Justin Sullivan

Thesis

Advanced Micro Devices, Inc. (NASDAQ:AMD) stock has recovered remarkably from its July lows as the market anticipated a robust Q2 release. However, its post-earnings momentum has stalled somewhat after surging through July.

In our previous article in June, we posited that AMD could stage another low before recovering. We had suggested investors wait for a deeper pullback closer to $70 before pulling the buy trigger. Therefore, we aren’t surprised that AMD staged its July bottom at our posited levels, in line with the market’s bottom.

We believe AMD’s underlying metrics, strong execution, and market share gain potential augur well for its medium-term re-rating at the current price levels. In addition, its price action has also likely bottomed out on its long-term chart as AMD looks towards its data center and embedded segments to continue gaining share rapidly. Therefore, we are confident that the improved buying sentiments on AMD indicate a re-rating, which should help lift buying momentum further.

As a result, we reiterate our Buy rating on AMD. Notwithstanding, we posit that AMD will likely face near-term downside volatility, given its rapid surge from its July lows. Therefore, investors can consider waiting for a pullback first before adding exposure.

AMD’s Diversified Business Helps Overcome Consumer Headwinds

The recent consumer spending headwinds, exacerbated by worsening macros, have also buffeted AMD. As a result, management revised its Q3 PC outlook from a decline in the high-single digits to the mid-teens, as discrete graphics also disappointed. Yet, AMD performed admirably in the data center and embedded segments as it continued to gain share against Intel (INTC).

The headwinds against NVIDIA (NVDA) in the discrete GPU segment are not trivial. Even though NVIDIA highlighted its troubles in a prelim Q2 release in early August, the challenges could beset it for the rest of H2’22. A DIGITIMES report in August highlighted:

Taiwan’s major graphic cards suppliers have estimated their 2022 shipments to fall 40-50% on year due to a sharp decrease in demand for cryptomining applications, with prices also trending downward. Accordingly, Nvidia’s revenues for both second-half 2022 and the whole year are estimated to fall at a pace beyond imagination, the sources indicated. – DIGITIMES

Therefore, AMD’s ability to gain share steadfastly against Intel is an excellent hedge against the consumer headwinds, helping undergird its valuations. Notably, the prelim report from Omdia suggested AMD continuing its server market share gains, reaching 22.7% in Q2. In contrast, Intel saw its server market share fall further to 69.5% in Q2, down from Q1’s 72.7%, as AMD and Arm architecture chips gained ground.

AMD CEO Dr. Li Su also alluded to its superb performance in data center in response to an analyst question on market share in the recent earnings call. She also sees more potential for further gains as AMD remains “under-represented.” She articulated:

I know you guys have been asking about [market share] for a while. So I think your math is in the ZIP code [of around mid-20%] from our point of view. And we’re pleased that we’re gaining share. And we will continue to focus on that going forward. I think we continue to see significant growth opportunities as we go into the second half of the year and into 2023 just given our strong product positioning. We see Milan continuing to ramp into the second half of the year, and then we see Genoa coming in towards the end of the year into 2023. So we’re a larger piece of the market, but we are still underrepresented. And the visibility with our customers, especially our large cloud customers, second half of this year into next year is very good. (AMD FQ2’22 earnings call)

We are confident that AMD’s superb execution under Dr. Su’s remarkable leadership provides clear revenue visibility into AMD’s near- and medium-term growth cadence. Therefore, we are quietly confident that the company should remain on track to meet its 20% revenue CAGR target over the medium-term, despite facing pretty intense consumer headwinds through H2’22.

As AMD continues gaining share through its data center and embedded segment, it should help mitigate the challenges seen in its client and gaming segment (mainly its discrete GPU). Furthermore, AMD’s guidance seems somewhat conservative, and Dr. Su highlighted that its estimates had de-risked the headwinds from the PC business. Nevertheless, we are confident that management is on top of the situation and urge investors to stay on track, as AMD should emerge stronger from it.

AMD’s Price Action Suggests Near-Term Consolidation

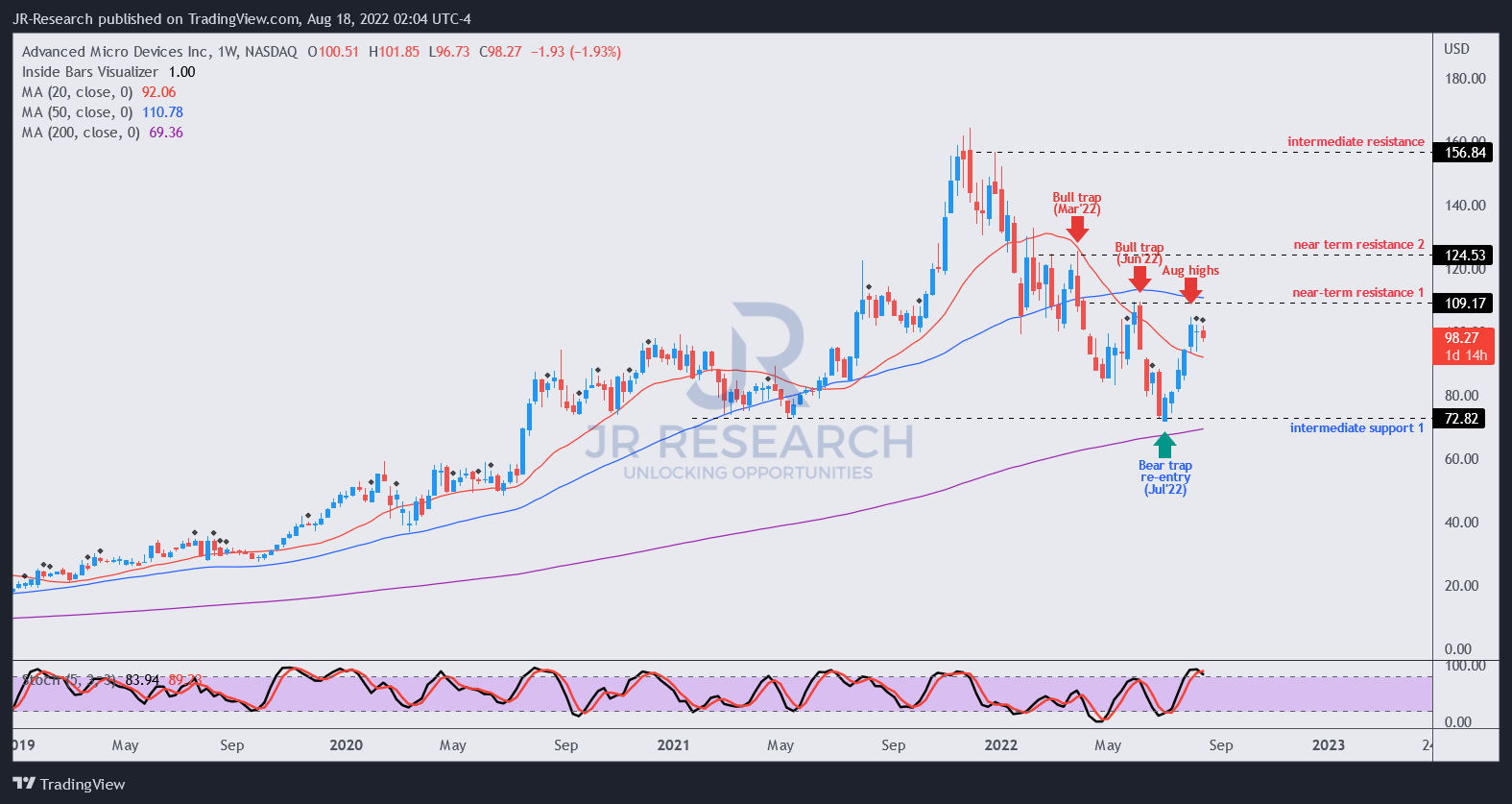

AMD price chart (weekly) (TradingView)

As seen above, AMD formed its July lows close to its intermediate support of $70, as we posited in our previous article. We are confident that AMD has likely staged its medium-term bottom, in line with our assessment of the market’s medium-term bottoming process.

However, the rapid surge from its July lows has surprised us. Also, AMD’s buying momentum has stalled post-earnings, which suggests that the market had anticipated a robust card pre-earnings, leading to the rapid recovery.

We posit that a near-term consolidation in AMD is looking increasingly likely, as the market digests the bullish momentum from its July lows, given its overbought breadth and momentum indicators.

Hence, investors can consider adding more aggressively at its next meaningful pullback.

Is AMD Stock A Buy, Sell, Or Hold?

We reiterate our Buy rating on AMD.

We have re-rated AMD, requiring lower free cash flow yields, as we are confident that the market has lifted the buying sentiments over it. Coupled with the company’s solid execution and market share gains visibility, we urge investors to use potential downside volatility to add exposure, as AMD is not expensive.

Be the first to comment