wildpixel

Mortgage REIT giant Annaly Capital (NYSE:NLY) reported fourth quarter and full-year earnings on Wednesday night, and results were mixed from my perspective. The last time I covered Annaly, which was about two years ago, I wasn’t impressed and issued a neutral rating. Today, I think the outlook for Annaly may just be worsening right as the stock has put in a massive rally, so I’m equally as cautious today.

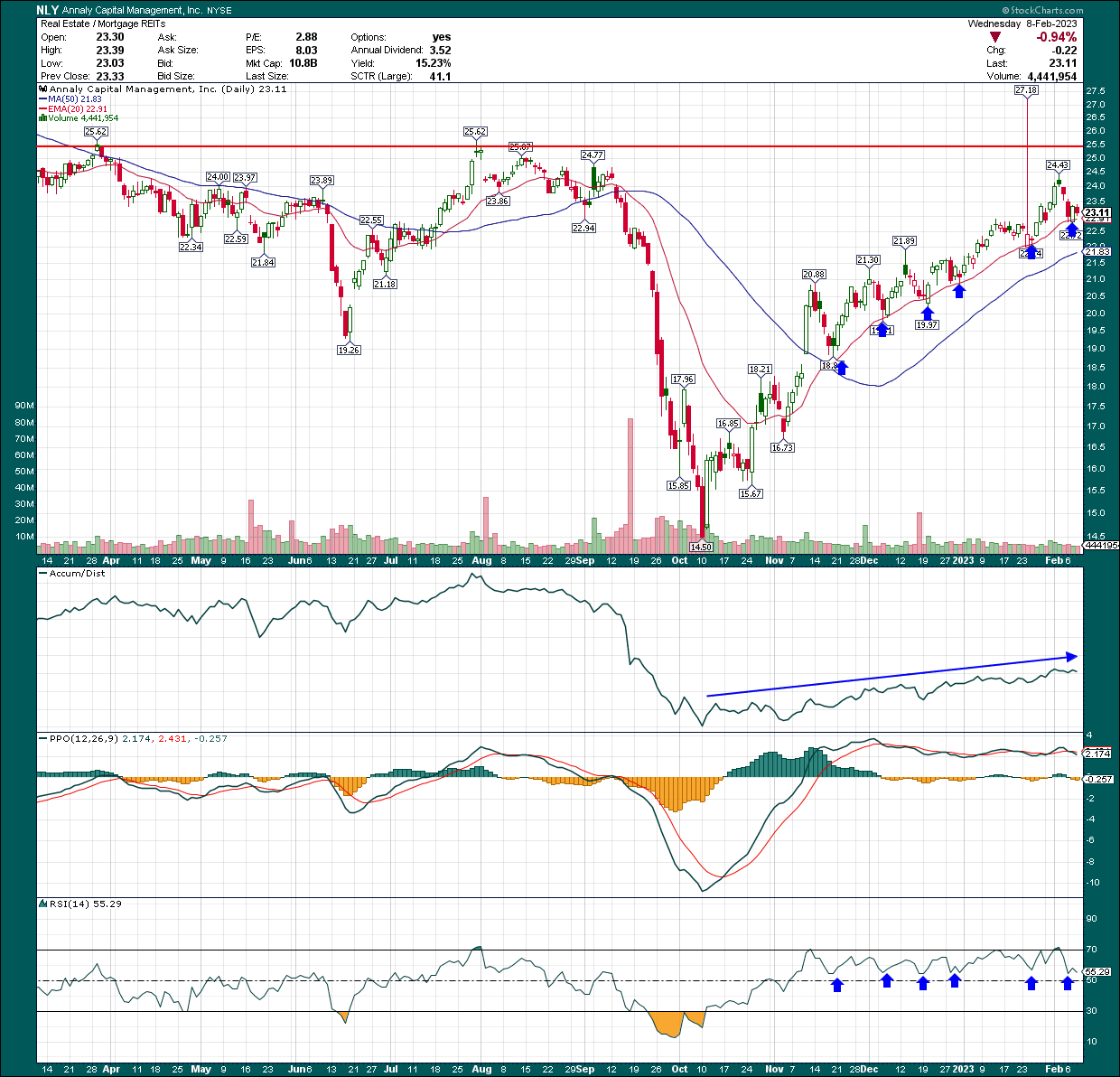

Let’s begin with the chart for Annaly, and get a sense of the technical outlook before we have a look at the fundamentals.

