dusanpetkovic/iStock via Getty Images

It pays to buy into companies with durable and economically essential attributes, especially when their growth stories are temporarily disrupted. Such I find the case to be with Americold Realty Trust (NYSE:COLD), which as shown below, had a fairly strong growth trajectory before being derailed in recent years. In this article, I highlight why patient investors may want to considering layering into the stock before growth picks back up.

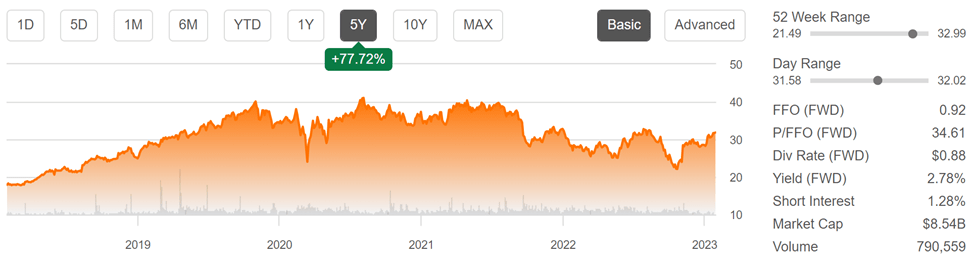

COLD Stock (Seeking Alpha)

Why COLD?

Americold is the world’s largest publicly-traded REIT that’s focused on providing cold chain storage solutions for food producers and end points, including grocery stores and distribution centers for restaurants. It’s has been in existence for over 100 years, and has a worldwide presence, including operations in North America, Australia/New Zealand, Europe, and South America.

At present, COLD has a portfolio of 245 properties, of which 194 are owned, 46 capital leased, and 5 are managed for a third party owner. COLD benefits from the “network effect” as cold storage is a critical element of the food supply chain, and having more facilities means that has the scale and capacity to serve large customers.

