When we wrote about Annaly Capital Management Inc (NYSE:NLY) recently, we warned investors that the facts were pointing to a crushing defeat for the bull case. That crushing was going to come from an extreme interest rate spread compression and you were likely to get more than your fair share of dividend cuts in 2023.

Today your yield on original cost has dropped to 5.9% (from 10 years back). We will bet it will be a lot lower when 2023 is done.

Source: 3 Reasons To Be Bearish On Annaly For 2023

NLY reported its Q4-2022 results and we checked out how the thesis was progressing.

Q4-2022

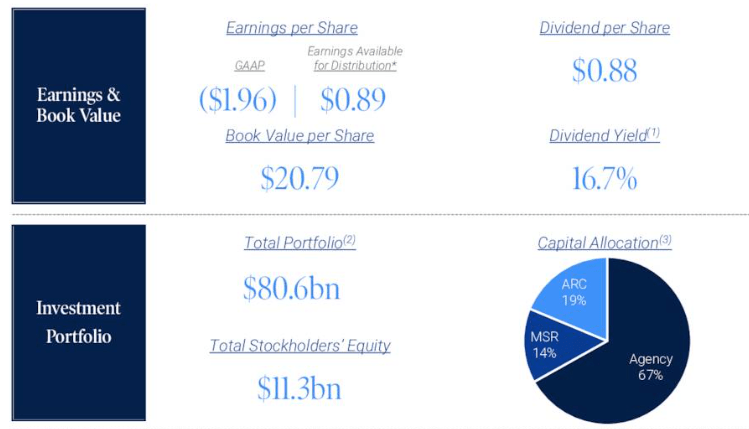

NLY reported a book value per share of $20.79, which was about in line with our estimates. The portfolio continued to be weighted towards high quality assets with less than one fifth allocated to non-agency credit.

NLY Q4-2022 Presentation

The bounce in tangible book value also allowed NLY to lower its economic leverage back into its historic range. As investors are aware, in Q3-2022 NLY’s leverage had moved over 7.0X.

NLY Q4-2022 Presentation

Overall quarterly results held little in the way of surprises for anyone who examined the company’s setup going into the fourth quarter.

Outlook

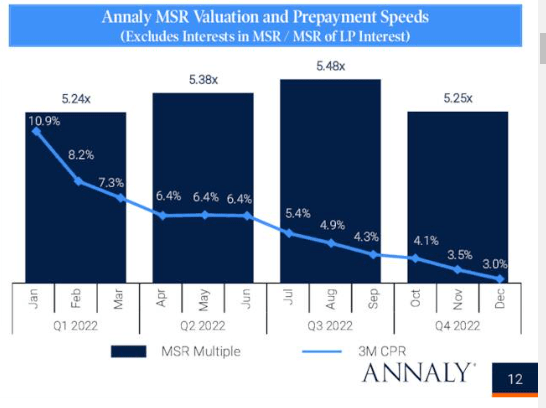

NLY’s MSR segment continues to do best today as pre-payments have slowed to a crawl. This means that the costs of acquiring and servicing a mortgage are spread over a longer period of time and result in more profits.

NLY Q4-2022 Presentation

NLY has expanded this area over time and you can see how much larger we are in Q4-2022 vs Q1-2021.

NLY Q4-2022 Presentation

While this may be a good thing today, we see this as a source of another risk down the line. The portfolio is marked at peak valuations for the MSR side. Today things are about as good as it gets and no one wants to prepay their mortgage. Down the line, should we have interest rate cuts, things will get dicey for this segment and it will likely be a source of losses for book value.

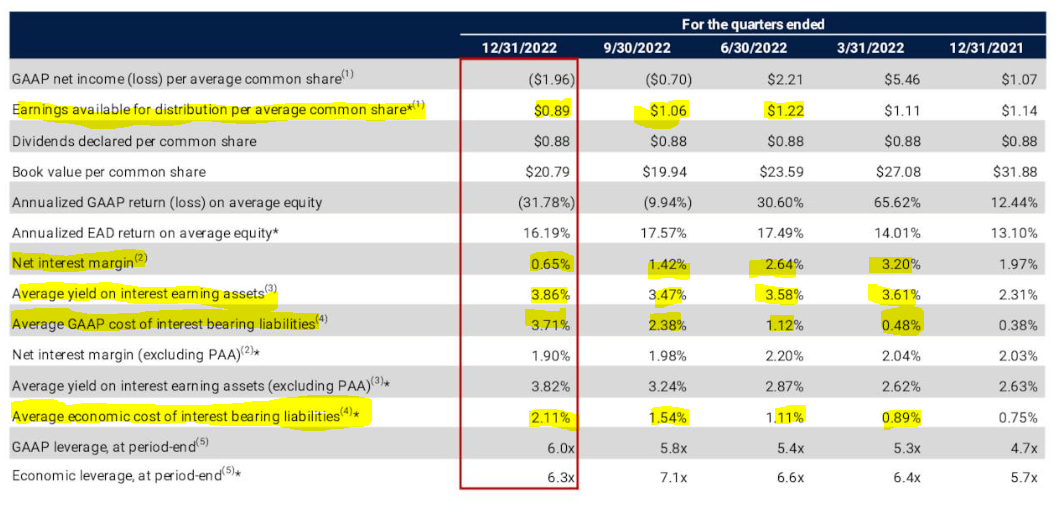

While that is a future issue, the bread and butter of NLY’s existence is the spread income. We have highlighted a few relevant numbers in the slide below and will go through them briefly.

