PonyWang

Analog Devices (NASDAQ:ADI), a leading provider of analog and mixed-signal semiconductors, is renowned for its superior margin and capital return performance, which is enabled by its highly efficient “fab-lite” production model. This model not only supports the company’s long-term dividend growth strategy, but also its commitment to repurchasing material amounts of its own stock.

Over the years, Analog Devices has continued to expand and strengthen its product portfolio through a series of strategic acquisitions. These acquisitions have given the company not only the ability to offer a diverse range of products tailored to various vertical markets but also the scale necessary to maintain industry-leading margins.

Despite the inherent cyclicality of the semiconductor industry, Analog Devices stands out as a relatively safe choice for investors seeking a combination of attractive capital returns and steady growth opportunities.

This article will delve into one of ADI’s businesses, strategy, risks, financials, and valuation to give readers a more comprehensive understanding of the potential risks and rewards of owning the stock.

Note: This article is for educational purposes only and does not constitute financial or investment advice. Please do your own due diligence and consider your unique financial needs and constraints before buying any stock.

Business

ADI 2022 Investor Day

Analog Devices, Inc. is a global technology leader in the design, manufacture, and marketing of a broad portfolio of high-performance analog, mixed-signal, and digital signal processing (DSP) integrated circuits (ICs) used in virtually all types of electronic equipment. The company was founded in 1965 and is headquartered in Norwood, Massachusetts.

The company has consistently invested in R&D and technology to stay ahead of the curve and offer customers the most advanced and reliable products. Additionally, Analog Devices has pursued a strategy of growth through strategic acquisitions, including the acquisition of Hittite Microelectronics in 2014, Linear Technology in 2017, and Maxim Integrated in 2021. These acquisitions have expanded the company’s product offerings and enabled it to offer a wider range of solutions to customers in various markets.

ADI 2022 Investor Day

Analog chips are integral in transforming real-world signals such as sound, temperature, and pressure into digital signals that can be processed by computers. Our analysis posits that Analog Devices holds a robust competitive advantage, characterized by its proprietary analog designs and the elevated costs associated with customer switching. Unlike several other semiconductors, analog chips are not prohibitively expensive to produce, nor do they necessitate the utilization of cutting-edge manufacturing processes. This allows high-quality analog chip manufacturers to maintain their design wins and retain favorable pricing and strong profitability, as long as the end product is in production.

