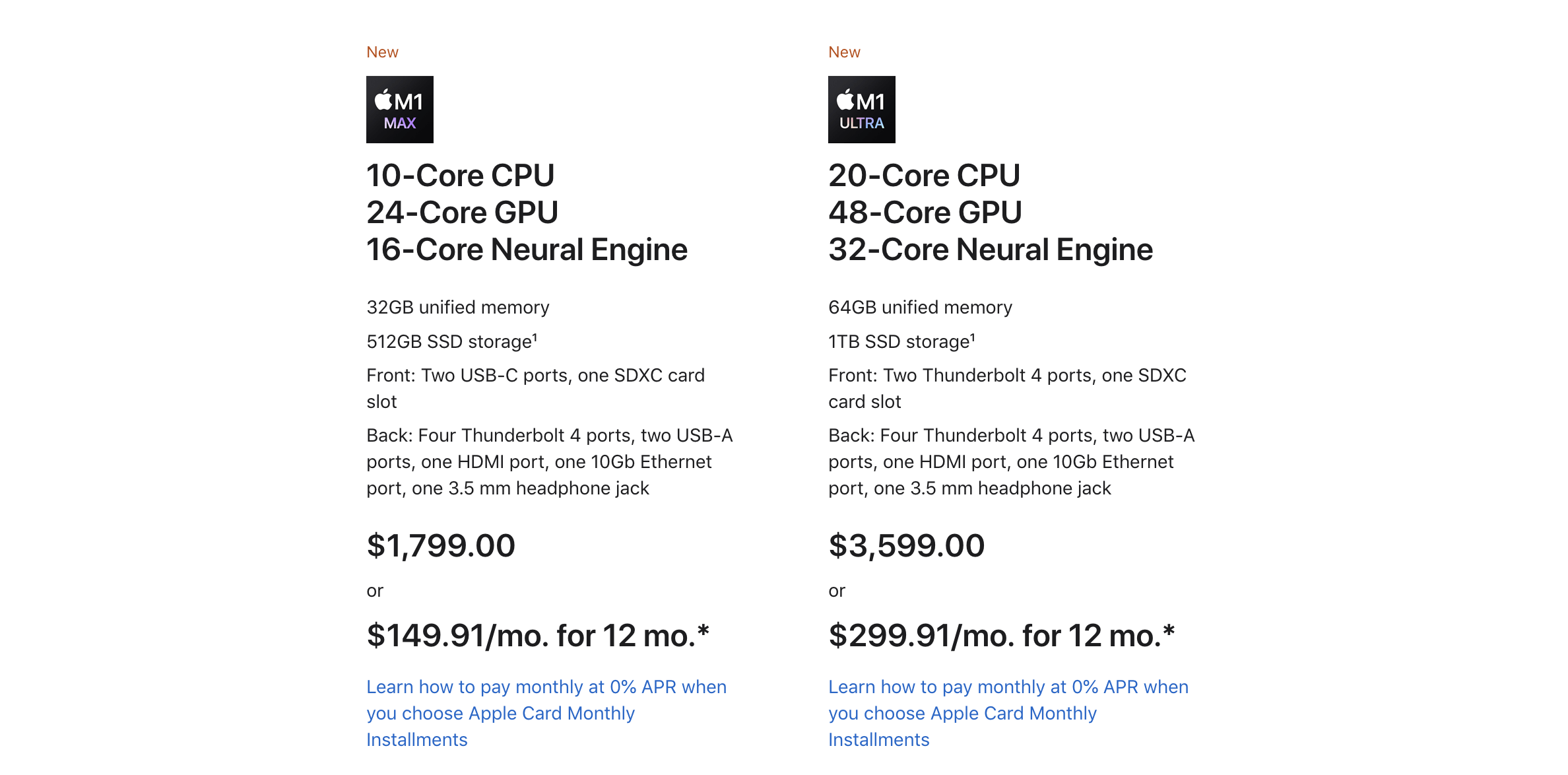

Apple already offers customers the ability to pay for hardware via a 12 or 24-month installment plan along with a discount on a trade in, or monthly payments via the Apple Card. A prime example is the new Mac Studio offered to consumers via 12-month installment payments of either $150 for the lower end product and $300 for the higher end product.

Source: Apple.com

The tech giant could definitely work out a subscription service to offer customers the ability to automatically upgrade into a new iPhone or Mac with each annual release. These customers would have to pay a higher fee than the current monthly installment costs or pay the monthly subscription far beyond a current cycle where customers replace iPhones every 3 to 4 years.