StockCharts

Annaly has been in an extremely impressive uptrend since October, with no less than six successful tests of the rising 20-day exponential moving average. Strong, up-trending stocks tend to rally off the 20-day EMA, and there are few examples that are better than the above. The 50-day simple moving average is sharply upward-sloping as well, so from that perspective, Annaly looks great.

I would have liked to have seen the accumulation/distribution line move toward its highs, but it’s not really that close. It’s not critical the A/D line makes new highs, but it’s a fairly good predictor of how sustainable a rally is, and it doesn’t look very good.

The PPO also topped out months ago while the stock has continued to rally, and like the A/D line, while this isn’t critical, it certainly helps with ensuring there’s enough bullish momentum to keep the rally going. Momentum on the PPO waned a long time ago, so I’m wondering when the bulls will run out of steam.

Finally, the 14-day RSI has tested the 50/60 area several times, which again, is bull market behavior. On this measure, it looks great. Should this fail, and we get a sub-50 reading, that’s probably a good indication the rally is done.

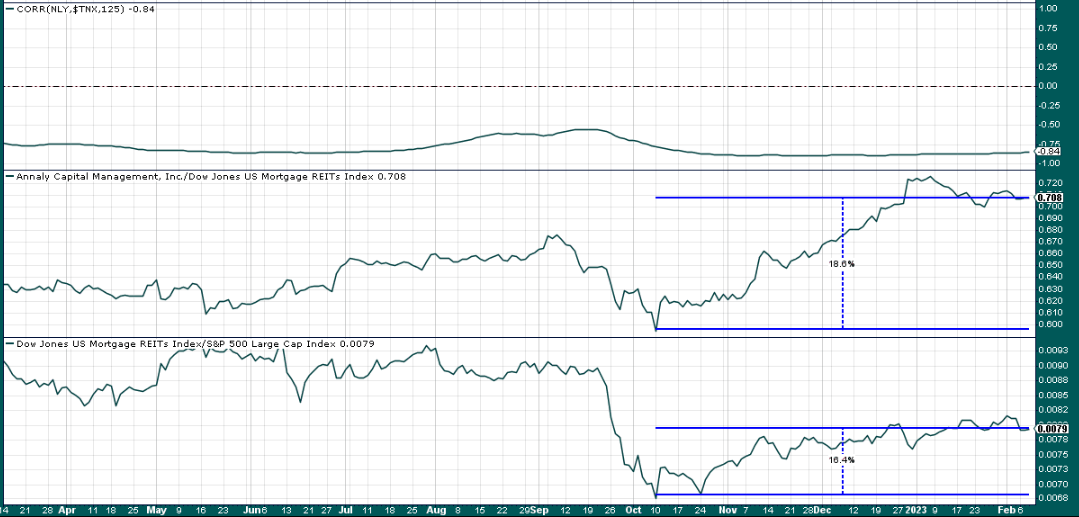

Now, let’s take a look at relative strength and the stock’s correlation to interest rates. On relative strength, Annaly has been predictably outstanding, given what we saw with the price chart above. It has outperformed REITs by ~19% since October, and in turn, REITs have outperformed the S&P 500 by ~16%.

StockCharts

In the top panel, we can see the stock’s correlation to the 10-year Treasury yield, which I’ve plotted over 125 days. That’s a six-month view of correlation (assuming ~21 trading days per month), so it’s a medium-term look. We can see NLY correlates extremely negatively to the 10-year yield, so it makes sense to look at that to see if we can get any clues as to the direction of NLY. In other words, given this correlation, we can reasonably expect the 10-year yield and NLY shares to move in opposite directions.