NLY Q4-2022 Presentation

NLY’s “earnings available for distribution per average common share” is easily the most watched metric for dividend hawks. Keep in mind that this is a complex to calculate, non-GAAP number. There are also some forward assumptions built into this. Nonetheless, it is one that comes directly from the company and offers the best glimpse into how well they are covering their dividend. As is clear in the chart, that number peaked in Q2-2022.

So the bulls have to first answer how in the world is NLY posting a lower number here if this is the best time to be a mortgage REIT?

The rest of the highlighted numbers are great for answering that question. Going sequentially down, we can see that,

1) Net Interest Margin peaked in Q1-2022 and is down 80% from that level.

2) Average yield on earnings assets is up, but the move is extremely modest. This number has gone up just 7% over the last 4 quarters.

3) Average GAAP Cost Of Interest Bearing Liabilities is up more than 670% since four quarters back.

4) Average Economic Cost Of Interest Bearing Liabilities is also up but this lags the previous number thanks to hedges.

To these straight facts we will add that NLY’s GAAP cost of interest bearing liabilities moves with a one quarter lag to actual interest rate movements. So We are seeing the impact of July 2022 to September 2022 interest rates in this number. NLY’s average economic cost of interest bearing liabilities lags the above metric by another 1-2 quarters. This is due to the big hedges that are on the book and take time to roll off. In the interim they prevent that number from rising too quickly. So the take is simple.

Net Interest Margin should compress further in Q1-2023 and likely could go negative in the quarters ahead. Average Economic Cost Of Interest Bearing Liabilities will rise quicker than the GAAP Cost Of Interest Bearing Liabilities as hedges run out.

Verdict

As we see 3-4 quarters ahead, we think NLY is setup for the most hostile climate for mortgage REITs. We will see very strong compression of the interest spread, which has been held up due to lag and hedges. We think NLY will be lucky if they can manage their own distribution metric to come above 50 cents in 3 quarters. NLY also sees the direction if not the extent and telegraphed the next dividend cut.

Now before handing it off to Serena, I wanted to make one last point as it relates to earnings available for distribution. While we generated EAD that covered our dividend this quarter, we witnessed the moderation discussed in recent quarters, and we anticipate some further pressure on EAD going forward.

As a result, subject to determination by our Board, we expect to reduce our quarterly dividend in the first quarter of 2023 to a level closer to Annaly’s historical yield on book value of 11% to 12%, which compares to the approximately 16% yield on book we are paying today. We believe this decision allows us to appropriately manage the portfolio within conservative risk parameters while also delivering a more sustainable yield that is competitive with the peer set and broader fixed income benchmarks, which has always been our objective.

This first step looks setup for the dividend to go to 60 or 65 cents. We told you this 5 months back.

We project that based on forward curves, it will be very difficult for NLY to make money in 2023 and a new dividend, likely around 15 cents a share a quarter will be implemented in Q2 or Q3. This would be 60 cents a share based on the reverse split that comes into effect soon.

NLY gets the following dividend safety rating on our proprietary Kenny Loggins Scale.

Trapping Value

A “Call Kenny Loggins” rating implies a 90% plus probability of a dividend cut within 12 months.

Source: The Lost Decade Behind And The Challenges In 2023

Revisiting that dividend history from 10 years back, your yield on original cost will now drop to about 4% after NLY implements this next dividend cut. We are extending our prediction here that even that 60 cents a quarter is going to very difficult to maintain in 12-14 months. Buyer beware. We continue to rate this a Sell.

What About The Preferred Shares?

NLY has three sets of preferred shares currently.

1) Annaly Capital Management, Inc. 6.95% PFD SER F (NYSE:NLY.PF)

2) Annaly Capital Management, Inc. 6.75% PFD SER I (NYSE:NLY.PI)

3) Annaly Capital Management, Inc. 6.50% PFD SER G (NYSE:NLY.PG)

NLY.PF has started floating is at LIBOR + 4.993%. This will put abnormally high pressure to redeem but the shares are priced for it.

Seeking Alpha

NLY.PG is now about 45 days away from floating at LIBOR +4.172%. This one is unlikely to be called any time soon so the current high price represents an abnormal risk in the next rate cutting cycle.

NLY.PI begins floating at LIBOR plus 4.989% on June 30, 2024. Again, we don’t see this well priced for the risks ahead considering it is trading at $23.51.

At present neither the common shares nor the preferreds look extremely appealing, but we would still favor the preferreds on a relative basis.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment