“There is a time to make money and a time to not lose money.”

– David Tepper

Introduction

We’re about to enter the first recession since the brief one we had to deal with in 2020. Earnings are being revised, the market is nervous, and it’s increasingly hard to find stocks that do well. Hence, I started this article with an interesting quote from hedge fund legend David Tepper. While I’m not entirely sure in what context he made this statement, it’s fair to say that it applies to a lot of scenarios. After all, protecting the downside during recessions is key when it comes to long-term outperformance. In this article, I will give you a company that not only tends to outperform the market by a wide margin during recessions but also comes with satisfying long-term returns, an above-average dividend yield, solid dividend growth, and outperformance versus its peers. That company is American Electric Power (NASDAQ:AEP). A highly boring but important stock when it comes to adding low-volatility exposure to one’s dividend portfolio.

So, let’s get to it!

Downside Protection Is Key

There’s a huge difference when it comes to capital loss prevention in trading and investing. Most long-term dividend growth investors like myself pick stocks they trust and keep these stocks during recessions. Traders change their tactics when market circumstances change. Traders execute many trades and have to balance losing trades against winning trades. Investors mainly need to make sure that they pick the right long-term investments.

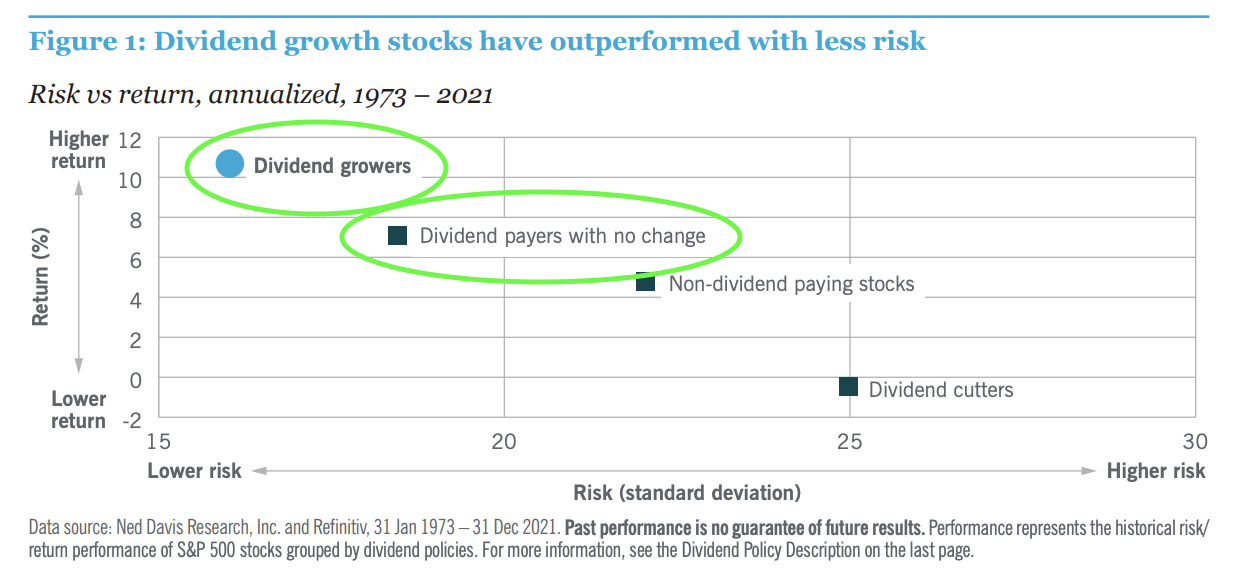

One of the charts I often show in dividend articles is the one below. One of the reasons why a lot of dividend growth strategies are successful is that dividend stocks tend to outperform during recessions.

Nuveen

These dividend stocks, more often than not, also fall during recessions. However, they tend to fall less, which means that even if they do not outperform during every bull market, they have a great shot at delivering long-term outperformance.

Hence, while I am not a fan of boring stocks like utilities, I do buy them, as they are important parts of a low-volatility dividend growth strategy. Also, when I call an investment boring, that’s often a compliment. After all, steady capital gains and dividend growth without drama are what my portfolio needs.

A Recession = Market Crash?

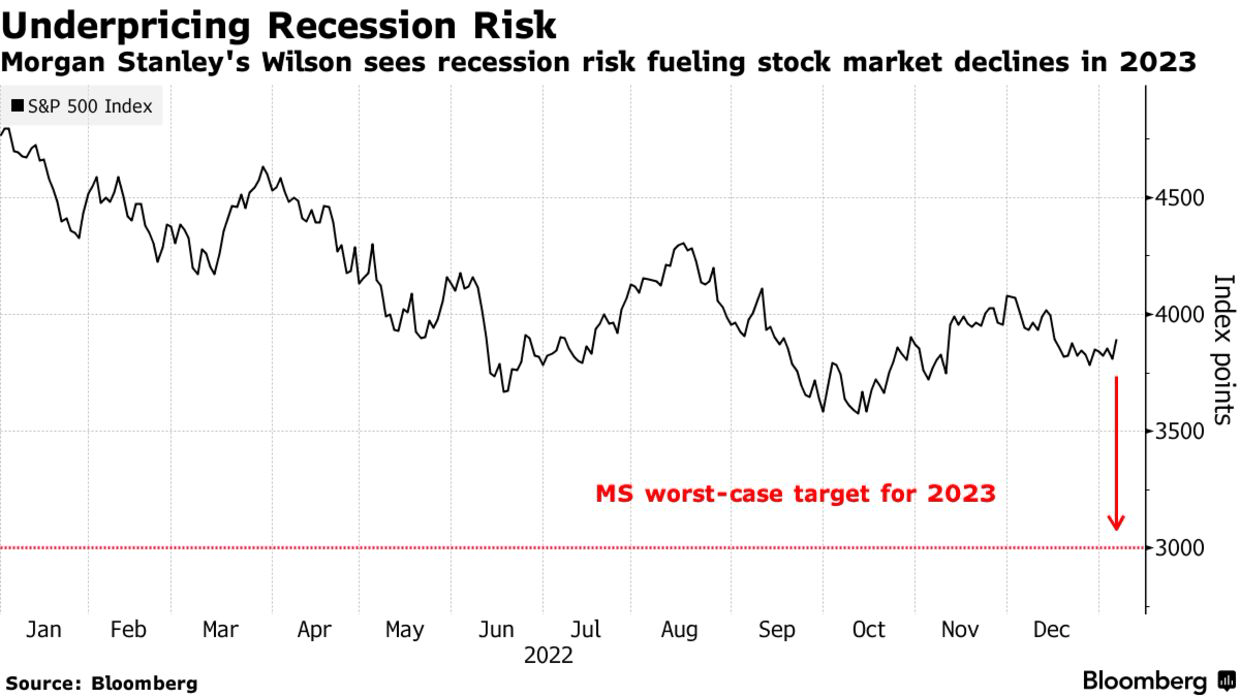

The answer is yes if you were to ask Morgan Stanley (MS). Earlier this month, the investment bank warned that things could get ugly.

Michael Wilson — long one of the most vocal bears on US stocks — said in a research note that while investors are generally pessimistic about the outlook for economic growth, corporate profit estimates are still too high and the equity risk premium is at its lowest since the run-up to 2008. That suggests the S&P 500 could fall much lower than the 3,500 to 3,600 points the market is currently estimating in the event of a mild recession, he said.