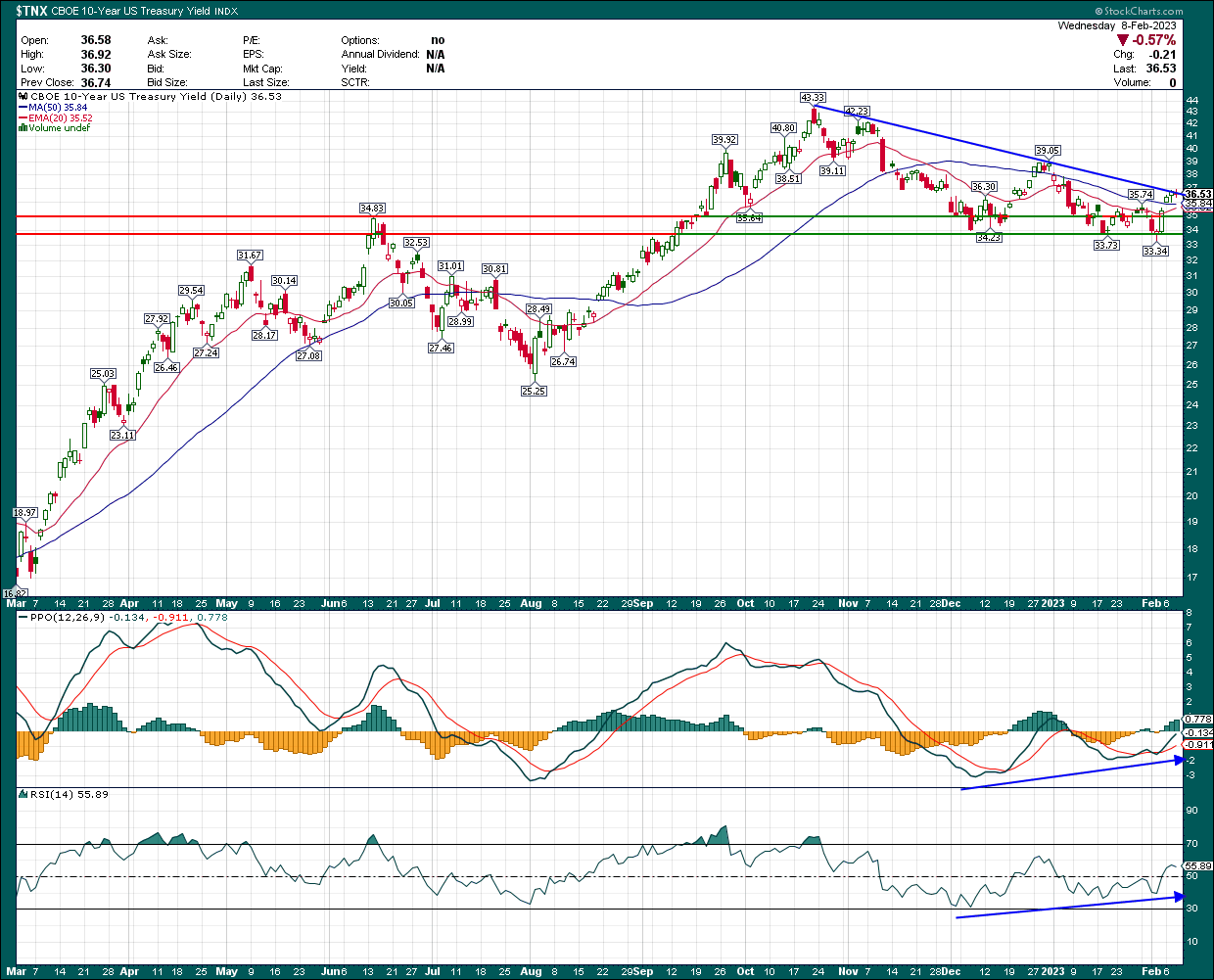

There are a few things going on here, so let’s start with the price chart itself.

StockCharts

There’s a zone of support around 3.4% to 3.5%, which was formed with the June 2022 high, and three subsequent tests since then. However, we also have a downtrend line in blue that the yield is testing currently. How this descending triangle resolves will signal the next big move for rates, and therefore, mortgage REITs.

Right now, yield has upside momentum so if I had to bet, I’d say we’re more likely to break out higher from this triangle. But the key here is that if we break out, rates are likely to move meaningfully higher, which would be negative for NLY, and if we fail the 3.4%/3.5% level, that would be a positive for the stock given the negative correlation we looked at. The 10-year yield is at a critical point right now, so we should get a resolution quite soon. I am not saying yield is definitely going to move higher, but right now, the chart looks, in my view, more likely to continue higher than break down at the moment. The point here is that from a risk management perspective, there’s far too much evidence for my liking that NLY will be negatively impacted by rates in the coming weeks/months.

Let’s now turn our attention to the fourth quarter report and outlook for NLY.

