Pavel Byrkin

Work hard, take care of yourself, and you’ll be just fine.

~ Richard Simmons.

Sometimes when people talk about reinvigorating their core, they are discussing health and fitness, as in the best 90s workout videos. But instead of Paula Abdul, Jane Fonda, and Richard Simmons, in this case I am referring to computing technology, as in rebooting your expectations based on new technologies that can reinvigorate the core processors for data centers and high-performance computing.

Following a disastrous earnings report that missed expectations and disappointing forward guidance from Intel Corporation (INTC), investors in technology stocks may be asking themselves what’s next. Is Advanced Micro Devices, Inc. (NASDAQ:AMD) going to suffer the same fate when they report fourth quarter results? We will find out after the close on Tuesday January 31st when AMD reports, but my research indicates that AMD could surprise the bears and naysayers with a much more positive report than many are expecting. My belief is that AMD is stealing market share from Intel in the enterprise data center and high performance/AI computing segments, and I, therefore, rate AMD a Buy ahead of earnings.

Meanwhile, some analysts are wary of the downturn in demand that could lead to another disappointing quarter for AMD:

“In recent months we have been growing more wary of potential PC dynamics, both given the market outlook as well as exacerbated by Intel’s semi-destructive behavior as of late as they use both price and capacity as a strategic weapon, continuing to over-ship even amid broader breakdowns in the industry,” Bernstein analyst Stacy Rasgon wrote in a note to clients, moving the firm’s rating on AMD to Hold.

According to this Seeking Alpha review of Intel’s Q4 report, data center and AI weakness were key contributors to the revenue miss:

The company said the shortfall was due to weakness in its Client Computing and Datacenter and AI-related units, which saw revenue fall 36% and 33% year-over-year, respectively. Its nascent foundry business, which CEO Gelsinger is working to help lead Intel’s (INTC) transition, generated $319M in revenue in the quarter, up 30% year-over-year.

The data center and AI segments are where AMD has been especially focused for the past two years, and that is in large part due to their acquisitions of Xilinx, followed later with Pensando. A recent article from SA contributor Envision Research suggests that data center growth will improve for AMD due to those acquisitions, and I agree. The Xilinx acquisition, in particular, gives AMD an advantage over Intel due to their ability to now embed FPGA (field programmable gate array) technology into their product offerings, as discussed in this article from another SA contributor in February 2022.

Because FPGAs are programmable, it offers an entry for AMD into many markets by offering comprehensive solutions that include FPGA devices, advance software, and configurable, ready-to-use IP (intelligent processor) cores. Those markets include Data Centers, High Performance Computing, Industrial, Automotive, Aerospace & Defense, and more.

AMD Advantages over Intel

In a Reuters report from November 1, 2022, regarding forecast fourth quarter revenues, it was noted by several analysts that AMD is continuing to take market share from Intel due to their growing advanced technology advantage:

“We expect AMD’s share gains to continue, as the company’s upcoming, next-generation server CPUs are expected to outperform Intel’s lineup across price and performance metrics,” said Nathaniel Harmon, analyst at YipitData.

I have been reading a lot of comments on articles from people who know more about the inner workings of the technology than I do, and one of those comments that helped me to understand the technical advantage of the Xilinx FPGA integration is this comment from geekinasuit. What becomes even more clear to me after reading some of those comments is that AMD is truly leading the way in desktop, data center, HPC and AI technology.

One example of this new innovation in technology using 3D stacking in a desktop CPU was unveiled at the recent CES 2023 show. CEO Lisa Su unveiled the new 7950X 3D CPU that delivers 16 cores, 32 threads and is built on the TSMC 5nm process node.

AMD

You can read more about the design architecture of the chip here, but one key consideration is the increased energy efficiency in this tiny processor. The new AMD Ryzen 7950X 3D offers 57% better content creation performance using V-Ray Render and is 47% more energy efficient than the competition.