“The consensus could be right directionally, but wrong in terms of magnitude,” Wilson said, warning that the benchmark could bottom around 3,000 points — about 22% below current levels.

Bloomberg

In this case, he’s not alone as both Goldman Sachs (GS) and Deutsche Bank (DB) have come out, warning that earnings estimates are still too high.

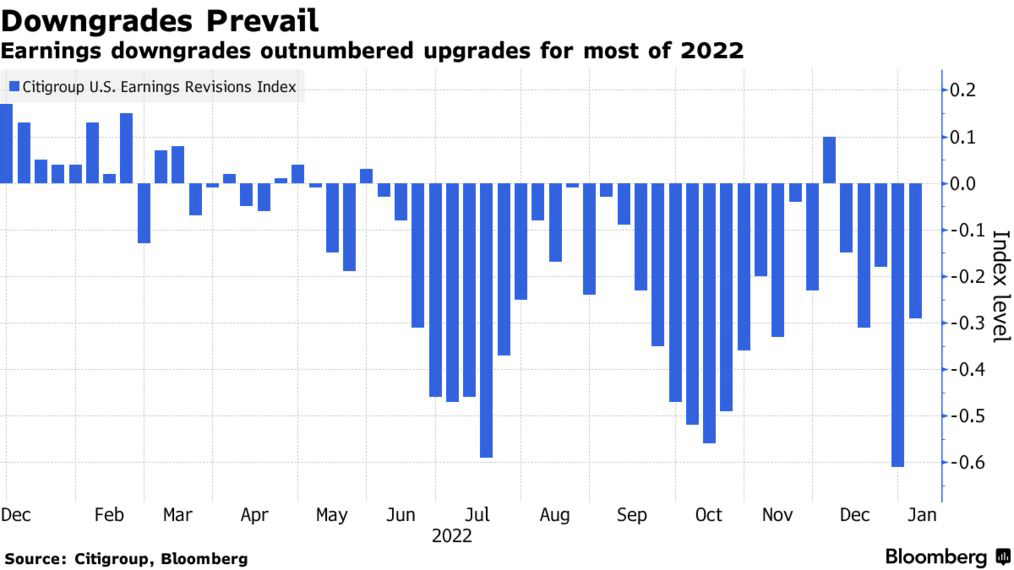

What’s interesting is that earnings have consistently been revised lower since June 2022. Since the summer of last year, analysts have consistently downgraded expected corporate earnings as the chart below shows.

Bloomberg

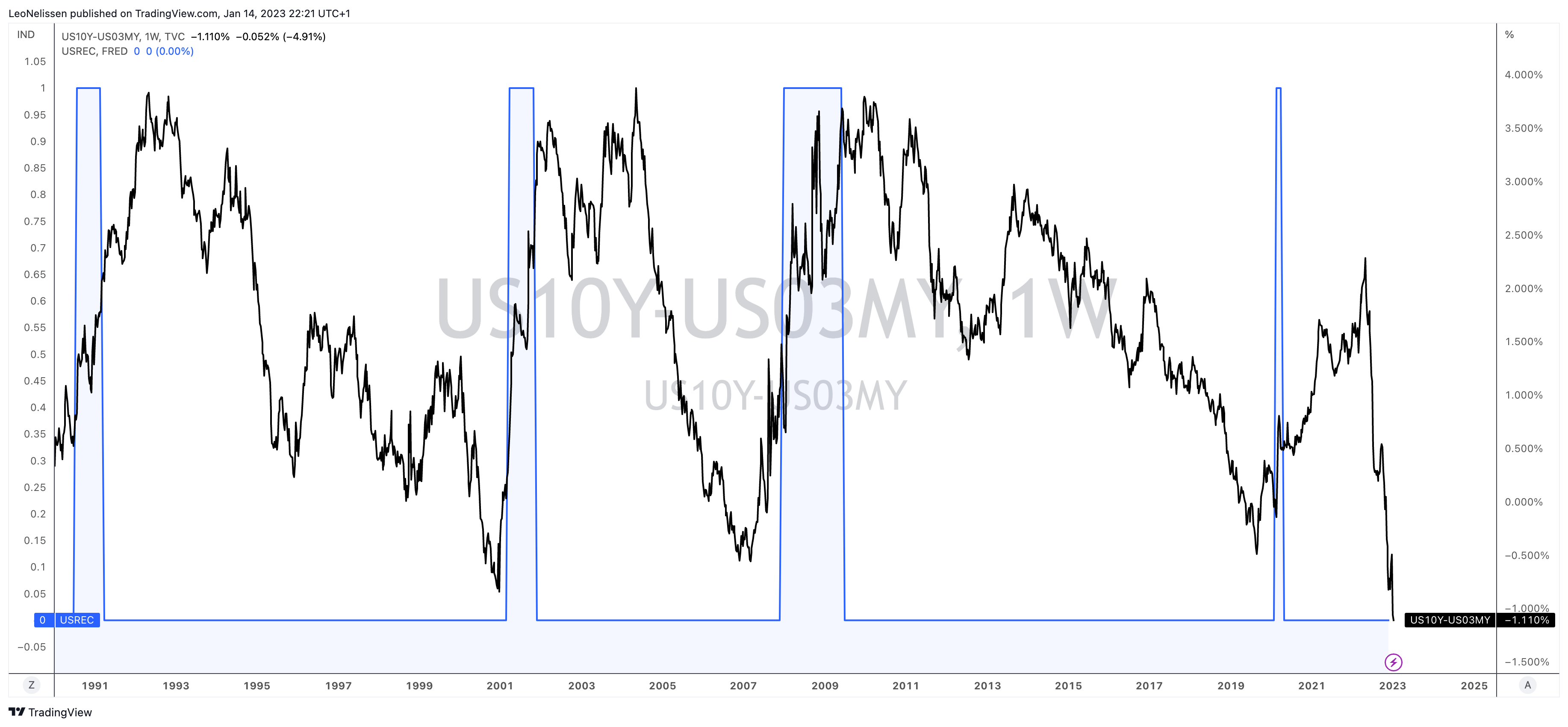

Moreover, the Fed’s favorite recession indicator, the 10Y/3M yield curve has been inverted since the fourth quarter of 2022. The difference between 10-year government bond yields and 3-month government bond yields has been a great predictor of recessions as the chart below shows. The blue area highlights recessions.

TradingView (10Y/3M Yield Curve, Recessions)

Even the nation’s largest bank JPMorgan (JPM) is making the case that earnings estimates will have to come down even further.

“With developed economies slowing, we think Street estimates will likely continue to move lower, but not collapse immediately,” Faller said. “Margin degradation will likely continue into 2023 and will be the focus in management discussions with investors.”

In other words, I believe it cannot hurt to take a close look at some great defensive stocks.

