Mario Tama/Getty Images News

Introduction

Altria Group Inc. (NYSE:MO) shares fell 9.2% on June 23 after the Wall Street Journal reported that the Food and Drug Administration (FDA) has banned all of Juul Labs’ vape products from the U.S. market in a widely anticipated move that one could argue had already been discounted in shares of MO.

MO paid $13 billion in 2018 for a one-third stake in Juul. Altria has already written down all but $1.7 billion of its original investment in Juul. With a formal ban on the vape products, it was a one-two punch for MO shares.

The FDA has the power to regulate nicotine as an addictive drug. As such, nicotine vape products have had to file PMTA applications (Premarket Tobacco Product Approval) to keep their products on the market. The FDA said that Juul’s applications had insufficient toxicology data on its e-liquid pods which contain the consumable nicotine.

Juul said it would seek a stay of the FDA ban and consider appeals. The company’s products apparently will remain on the market during the appeals process.

Below is the long process that MO is up against when working through the FDA process.

Alteria.com

Philip Morris International (NYSE:PM) and MO typically have been solid defensive plays in recessions. MO and PM pay high, generally sustainable dividend yields and might be considered in a well-rounded portfolio.

History

PM was an operating company of MO until a spinoff in March 2008. This was widely seen as a way for PM to have more freedom from the rules and standards that a US based company could potentially have in regards to potential litigation and legislative restrictions. MO also appeared to see the spinoff as an easier way to pursue sales growth in emerging markets. PM’s operational headquarters are in Lausanne, Switzerland. To confuse things a bit, MO is the parent company of Philip Morris USA which is the producer of Marlboro cigarettes.

PMI.com

Outlook Overview

Like MO, PM manufactures and sells cigarettes, other nicotine-containing products and smoke-free vape products as well as related electronic devices and accessories.

The pandemic led to many lifestyle changes and different types of stresses which drove tobacco sales up. As a first in 20 years, cigarette sales increased in 2020 according to a report from the Federal Trade Commission. Its annual Cigarette Report shows that manufacturers sold 203.7 billion cigarettes in 2020, a 0.4% increase from 202.9 billion in 2019. The report does not include sales of e-cigarettes.

As a side note, marketing increased from $7.62 billion in 2019 to $7.84 billion in 2020, with the bulk of spending on price discounts paid to cigarette retailers and wholesalers.

Strict FDA regulations and plans to force nicotine cuts in cigarettes have incentivized MO and PM to develop smoke-free products. Apparently, even PM has decided to go smoke free with their newer products as shown below.

PMI.com

Source: PMI.com

Both companies are generally positioned to perform well in recessions – especially if the future is like the past. The U.S. tobacco market is expected to grow at a 3.4% CAGR to reach $102.70 billion by 2030.

Grandviewresearch.com

Which of these stocks is a better pick now? Keep reading.

How Valuable Is Juul to Altria?

While the reaction in MO’s share price looked overdone, it was a result of Juul being pulled from MO’s revenue and potentially having the company write down the remaining Juul investment on their books.

MO has over a 42% share of the U.S. cigarette market by volume and industry profits, which appear primarily due to Marlboro retail product. With or without Juul, MO seems positioned well to weather this storm. However, increased regulatory pressures mentioned herein will be a headwind for MO. Getting new, acceptable e-vapor products could take years to develop.

