Mario Tama

Introduction

Altria (NYSE:MO) is a well-established company in the tobacco industry with a long history of growth and resilience. The company recently released its Q4 2022 earnings report, with earnings per share coming in at $1.18, beating forecasts by $0.02. The company now projects a growth rate of 3-6% for 2023 earnings per share and has approved a $1 billion share repurchase program.

The stock’s valuation and returns from dividends, share buybacks, and net income growth make it a strong investment option with a projected annual return on investment rate of ~12%. The stock price of Altria appears to be holding strong near its moving averages, making it attractively valued based on fundamentals and its stock chart.

Q4 2022 Earnings

Altria recently released its quarterly earnings report.

Earnings per share came in at $1.18, beating forecasts by $0.02 for the company. However, $5.08 billion in revenue fell short of projections by $66.37 million, or a 0.06% YoY decline. Lower net sales in the category of smokeable products was the main cause of the miss on revenue. Despite this, the adjusted diluted earnings per share grew by 8.3% to $1.18.

Compared to the adjusted diluted EPS base of $4.84 in 2022, the business projects 2023 adjusted diluted EPS in the range of $4.98 to $5.13. This indicates a growth rate of 3% to 6%. Reduced outstanding shares, increased adjusted operating cash inflow, and favorable interest expenses are the main forces behind this growth.

A fresh $1 billion share repurchase program was further approved by the company, and it is expected to be finished by the end of 2023.

Fundamentals

As its net income keeps increasing, Altria continues to show its moat. The average growth rate has been in the low single digits and has largely been attributed to price hikes. The company has not reinvested much of its earnings back into its operations. The ability to grow its bottom line without significant reinvestment is remarkable and a testament to the robustness of its products. Based on expense reductions and the support of inflation-driven price increases, it is plausible that Altria will maintain its trend of low single-digit growth in net income in the future.

As the firm prioritizes dividends and share buybacks over reinvesting earnings, the intrinsic growth and capital gains are closely tied to the stock’s valuation.

The company is boosting intrinsic growth by executing share buybacks that enhance its EPS. These buybacks are currently taking advantage of a favorable valuation, and are estimated to contribute ~2.45% a year at its current earnings multiple. The remaining intrinsic growth will stem from the net income growth, which, as previously discussed, has been and is projected to remain in the low single digits.

When considering the returns from the dividend, share buybacks, and net income growth, a projected annual return on investment rate of around 12% appears plausible. This estimate is based on the assumption that the business will maintain its current earnings multiple and that dividends will be reinvested at a similar rate.

Valuation

Altria continues to demonstrate strength, as shown by its most recent quarterly financial performance. Since 2005, the stock has grown by 8.65% on average each year without seeing a decrease, which is a strong testament to the company’s resilience. Analysts agree with my projection of mid-single-digit EPS growth in the upcoming years.