American Electric Power & Energy Transition

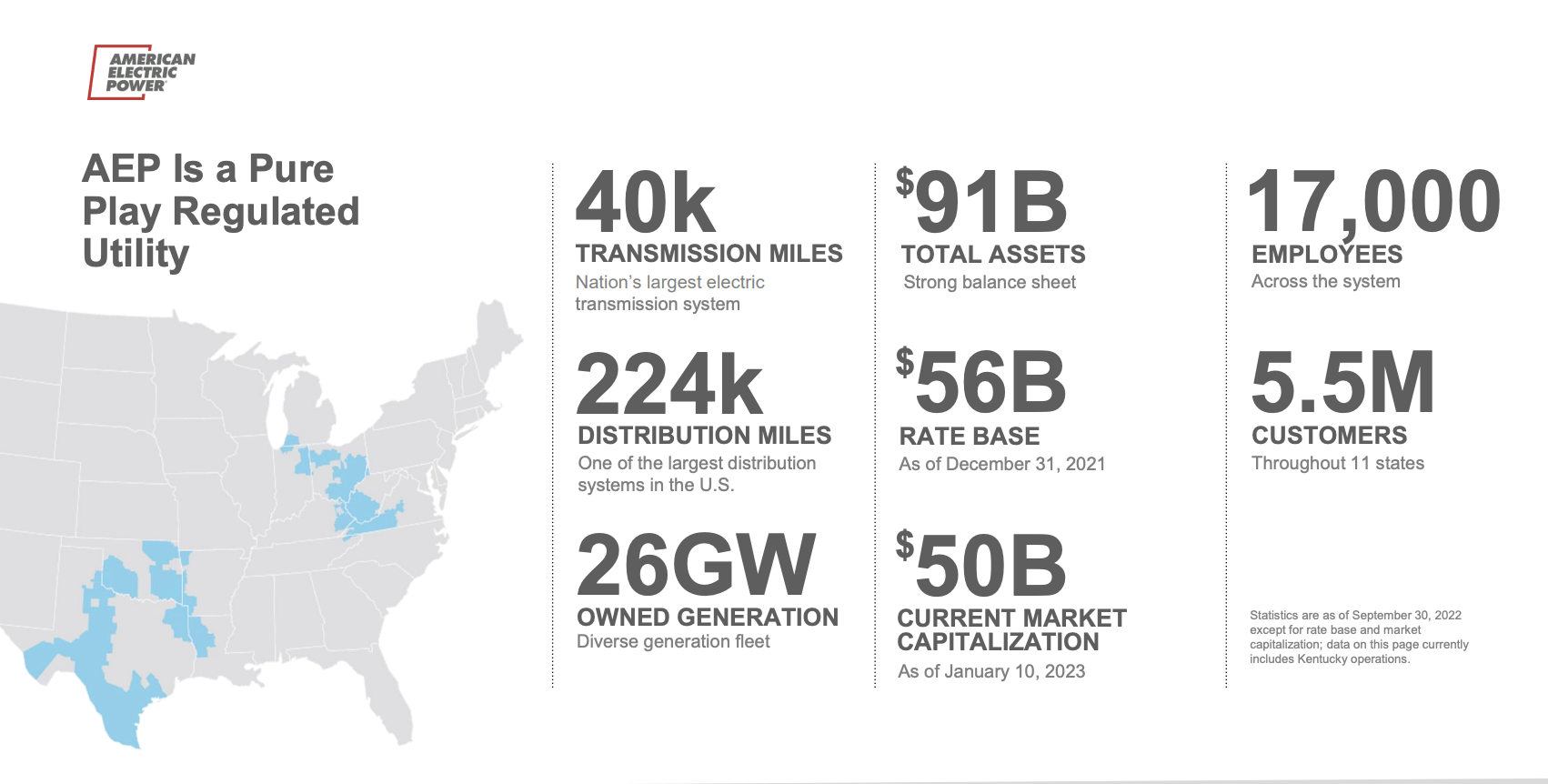

With a market cap of $48.7 billion, American Electric Power is America’s 4th-largest stock-listed regulated electric utility company. As the brief overview below shows, the company services 5.5 million customers in the Midwest, Southeast, and South.

American Electric Power

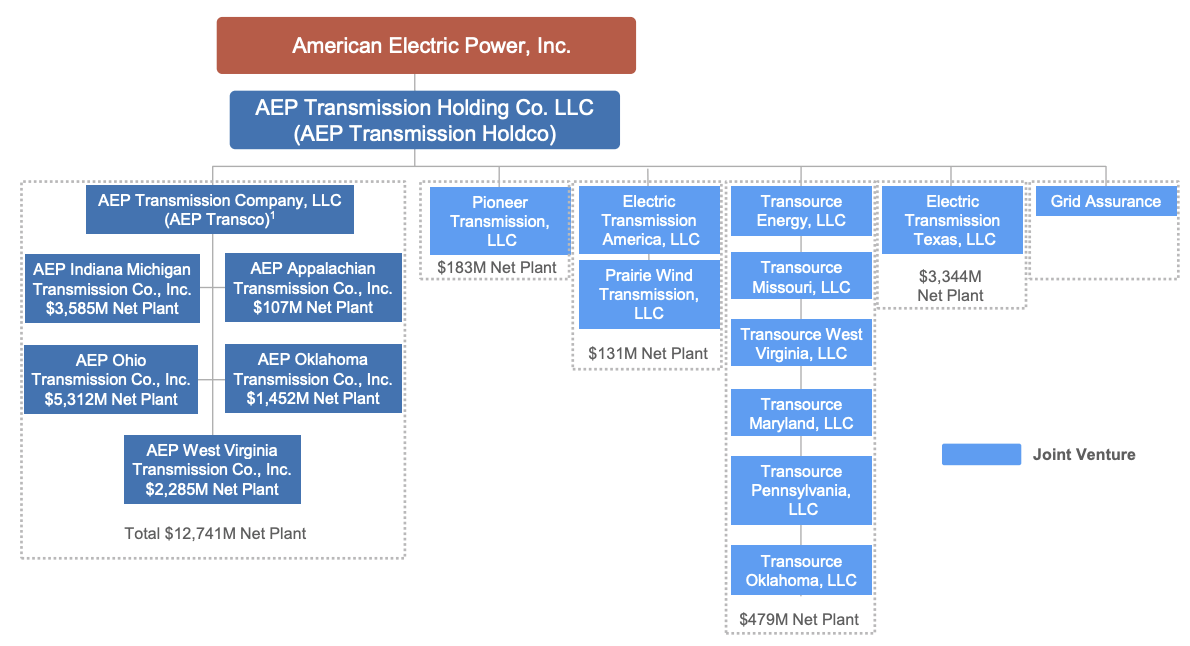

Headquartered in Columbus, Ohio, AEP consists of several legal entities covering its various businesses and operations like transmissions, distributions, and related.

American Electric Power

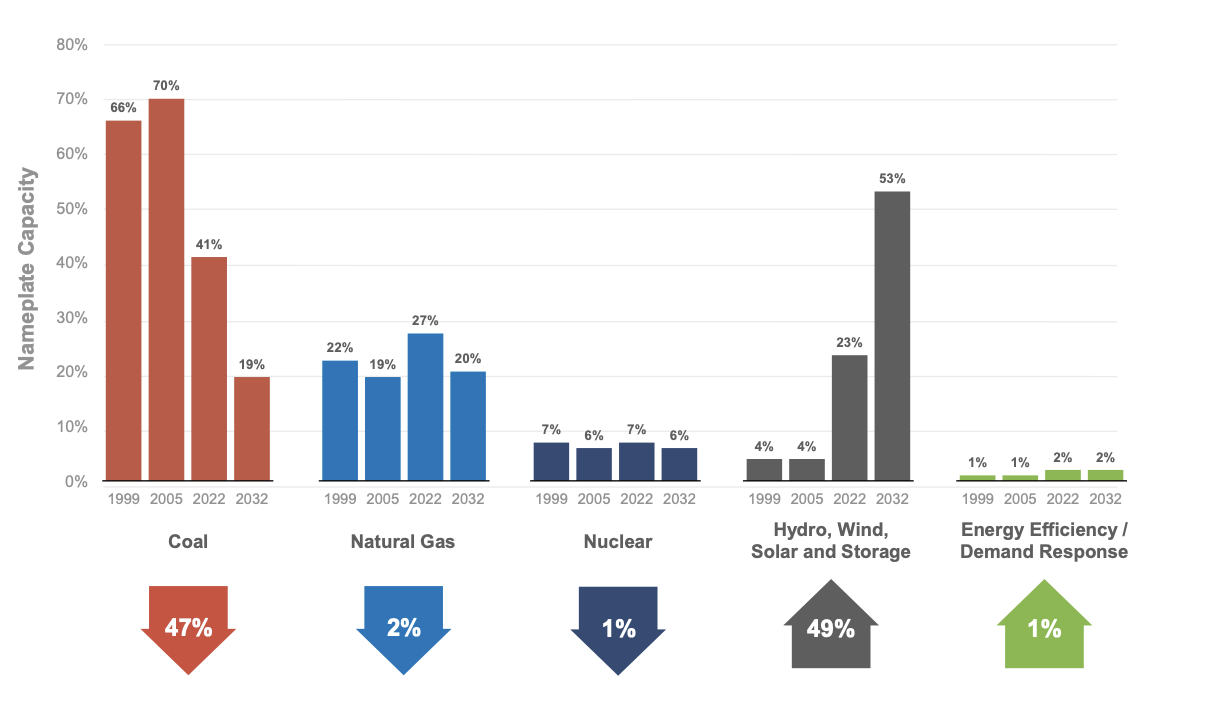

Founded in 1925, AEP used to be heavy in coal. In 2005, the company generated 70% of its energy from coal. Now, that number is expected to drop to 19% by 2032 as the company is working on net zero (like all major utility companies).

American Electric Power

In 2032, the company aims to generate more than half of its power from renewables, including hydro, wind, and solar. It is expected to maintain roughly 20% natural gas and 6-7% nuclear energy exposure.

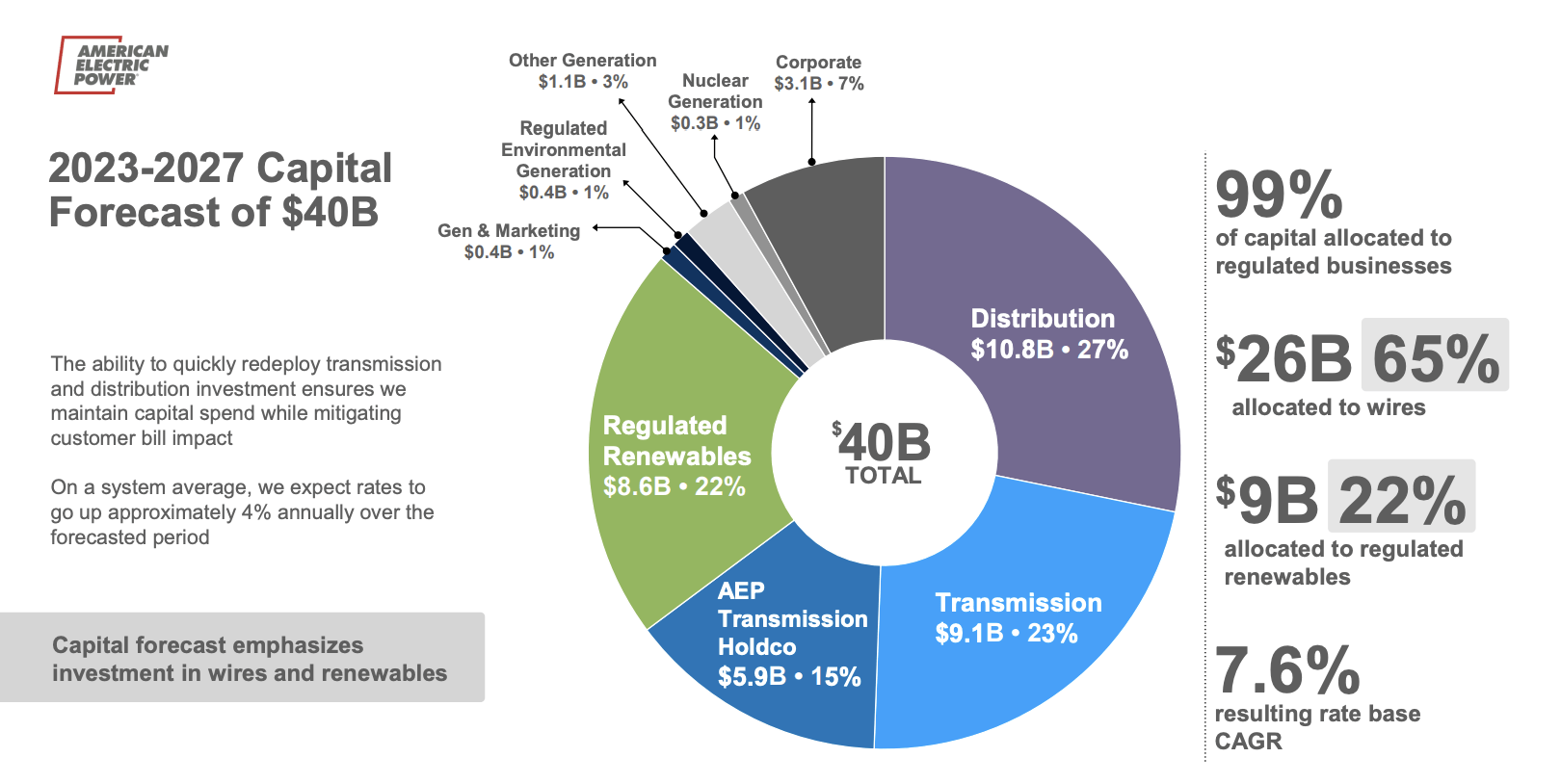

As you can imagine, this will cost a lot of money. AEP estimates that it will spend roughly $40 billion from 2023 to 2027. A fifth of this is dedicated to regulated renewables, 27% will go towards distribution, and 23% will be spent on transmission.

American Electric Power

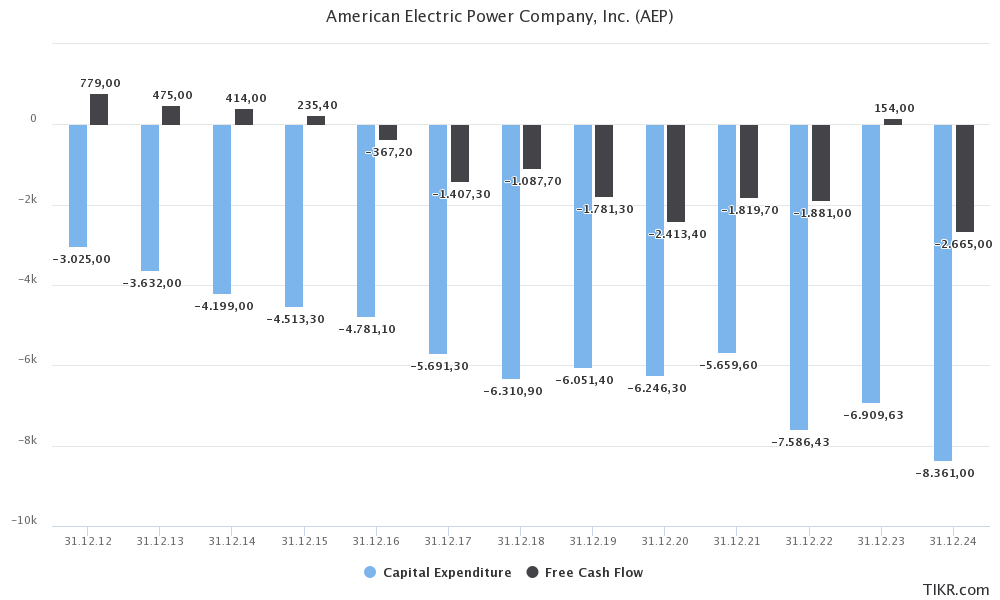

The chart below shows that AEP used to spend $3.0 billion on CapEx in 2012. That number has gradually increased to $6.3 billion in 2018. The new wave of investment requirements will (likely) push that number to $8.4 billion in 2024.

