Edson Souza/iStock via Getty Images

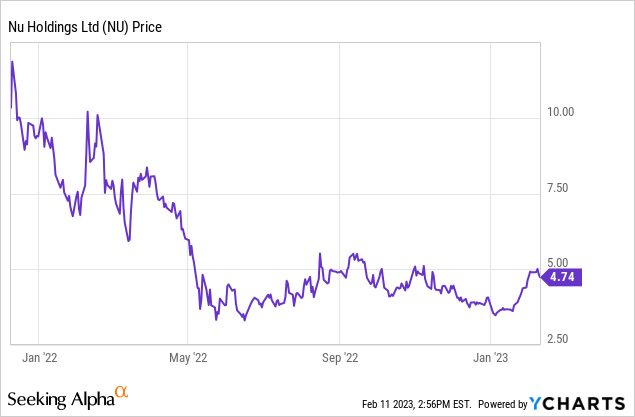

Nu Holdings (NYSE:NU) is a splashy digital bank from Brazil which has now spread to many Latin American markets. It had a high-profile IPO at the end of 2021 but shares have sunk considerably since then. Today, we’ll examine whether shares are a buy at this newly discounted price:

What Is Nubank’s Unique Value Proposition?

The company is a digital bank and has the sort of business model you’d expect when hearing that identification. As such, I will dive right into specifics rather than focusing on the broader industry. Two notes. First, my analysis is influenced by reading transcripts of calls with numerous ex-Nu employees and people that worked at rival financial organizations through the Stream by Alphasense research organization. Second, while I don’t have any experience with Brazil’s financial system, I am a Colombian resident and have observed Nu and rival banks in the Colombian market for quite some time.

According to former Nu employees, the main draw of the company is its credit card product. While Nubank, nowadays, offers a wider variety of different financial tools within its app, the credit card is the main driver for attracting new business.

This makes sense. After all, in Brazil (like most of Latin America), it can be very difficult to obtain loans or credit products. The big legacy banks tend to only extend credit to the top quartile or so of society.

In Colombia, for example, people are sorted into social strata, ranging from 1-6, and the big banks almost exclusively do business with people that are 5s or 6s. If you are below 4, forget about trying to get good service within the traditional banking system.

How does this play out for Nubank? It is willing to offer starter credit cards to the lower group that the rest of the banking system views as undesirable clients. Nubank starts out with these folks with smaller credit limits to reduce its risk. Over time, if the client pays their bills on time, they get access to a wider range of credit products and bigger credit limits.

The second key feature is that Nubank doesn’t charge a monthly fee for the credit card in most cases.

In addition, Nu eats the little taxes and fees that governments put on financial transactions, instead of passing them on to customers. That’s a huge difference from most LatAm banks which nickel-and-dime for absolutely everything.

Many South Americans choose not to get a savings account or credit card, even if it might be useful, because they are worried about being hit with monthly expenses or hidden fees merely for having the product line open. Nubank helps reduce this friction and open up the banking system to folks who would otherwise view it as not obtainable.

Nubank’s Early Edge May Be Fading

I believe Nubank had more success in its home Brazilian market due to first-mover advantage whereas its subsequent launch in countries like Colombia has been less successful.

Nu achieved a tremendous amount of success through word-of-mouth marketing. Back in, say, 2015, the idea of a free credit card for the middle class was a truly novel idea in the LatAm market. Nowadays, however, there are more digital banks offering a similar product. Additionally, the legacy banks have started to adjust their portfolios to respond.

I found one exchange between an analyst and a former Nubank product manager interesting.

The analyst asked why the big banks in Brazil still have positive net promoter scores “NPS” whereas the big banks are reviled in America. Here’s the former Nu product manager’s answer:

“The incumbents are not bad. Their product works okay. They started to invest a lot of money after Nubank and neobanks became a real threat.

Back in 2016, 2015, they used to laugh about Nubank and say, “Yeah, we are so big that you’re never going to have enough relevance for us.”

Now, the [big Brazilian banks] offer a quite good service. They started to remove some hidden charges. They used to charge for a lot of random things. They are not doing that anymore.”

That’s capitalism in action right there. Nubank rightly saw a problem in the banking market and leapt in to great initial success. However, the big banks reacted and changed their procedures enough to head off this threat before it started taking away their core customers.

As the big banks reacted, Nubank arguably started to take more risk to keep its own customer numbers and lending levels increasing. A former employee spoke about the company increasing its eligible base greatly in 2020, at the height of the pandemic, as other lenders pulled back.

This gets to the crux of the matter. More than half of Brazilians either have a bad credit history, or no credit history at all. These are people that most banks simply aren’t going to touch regardless of other extenuating factors.

Is Nubank making a smart move trying to be the bank of last resort for these folks – even during a potential economic bust of unknown proportions? If it works, it could go down as a brilliant gamble. But it’s a risk nonetheless.

This approach to community involvement extends to employees. Nubank has spent more freely on employee compensation, including lavish restricted stock units (RSUs), than other Brazilian rivals such as StoneCo (STNE).

This hasn’t been such a problem recently, given that Nubank’s stock price has declined. However, if shares go up, expect significant dilution. Also, note that Nubank may have to pay employees more in cash salary and bonuses going forward, given that all these RSUs have dramatically decreased in value over the past year.

There’s a worthwhile philosophical debate over employee compensation and investing for growth. That said, in current market conditions, a company like StoneCo’s focus on profitability is more likely to be well-received than Nubank’s path of running operating losses.