Data centers and HPC applications are only going to continue to grow and expand over the coming decades. A recent report from Gartner that I came across on the Equinix, Inc. (EQIX) data center real estate investment trust (“REIT”) website, explained that demand is likely to continue growing for the foreseeable future:

According to Gartner, “Workload placement is not only about moving to the cloud, it is about creating a baseline for infrastructure strategy based on workloads rather than physical data centers. This is causing I&O leaders to rethink infrastructure strategies, which have a direct impact on enterprise data centers.”

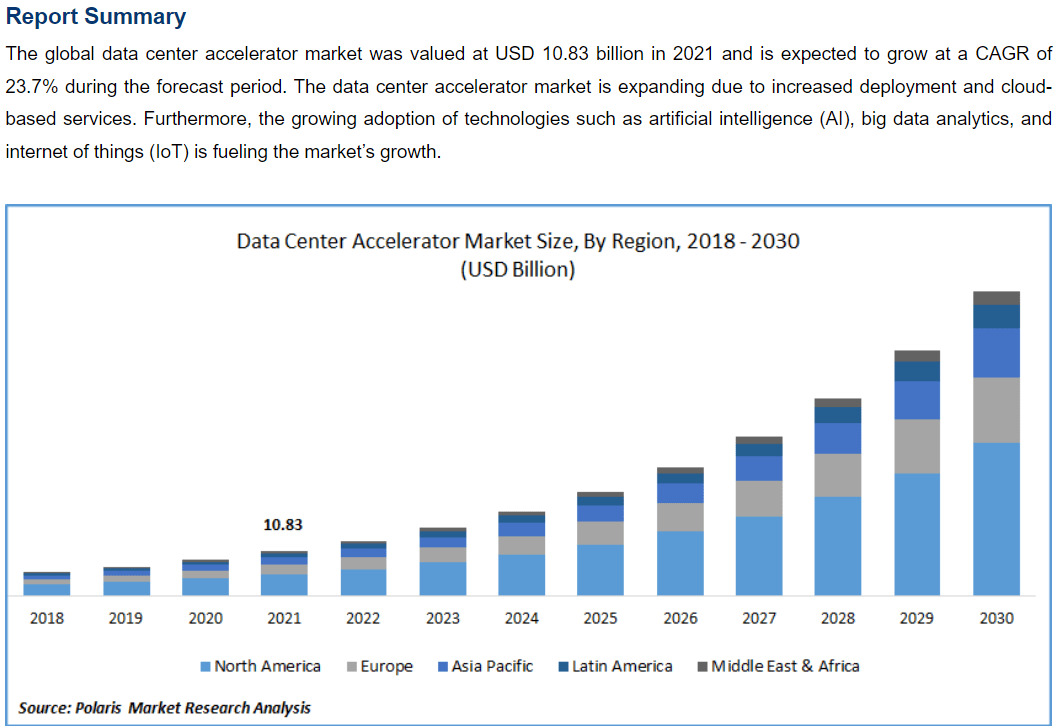

The market for data center accelerators is expected to grow by a CAGR of 27% from 2022 to 2030, according to this market research report from Polaris.