TIKR.com

As a result, the company is unable to generate positive free cash flow. This means it is heavily borrowing to fund operations and to pay its dividend.

While that may be a huge red flag, it’s not that bad. After all, this is something that applies to almost all utilities. Moreover, utilities are generating tremendous value. They are not burning cash on useless projects.

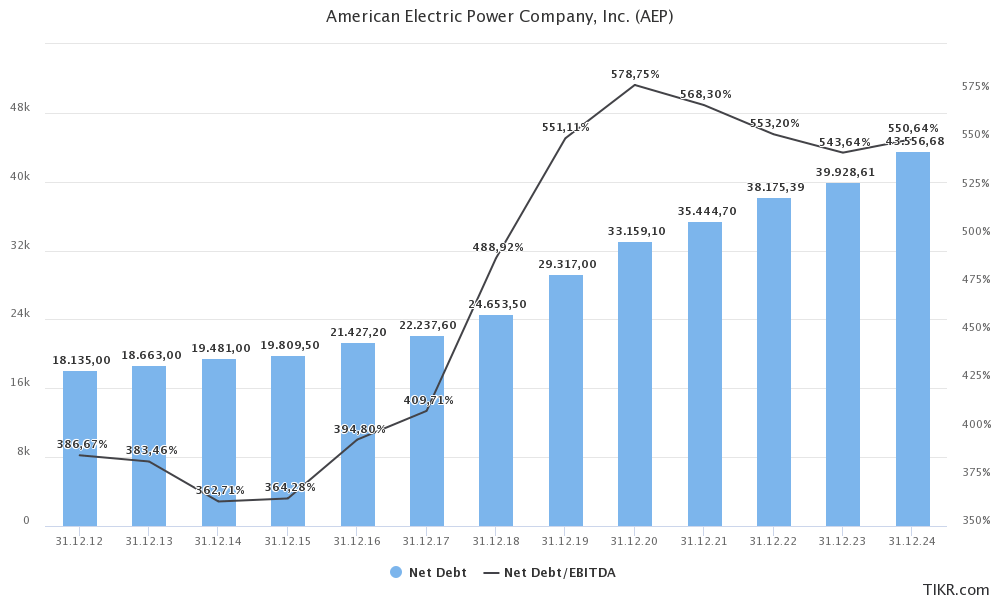

For example, when incorporating 7.6% base rate growth during the 2023 to 2027 period, and asset value creation, AEP has done a great job growing equity and maintaining a healthy balance sheet.

As we can see below, net debt has increased from $18.1 billion in 2012 to $35.4 billion in 2021. This year, net debt is expected to end up at more than $38 billion. In 2024, that number will be north of $40.0 billion. Yet, as we can see, the net-leverage ratio peaked in 2020 at close to 6x EBITDA. Now, leverage is not expected to increase, which indicates outperforming EBITDA growth.

TIKR.com

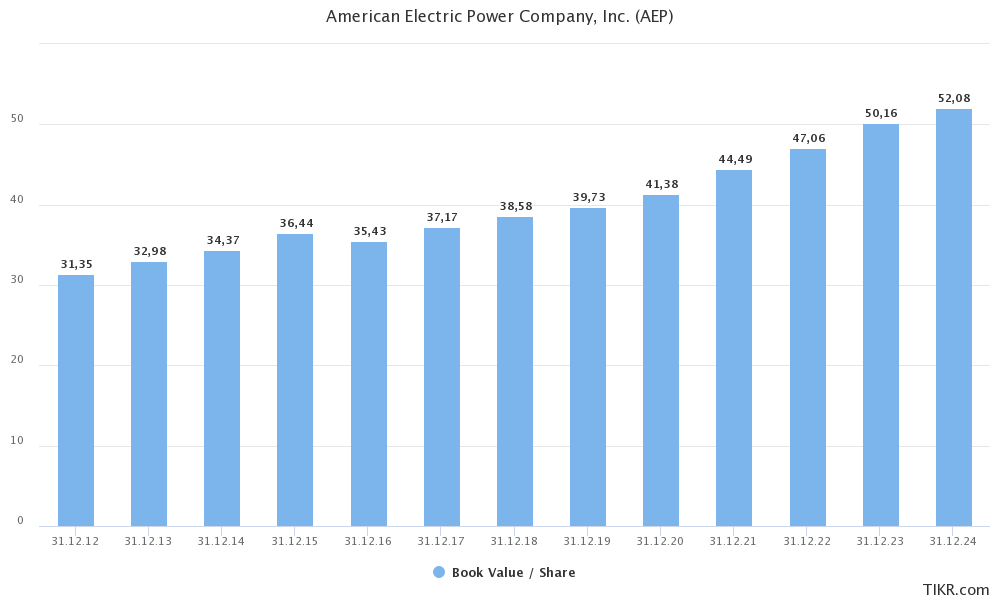

The book value per share is also steadily rising. In this case, that number is important as it shows the difference between total liabilities and total assets PER SHARE. Meaning, it also takes share dilution into account. In the case of AEP, the company prefers debt over equity funding. Since 2017, the number of shares outstanding has increased by just 1.7%.

TIKR.com

Thanks to these numbers, the company has a Baa2/BBB+/BBB credit rating from the big three rating agencies. This is one step below the A-range. The outlook is stable.

Now, there’s another benefit that comes with steady value creation.

A Terrific Dividend & Outperformance

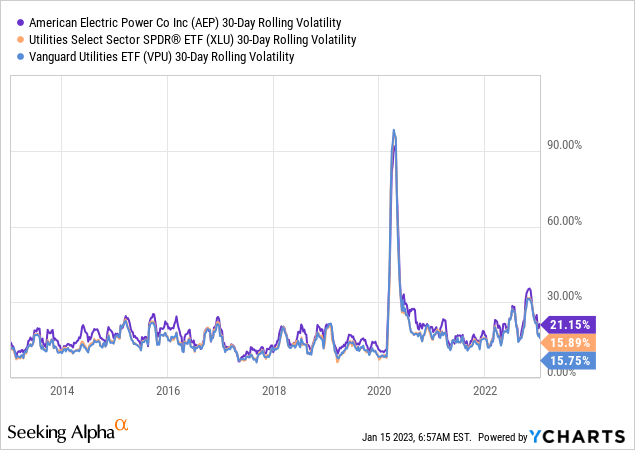

AEP shares yield 3.5%, which is based on a $0.83 per quarter per share dividend. This dividend may not look like a lot, given that we’re dealing with a mature utility company. However, it is well above the yields of the two biggest utility ETFs in the United States:

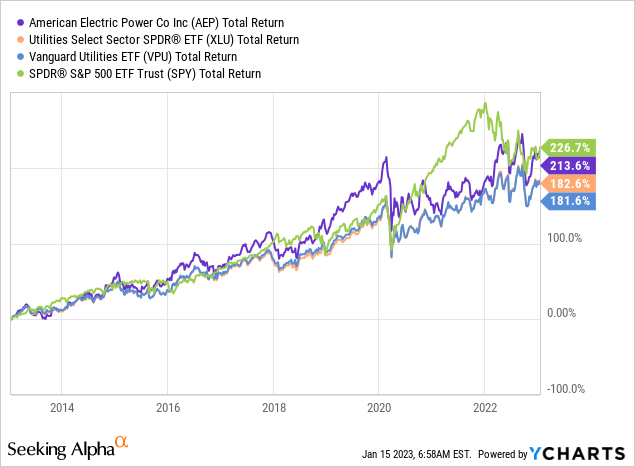

The AEP ticker has also generated a higher total return than these two ETFs over the past ten years, returning 214%. Moreover, AEP has consistently outperformed the S&P 500 in the past. The only reason why AEP did not outperform the market over the past ten years is the pandemic and the surge in tech stocks that fueled the S&P 500’s fantastic total return.

