krblokhin/iStock Editorial via Getty Images

Introduction

U-Haul is the largest and most well-known moving equipment company in the United States. The self-moving trucks U-Haul offers are easily the most dominant brand name to buy. The company also has a fast-growing self-storage operation to bolster growth. Known under the Amerco (NYSE:UHAL, NYSE:UHAL.B) until November 2022, the company underwent a name change to The U-Haul Holding Co. and commenced a 10 to 1 stock split. Not only does the consolidated company have the moving and storage operations, but also an insurance business that offers complimentary sales to the overall business. Overall, the company is growing at a nice rate, is the dominant player in the industry, and is trading at a fair value.

Financial History

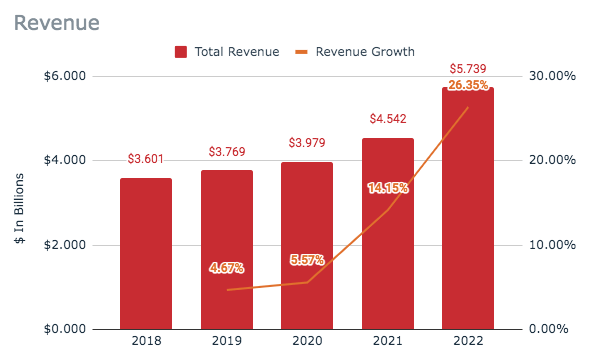

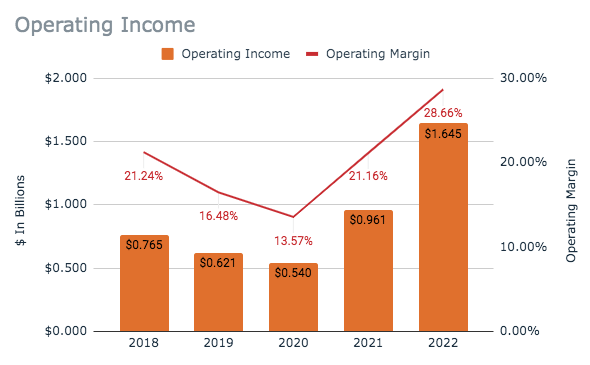

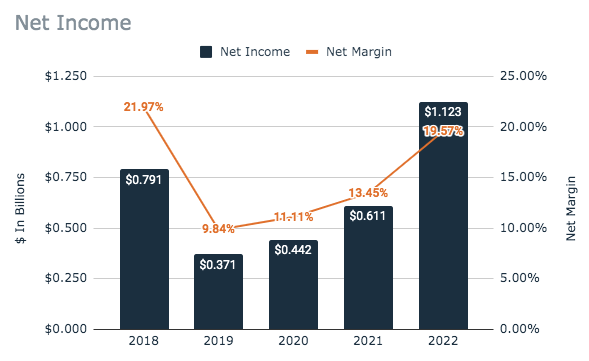

U-Haul Total Revenue (SEC.gov) U-Haul Operating Income (SEC.gov) U-Haul Net Income (SEC.gov)

Amerco has seen a very strong revenue growth pattern over the past five years, with the past two years showing double-digit growth rates. This has helped the operating and net profits rebound from a downward trend. The trend is attributable to the Moving & Storage segment’s growth, as seen below. Over the past five years, the business has posted a CAGR of 9.77% per year in revenue and 7.26% in net income.