I could go on with other observations, but I want to jump straight to what I see as the biggest hurdle that Nubank has to overcome going forward.

I can summarize the issue with just one exchange with a former Nubank product manager:

“Analyst: What do you think’s been tough for Nubank? What challenges or hurdles have they faced?

Product Manager: I think the company struggles a lot with the upper [class] segments, especially because the upper segments are really well-served by Brazilian big banks.

Nubank goes well with middle-class and lower markets to put people in the financial systems, but they struggle with the upper market. Their limits are too low. Their rates are not so [attractive], even with people with investments with them. If people that earn more than 10,000 Real ($2,000) salary a month, it’s not worth it for them to have Nubank. They could get more advantages in other companies.”

Let me restate that point. As per this expert, for anyone making more than $24,000 per year, it doesn’t make sense to use Nubank. Anyone that is more prosperous than that gets more benefits from a traditional Brazilian bank. I expect that basing a business around its current client base will cause Nubank to always struggle with profitability.

Following up on that, Nubank might simply not have the range of products necessary to attract wealthier clients. If you only need a low limit credit card, great, go with Nubank. But how much money are you going to make servicing a credit card with a $25 or $50 credit limit anyway?

Even in emerging markets, from what I’ve heard, it costs a surprisingly high amount per year to keep a bank account open and in regulatory compliance. This adds up across tens of millions of accounts.

The real money is in getting people to move their whole financial life to Nubank, but that’s hard when it lacks so many more specialized financial services that are harder to run solely through an app.

Nubank works great for younger consumers that just need a credit card or other simple product. But as people move up the wealth strata, it gets harder. The legacy Brazilian banks have a huge edge in products such as home mortgages, car loans, insurance, and remittances/foreign money transactions.

That sums up the reasons for skepticism around Nubank as a model. So, let me throw on my contrarian hat and argue the bull case for a minute.

The Alternate View: If I’m Wrong, Here’s How Nubank Wins

While I’m skeptical of Nubank, I do think there’s something there. The company has developed a large customer base, and it has legitimately good technology compared to most incumbent banks. It also has better operational chops than even other neobanks that in turn sought to copy Nubank. The firm has a defensible position.

I’m skeptical this becomes a highly profitable business anytime soon. But, make no mistake, there is a viable business here. This isn’t one of the legions of busted SPACs with a bad balance sheet that is going to $0.00 when the next recession hits. Nubank has a business with commercial traction and a legitimate shot at success.

For one thing, Nubank is already around breakeven profitability. Breakeven isn’t great – especially in what’s been a good year for LatAm economies. You’d like to see them make some money when local economies were posting double-digit GDP growth in 2022. But breaking even is a lot better than running minus 40% operating margins as many American FinTech/neobanks have been prone to doing. Nu isn’t another generic FinTech SPAC incinerating Silicon Valley money at breakneck speed.

Nubank’s reliance on stock-based compensation makes me nervous that they will dilute shareholders significantly, especially if the stock price remains depressed for an extended period. But, there’s a huge difference between stock dilution and running out of money entirely. As Nubank has already reached more-or-less breakeven operational results, they have time to play the long game. Unlike most FinTech firms, Nubank doesn’t need much more outside capital, and thus it has more flexibility and – importantly – staying power.

The Generational Shift

I don’t think Nubank will ever be able to steal the current generation of, call it, 40+ year-olds with money that like banking at LatAm giants like Itau, Santander, BBVA, Bancolombia, and so on. That group is set in its ways.

What Nubank can do, however, is keep signing up more 25 and 30-year-olds that are professionals with currently modest incomes. In ten years, maybe those folks start to get promotions and earn a lot more money. By then, hopefully, Nubank adds competitive car loans, insurance, and other such services into the app. In, say, 2030, Nubank can start to be that all-in-one bank for millennials and Gen Z as their spending power increases.

The issue, at least for foreign investors, is that few fund managers have the patience to play a slowly unfolding demographic shift like that. The biggest way that financial assets shift to different banks is due to demographics. The evolution of assets from financial firms will be a long slow process driven by inheritances and the passage of time.

So where does this all leave us?

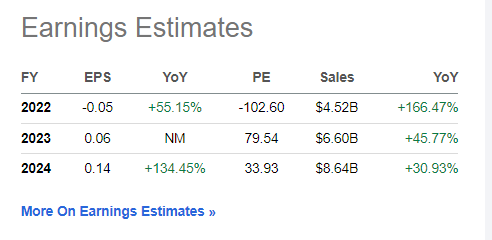

Here are the analyst estimates for Nu going forward:

Nu earnings estimates (Seeking Alpha)

If Nubank can hit the earnings consensus, they’d actually be trading at 34x earnings in 2024 which isn’t terrible. Do I think they’ll hit these numbers? Probably not. There’s a lot of assumption of margin lift in those figures which I won’t believe until I actually see it.

That said, the business can continue to run in its present state for an indefinite period. There’s no ticking clock or last-ditch equity raise needed to keep the firm viable. That alone puts Nubank ahead of most of its FinTech peers.

I’m not sold on the model working yet. But management has proven to be intelligent up to this point and built a competent organization. For a 5+ year time horizon investor, this is hardly the worst pick you could come up with in the financial innovation space. That said, I would expect shares to have an extended period here in the low-to-mid single digits before the bull case really starts to potentially play out.

Be the first to comment