Studio4/E+ via Getty Images

Back in July 2023, I wrote an article on Apple Hospitality REIT, Inc. (NYSE:APLE) labeling this Stock as a buy given the momentum in the underlying earnings and a ~30% discount to other publicly traded hotel REITs.

Since then, APLE has registered a total return performance of ~10.5%, which is roughly 700 basis points above the broader REIT market. About 70% of this performance has stemmed from price appreciation, thus implying that some multiple expansions have taken place.

Now, just recently the Company issued its Q4 earnings deck, which in combination with the total result profile over 2023 and enticing outlook for the remainder of this year, has led me to buy more of APLE’s stock.

Let me now explain the key reasons behind my bullish thesis here.

Thesis

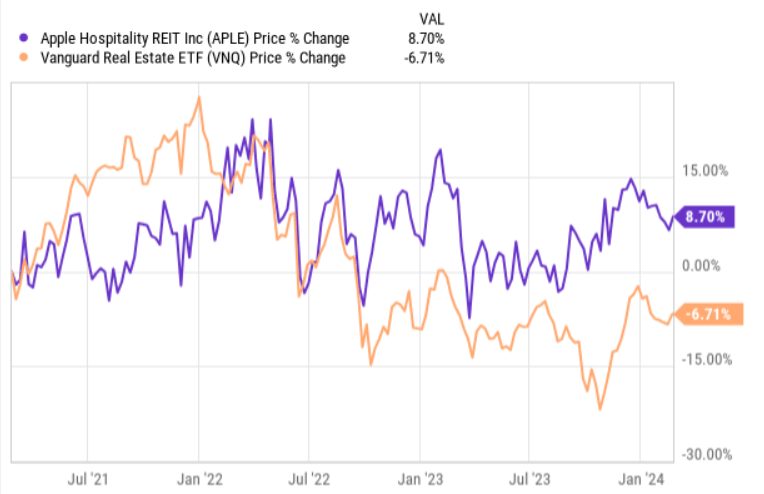

First, if we look at the 3-year historical price levels of APLE and the overall REIT market – Vanguard Real Estate Index Fund ETF Shares (VNQ) – we can see that Apple Hospitality has got a bit ahead of the index. During this period, APLE has outperformed VNQ by ~15% (measured on a price return level).

Ycharts

There are two major reasons behind this gap:

- APLE’s continued recovery from the consequences of the pandemic.

- Downward pressure on the index from the office sector, which has struggled a lot lately.

Considering the above, one might theoretically argue that currently, the entry point in APLE is not that favorable as the stock price has gone up, while the market has declined, becoming relatively cheaper from a multiple perspective.

However, I think that this kind of thinking is incorrect.

First, stock price appreciation of ~9% over a 3-year period is nothing material to substantiate a change in thesis. Second, from the P/FFO multiple perspective, APLE still trades at an attractive level in both relative and absolute terms: ~10% below the sector average if adjusted for extremes, and at P/FFO of just 9.9x, respectively. Third, most importantly, the fundamentals have improved a lot, rendering the prevailing multiple cheap compared to the underlying financial dynamics.

Let’s now explore the essence in a bit more detail.

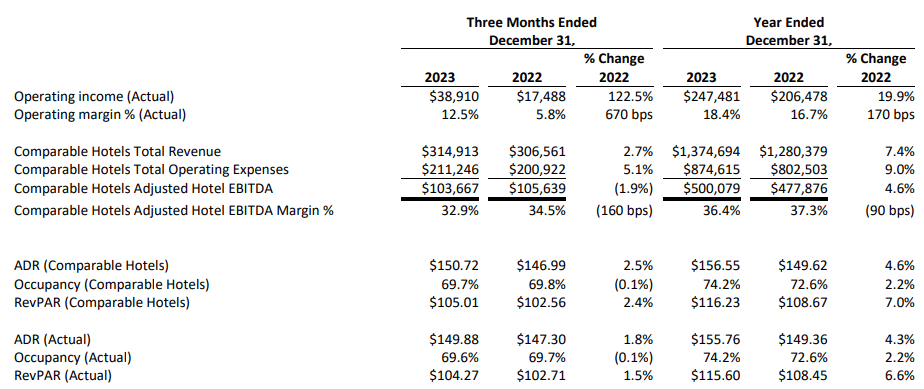

The recent earnings package revealed positive movement across the board. This is an achievement in itself given a very tough comparable base in 2022, which was supported by the pent-up demand and opening of economies that led to massive consumer spending levels (including travel & leisure)

Comparable hotel sales landed at $315 million for the quarter and $1.4 billion for the year that translates to a 3% and 7% increase compared to the same period of 2022, respectively.

Here it is important to underscore that the uptick in sales and RevPAR was primarily driven by a better pricing mix since occupancy levels remained more or less flat.

APLE Q4, 2023 earnings

Yet, looking at the margins, we can notice that there has been some minor contraction despite higher sales on a comparable hotel basis. Against the backdrop of a highly inflationary environment going into 2023 and persistent pressure on wages as well as utilities (two notable cost items for hotels), it is only logical that the margins have remained flattish or declined a bit.