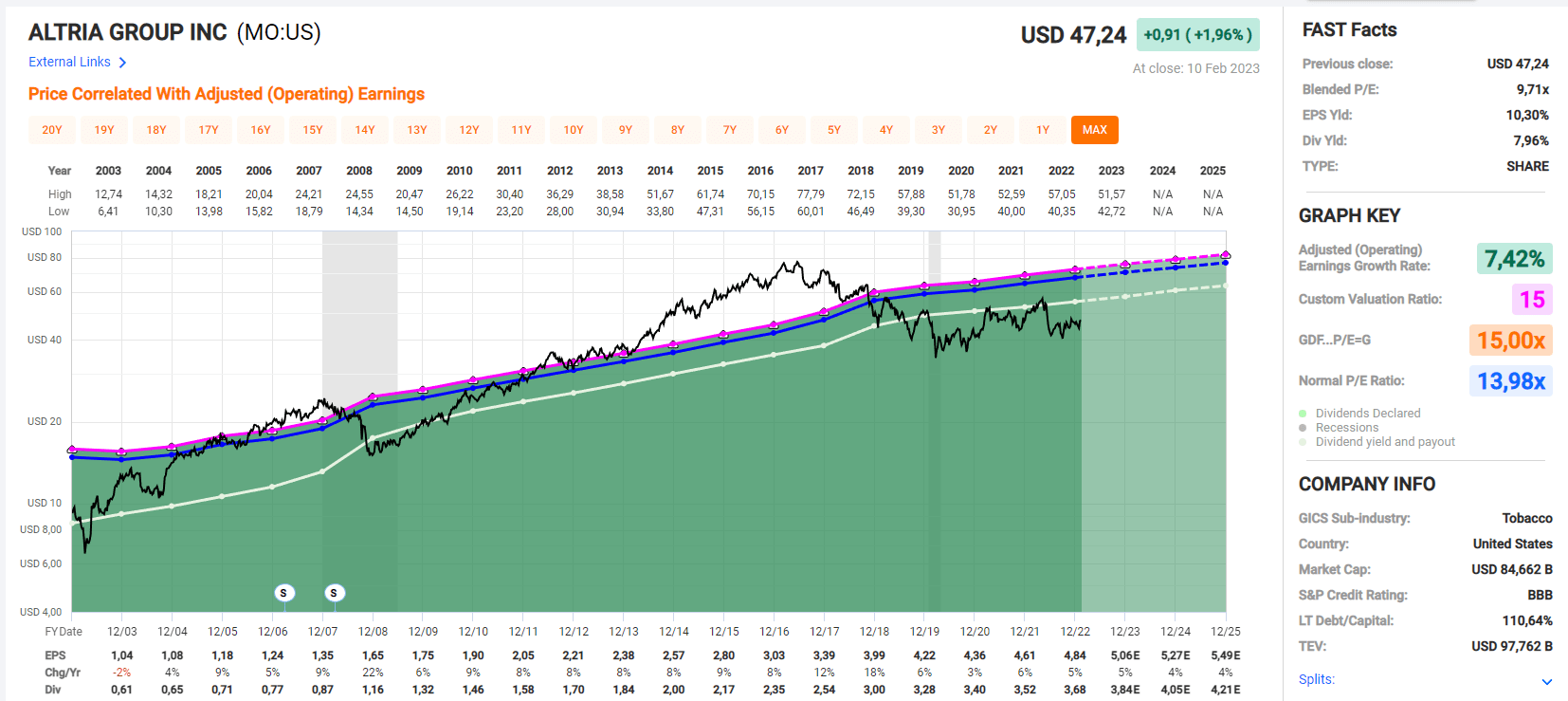

Altria’s current trading multiple of 9.71 is significantly below its historical average of 14.46. While I do think that the stock deserves a higher multiple, I do not believe that a fair value would be its historical average multiple. The company has a substantial amount of net debt, which is currently at $22 billion.

If a standard 15 earnings multiple were applied, which would also be close to its historical average, the market capitalization of the company would be around $130 billion. Adding the net debt to the market cap, the price per share at the new 15 earnings multiple would be approximately $62. Despite the debt, the modest net income growth, combined with the dividend and share buyback payments, and the low net income growth, an annual return of around 12% should be attainable in the future.

Contrary to my previous article about Altria, I no longer believe that an earnings multiple of 15 is appropriate. This is mainly due to the need for a lower multiple to stay competitive and the significant level of net debt. However, the stock still appears very attractive, with a price of ~$62 per share being reasonable.

