vzphotos

Amgen (NASDAQ:AMGN) has endeared itself to dividend growth investors by growing its dividends for 11 consecutive years, with the most recent hike announced in December being a 10% increase to $2.13 per share from the prior $1.94. AMGN has maintained a 5-year dividend growth rate of 11%, giving income oriented investors who’ve held on to the stock considerable downside protection against the raging inflation that hit the economy last year.

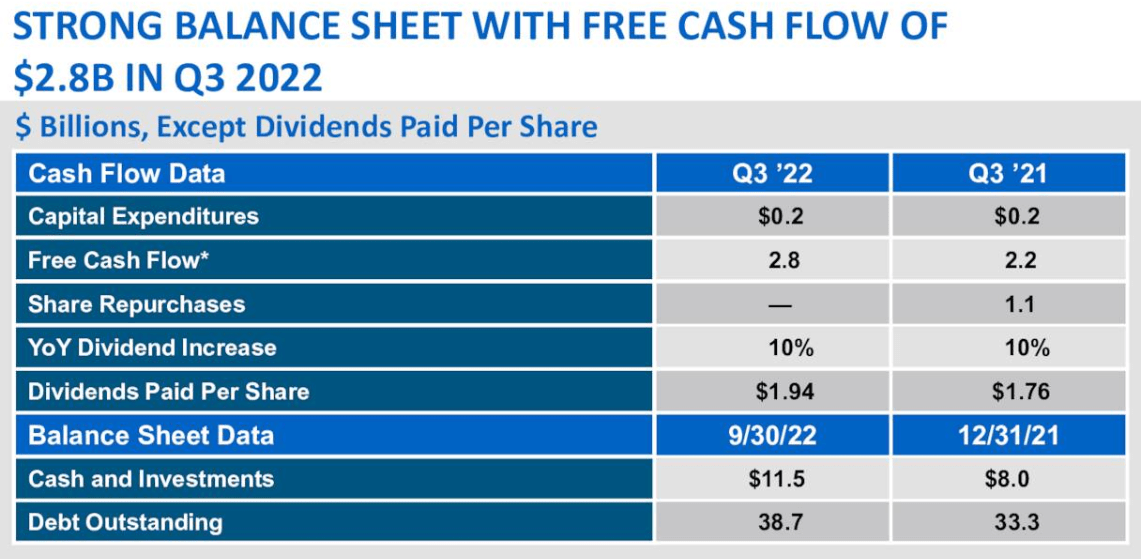

As a mega-cap biotech company with strong and reliable cash flows, AMGN can be counted on for regular dividend income. At the end of Q3 2022, it had free cash flow of $2.8 billion as the chart below illustrates.

Amgen Earnings Presentation

While AMGN’s regular dividends are almost assured in light of its strong balance sheet, what is less certain is whether the current strong pace of dividend growth can be maintained over the long-term. There is no crystal ball to tell this but there are a number of indicators that point to the likelihood of continued strong dividend growth.

Firstly, AMGN is pursuing opportunities through organic growth and acquisitions that could help it grow topline much faster in coming years. Secondly, AMGN has a compelling capital allocation strategy, which emphasizes returning capital to shareholders through dividends and buybacks. AMGN spent $6.4 billion on share repurchases in the first nine months of 2022 and its latest share count of 533 million outstanding shares represents a 26% reduction from 722 million shares in 2017. Fewer shares means higher EPS, hence faster share price growth and higher dividends per share.

Growth top on agenda

AMGN has around 26 brands treating a wide range of serious illnesses, including inflammatory diseases such as rheumatoid arthritis, severe asthma, stroke, heart diseases, cancer and others.

Enbrel, which treats arthritis, has been the company’s cash cow for a long time, bringing in $1.11 billion or 18% of product sales in Q3 2022, as per the company’s earnings presentation.

Like other biotech companies involved in the development of medicines, AMGN’s business model relies on ring fencing its portfolio through the use of patents which limit competitors from introducing biosimilars. These patents usually expire after several decades. With Enbrel’s expiry coming up in the next few years, the company has been hard at work to diversify its revenues by developing new drugs to offset the anticipated decline in Enbrel.