In this case, I would not be that concerned about APLE’s ability to safeguard the existing margin levels (or even improve this going forward) due to the following reasons:

- Inflation is clearly slowing down, which is confirmed by the fact that the Fed has stopped its hiking cycle and instead is increasingly focusing on the timing and level of interest rate cuts.

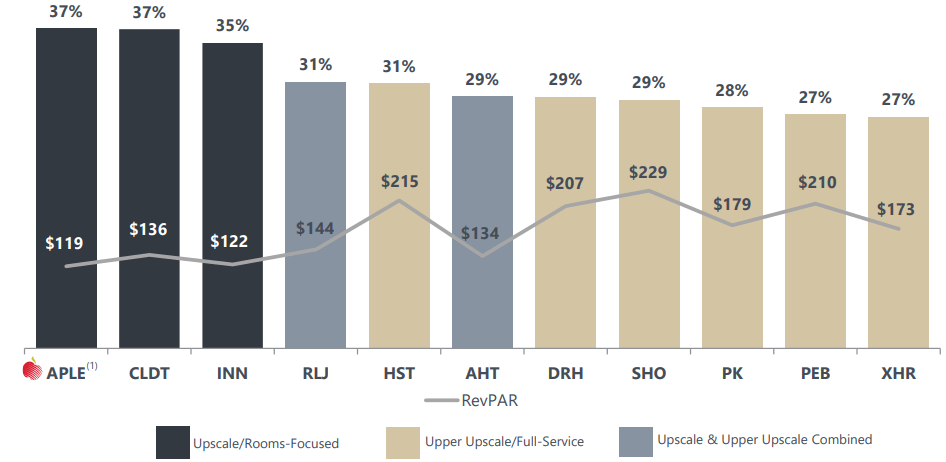

- APLE’s business model is placed in upscale/rooms-focused segments, which makes it easier to pass through the inflationary effects to the end customers. 2023 has been clear proof of that, where growing RevPAR managed to offset the bulk of cost inflation. Lastly, the chart below captures this story quite nicely: i.e., where the focus on higher-end customers leads to better pricing opportunities.

APLE Investor Presentation

Besides the strong top-line and the company’s pricing power, it is important to have a sound balance sheet in place that acts as a shield against deteriorating economic conditions and helps to feed growth in a sustainable manner.

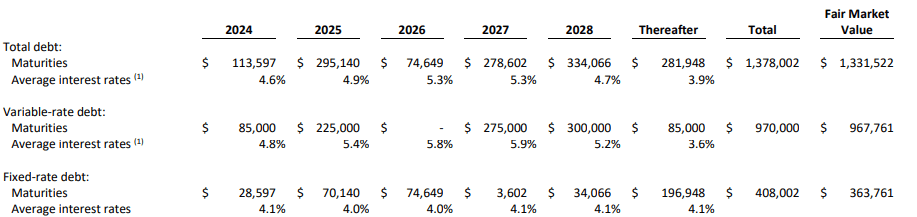

This aspect is one of the key drivers why I have decided to load up on APLE’s stock. Namely, as of now, Apple Hospitality carries a debt ratio of 28%, which is approximately half the lodging sector average. The Company has a net debt to EBITDA of 3.1x, where the underlying debt proceeds are based on a weighted average interest rate of 4.3%.

Now, the table below indicates an additional aspect, which makes the story of the fortress balance sheet even more enticing.

APLE Q4, 2023 earnings

Approximately 80% of APLE’s debt is stipulated at fixed interest rates, which in turn allows it to avoid some headwinds from higher SOFR. While there are some fixed rate debt maturities in 2024 and 2025, the majority of them start to fall due from 2027, which offers sufficient time for APLE to avoid incremental material pressure from higher financing costs until the interest rates normalize.

Going forward, APLE is well-positioned to accommodate organic growth in an investor-friendly fashion. According to Justin Knight – CEO in the recent earnings call, the Company will continue to acquire additional properties that should feed higher EBITDA generation.

Combined with our tremendous transaction experience, our available balance sheet capacity, and our deep industry relationships, we believe we continue to be well-positioned relative to competitors in the current market environment and are optimistic that we will continue to be net acquirers in the coming months. We also actively seek opportunities to refine our portfolio and optimize our capital reinvestment program by disposing of older assets in lower-growth markets.

The bottom line

APLE trades at a P/FFO that is just below 10x and also ~10% below the hotel REIT sector average. In the context of improving performance, a fortress balance sheet, and inherent competitive strength to pass the inflationary pressures forward to the end customers, the prevailing valuations seem too low.

In my humble opinion, this gap will be eventually closed by APLE’s continued investments in existing hotels and M&A that could be accommodated by solid internal cash generation (FFO payout of just 66%) and a very strong balance sheet – all of which support growth without shareholder dilution.

For me, Apple Hospitality is a strong buy.

Be the first to comment