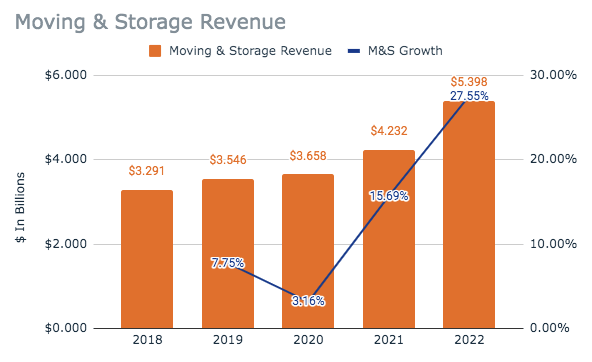

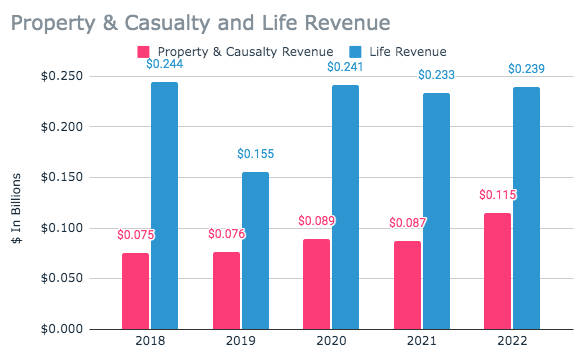

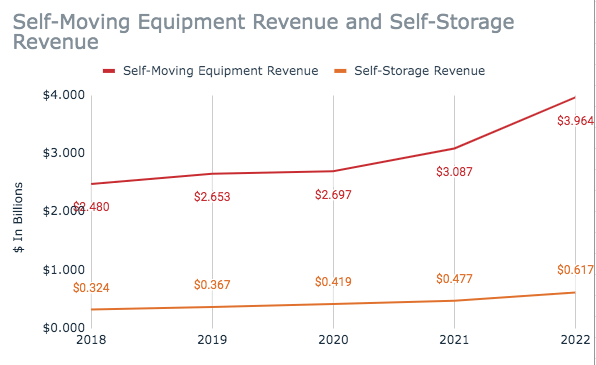

U-Haul Moving & Storage Revenue (SEC.gov) U-Haul Insurance Revenue (SEC.gov) U-Haul Moving & Storage Revenue Breakdown (SEC.gov)

As mentioned, this growth is powered by the main segment of Moving & Storage, the bread and butter of the company, making up 92% of all sales. This segment has grown every year since 2018 and produced double-digit growth in 2021 and 2022. This is while the insurance segment stays rather stable. Looking at the chart above shows that self-moving equipment has seen an impressive 9.83% increase in revenue due to more retail locations, usage, and a larger fleet. But self-storage has really been the star of the past two years. Self-storage revenue has grown 13.75% per year, with the number of units drastically increasing by 235,000. On top of this, the occupancy rate has climbed from 71.6% in 2018 to 82.6% in 2022. Overall, Amerco has expanded in the past few years to bolster the financial growth seen above.

This Year

So far in 2023, Amerco has seen good, albeit lower results when compared to last year. Total revenue so far is 2.3% higher, but operating and net income are down by 9.8% and 14.12%, respectively. Some of this downward pressure is due to poor insurance segment results, with P&C down 20.9% and Life down 25.1%. On the other hand, Moving & Storage is up 3.8%. The pressure on operating and net income are in part due to the insurance segments, but mostly attributable to lower one-way equipment rentals and increases in costs from more stores and vehicles. Much of the increased costs of the fleet have been due to supply chain issues and the inflationary cost of vehicle maintenance. Self-storage has continued to truck along with 13% more units and a continued 85% occupancy rate. Altogether, Amerco is having a good year, although the comparable results don’t stun, slightly lower demand and high costs are part of the ebb and flow of the business. Nothing drastic has changed, the business is still increasing locations and fleet, and the storage product line is doing great.

Balance Sheet

As of the most recent quarter, Amerco has ample liquidity with a current and quick ratio of 1.42x and 1.32x, showing the company can pay off any current obligations and still have leftover cash. The business also isn’t highly leverage at 1.87x debt-to-equity. Overall, Amerco is in great standing financially, allowing for less risk when growing the business further.

Valuation

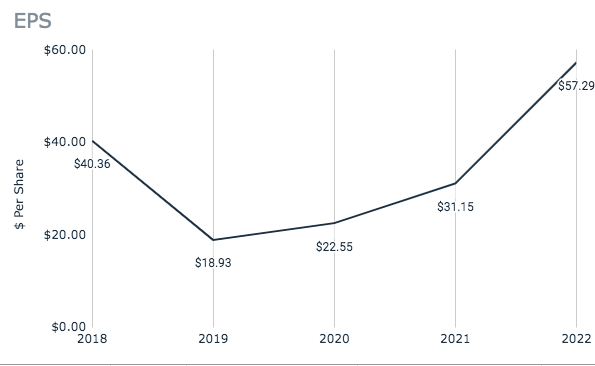

U-Haul EPS (Non-Split 10 to 1) (SEC.gov)

As of writing, Amerco trades around the $70 price level. Above is a graph that shows the diluted EPS for Amerco prior to the 10 to 1 stock split announced in November 2022. Either way, at the $70 price level, the company trades at a trailing P/E of just 12.22x using the 2022 EPS. The 2023 EPS estimate is along the same line at $5.61. The company also trades at a P/BV of 2.17x. If you average the past five years’ EPS at $3.41, Amerco trades around a 21x P/E. Not a terrible valuation for a growing business in a steady industry. There are two share types, the Class A and Class B shares. The B shares trade at a $7 discount to the A shares right now, making for even better value. The only aspect of the B shares is you don’t get the 4 cents per quarter dividend. At $63 per share, you can buy Amerco at a close to 10% discount.

Conclusion

Amerco, or The U-Haul Holding Co., is a business that has a dominant market share in a steady industry. The company has seen good growth over the past few years, and more should come as the company footprint expands. I think at 21x the average EPS of the past five years, the company is a good deal for such a steady business. I don’t currently have a position, but may purchase the B shares to take the 8% discount in lieu of the minuscule dividend.

Be the first to comment