Moreover, AEP has subdued volatility. The company is barely more volatile than the two aforementioned ETFs, even though these ETFs benefit from diversification.

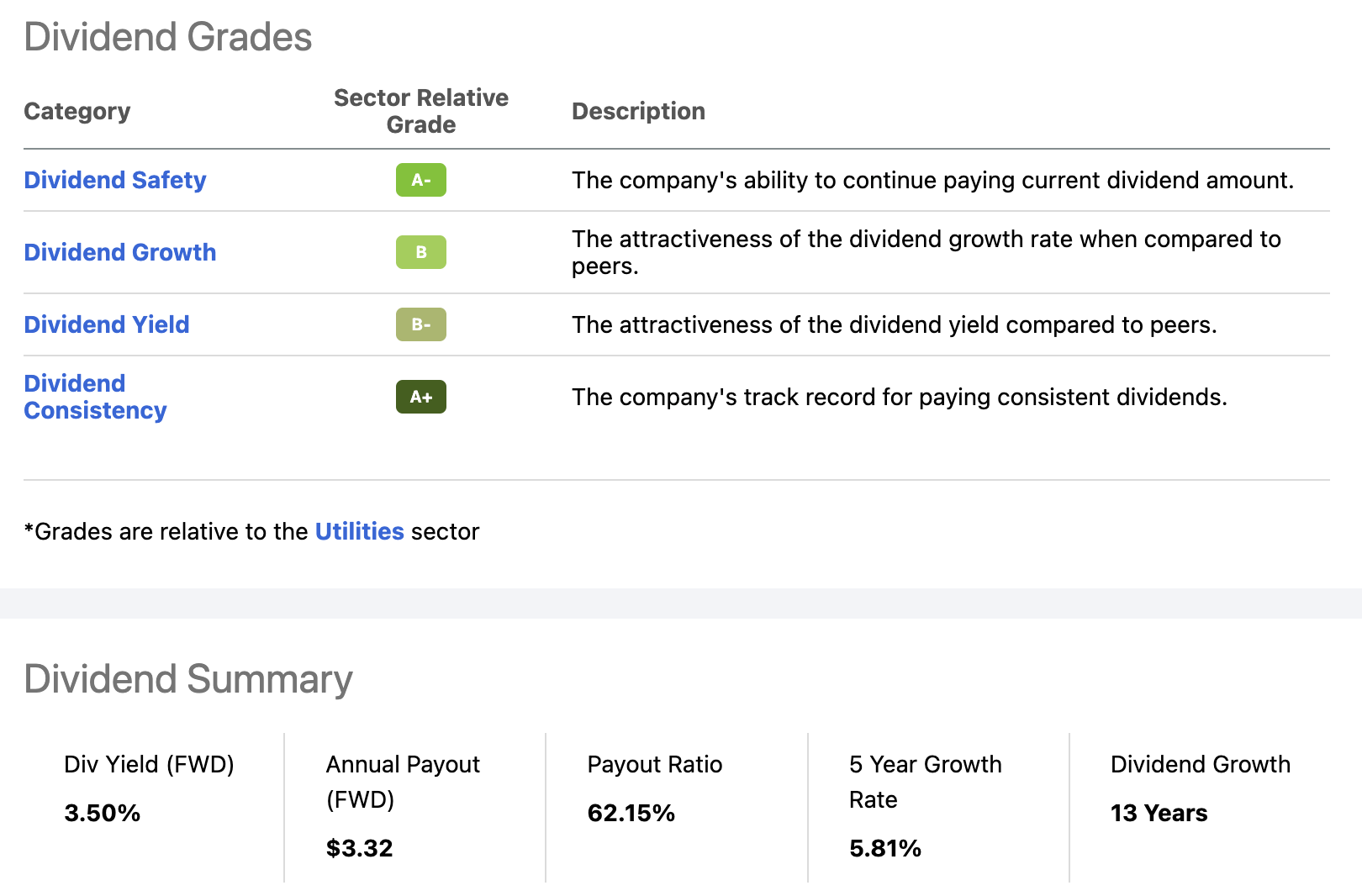

Looking at the Seeking Alpha dividend scorecard below, we see very satisfying scores. The company scores high on dividend safety, and consistency, and moderately high on growth and yield.