Polaris

Benefitting from Xilinx and Pensando Acquisitions

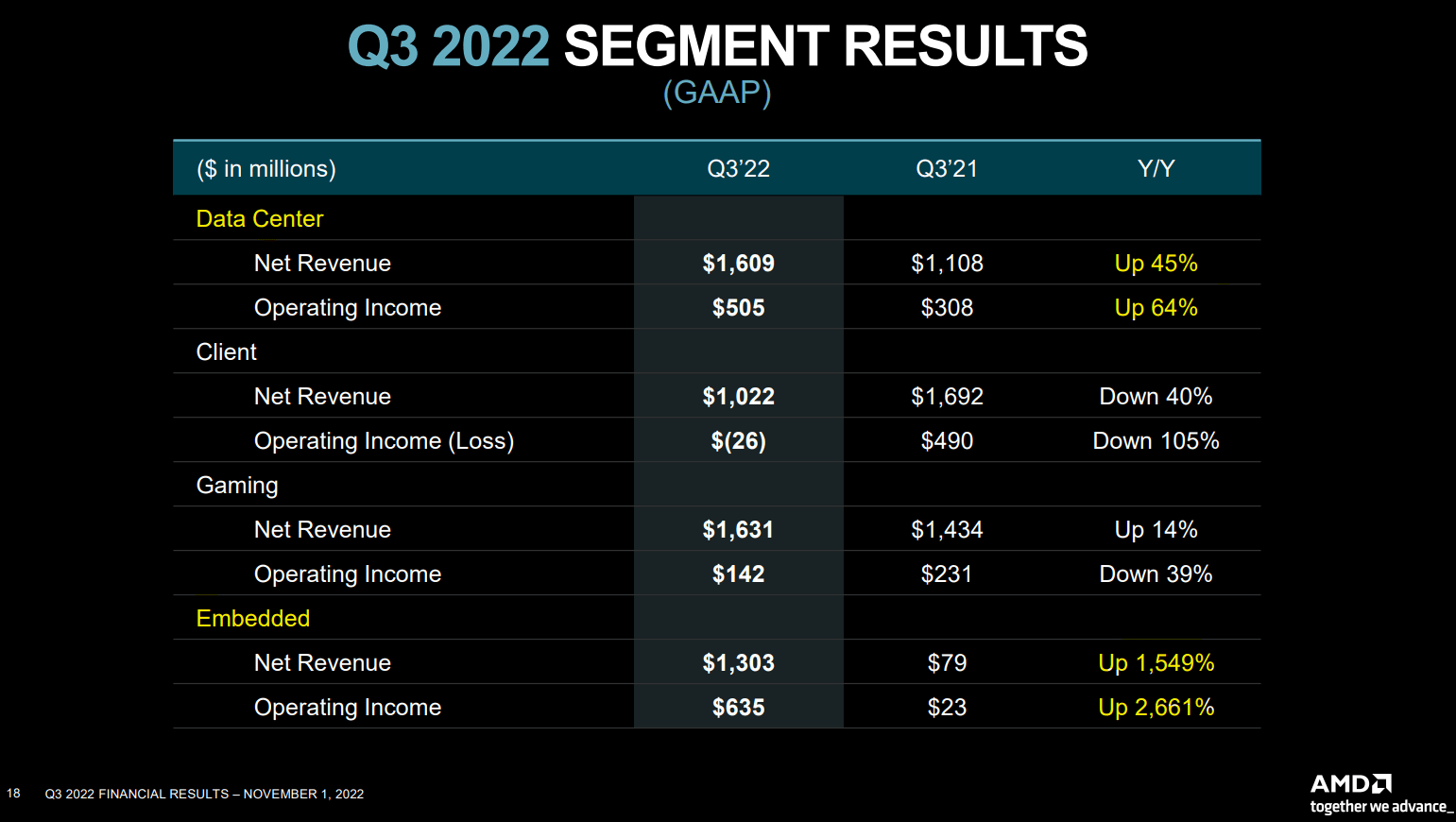

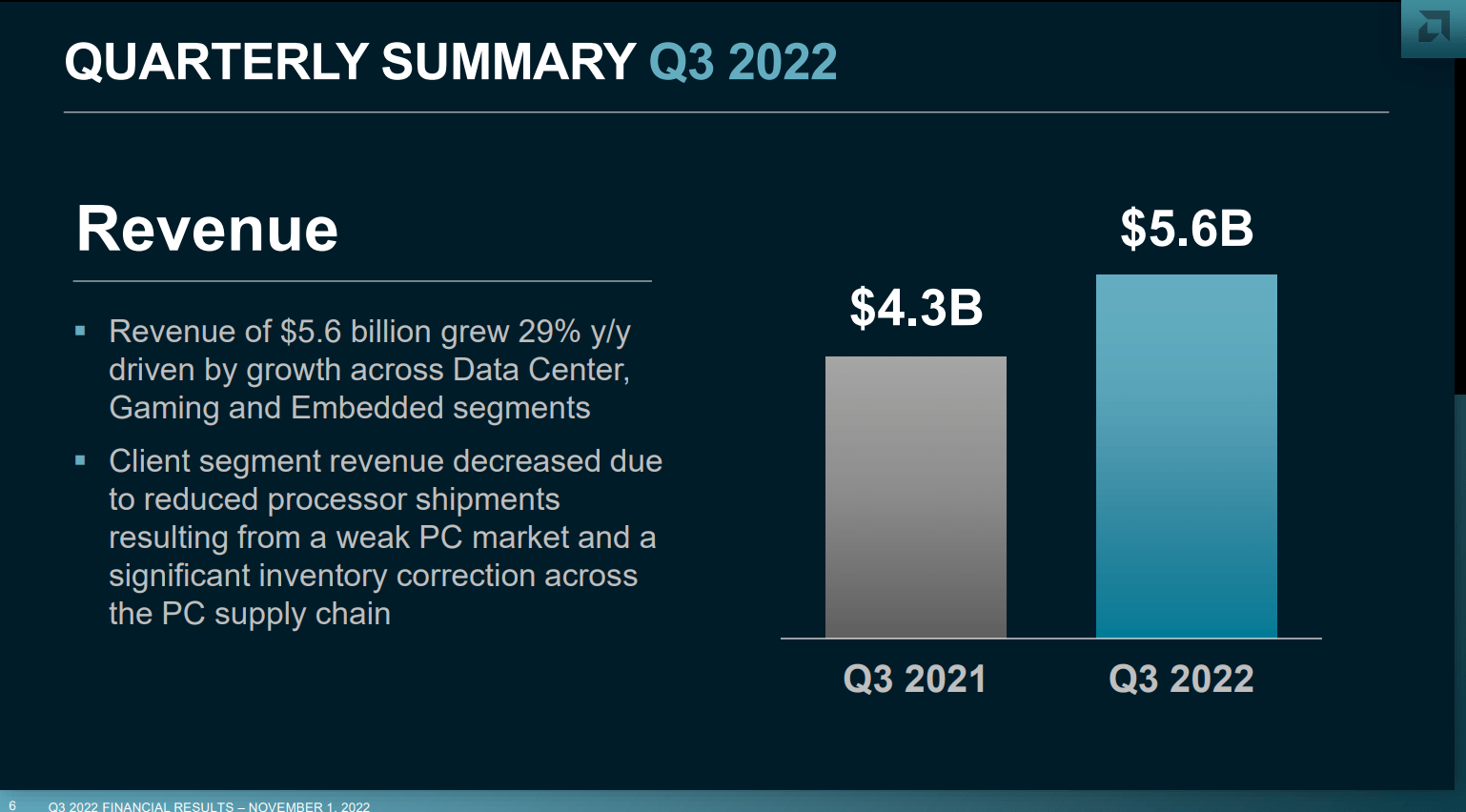

In a Forbes article from June 2022 the (soon to retire) CFO from AMD, Devinder Kumar, discussed the AMD product roadmap with Xilinx and Pensando fully integrated. His message indicated that AMD is ready for the expansion into the new era of hyper growth and scaling that is coming. The Data Center and Embedded segments currently represent more than 25% of overall revenue for AMD and is growing with a goal to become 50% of revenue based on an estimated total addressable market (“TAM”) of $125B.

AMD Q322 Earnings Presentation

The Pensando purchase gives AMD additional firepower in the battle over DC supremacy, as explained by Lisa Su, CEO of AMD, in this press release announcing the acquisition last May.

“The data center remains one of the largest growth opportunities for AMD. The addition of the Pensando Systems team with their hardware and software portfolio will enables us to offer cloud, enterprise and edge customers a broader portfolio of leadership compute engines that can be optimized for their specific workloads,” said AMD Chair and CEO Dr. Lisa Su. “Pensando’s leadership DPU complements our data center product portfolio, enabling AMD to offer solutions that can significantly accelerate data transfer speeds while providing additional levels of security and analytics that will play a larger role in defining the performance of next-generation data centers.”

The moat from the Xilinx and Pensando acquisitions enables AMD to compete in the DC and AI markets better than before due to the fact that Xilinx had captured about 70% of the FPGA market prior to the acquisition. And by using 3D stacking technology, AMD can better integrate CPU, GPU, and energy efficiency into a single chip.

