marchmeena29

After raising interest rates by 75 basis points four times in 2022, the central bank eased off the gas in December, raising rates by only 50 basis points. However, this does not imply that the Fed is becoming more dovish.

In fact, persistently high inflation is expected to push interest rates to new highs in 2023, exposing mortgage trusts like Annaly Capital Management, Inc. (NYSE:NLY) to greater net interest spread headwinds.

Widening mortgage-backed security spreads and a steeper interest rate curve pose risks for Annaly, and the trust’s valuation has recently run ahead of itself, in my opinion. The 16% dividend yield that Annaly promises is associated with very high risks, and I believe the stock will soon return to a discount valuation.

Spread Challenges

Mortgage trusts use short-term borrowing to purchase mortgage assets. As a result, the business model necessitates trusts incurring significant debt on their balance sheets in order to purchase mortgage securities.

Trusts like Annaly can generate a net interest spread by purchasing mortgage securities with debt. A net interest spread is the difference between asset yield and funding costs. Because the size of the spread affects a trust’s profitability, it stands to reason that they benefit most from low interest rates. When a central bank changes its policy (as it did in 2022 due to skyrocketing inflation), interest rates rise, and the math shifts.

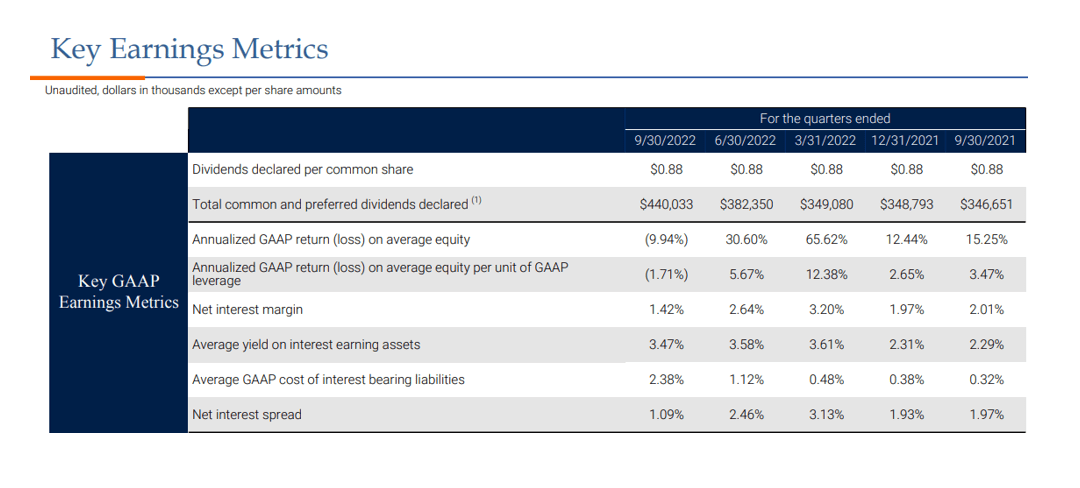

Annaly has long benefited from low interest rates, but as rates rise, the trust is seeing increasing pressure on its net interest rate spread in 2022, a trend that is likely to continue in 2023. Annaly’s net interest spread fell significantly in the third quarter, from 2.46% in 2Q-22 to 1.09% in 3Q-22, owing primarily to higher interest costs (which more than doubled to 2.38% QoQ).

Since the central bank has clearly indicated that it will remain hawkish, investors must expect an ongoing contraction in Annaly’s net interest margin.

Key Earnings Metrics (Annaly Capital Management )