Fastgraphs.com

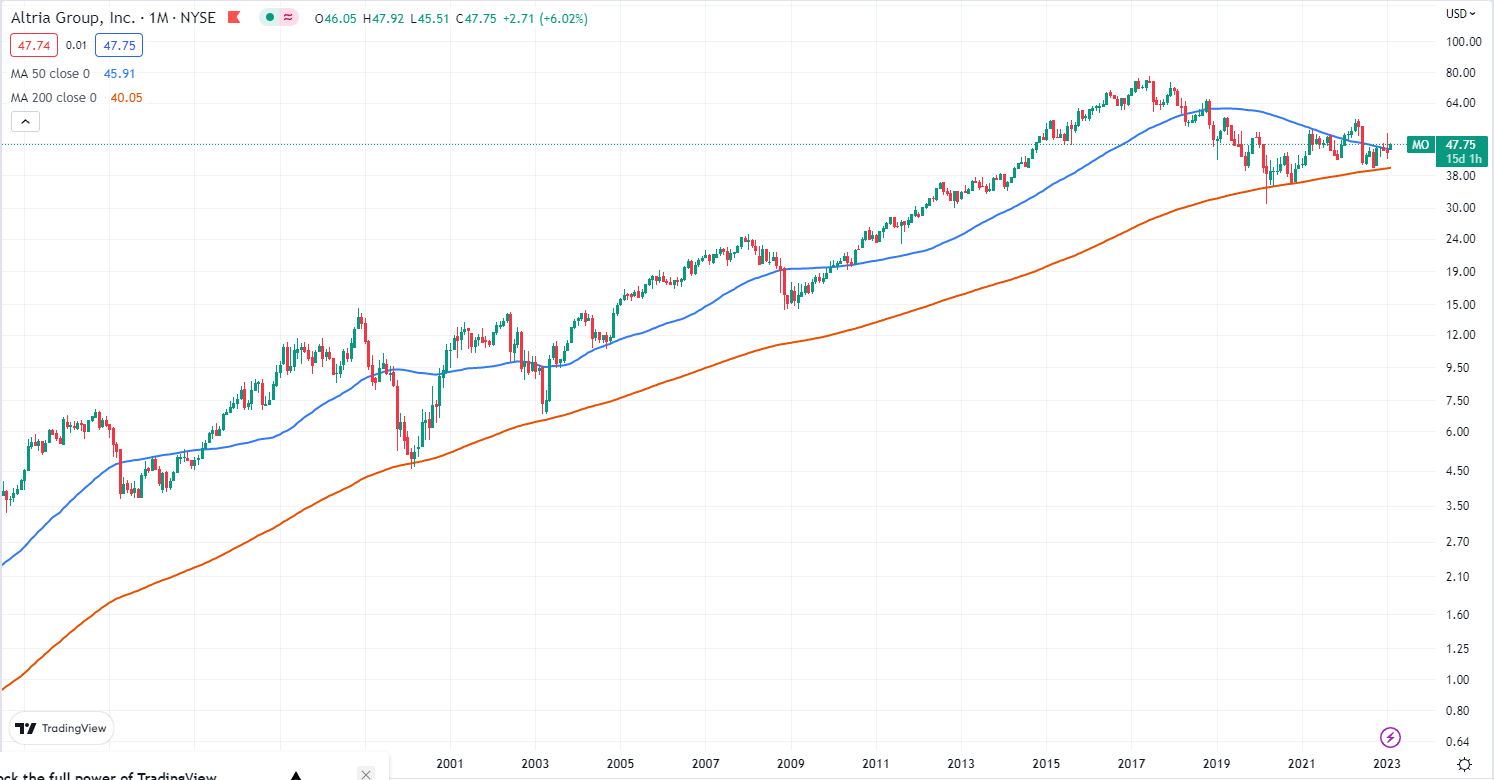

Stock Chart

Quick disclaimer: A technical analysis in itself is not a good enough reason to buy a stock, but combined with the company’s fundamentals, it can greatly narrow your price target range when you buy.

The stock price of Altria seems to be holding strong near its 200-month moving average, just as I had previously mentioned in a past article. This trend has only become more evident following the announcement of an increased share repurchase program and the company’s outstanding performance in their latest earnings report, which has lifted the stock since the announcement.

Given that the stock is still near its 50- and 200-day moving averages, I maintain the belief that it is attractively valued. The fundamentals that have been discussed only strengthen this view.

Tradingview.com

Final Thoughts

Altria is a strong company with a strong history of growth. The primary source of expected capital gains from investing in Altria will come from its dividend payments, which are tied to the stock’s valuation. Share buybacks are also boosting intrinsic growth by enhancing its earnings per share. The company is expected to maintain a low single-digit growth rate in net income in the future, which combined with dividends and share buybacks, should result in an annual return on investment rate of around ~12%.

Altria is currently trading at a lower multiple compared to its historical average, which I believe largely is due to its significant level of net debt. Despite this, the stock still appears attractive, and its strong support near its 200-month moving average, combined with the fundamentals of the company, make it a strong investment opportunity.

Based on the company’s fundamentals and attractive valuation, I adjust my price target to ~$62 per share and give it a “buy” rating.

Be the first to comment