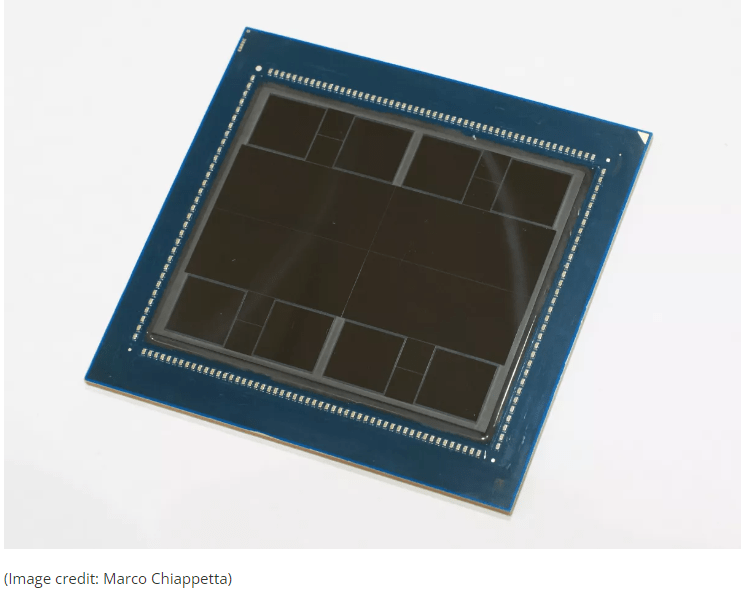

Another example of this technology innovation from AMD in Data Centers was announced at the CES show – the new MI300 data center APU, expected to be available by mid-2023. As explained in this review from Tom’s Hardware (bold emphasis mine), the MI300 is a monster device with 123 chiplets and 146 billion transistors, implemented using 3D stacking to create a 24 Zen 4 CPU core integrated with a CDNA 3 graphics engine and 8 stacks of HBM (high bandwidth memory).

Make no mistake, the Instinct MI300 is a game-changing design.

The 3D design allows for incredible data throughput between the CPU, GPU and memory dies while also allowing the CPU and GPU to work on the same data in memory simultaneously (zero-copy), which saves power, boosts performance, and simplifies programming.

new MI300 data center chip (Tom’s Hardware)

Risks to AMD and Intel

A drop in demand in enterprise data centers could pose a risk to both AMD and Intel. If there really is a big global economic slowdown or even recession in 2023, demand for new data centers could retreat causing some pricing and inventory issues to develop. If there really is a major slowdown in business growth in 2023 as some are predicting, the demand for enterprise and cloud solutions may weaken, which could impact pricing power and lead to a price war.

My own research looking at other companies that provide equipment and services to data centers, is that just the opposite is occurring, and demand is actually picking back up again after slowing down in the second half of 2022. For example, Super Micro (SMCI), who make application-optimized total IT solutions for data centers, AI, HPC, enterprise and cloud infrastructure, announced updated guidance for their fourth quarter earnings report.