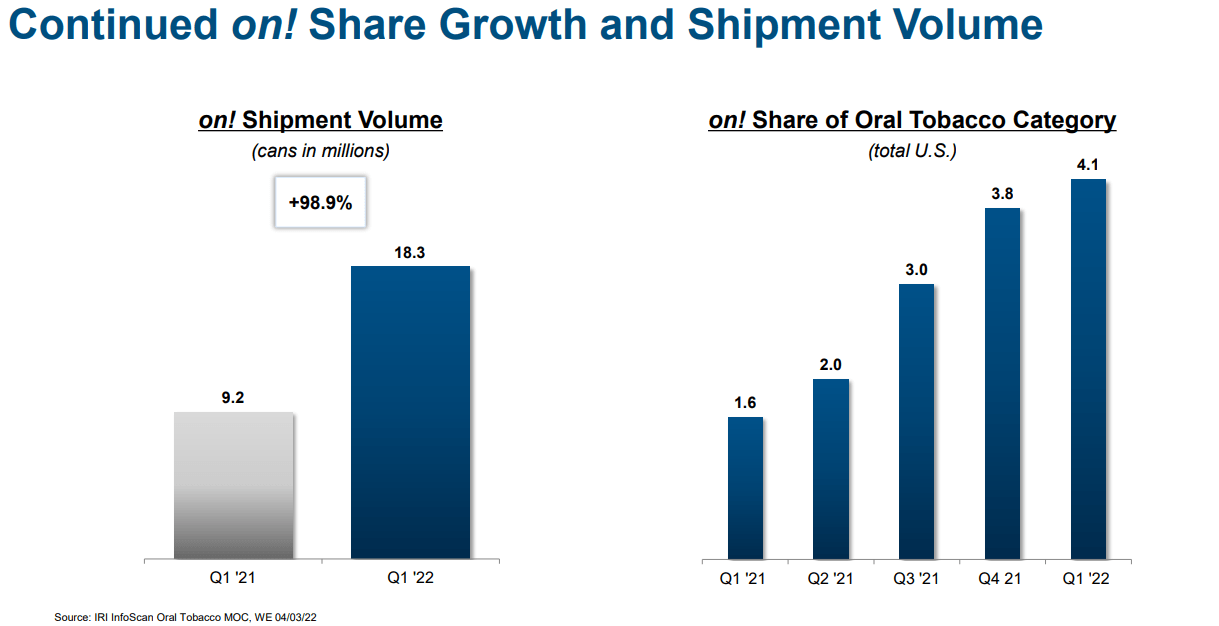

MO is driving growth in its On! nicotine pouches, but this does not directly address the e-vapor market. It is hard to know if these nicotine pouches are converting large numbers of cigarette smokers to the use of On!.

Altria.com

Dividend Yield and Other Key Metrics Comparison

Altria

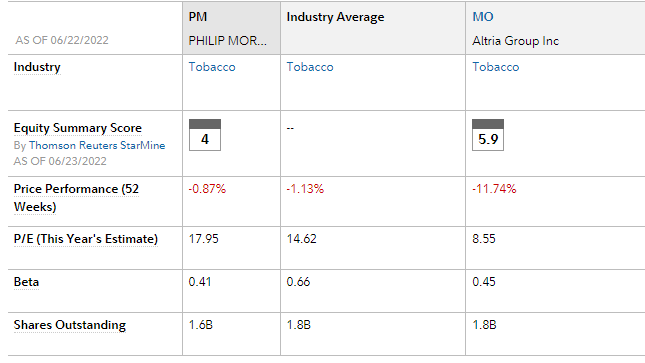

MO stock is attractive at this price with a P/E of just over 25 and a dividend yield of 8.7%. The stock has decreased from a 52 week high of 57 and is now in the 42 price range. MO stock has been depressed due to the Juul rumors and ruling as well as increased costs in labor and products. Cigarettes, especially Marlboro, remains the core business and cash cow for MO.

MO also has a 45% stake in Cronos (CRON). Direction of a Federal-level legalization of marijuana in the United States could present a major value creation and appreciation in MO shares.

Philip Morris International

PM stock has a P/E of just over 17 and a dividend yield of 5.04%. The stock has decreased from a 52 week high of 112 and is now in the 101 price range. PM stock has not taken as big of a hit compared to MO.

The primary advantage that PM has going for over MO it has worldwide reach without the US government influence.

Fidelity.com

Conclusion: Which is a Better Buy – MO or PM

Altria shares fell 9.2% after the FDA ban on Juul products and now has an 8.7% dividend yield and P/E of 25. While PM has a 5% dividend yield and P/E of 17.

With headwinds that both companies are facing with inflation, we believe that both stocks could be under pressure.

However, both should continue to pay their dividend and trudge through the next inflationary and recessionary environments.

We believe investors overreacted and have driven down the price of MO into an oversold range and expect a technical gap fill back to the 47-50 price; however, that is highly dependent on the overall direction of the stock market.

We do not expect much appreciation from here on PM.

To preserve capital, we are looking at either selling a naked put on both MO and PM or a risk defined play of a bull put spread going out 45 days.

For example, one could buy MO here and hope for a drive up and that might not be a bad idea. However, 100 shares will cost you $7,400+ and you get that juicy dividend. As an alternative, one could sell an August 40 put for $116 (at current prices) with a 30 delta and a probability of profit of 67%. If the stock stays above 40, you keep 100% of the premium you collected by expiration. On the other hand, if the stock goes under 40, the stock will most likely get put to you at 40, with a collection of $1.16, your basis is under 38 – creating a dividend yield roughly over 9%.

Be the first to comment