Seeking Alpha

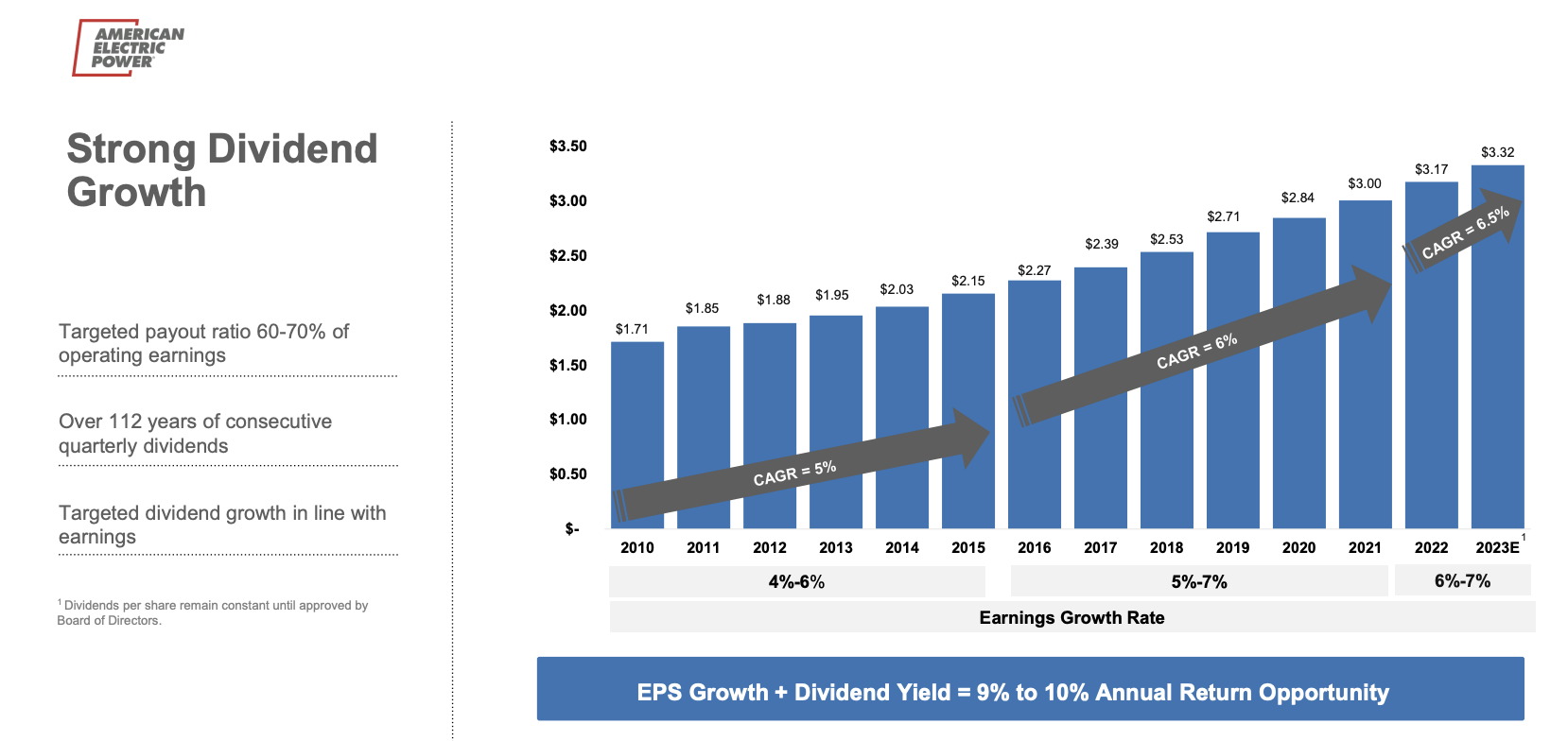

AEP’s five-year annual compounding dividend growth rate is 5.8%. The most recent hike was announced on October 25, when management rewarded shareholders with a 6.4% hike.

Consistent and satisfying dividend growth is part of the company’s ability to grow earnings. On a long-term basis, AEP generates between 9% and 10% in total annual shareholder returns. This is based on 6% to 7% EPS growth and a 3% dividend yield (that’s now 3.5%).

As the overview below shows, AEP targets a 60-70% payout ratio, which means that if earnings accelerate, dividend growth improves. Since 2010, EPS growth has consistently improved, allowing the company to boost dividend growth to more than 6% per year. If the data we discussed in this article offers any indication, we can assume that 6% annual dividend growth continues.

[…] our dividend growth is in line with our long-term growth rate and within our targeted payout ratio of 60% to 70%. We continue to derisk our platform and execute our strategy to ensure that we are best positioned for value creation in the face of global economic uncertainty and inflationary pressures. As part of this effort, we are continuing to work with states to drive reliability and resiliency in our service territory amidst customer bill considerations and other macroeconomic factors.

American Electric Power

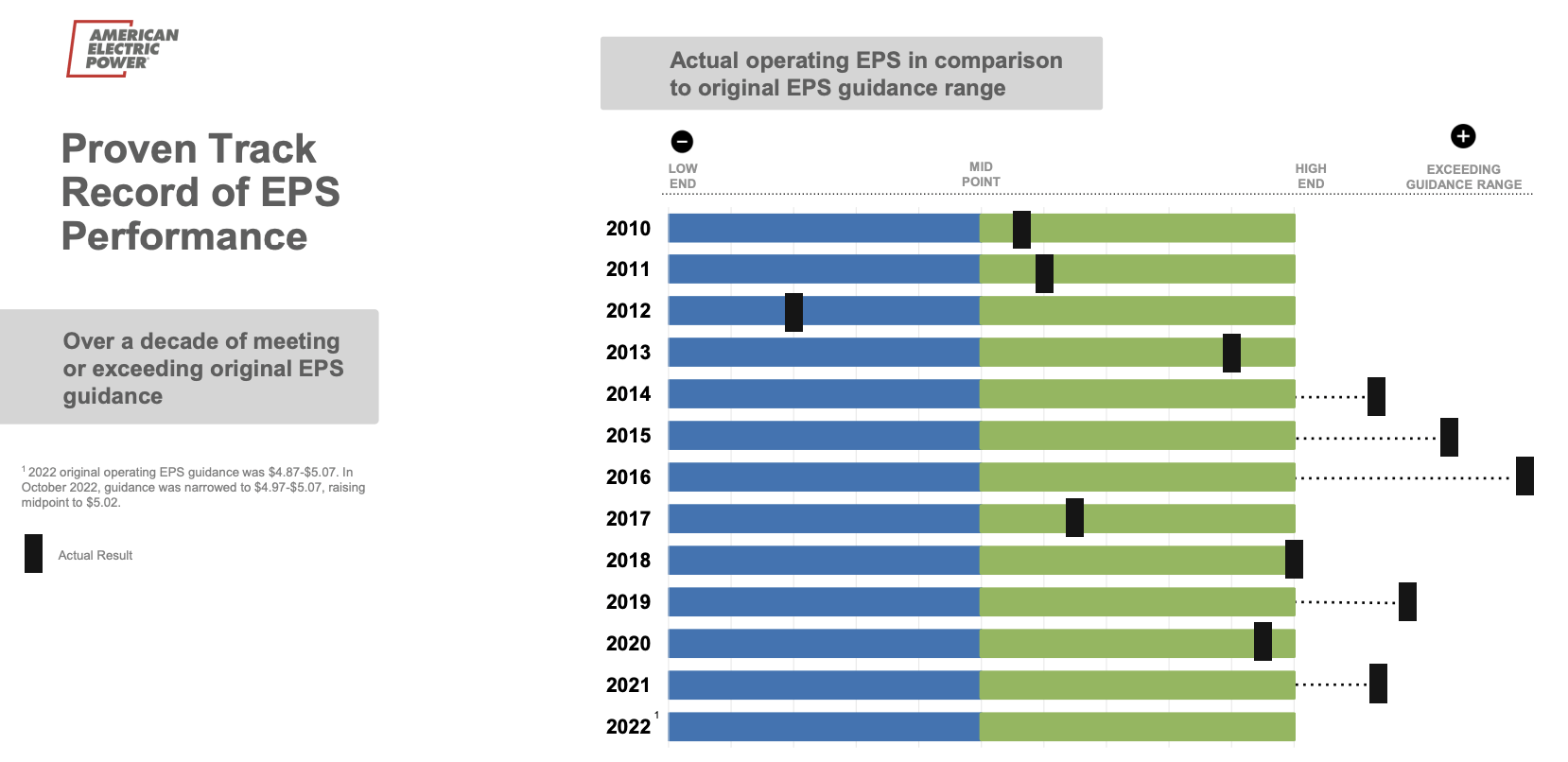

Moreover, the company has reported below-midpoint EPS just once since 2010. It even beat the high-end of guidance in five years.

American Electric Power

With that said, let’s talk about the valuation and recession outperformance.