Strategy & Transformation

ADI 2022 Investor Day

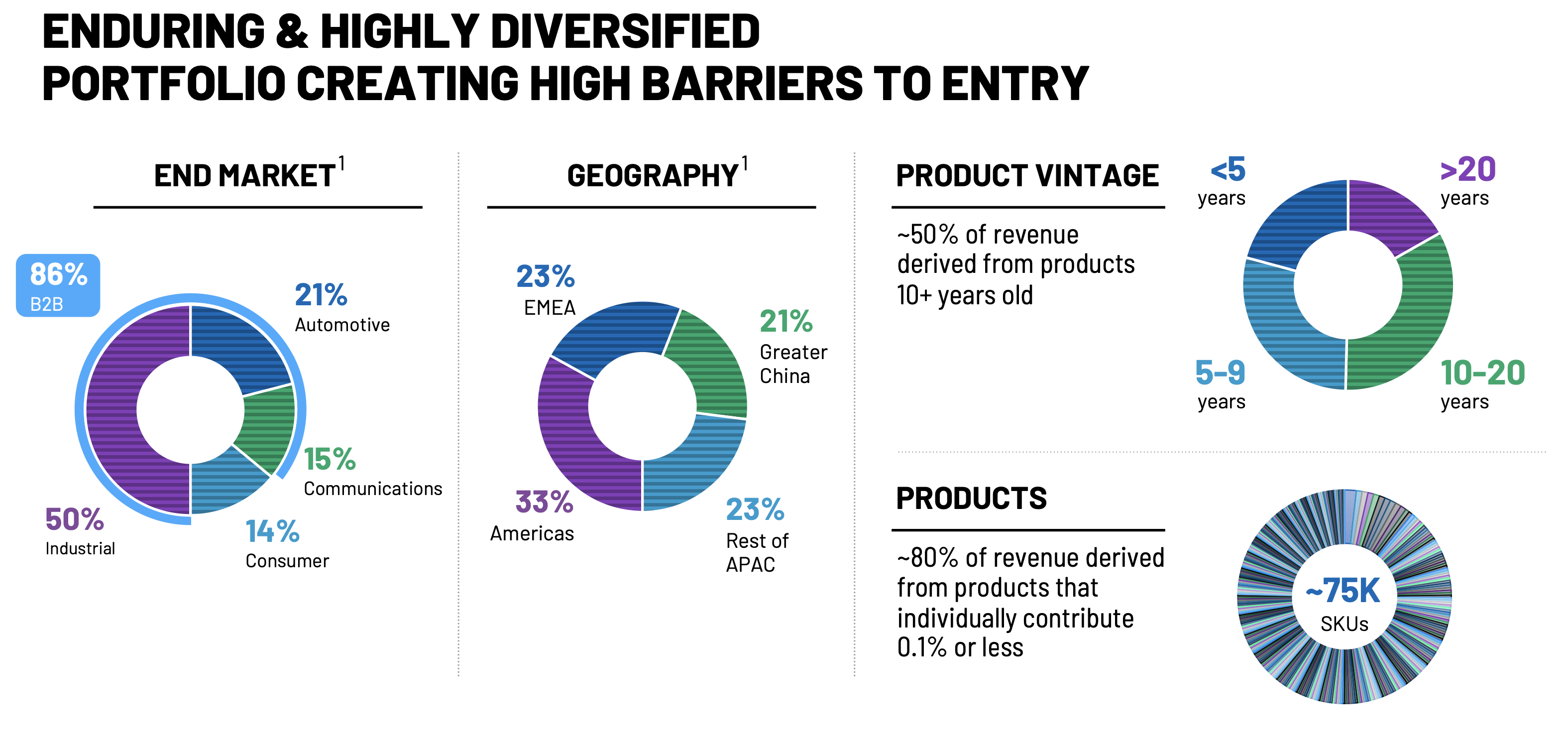

Approximately a decade ago, the company was known for its technology story as a leader in data converters. These converters act as a bridge between the physical and digital worlds. However, the company decided to position itself at the heart of the B2B sector with a focus on industrial applications, which currently make up approximately 50% of its business. Additionally, the company has targeted the most attractive segments of communications, including base stations, wireline connectivity, backhaul and metro long-haul for optical systems, as well as the automotive and consumer industries.

The company has reconfigured its R&D stream to tackle the most pressing problems in these areas. With a focus on innovation, the company covers a wide range of applications and has 75,000 product SKUs, which increased to 100,000 with the acquisition of Maxim. The company invests $1.5 billion in R&D annually and differentiates itself through its innovative solutions and added value to the semiconductor industry.

The company leverages customer intimacy and innovation to drive its growth forward. Over the past decade, the company has increased its average selling prices by 4 to 5 times, driven by its desire to manage customer complexity and develop more sophisticated solutions. Today, the company is well-positioned with momentum on the innovation and customer engagement fronts.

With more concurrent secular growth drivers than at any point in the past, the industry is poised for growth. As the company pushes towards the epoch of the intelligent edge, it is better positioned than ever before in its history.