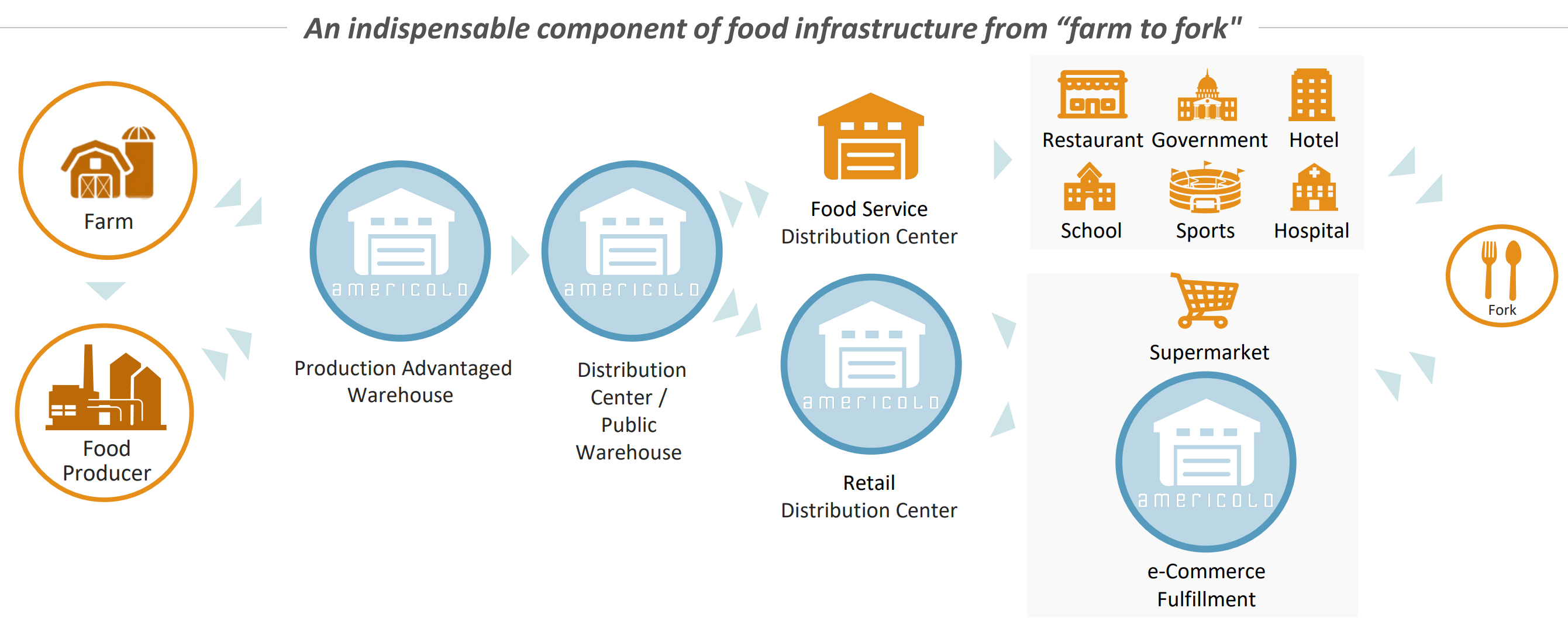

This is reflected by COLD’s 18% market share in North America, serving over 4,400 customers, which include some of the biggest names in food production and grocery, such as Conagra Brands (CAG), Kraft Heinz (KHC), Unilever (UL), Safeway (ACI), and Sprouts (SFM). The following illustration provides a good overview of COLD’s role in connecting “farm to fork”.

COLD’s Role (Investor Presentation)

Like many in the food industry, COLD hasn’t been immune to higher operating costs at its facilities amidst an inflationary environment, which pressured margins. However, it appears that COLD is ready to turn the chapter and is bouncing back as labor shortages have eased along with tempering of high inflation and wage growth.

This is reflected by Global Warehouse segment revenue growing by 10.5% YoY to $599 million during the third quarter. Encouragingly, margin pressures are starting to ease, as lower operating expenses contributed to GW net operating income growing at a faster rate of 15% YoY.

Looking forward to Q4 results, COLD should continue to see benefits to margin, as service price increases were done midway during Q3 and thus did not get a full quarter’s benefit. Moreover, management has implemented power surcharge initiatives during the fourth quarter, thereby expecting to cover all known inflationary effects during the fourth quarter.

Moreover, COLD is making good progress on filling more permanent roles, with lesser reliance on temp workers, which are less productive and cost more. Management has a long-term goal of achieving 80/20 mix between permanent and temp workers. This ratio currently stands at 72/28, which is higher than the 70/30 pre-COVID level.

Additionally, COLD has plenty of greenfield opportunities as the largest publicly traded player in the cold storage space, which gives it access to more sources of funding. Management highlighted two such newly opened properties in Europe during the recent conference call:

We are very pleased to announce that we recently opened two new facilities: one in Dublin, Ireland, and one in Barcelona, Spain. The Dublin facility is a Greenfield build at a 6.3 million cubic feet and 20,000 power provisioned. This building brings much needed capacity to a key market for Americold and was designed with features and technology to support the demand in this market including blast freezing, mobile racking and conveyor systems. Our Barcelona facility is an expansion project on land already owned by Americold that has 3.3 million cubic feet and 12,000 power provisioned into a critical distribution market.

Meanwhile, COLD carries a strong balance sheet to support continued growth, with significant liquidity of $700 million in available capital. It carries a BBB investment grade credit rating and has a net debt to EBITDA ratio of 6.5x, which is reasonable for a growth REIT. Moreover, 84% of COLD’s debt is unsecured and 80% is carried at fixed rates, giving it balance sheet flexibility, and it has a low weighted average interest rate of 3.7%.

Importantly, COLD’s dividend is well protected by an 80% payout ratio, based on the $1.10 AFFO per share that management expects to achieve for the full year 2022. while dividend growth has been lacking, I would expect for growth to pick up steam after near-term inflationary headwinds are worked through.

Lastly, I see value in the stock at the current price of $31.83, which equates to a P/AFFO of 28.9. While this may seem pricey on the surface, this has more to do with the margin headwinds that COLD has seen. Analysts expect these pressures to moderate and combined with external growth, COLD is expected to see double-digit FFO/share growth next year and thereafter. Analysts also have a consensus Buy rating on the stock with an average price target of $32.60.

Investor Takeaway

Americold is well-positioned for a continued rebound, with moderating inflation, and eye on cost containment, and price increases and power surcharges to customers. Plus, it’s made progress in shifting more towards permanent workers to drive operating efficiencies. While the stock may not see much near term upside, COLD’s essential positioning across the food landscape and its growth opportunities make it a good long-term buy at current levels.

Be the first to comment