Sundry Photography

Despite scaring investors last quarter by saying that they were seeing some order cancellation, Analog Devices (NASDAQ:ADI) reported an impressive fourth quarter, delivering revenue of $3.25 billion with all markets growing sequentially. For fiscal 2022 revenue was $12 billion, operating cash flow $4.5 billion, and free cash flow $3.8 billion. Free cash flow was 31% of revenue despite a record $699 million in capital expenditures. The company is committed to growing free cash flow to 40% of revenue. Adjusted EPS increased nearly 50% to $9.57 for the year, and for the quarter it came in at $2.73, up 58% y/y.

Analog Devices continued to make heavy R&D investments, to the tune of $1.7 billion in fiscal year 2022, and it also had significant capex of roughly $700 million. The reason for this capex was to increase its manufacturing output. In 2023 the company is expecting it will once again invest aggressively in its US and European factories to significantly expand capacity. Analog Devices continues improve its balance sheet, ending the quarter with approximately $1.5 billion of cash and equivalents and a net leverage ratio below 1x.

Growth

For the year growth was fairly balanced, with about half coming from increasing average selling prices to counter inflationary pressures. While growth came from many different places, one thing that management shared that we found particularly interesting was that growth in automotive was underpinned by battery management systems, which now has an opportunity pipeline nearing $4 billion.

The company also reported that the design pipeline is beginning to benefit from cross-selling ADI’s and Maxim’s portfolios. In part thanks to these revenue synergies, management feels confident in their ability to bend the growth curve and move from their historical mid-single digit growth rate to a long-term model of 7% to 10%.

Order Cancellations

The big news last quarter was that the company was seeing a slight moderation in demand and an uptick in order cancellations, which they thought might climb in the current quarter. This quarter, however, management sounded a lot more optimistic.

They said that while the uncertain and slowing macroeconomic environment has had some impact on demand, after a couple of months of slowing orders they saw bookings stabilize at what they consider relatively normal levels. It also doesn’t hurt that they are gaining market share in general, so they are having some tailwinds that counter some of the macroeconomic weakness.

During the most recent earnings call CFO Prashanth Mahendra-Rajah addressed the cancellations issue reported last quarter, hinting that it is no longer an issue:

Let me just make a comment on cancellation. So we provided cancellations as a metric that we watch in the third quarter because we wanted to give everyone some context that we saw an inflection happening with orders. So it was in the spirit of transparency. However, I don’t want to get into a pattern of reporting cancellation data every quarter. So if it was something meaningful, we would have called it out, which we didn’t. So you can read that for what it is.

I would say that unlike others in the industry, we are proactively analyzing our backlog and working with customers to remove orders that they no longer want given the rapidly changing environment. So this strategy for us is to seek out cancellation. It helps us align our backlog with current demand, and it really gives us better visibility into where the supply needs and what we need to build. So that has increased our confidence in the quality of the backlog we have. It is still — the coverage is out still over a year, but it is down sequentially. And so while we’re always mindful that there can be some continued noise in that backlog, we feel pretty good about both the guide and as we mentioned, the near term.

Guidance

The outlook for the next quarter is good, with the company guiding first quarter revenue to $3.15 billion, plus or minus $100 million. Consumer is expected to be a weak segment, probably down double digits sequentially. At the midpoint of their guidance, revenue should be up high teens y/y. Management is expecting Adjusted EPS to be $2.60 plus or minus $0.10. One of the reasons they are optimistic about the coming quarter is that orders are stabilizing and they have a backlog that extends out 12 months.

Valuation

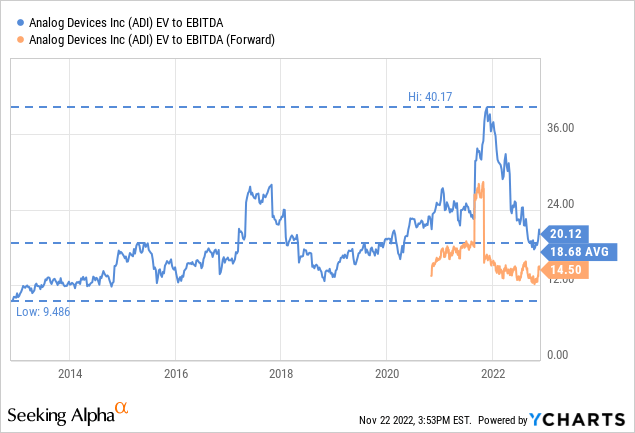

We believe that given the quality of the company, including its excellent revenue growth and outstanding profit margins, a forward EV/EBITDA of ~14.5x is quite reasonable. Another way to think about the valuation is comparing the current market cap of ~$86 billion to the free cash flow generated in 2022 of ~$3.8 billion, which results in a 22.6x multiple, or seen another way, a ~4.4% free cash flow yield.

Analog devices is targeting a 100% free cash flow return to investors, which should result in a growing dividend and generous buybacks. The company aims to raise its dividend, currently yielding a little under 2%, at a 10% CAGR through the cycle, with the remaining cash used for share repurchases.

Risks

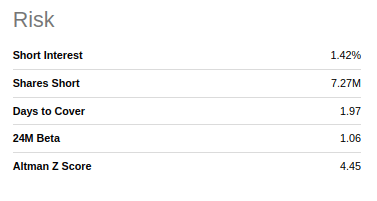

The company was relatively leveraged after the Maxim acquisition, but has quickly de-levered, reducing risks considerably. Right now the balance sheet appears to be in good shape, profit margins remain very high, and the Altman Z-score is a solid 4.45x.

Some of Analog Devices end markets can be somewhat cyclical, but we are not overly concerned. The biggest risk might be the valuation. We believe the company is currently fairly valued, but without much in the form of margin of safety in terms of valuation.

Seeking Alpha

Conclusion

Analog Devices appears to be avoiding the chip downturn, after it delivered solid Q4 results. The strength of the results was particularly surprising given that the company had warned the previous quarter that it was seeing some order cancellations and a slight moderation in demand. We believe shares are currently fairly valued, and the balance sheet is now in better shape after the de-leveraging following the Maxim acquisition. Given the solid results delivered this quarter, and the optimistic guidance, we are upgrading our rating to ‘Buy’ from ‘Hold’ previously.

Be the first to comment