ADI 2022 Investor Day

Financials & Valuation

ADI 2022 Investor Day

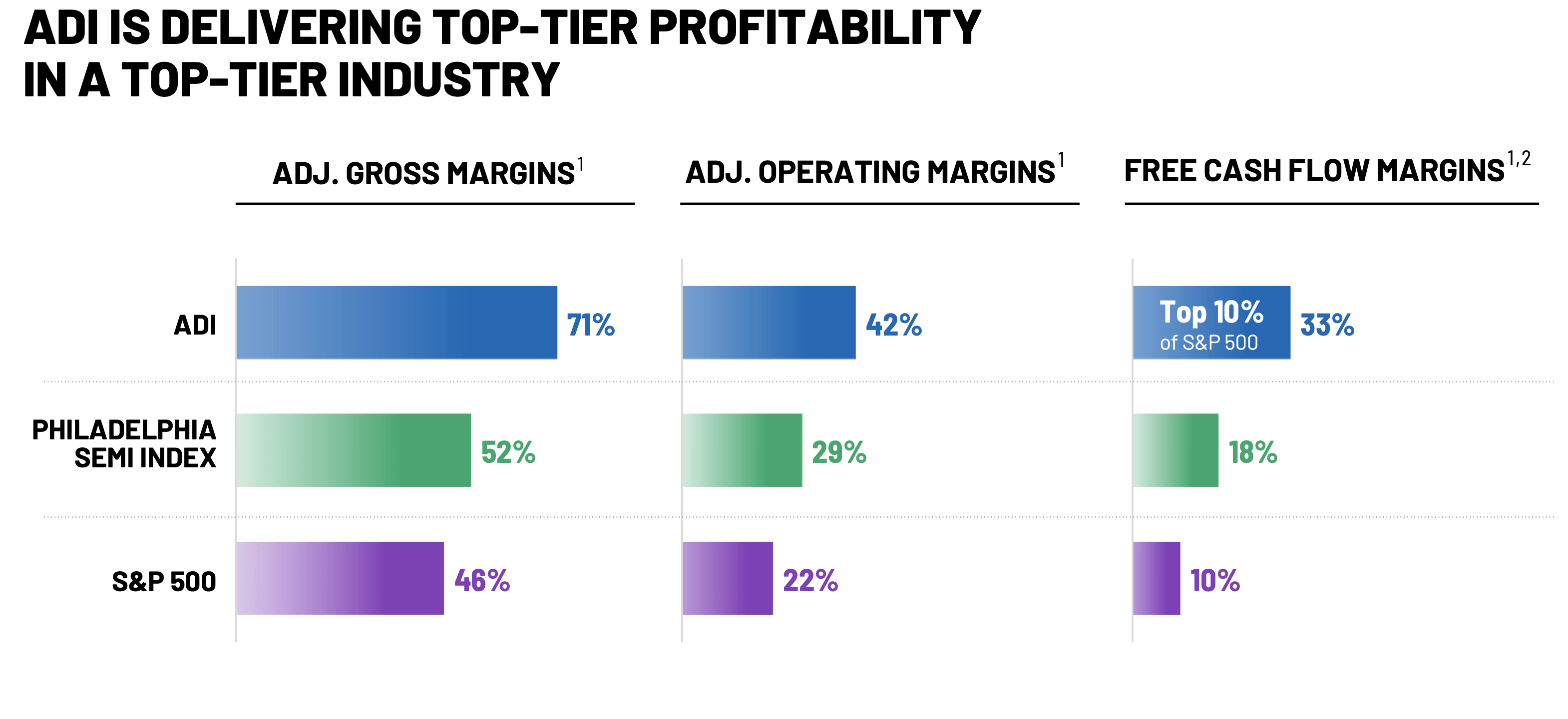

Analog Devices has a proven track record of financial stability and performance, thanks in part to its capital-efficient business model, diverse customer base and portfolio. This model, combined with the company’s significant scale advantage and its focus on the mature and comparatively slow-growing analog market, has allowed Analog Devices to consistently achieve industry-leading gross, operating, and free cash flow margins. This solid financial foundation has provided stability and dependability for investors even during market fluctuations.