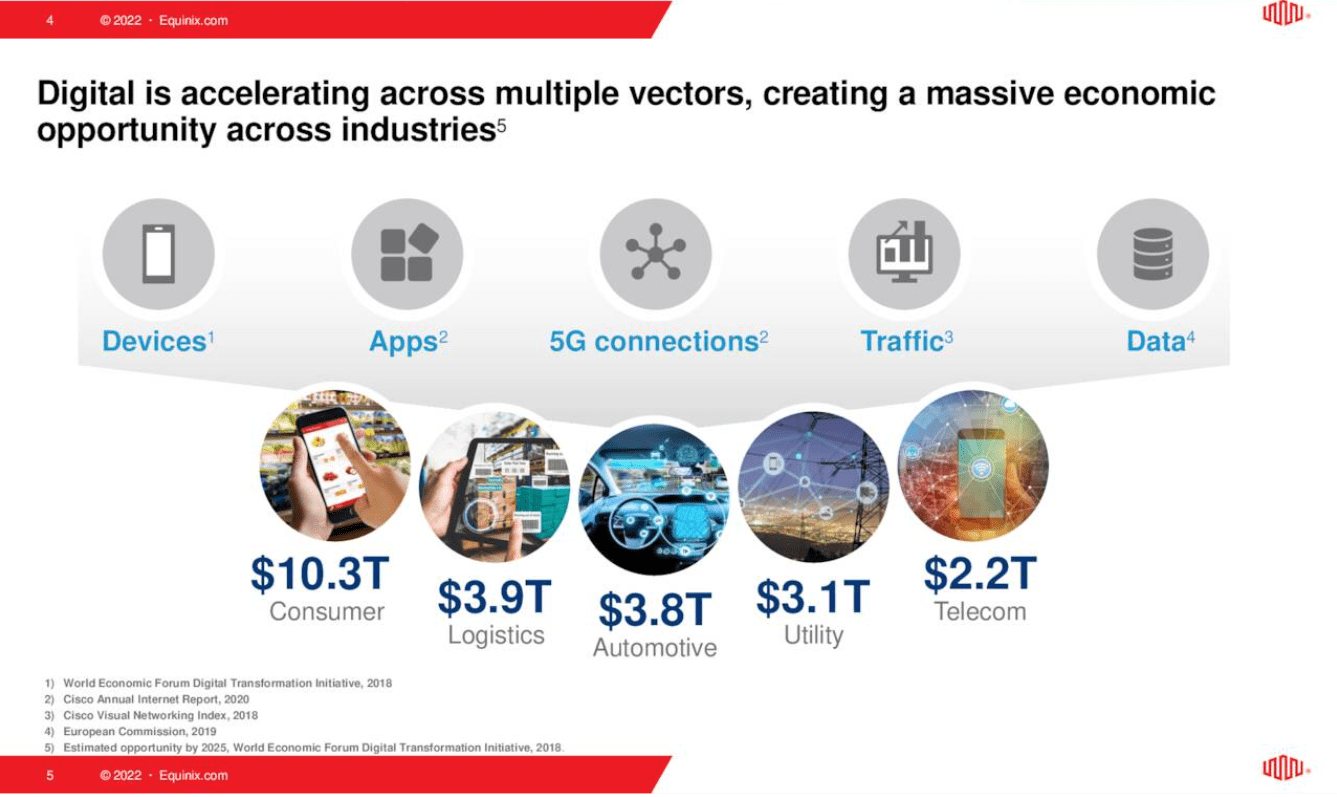

Also, EQIX, one of the biggest data center REITs with a market cap of $67B, was rated a “best idea to outperform” in 2023 by Cowan. This slide from the EQIX Q322 investor presentation illustrates the growing market for digital data centers across multiple industries. AMD offers solutions to most, or perhaps all of them.

Equinix

AMD Financial Performance

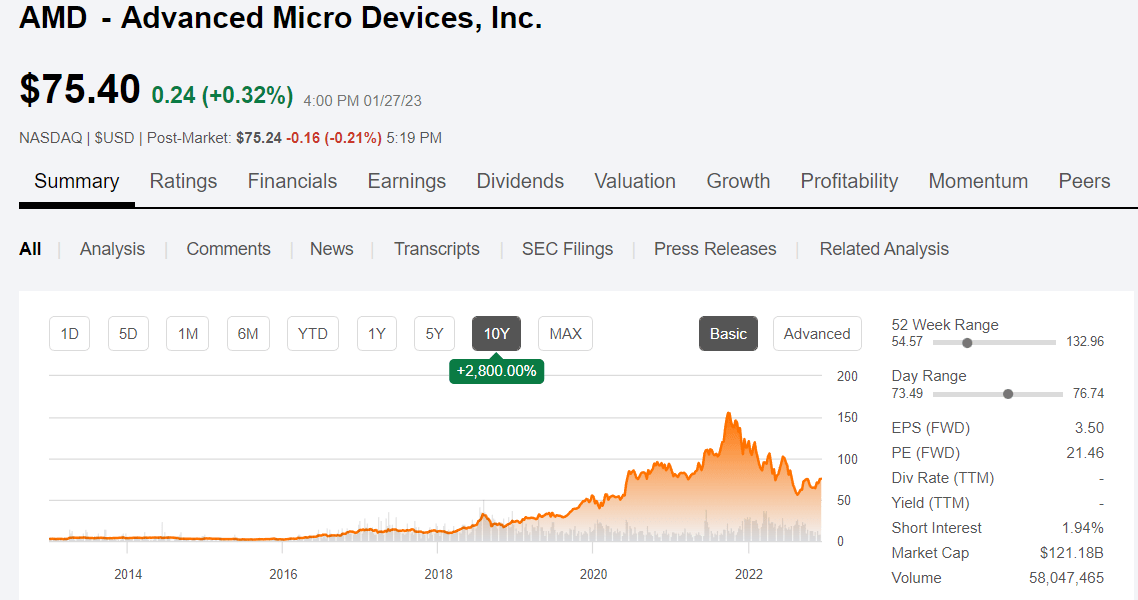

While AMD stock was on a tear for most of the ten-year period leading up to the end of 2021, investors got accustomed to incredible growth with revenues and earnings beating consensus estimates. But that all changed at the end of 2021. After hitting an all-time high price of $155 in November 2021, the stock came crashing down, losing over half its value in 2022, now trading for around $75.

Seeking Alpha

In the most recent Q322 earnings report from November 1, AMD missed estimates by a slight amount, and offered reduced guidance for full year 2022 revenues, although still expecting an increase of 43% over 2021 led by Embedded and Data Center segments. The stock price bottomed at just below $55 prior to that report and has been on the rise since then.

AMD

At the time, guidance for fourth quarter revenues suggested very little to no growth from the previous quarter (“only” $5.5B) and about 14% YOY growth, although Embedded and Data Center segments are expected to continue to grow both YOY and sequentially.

Now, as we approach the Q4 report coming up next week, some analysts are downgrading expectations due to continued sluggish growth in PC markets, although data centers and embedded segments still show signs of growth to offset those losses as a result of AMD’s Genoa series chipsets offering better technology that Intel’s Sapphire Rapids chipsets. One analyst, Vivek Arya from BofA, has a Buy rating on AMD due to that technology advantage:

Regarding the server space, Arya noted there are some “cycle risks,” but that AMD is continuing to gain share in the lucrative market. Arya said he anticipates “a healthy ramp” for AMD’s 5-nanometer Genoa chipset over the Intel 7 Sapphire Rapids products set to be launched this week. Arya added that AMD (AMD) could have as much as 28% of the server market in 2023, up from 23% in 2022 and ultimately get to 31% next year.

With continued growth in data centers, embedded systems, and high-performance computing/AI ramping up again in 2023, I anticipate that AMD will be reporting better than expected earnings and is likely to offer updated forward guidance for the year as well.

Another recent article on AMD from fellow contributor Juxtaposed Ideas expresses an optimistic view of AMD’s future prospects due to the growing interest in ChatGPT, a popular AI model that requires high performance computing power. The rise in demand for AI applications such as ChatGPT demonstrates the increasing need for semiconductor solutions from companies like AMD and Nvidia (NVDA) that enable high performance computing in support of those AI platforms and applications.

Seeking Alpha

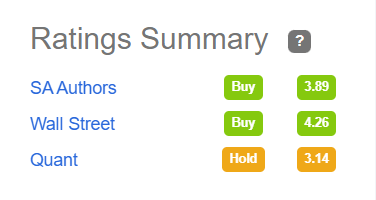

I am going to take the side of the majority of SA authors and Wall Street analysts who rate AMD a Buy. I had sold off all my AMD shares last year when the price dropped below $90 but just started buying shares again for about $75. With a forward P/E of 21x earnings estimates, AMD stock is not the screaming bargain it once was, but with the tailwinds from data center expansion and new technology offerings from the Xilinx and Pensando acquisitions now being offered and integrated into new chip designs, I believe that AMD will reinvigorate growth and the stock will outperform over the next 5 to 10 years.

Meanwhile, I will be watching and reading closely when AMD reports on Tuesday January 31st after the closing bell.

Be the first to comment