A decent quarter from Annaly Capital, but not great

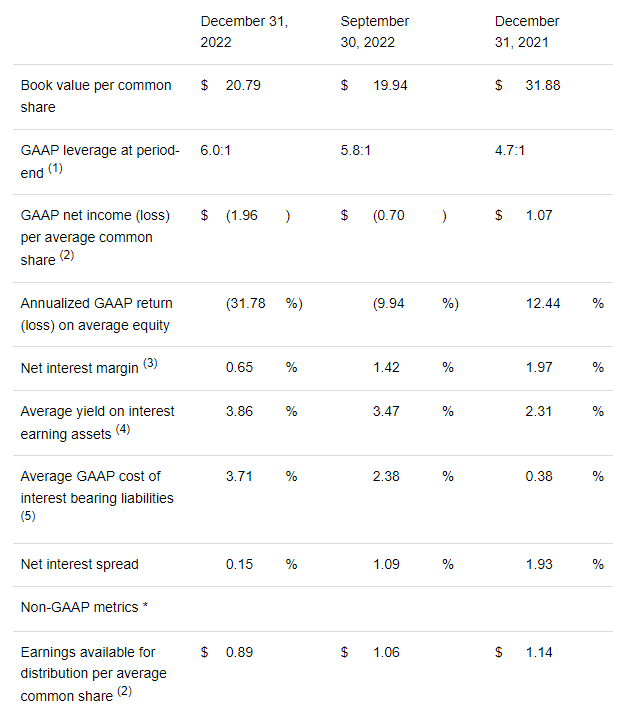

Annaly’s earnings came in essentially as expected, with earnings available for distribution at 89 cents per share. That number was $4.23 for the full-year, and the REIT declared $2.20 per share in dividends last year. That’s good for a 9.5% yield on a TTM basis, so Annaly retains its title as a terrific income stock.

The economic return for the quarter was 8.7% but was -23.2% for the year. Book value ended the year at $20.79 per share, which puts P/BV at 111%.

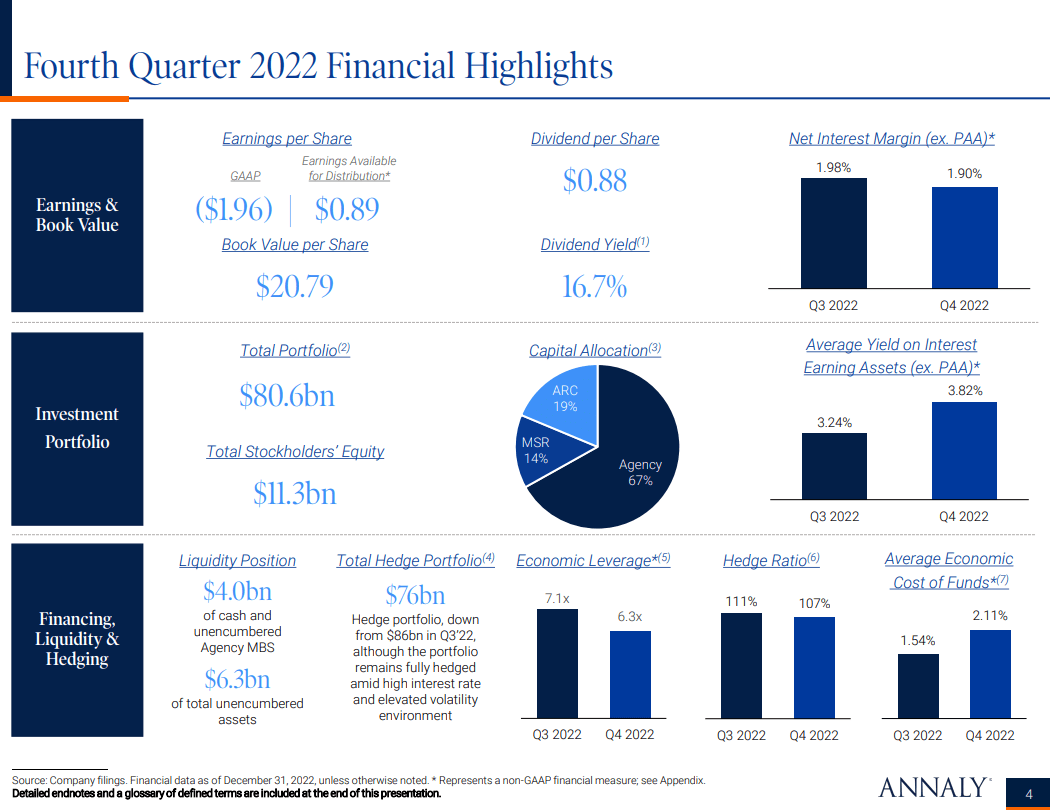

Net interest income declined both quarter-over-quarter and year-over-year, however, which brings me to where I’m becoming a bit concerned for Annaly’s ability to grow distributable earnings in 2023.