ADI 2022 Investor Day

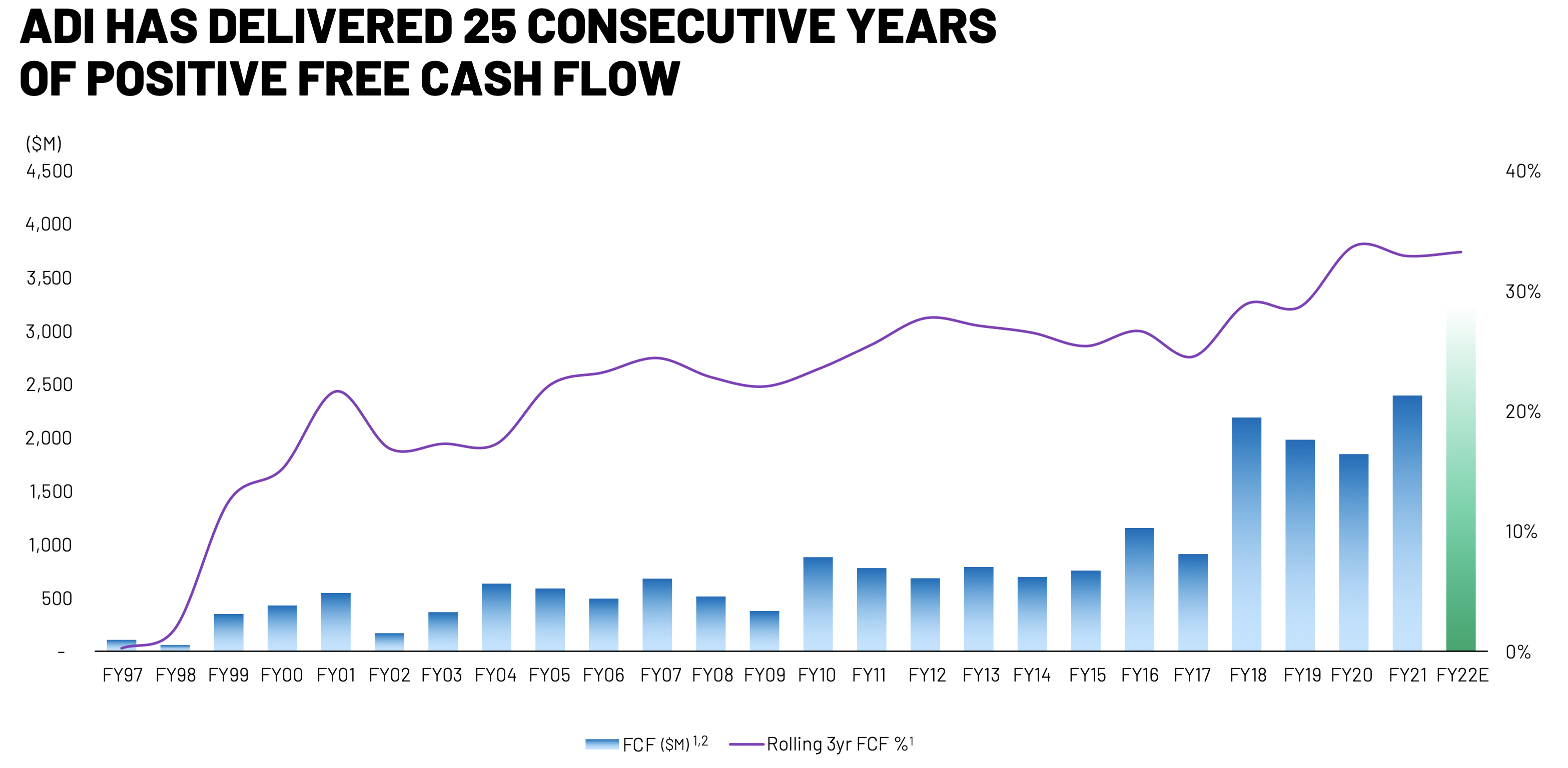

Despite the cyclical nature of the semiconductor industry, the company has demonstrated remarkable stability, with 25 consecutive years of positive free cash flow. This record of dependability is a testament to the strength and resilience of Analog Devices’ business model, and it has earned the company a reputation as a reliable and trustworthy investment opportunity. Investors can be confident that, despite fluctuations in the broader market, Analog Devices will likely continue to deliver strong and steady financial performance, driven by its broad portfolio of products and its well-established position in key end markets.