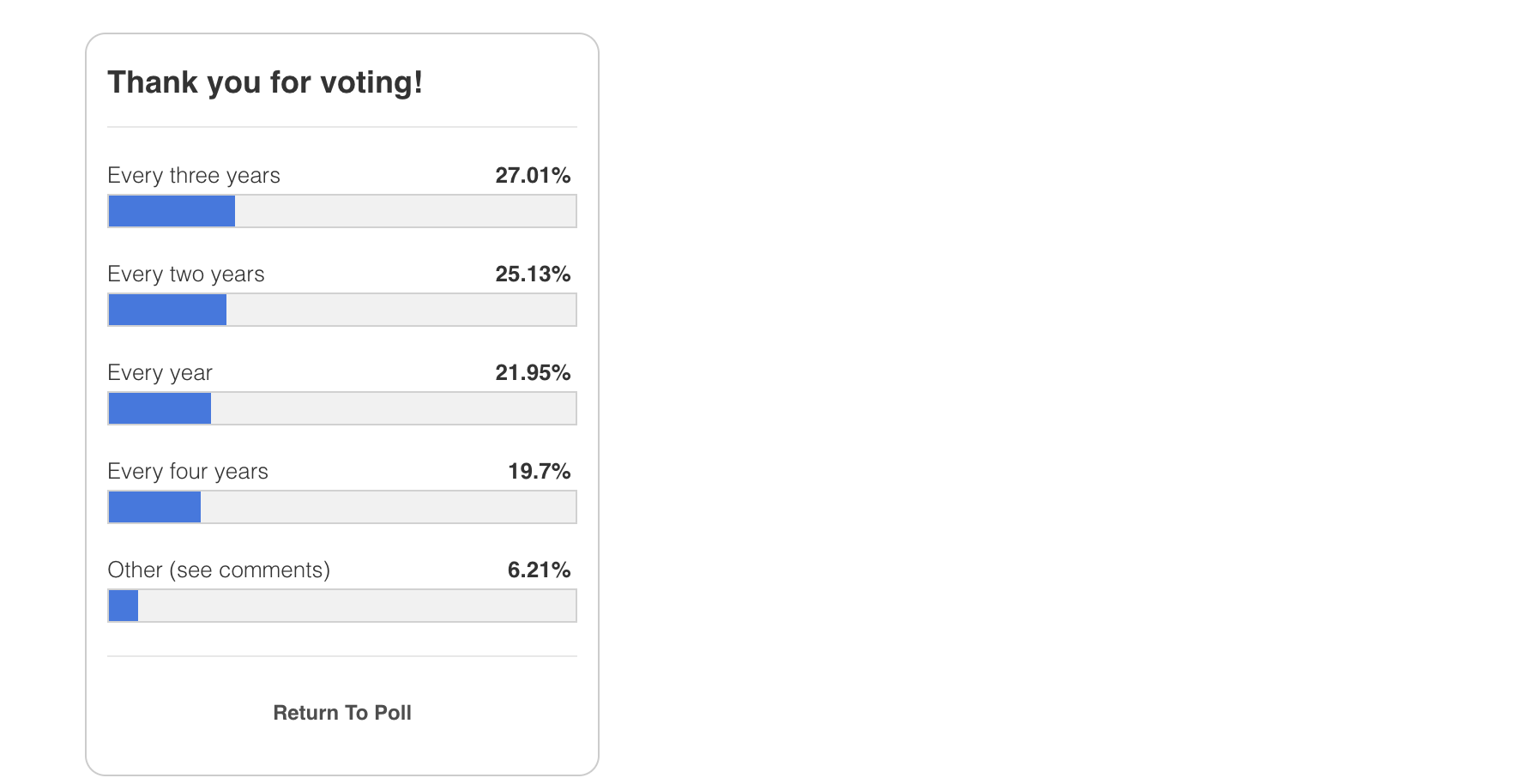

A 9to5Mac poll from earlier this year suggests that only 52% of consumers upgrade an iPhone within 2 years. A lot of people now delay upgrades for 3 to 4 years and save a significant amount when compared to paying for a new iPhone every 2 years.

Source: 9to5Mac

More research by BlinkAI about a year ago found that 34% of iPhone users plan on keeping their iPhone beyond 3 years before upgrading. This research had nearly 60% of iPhone owners taking at least 24 months before upgrading.

Source: 9to5Mac

Either way, a large amount of consumers are now extending the iPhone upgrade cycle from the traditional 24-month cycles with wireless carrier subsidies reducing the revenue potential for Apple. These consumers are paying off iPhone installment plans with Apple or wireless carriers and saving money with the smartphone still functioning correctly for a longer period now.

These consumers seem highly unlikely to suddenly participate in a subscription plan requiring additional long-term costs and a lack of any potential subsidies from the wireless carriers. Of course, some customers that upgrade every year might find a monthly subscription the best way to grab a new iPhone or iPad each year.

In essence, Apple would have to provide some financial incentive for users to upgrade more often with plentiful current options for monthly payments. Any discounts wouldn’t necessarily make more money for Apple because consumers are already adequately able to purchase iPhones.

Minimal Boosts

As my previous research has discussed, Apple moving into AR/VR devices and electric AVs or now possibly hardware subscriptions isn’t necessarily a boon to a business with $400 billion in annual revenues. Analysts aren’t hiking revenue or EPS estimates as fast as the stock is rising.

Even after a big quarterly beat in FQ1’22, Apple will struggle to generate even 5% revenue growth annually over the next 3-year period. The tech giant beat revenue estimates by a large $5.4 billion for 11.2% growth and EPS estimates by $0.21, but analysts have only boosted the FY22 revenue estimates to 8.2%.

Source: SA Earnings estimates

The market just doesn’t appear to understand the trend where FQ2’22 revenues are only set to grow 5.1%, down from 11.2% in the December quarter. My previous article highlighted how Apple didn’t beat EPS targets by a wide margin pre-Covid.

The normalization of the market should lead the quarterly results back to this normal range to where a forecast for 5.1% revenue growth leads to actual reported revenue growth of no more than 6.0%. The market still thinks Apple is going to smash these growth rates while history suggests otherwise.

Apple has soared close to all-time highs, but the FY22 EPS target remains at $6.16. The stock trades at 28x these EPS targets. Even worse, the tech giant trades at nearly 27x FY23 EPS targets of $6.55.

Takeaway

The key investor takeaway is that the AR/VR device and likely hardware subscriptions going forward aren’t going to boost the current bottom line targets of analysts. Apple remains far too expensive for forecasted financial targets, especially considering the trends in normal times of these targets being close to the actual reported numbers. The stock just isn’t priced for this reality while all of the hyped new products aren’t going to move the needle.

Be the first to comment