Investor presentation

Economic leverage was reduced from 7.1X to 6.3X QoQ, and while average yield on interest-earning assets rose, so did cost of funds. Indeed, net interest margin fell from Q3 to Q4 despite prevailing rates being quite elevated relative to the past decade. That saw funds available for distribution decline from $1.06 in Q3 and $1.14 in the year-ago period to the 89 cents we looked at earlier in Q4.

The way that I’m looking at this, Annaly needs yields to break down and move lower for these numbers to improve in the early part of this year. Will that happen? Perhaps, but we don’t have a resolution on that just yet. And if the yield breaks out higher, I think there could be a meaningful downside for Annaly shares. Again, this is about risk management.

Seeking Alpha

I won’t read this table to you, but it’s instructive in terms of showing where Annaly struggled in Q4, particularly in net interest spread, which almost disappeared entirely. These numbers will almost certainly get a lot worse if yields move up further, so that’s a big risk, in my view.

NLY is an expensive stock with risks

Here’s the problem; Annaly has put in a massive rally in the past few months, which means it’s pricing in a lot of optimism. I also noted that momentum hasn’t looked that great in terms of the share price, which can often indicate waning bullish enthusiasm.

The stock is very negatively correlated with long-term interest rates, and the 10-year is at a critical crossroads right now in terms of determining the next big move. That, in turn, is a big risk for Annaly. Rates could break down and be a boon for Annaly, but they could just as easily make new highs, and that would see significant deterioration in Annaly’s ability to generate spread, which has already materially worsened.

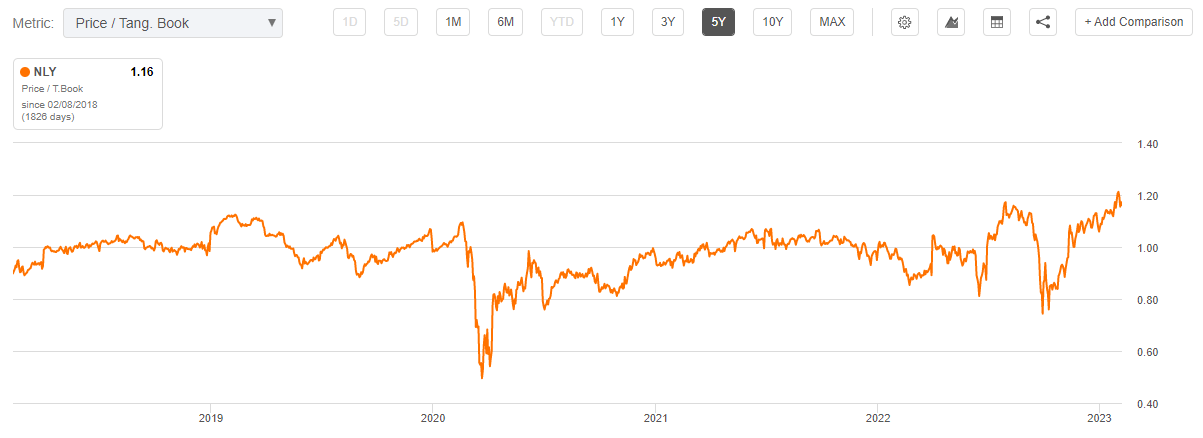

The issue is that the stock is also now more expensive than it has been for the last five years on a price-to-tangible-book-value basis.

Seeking Alpha

Shares are 116% today, having been about 80% at the start of the big rally. The stock was cheap then, but it is anything but that today.

The bottom line on Annaly is that the REIT saw a meaningful deterioration in its ability to generate spread from its investments in Q4, and given the combination of where rates are (and could be going), and the valuation, I think the risks of holding Annaly are way too high.

I certainly would not short here, but I do think that if you have owned it during this rally, this is a great place to take profits and move on. History has proven that owning Annaly at 115%+ of tangible book value is anything but prudent, and that’s where we find ourselves. If you want to own Annaly post-Q4 results, I think you’ll get the chance to do so at a price much closer to book value, or perhaps even below it.

Be the first to comment