An Evaluation Of The Chart Profile

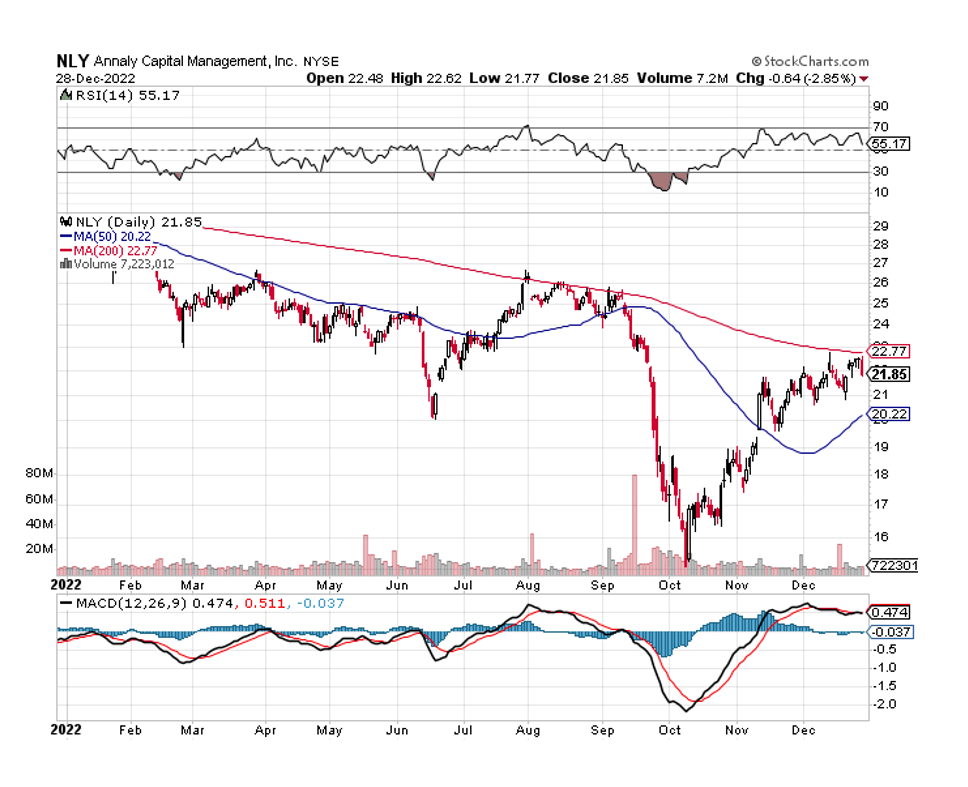

Annaly has made a significant comeback since hitting bottom in October, with the trust’s stock up 45% since then. However, the recovery has recently encountered some stumbling blocks, as Annaly’s stock price was rejected at the 200-day moving average line, the same line that prevented Annaly’s breakout in August, September, and December.

Even though Annaly’s stock is technically in neutral territory, the failed breakout above the 200-day moving average line is a negative trend signal that could indicate the formation of a new down channel.

Moving Average (Stockcharts.com)

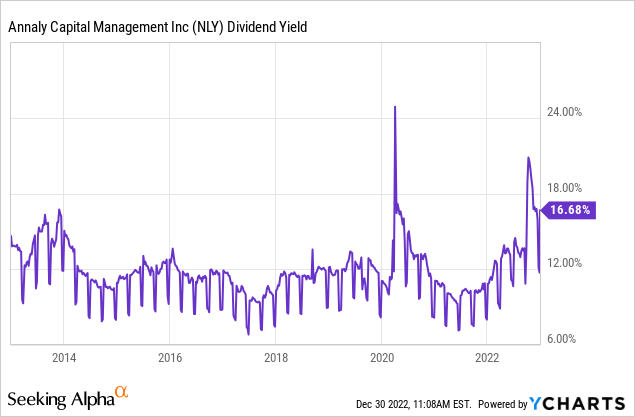

Yield Above Historical Average

Annaly currently has a dividend yield of 16%, which is significantly higher than the company’s historical average. Given the risks posed by rising interest rates, I believe investors have overpriced Annaly, and I expect the yield to fall back to the 10-12% range in 2023.

Annaly Now Trades At A Premium Valuation

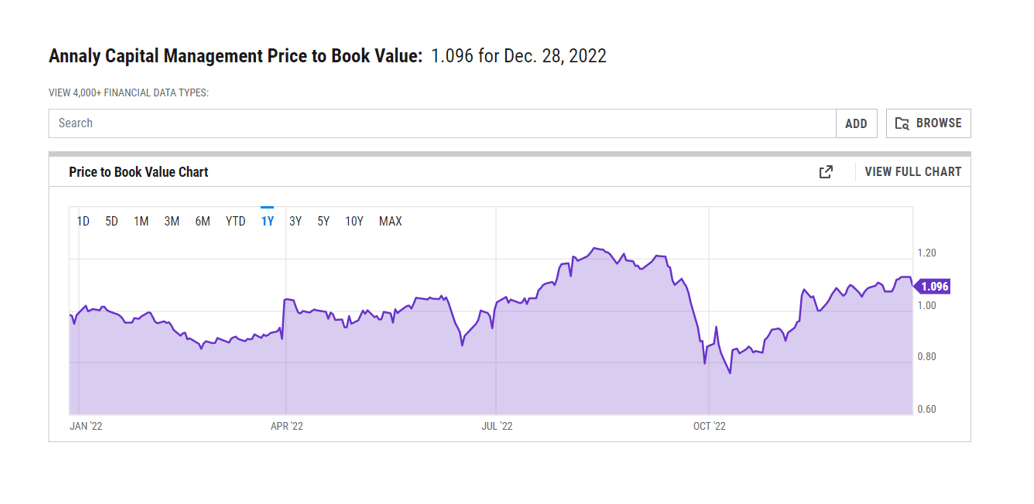

Annaly was able to close the gap between the trust’s book value ($19.94 as of September 30, 2022) and the stock price thanks to the October-December upside retracement. Annaly even returned to a 10% premium valuation in December.

However, given the risks to Annaly’s net interest margin and portfolio value in a rising-rate environment, I do not believe NLY deserves to trade at a premium to book value. Rather, given that the interest rate curve is expected to steepen further in 2023, I believe a 10-20% discount to book value is more appropriate.

Price To Book Value (YCharts)

Why Annaly Could See A Higher Valuation

A new round of interest rate hikes in 2023 is likely to put additional pressure on MBS spreads as well as mortgage-related portfolios. An unexpected increase in inflation could be a headwind for the mortgage trust sector as a whole, as well as for Annaly.

Higher interest rates pose a challenge to Annaly’s net interest spread, which is determined by asset yields on the one hand and borrowing costs on the other. If funding costs rise faster than asset yields, Annaly’s net interest margin and portfolio value could fall significantly by 2023.

My Conclusion

After a significant upside retracement that resulted in Annaly Capital Management, Inc.’s discount valuation becoming a premium valuation, I would caution investors against purchasing Annaly’s sky-high 16% dividend yield.

As long as inflation remains above normal levels, the central bank is likely to keep raising interest rates in 2023, potentially resulting in a lower net interest spread.

In this environment, and with the very real risk of additional jumbo-sized rate hikes in 2023, Annaly Capital Management, Inc. and other mortgage trusts that rely on large amounts of debt do not deserve to trade at a premium to book value.

Be the first to comment