ADI 2022 Investor Day

In fiscal year 2022, Analog Devices Inc. experienced significant growth of 64% due to a full year contribution of revenue from the recently acquired Maxim Integrated, as well as strong demand for the company’s products amidst the global chip shortage. However, we expect a slowdown in revenue growth in the next two fiscal years, primarily due to macroeconomic concerns, and predict growth of flat to low-single-digits in fiscal 2023 and 2024.

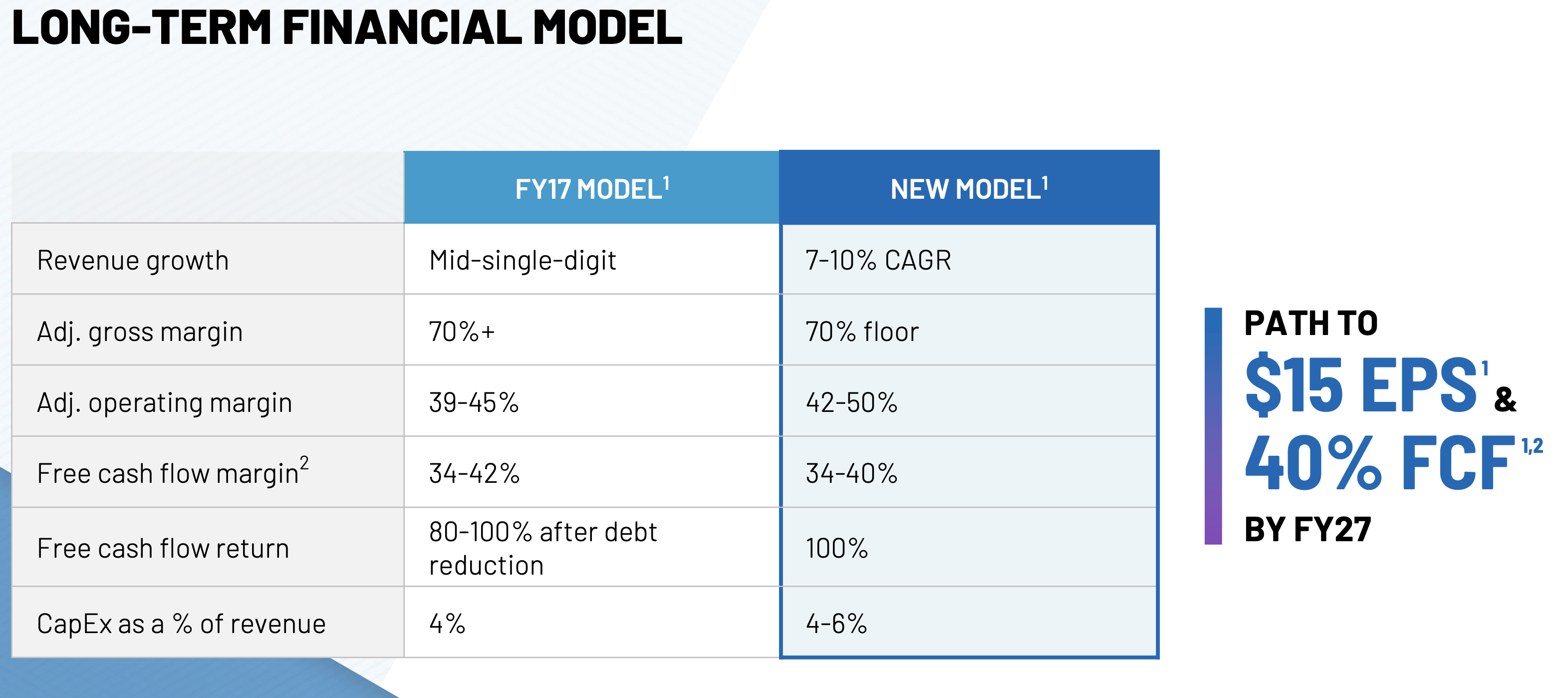

If the company reaches its “new model” targets, the company could grow 7-10% per year through the cycle. This robust growth is expected to be driven by the increasing electronics content in the automotive and industrial sectors, as well as near-term benefits from the 5G wireless infrastructure buildouts.

In fiscal 2022, the company achieved a remarkable adjusted operating margin of 49%, driven by elevated sales levels, full utilization of internal factories, and a favorable chip pricing environment. However, we expect this margin to decrease in the upcoming fiscal years due to difficult comps and a weakening macroeconomic environment. We note that the company’s long-term operating margin target of 42-50%, implying a mid-cycle target of 46%. In a global recession scenario, we would expect operating margins to be towards the low-end of this target range.

However, based on consensus projections, it is estimated that the company will experience a moderate decline in its operating results, reaching 48.3% in the fiscal year ending October 2023 and 48.4% in the fiscal year ending October 2024. Given the company’s target margin range of 42-50% and the negative outlook on the global economy, we believe there is a significant risk that the consensus numbers may not be met.

Trading at 17x forward 1-year earnings per share, ADI may seem somewhat discounted compared to its 5-year range of 14x to 27x. However, it should be noted that there remains significant potential for downward adjustments to projected EPS, rendering the supposed discount an illusion. Given the rapidly changing macroeconomic environment, it is not advisable for us to make a projection for 2023’s EPS. Our assessment suggests that the risk is skewed towards a downward adjustment.

Risks

Overcapacity

Several leading companies in the semiconductor industry, including Texas Instruments (TXN), Analog Devices, STMicroelectronics (STM), Infineon (OTCQX:IFNNY), onsemi (ON), and NXP (NXPI), among others, have declared their plans to significantly increase their capital investments in the near future. This move follows the recent capacity constraints which have resulted in a rise in pricing. Nonetheless, it is important to consider that there has been some observed weakness in macroeconomic indicators and crucial end-demand verticals. If the demand environment weakens more than expected, the industry may be plagued by overcapacity, inventory buildup and weak pricing.

Negative Revision

The company aims for an operating margin of 42-50%, with a mid-cycle target of 46%. In case of a recession, margins are likely to reach the lower end of the target range. Despite consensus projecting a moderate decline to 48.3% in FY23 and 48.4% in FY24, the risk to these numbers is high due to the unfavorable economy and the company’s target range.

Geopolitical

As a leading player in the semiconductor industry, Analog Devices Inc. faces a potential impact from the ongoing geopolitical risks between its home country, the United States, and China. With 21% of the company’s revenue being generated from China, any escalation in trade tensions could result in a shift in customer preferences towards neutral European-based competitors or domestic Chinese analog suppliers. This could potentially affect Analog Devices Inc.’s market position and financial performance in the region.

Conclusion

ADI’s strong financial performance in a cyclical industry is commendable. Its growth strategy, including organic investments and M&A, has broadened its customer base, market reach, and product portfolio. We anticipate ADI to continue delivering dependable results. However, investors should be aware of emerging risks such as increasing industry capacity investments amid a potential global recession, optimistic earnings estimates that may not align with the company’s guidance or the weakening macroeconomic environment, and geopolitical uncertainties as 21% of ADI’s revenue comes from China.

Given these risks, we believe the risk-reward balance for investing in ADI’s stock is balanced and will wait for a more favorable entry point before making a move.

Be the first to comment