Valuation & Recession Outperformance

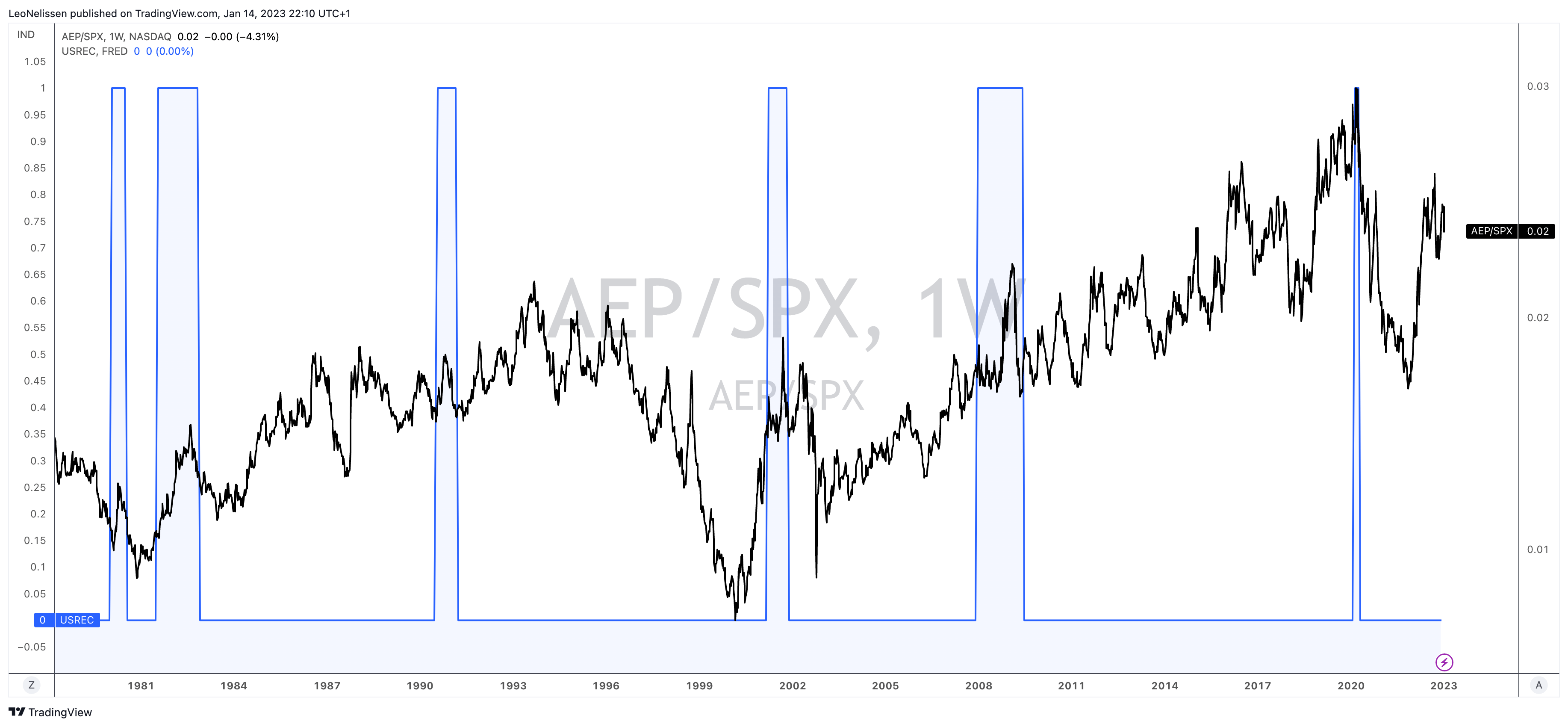

The blue areas in the chart below display official recessions, as defined by the National Bureau of Economic Research. The black line displays the ratio between the AEP stock price and the S&P 500 (dividends are not included).

TradingView (AEP/SPX Ratio, Recessions)

Two things quickly become clear:

AEP has a great track record of outperforming the market during recessions.

On a long-term basis, the company is outperforming the S&P 500.

This confirms that outperformance is likely when a company can do well during recessions. Companies don’t even have to be high-flying stocks during bull markets, as long as it refrains from tanking when economic weakness hits.

Given the current situation, I do expect that AEP will continue to outperform – even if high rates are a headwind for utilities. After all, higher rates make borrowing more expensive (and utilities need to borrow a lot), and high rates push are competing with the dividend yields of utility stocks (and dividends in general).

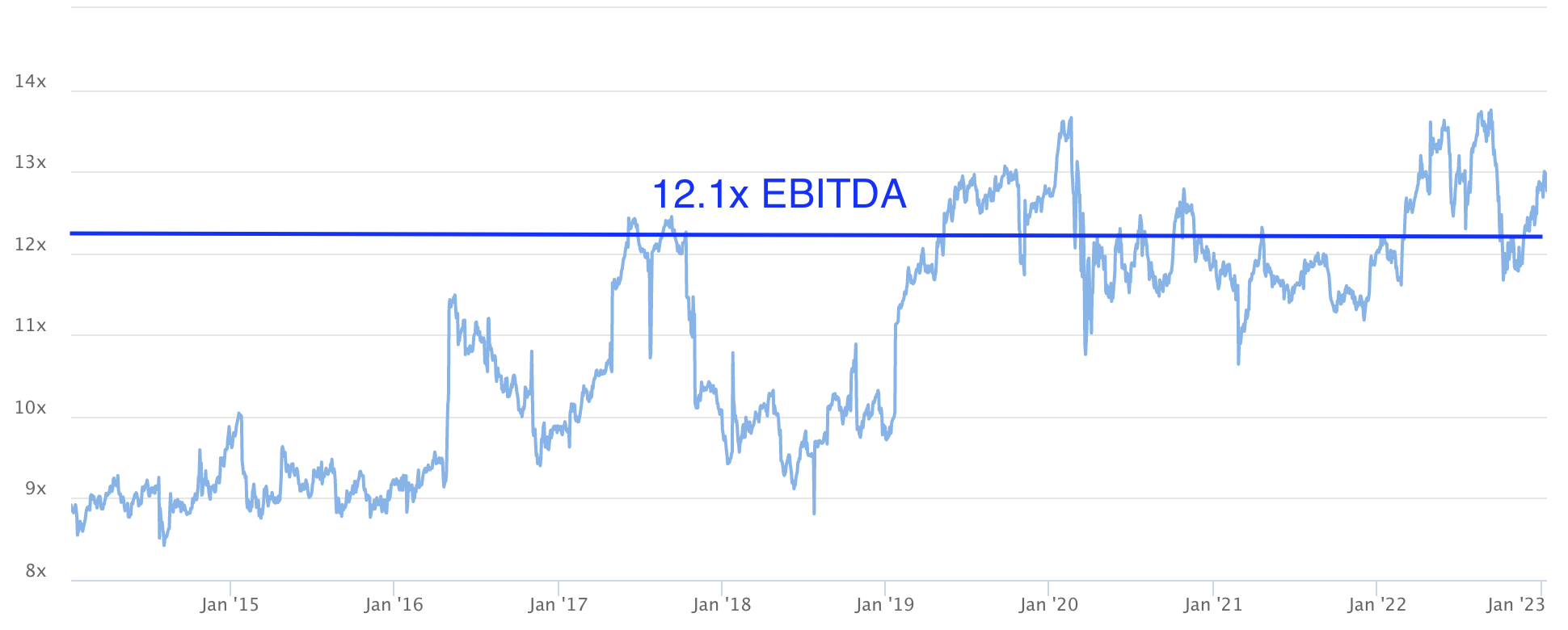

With that said, the company is trading at 12.1x 2023E EBITDA ($7.4 billion).

TIKR.com

This valuation isn’t deep value. However, it’s a fair value, offering investors a good opportunity to buy a great dividend stock at a good price.

Takeaway

In this article, we discussed a conservative, anti-cyclical dividend growth opportunity. Columbus, Ohio, based American Electric Power offers an above-average dividend yield, consistent and improving dividend growth, a healthy balance sheet, and a very high likelihood of long-term outperformance.

Especially in this economic environment, the stock is set to deliver outperforming total returns.

If you’re in the market for a conservative dividend stock, I think the AEP ticker might be right for your portfolio.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment