RichLegg/E+ via Getty Images

Investment Overview

Alvotech (NASDAQ:ALVO) is an ~800 employee company, founded in Reykjavik, Iceland, that is “focused exclusively on developing and manufacturing biosimilar medicines for the global market”.

Its founder and Chairman, Róbert Wessman, has an impressive track record in the Pharmaceutical industry, having also played an instrumental role in the growth of Actavis into a globally significant generic drug company before it became Allergan, and sold its generics business to Teva Pharmaceuticals (TEVA) in a $41bn deal. Wessman also founded Alvogen, a contract manufacturing organization (“CMO”) based in the US which went to become another generics drug company of renown.

Alvotech joined the Nasdaq on June 16th this year, completing a business combination with the Special Purpose Acquisition Company (“SPAC”) Oaktree Acquisition Corp that included a $175m private investment in public equity (“PIPE”) financing, and the company completed a dual listing on the Icelandic stock exchange days later.

Alvotech’s lead product is AVT02 (adalimumab), a biosimilar version of AbbVie’s globally best-selling (>$20bn of revenues in FY21) autoimmune drug Humira.

Although it has other biosimilars in development – e.g. for Johnson & Johnson’s (JNJ) autoimmune drug Stelara – ~$7bn annual sales – Amgen’s bone density drug (AMGN) Prolia – ~$837m annual sales – Regeneron’s (REGN) eye disease therapy Eylea – ~$7bn annual sales – and Novartis’ (NVS) asthma indicated Xolair – >$3bn annual sales – Humira is Alvotech’s most important target and AVT02 the closest to making it to market.

In September this year, Alvotech received a Complete Response letter from the FDA denying its marketing application for AVT02 – which has already been approved in Switzerland and number of other European countries under the brand name Hukyndra, and in Australia, under the brand names Ciptunec and Ardalicip.

According to a press release, the FDA:

noted certain deficiencies related to the Reykjavik facility and stated that satisfactory resolution of the deficiencies is required before FDA may approve this BLA

The news rocked Alvotech’s share price, sending it as low as <$6 by mid-November, but yesterday, the FDA confirmed a new goal date for an approval decision on April 13th, 2023, stating that:

the data provided are sufficient to support a determination of interchangeability; approval requires satisfactory outcome of upcoming facility reinspection

Alvotech’s 280k square foot manufacturing plant in Iceland has passed inspections by the European Medicines Agency (“EMA”) and the Integrated Medicine Alliance (“IMA”), and the investment in this facility, experience of CEO Wessman and his staff, and importance of AVT02 to the company suggests to me that the FDA will give the green light to the biosimilar’s approval next year, and allow Alvotech to formally launch the drug commercially in July.

The market seems to be in agreement, as Alvotech stock has risen in value to $10 at the time of writing – the same as its listing price – valuing the company at $2.4bn.

An April approval would complete a lengthy saga that has involved lawsuits submitted by AbbVie, accusing Alvotech of stealing trade secrets, after poaching an AbbVie employee who allegedly emailed themselves “confidential and proprietary information”, and counterclaims from Alvotech which accuse AbbVie of creating a “patent thicket” around Humira.

The delay of its approval for AVT02 may not necessarily hurt Alvotech – almost every generic or biosimilar manufacturer – Amgen, Boehringer Ingelheim, Organon (OGN) / Samsung Bioepis, Viatris (VRTS) / Biocon, Sandoz / Novartis – have FDA approved Humira biosimilars, but none can launch in the US market until July 1st.

The level of competition may be problematic for Alvotech – and its rival biosimilar manufacturers – however, since there is no knowing in advance exactly how Humira’s loss of patent protection, or “loss of exclusivity” (“LOE”) will play out.

In the rest of this post I will discuss Alvotech’s business in some more depth, but first I’ll speculate about what the Humira LOE may mean for Alvotech and the value of its shares over the next couple of years.

Humira (Finally) Exits Stage Left – What To Expect

It’s no secret that AbbVie has fought hard for more than a decade to try to maintain patent protection for Humira, and prevent generic versions of the drug being made available.

I discussed this issue in some detail in a note for Seeking Alpha on AbbVie CEO Rick Gonzalez’ grilling by house representatives in May 2021. Humira has been awarded a staggering 130 US patents, and AbbVie stands accused of creating “frivolous” new patents relating to e.g. minor manufacturing changes in order to keep generic drug manufacturers away from its turf.

Had it not been for these new patents, Humira may have gone off patent back in 2017, but instead, with protection in place, the drug made sales in the US of $13.7bn, $14.9bn, $16.1bn, and $17.3bn between 2018 – 2021.

AbbVie’s response to critics is that without patent protection there is no incentive to innovation, i.e. having spent billions on R&D to develop an essential drug in the first place, it is only right the company should be permitted a lengthy period of exclusivity.

That may be so, but even AbbVie would probably concede that it has earned a staggering ROI on the funds it spent developing Humira, and there is no doubt that Humira’s sales will begin to plummet once the generics enter the market on July 1st.

For context, we can look at how Humira sales have changed since the drug lost its patent exclusivity in Europe in 2019. Sales in 2018 had been $6.3bn, but fell to $4.3bn in 2019, $3.7bn in 2020, and $3.36bn in 2021 – declines of 31%, 14% and 10% respectively.

If we therefore assume that Humira sales in 2022 are more or less the same as in 2021 – $20.7bn, and reduce that figure by 31% (the percentage decrease of sales revenues in Europe in 2019) for 2023, we can expect sales of ~$14.3bn, and correspondingly, ~$12.2bn in 2024, and ~$11bn in 2025.

Unfortunately for the generic drug manufacturers, it does not necessarily follow that the ~$7bn fall in Humira revenues in 2023 will be evenly distributed amongst them, or that there will ~$10bn of revenues to compete for in 2025.

Since generic drug manufacturers spend only a small amount on R&D, given they do not have to invest in the discovery a new drug, but merely figure out how to manufacture a version of an existing one, their generic drugs tend to have much lower price points than the original drug. Humira will not simply lose revenues due to lost sales volumes, but also because AbbVie will be forced to slash the price of Humira.

In researching the likely pricing of adalimumab biosimilars when launched, I came across an interesting interview of Marcus Snow, MD, chair of the American College of Rheumatology’s Committee on Rheumatologic Care, discussing previous generic drug pricing as follows:

In the European Union, biosimilars of Humira had taken a 59% share of the market by February 2021. Experience in the United States with biosimilars for other rheumatology biologic drugs suggests that biosimilar pricing has been very competitive. From the fourth quarter of 2019 to the second quarter of 2021, three biosimilars of Rituxan captured a 55% share of the Rituxan market. By the end of that period, one of those biosimilars, Truxima, was offered at a 36% discount to the originator’s price (before biosimilar competition).

The average sales price of the anti-inflammatory drug Remicade dropped 49% from the end of 2016 to the second quarter of 2021. Remicade biosimilars, however, achieved just a 26% share of the market from Remicade in that time. One difference that might explain the better uptake for Rituxan biosimilars is that Rituxan had dropped just 6% in price by the second quarter of 2021, whereas the makers of Remicade had discounted that product much more heavily.

In other words, the success of Alvotech’s AVT02 is dependent upon a number of pricing factors, including how much AbbVie may drop the price of Humira – currently a year’s supply of the drug costs ~$84k, although insurers cover most of that cost – and how much other generics drug manufacturers charge for their versions. We may see some kind of “race to the bottom” with companies lowering prices in order to drive volume, and that may not be good for business.

Sources suggest there could be as many as 11 adalimumab biosimilars on the market by the end of 2023, fighting over a market that is, let’s say for the sake of argument, 50% less than the decline in Humira sales, so ~$3.5bn in total. That may imply that the peak sales opportunity for a newly launched Humira biosimilar is ~$300 – $350m.

What To Expect From Alvotech in 2023 & Beyond

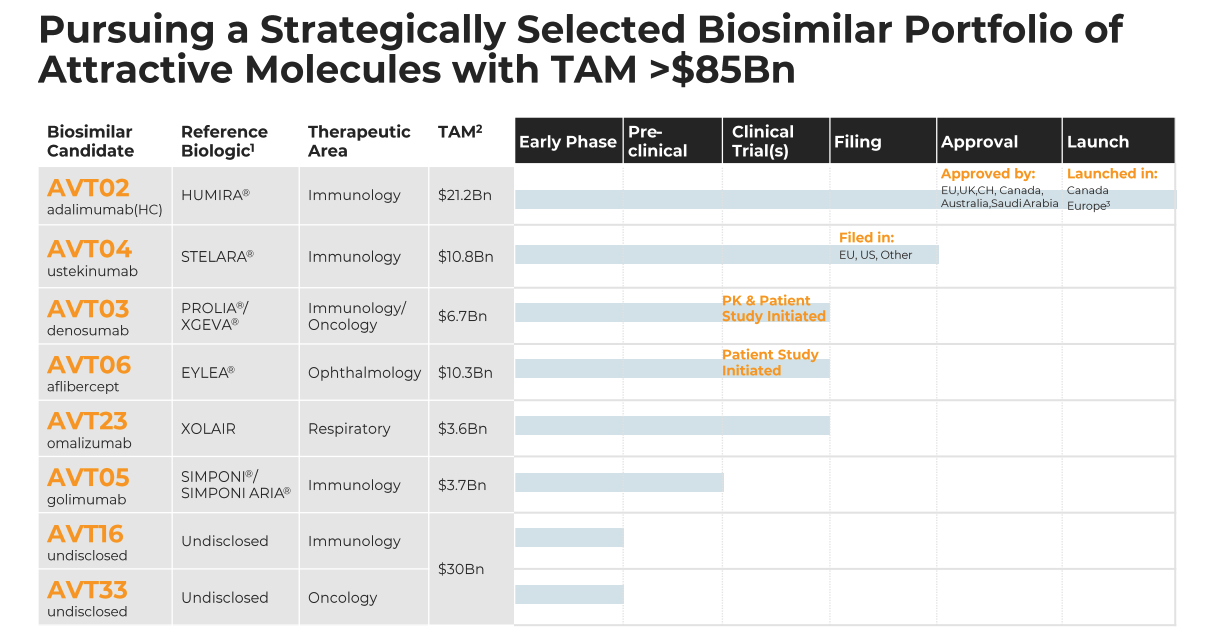

As we can see below in a slide from a recent investor presentation, Alvotech’s biosimilars pipeline addresses a total addressable market (“TAM”) of ~$85bn per annum.

Alvotech pipeline (investor presentation)

As we now know, however, $85bn is essentially a meaningless number in terms of Alvotech’s own market opportunity. In the case of Humira, the price point will fall, there will be 10 other companies competing for the same market share, and we may throw in more obstacles besides.

Many prescribing physicians remain skeptical of whether a biosimilar drug is genuinely as effective as the original, and may simply continue to prescribe Humira, at a lower price. The effect of prescribing biosimilars on a physician’s practice revenues is also presently unclear, but an obvious concern. Physicians who have worked with AbbVie for many years may be unwilling to switch.

Then there are formulary lists, which the biosimilars need to be selected for to stand any chance of being prescribed at all – and given Humira is indicated for a wide range of autoimmune conditions – ankylosing spondylitis, psoriatic arthritis, Crohn disease, ulcerative colitis, and rheumatoid arthritis – there will be concern around whether biosimilars work equally well across all different indications.

To summarize, the fact that Humira was an all-time best-selling drug does not necessarily mean that a biosimilar version of the drug will be anything close to a blockbuster (sales >$1bn per annum). There is simply too much availability of product, price competition, resistance to prescribing biosimilars, and not to mention new drugs on the market.

AbbVie, for example, has recently launched 2 new drugs – Rinvoq and Skyrizi – which between them are expected to secure approval in all of the markets in which Humira is currently prescribed.

Combined peak sales expectations for the 2 drugs are forecast by AbbVie management to be >$15bn – in other words, AbbVie management believes that Skyrizi and Rinvoq’s superior efficacy and safety profiles versus Humira will lead to physicians prescribing them over either Humira itself, or any biosimilar version of Humira.

All of this makes things very tricky for Alvotech. We can safely assume that all of the other targets on Alvotech’s hit list – from Stelara, to Eylea, to $3.7bn per annum selling Simponi – present a similar set of problems – so how does Alvotech generate a volume of annual revenues to justify its $2.4bn valuation?

If we assume that AVT02 is approved by the FDA and goes on to make our target $350m sales per annum, then we could also assume that a Stelara biosimilar can generate ~$175m revenues per annum based on its TAM being 50% of Humira’s, and that that figure would be the same for an Eylea biosimilar, perhaps ~$100m for a Prolia biosimilar, and ~$50m for Xolair and Simponi.

That gives me a rough total of >$900m in annual revenues should Alvotech go on to commercialize all of its current pipeline assets, and the potential to add at least another ~$500m per annum if its undisclosed targets work out also. $1.4bn revenues easily supports a $2.4bn valuation based on the low price to sales ratio of <2x, with some leeway for assets failing to make it to market – even when the revenue forecast is halved, the P/S ratio is not necessarily excessive at <3.5x. We can therefore make a good case for share price upside potential based on forecast revenues, but at this stage we do not know what the profitability of the company may look like.

If we study the financials of one of Alvotech’s partners – Teva Pharmaceuticals – for example, we can note that in 2021, its revenues were $15.9bn, gross profit $7.6bn, operating income $3bn, and net income $417m. That implies a net income margin of ~2.5%, although it should be noted in each of the previous 4 years Teva made heavy losses.

If we are generous and use the operating margin figure of ~19%, we can estimate Alvotech profits to be ~$240m, which works out at nearly $1 per share earnings, which translates to a forward price to earnings ratio of ~10x – very reasonable, and enough to suggest that Alvotech’s share are a buy.

Conclusion – Alvotech Remains A Risky Play Given Nothing Can Be Taken For Granted In The Biosimilars Market

There are a number of reasons for investors to believe that it is worth paying ~$10 per share for Alvotech stock at the present time.

The likely approval of its Humira biosimilar. The rest of the pipeline covering targets such as Eylea, Stelara, and Prolia. The experience of a CEO and the success he has had with other companies. The progress of biologic drugs – apparently this drug class represented 70% of the growth in U.S. drug spending between the years 2010 and 2015, whilst the market for biologic drugs is expected to reach >$700bn by 2030, from ~$366bn today – and the fact that it is relatively straightforward to produce biosimilar versions of biologic drugs.

With that said, there are several reasons why investors may be cautious about investing. The level of competition – as many as 11 biosimilar versions of Humira may hit the market in 2023 – the downward pricing spiral, skepticism amongst prescribing physicians and patients, and the difficulty associated with making it onto formulary lists and securing favorable reimbursement deals.

Alvotech’s AVT02 is not yet approved, let alone included on the formulary lists of major Pharmacy Benefit Managers (“PBMs”), whilst Amgen’s Amjevita, for example, will apparently be included on Optum Rx’ list next year, giving it a major headstart.

AVT02 is essentially the jewel in Alvotech’s crown, so if it’s not a success, the market will be increasingly skeptical about the company’s prospects of succeeding with smaller scale biosimilars such as an Eylea or a Simponi biosimilar. Alvotech also made a loss of $355m in the first 9m of 2022, and its cash position is relatively weak, with current assets being reported as $153m as of Q322.

As such, it’s tough to make a call on what price we may see Alvotech’s share price trending towards by the end of 2023. Personally, if, as I expect, AVT02 is approved, there will likely not be enough commercial data by the end of next year to make an informed judgement on its likely success, but there will be some goodwill from the market.

I could therefore see Alvotech’s share price pushing towards $15, and a market cap valuation of ~$3.7bn as I believe the excitement generated by a first commercial approval will be greater than skepticism around future revenues or level of competition.

I would stop short of recommending Alvotech as a strong buy opportunity, as I expect there to be a much discussion of the commercial viability of biosimilars in the coming years, which may be more negative than positive.

It was instructive, for example, to see Viatris, a spin out of Pfizer’s (PFE) Upjohn legacy brands division merged with generic drug manufacturer Mylan, offload its entire biosimilars division to the very first bidder.

Viatris does still hold a small stake in the acquiring company, Biocon, but that deal speaks to some underlying skepticism around biosimilars that needs to be fully explored, in my view, before the industry can be said to justify the hype.

Be the first to comment