One new drug worth mentioning is TEZSPIRE, a severe asthma treatment that was launched in January 2022. According to Amgen CEO and Chairman, Bob Bradway, who spoke at the recent 41st J.P. Morgan Annual Health Conference, TEZSPIRE is “off to a great start, whether measured by the clinical effect of the medicine or by the broad prescriber base that is reaching for TEZSPIRE.”

AMGN’s pipeline also looks exciting, particularly its foray into weight loss therapies where it recently announced positive results for phase 1 clinical trials for its experimental weight loss agent AMG 133, noting that it caused up to 14.5% reduction in body weight in people with obesity and without diabetes.

If AMGN’s experimental weight loss drug gets to the commercial stage, it will compete with offerings from rivals Novo Nordisk (NVO) (OTCPK:NONOF) and Eli Lilly (LLY). The market for weight loss therapies is in my view big enough for these three and others, making AMGN’s experimental drug a potentially huge growth driver assuming all approvals are secured and it advances to the commercialization stage.

Acquisitions amid growing debt

It is difficult to grow a business of the scale of AMGN organically as it has already reached relative maturity. Revenues for FY 2023 are expected to come in at $27.32 billion vs $26.25 billion (estimate) for 2022, $24.29 billion in 2021, $24.29 in 2020 and $22.20 billion in 2019, highlighting the single digit topline growth over the past few years.

This slow top line growth makes it essential to look for acquisitions, something that AMGN has done relatively well in the recent past. In October 2022 it completed the acquisition of ChemoCentryx for approximately $3.7 billion. Through the ChemoCentryx deal, Amgen acquired Tavneos, a treatment for a very rare but serious disorder known as ANCA-associated vasculitis. This is an autoimmune disorder that leads to inflammation and can lead to the destruction of small blood vessels with serious consequences for those who are experiencing it. Despite the rarity of the disease, it’s possible that AMGN could find ways to expand its reach through its network of rheumatologists who it has worked closely with for many decades.

AMGN in December 2022 also announced the acquisition of Horizon Therapeutics (HZNP) for $27.8 billion. Following the announcement, SA contributor William Meyers wrote a great piece that comprehensively covered the details of the deal and why it was, in his opinion, a good move. While I agree with his conclusions, the concern for me is the price tag and the fact that AMGN is racking up some serious debt to close the deal.

The series of acquisitions that AMGN has made in the past few years have already resulted in a steady build up in debt. Its last reported total debt was $38.7 billion, a 27% jump from $30.4 billion in 2019. It will be important to see where debt levels settle if and when the deal closes in the first half of this year.

Give thought to margin risks

Besides debt, the other risk investors need to be mindful of is the fact that margins are under pressure across the pharma industry. This is because of the declining price of prescription drugs, which could come under further pressure with the implementation of the Inflation Reduction Act.

AMGN has in the past been keen to grow volumes to mitigate some of the impact of the price declines. Investors should watch this carefully to ensure that the company is able to continue growing volumes for affecting products. Currently, AMGN’s margins are comfortably high, with 75.78% gross margin, 50.99% EBITDA margin, and 25.96% net income margin. This is higher than the industry average, including its peer Gilead Sciences (GILD). The antiviral drug maker has a 47.07% EBITDA margin and 12.29% net income margin. AMGN’s high margins give it some cushion relative to peers.

Takeaway: Hold and buy the dips

Investors who have been invested in AMGN for a while have no reason to sell in my opinion. It’s a great source of income and decent capital gains, having gained 46% in five years. The dividend growth looks set to continue but the pace of growth could come under pressure if debt service costs spiral out of control or margins come under pressure, resulting in lower free cash flow. That said, it wouldn’t be advisable to add at current levels or initiate a position as AMGN seems fairly valued if not slightly overvalued. Its P/E (fwd) is 22.53x vs a 5-year average of 18.26x, meaning there could be some short-term downside risks that present buying opportunities.

Be the first to comment