DNY59

One of my readers mentioned American Financial Group (NYSE:AFG) as a promising investment. It was on my screens before but unless one follows filings closely, it is easy to miss opportunities in insurance. Superficially, most insurance stocks look similar to each other and straightforward metrics alone (like Price/Book, for example) are coming short. AFG turns out to be an interesting company.

AFG business

In May of 2021, AFG sold its annuity business and became a pure property and casualty company focused solely on commercial specialty lines. For a pure specialty carrier, it is sizable with GPW (gross premium written) of ~$8B in 2021.

P&C operations are split between 35 different businesses that make underwriting decisions independently while ultimately reporting to the centralized management. The scope of the insurance business is broad as follows from the slide below:

Company

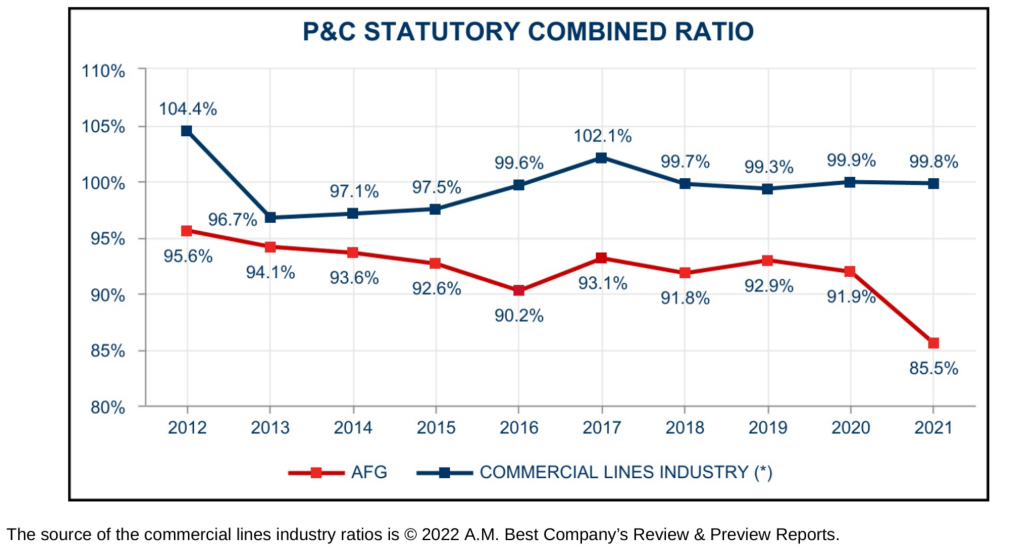

The main number for any mature P&C company is its combined ratio and AFG’s results attract attention immediately:

Company

AFG’s statutory combined ratio averaged 92.1% for the period 2012 to 2021 as compared to 99.6% for the property and casualty commercial lines industry over the same period. Since statutory accounting is generally more conservative than GAAP, GAAP combined ratios are slightly better.

Sometimes superior underwriting is achieved by limiting growth but this is not about AFG. Throughout 2012-2021, AFG’s CAGR for P&C lines only were 7.0% and 7.4% for GPW and NPE (net premium earned) respectively.

AFG reports two numbers for its earnings – EPS and core EPS. Core EPS does not take into consideration gains or losses from equities in the investment portfolio which is rather convenient for analysis. For 10 years (2012-2021), core EPS from P&C lines has grown at 15.1% CAGR. In 2022, AFG expects to make $11.25 in core EPS at the mid-point, slightly lower than in 2021. It means that currently, the stock is trading at P/core E~136/11.25~12, lower than the long-term EPS growth.

Please keep in mind that actual EPS, on average, should be higher than core EPS as over the long term, stocks in the investment portfolio appreciate. In 2023, analysts expect AFG to earn close to $12 per share.

The stock has been very rewarding for investors. First, since 2012, it has appreciated by more than 13% per year. Secondly, it has been paying generous dividends split between regular and special. It pays growing (for 17 years!) quarterly dividends and the current yield is close to 2%. However, it is huge special dividends that make AFG unusual. The company has a policy of paying out excess capital and over the last 5 years, it has paid out ~$46 per share in special dividends. Some of these special dividends are related to the sale of its annuity business and are not repeatable. If we sum up appreciation, and regular and special dividends, the annual long-term return becomes slightly above 20%, easily beating any relevant index. About 11% of it is due to the capital generated (growth in book value plus dividends) with the balance attributable to multiples expansion.

Why AFG is so successful

AFG’s success can be attributed to 5 factors:

- Conservative underwriting. As I mentioned this is a mandatory condition to hold any mature insurer. The low combined ratio is expected to be sustainable because the underwriting decisions are made independently in 35 niche unrelated groups. It is unlikely that underwriting prowess will deteriorate in many groups simultaneously.

- Profitable investing. AFG manages investments in-house and achieves strong returns primarily due to alternative investments. In Q3 22, the total portfolio was $14.3B with $2B in alts consisting of real estate, private equity, and private debt. About half of alt investments are multi-family properties. Alts are delivering disproportionately high net investment income – about 50% in both 2021 and 2022.

- Premium growth. It was achieved every year since 2012 with the only exception of 2020 due to the pandemic. The management continues to forecast consistent growth. At the end of 2021, AFG acquired a small fintech which is expected to form the core of the 36th underwriting group.

- Productive M&A activity. The company buys and sells underwriting groups regularly attempting to optimize the mix. The divestment of the annuity business in 2021 for P/B ~ 1.34 was a clear success.

- Strong management coupled with healthy insider ownership without super voting stock. AFG was founded by Carl Lindner, Jr. and his two senior sons serve as co-CEOs for 17 years. Altogether, the family owns more than 20% of the stock.

Valuations

At the end of 2012, AFG was trading P/Adj. BVPS of 0.9. Currently, this ratio stands at 2.6. There is no doubt that AFG is a high-quality and growing company but it might be already reflected in its stock price.

Perhaps, the best metric for the stock value is P/core EPS. It has been rather stable over the last 10 years with an average value of 12.8 and a standard error of 1.8 (both are determined using the end-of-year stock quotes). The current ratio is 12.1, well within its historic norm. What makes us circumspect, however, is that the combined ratios in 2021 and 2022 were well below the historic average – 86.4% and 84.9% respectively vs 92.4%. We do not know whether it is due to the hard market in specialty lines or a reflection of some long-term trend. But normalizing the combined ratio will make the stock less appealing as it almost halves the underwriting margin.

Good investing results due to alts may last. Other insurers have used alts productively for a long time and multi-family properties in particular should remain in demand due to the underbuilding of residential real estate. Last year, the National Association of Realtors issued a report with some relevant data. According to it, housing stock grew at an annual rate of 1.7% from 1968 to 2000, it grew by an annual rate of 1% over the past two decades, and just 0.7% over the past decade, resulting in an underbuilding gap of over 5.5 million units in the past 20 years. This has led to the crisis of affordable housing and multi-family properties are one recipe to alleviate it.

As we noted, AFG pays out excess capital in special dividends making them important for the stock value. After the recent big payouts, the level of excess capital is not that high any longer with only $100M ($1.16 per share) available for special dividends and/or buybacks at the end of Q3.

Conclusions

Summing up, we think that the stock may be mildly attractive but not a screaming buy. Further multiples expansion does not seem likely and without it, the stock will deliver returns of ~11% judging from the past results. We do not see any particular trend that can provide a tailwind. The best strategy seems to accumulate the stock on weaknesses.

We are holding a very small position in AFG but will increase it if the stock drops 10% or so. The last time it happened was in September 2022.

Be the first to comment