Huber & Starke

Altice USA, Inc. (NYSE:ATUS) is a holding company that operates through its subsidiaries. With its well-known brands, such as SuddenLink and Optimum, the company provides broadband communication and video services in the United States. In 2019, the company launched a full-service mobile offering to customers across its footprint.

Currently, the management is focusing on building an FTTH network, which will enable it to deliver multi-gig broadband speeds to comply with rising demand.

Also, residential data and business services contribute significantly to the revenue. As the company has been upgrading its technology and services, the data segment will see a significant improvement in business operations.

Residential services –

With its strong HFC network, the company provides its customers with a high-speed broadband network. The segment also operates in video, telephony, and mobile services. As the management is putting significant efforts into developing the segment, their effort to bring new and innovative technology might help the company to gain a substantial market share in the upcoming years.

Business services –

The segment offers a wide range of services to large and medium-sized enterprises. With its Lightpath bandwidth connectivity service, the company offers data speed of up to 100GB to its clients.

News and advertising –

The company owns well-known news networks like News 12 Networks, cheddar, and i24NEWS.

These business segments have been producing considerable profits for the company. The business model seems substantially robust as the company has been producing considerable cash flows. Still, in my view, due to its significantly high debt, any bad news can cause a huge stock price correction. Therefore, it is better to avoid companies with significant debt burdens, which bring substantial risk to the business model.

Historical performance

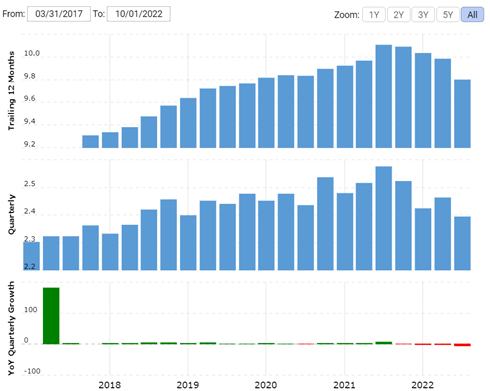

Revenue (macrotrends.net)

Since its public offering, revenue has increased slightly from $9.3 billion in 2017 to about $10 billion by 2021. Despite posting substantial revenue, the net profit margins have remained significantly volatile. After dropping to $18 million in 2018, net profits have increased to over $990 million till last year. It should be appreciated that management has been focusing on share buybacks; as a result, the share count has come down from 730 million to about 453 million.

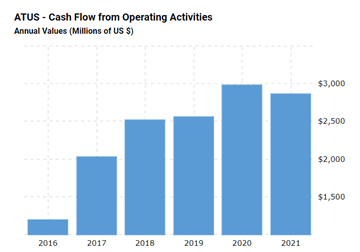

Cash flow from operation (macrotrends.net)

Although the net profit margins have been significantly volatile, cash flow from operations seems strong. Increasing CFO provides substantial stability to business operations.

As a result of consistent business expansion, debt levels have increased significantly to $24 billion. In contrast, it has just $2.5 billion in liquid assets and over $23 billion in intangible assets. I believe such a financial situation can bring substantial risk to the business model.

Since its IPO in 2017, the stock has lost over 86% of its value. After rising to approximately $38 per share in 2021, the share price has dropped to a low of $4.7 per share; due to such a huge drop, the company has become significantly undervalued. Even though the stock seems undervalued, various risk factors can affect the business, such as huge debt, rapidly changing industry dynamics, and rising competition.

Strength in the business model

The management is extensively focused on developing a fiber network; it can bear fruit in the upcoming years. After considering the sale of its Suddenlink business, the management decided to retain it and expand its operations. Note that the sale of the Suddenlink business was expected to bring over $20 billion, which shows that the company is significantly undervalued.

As the demand for data has been growing rapidly, the company has a significant addressable market to expand its reach. Being a high-speed data provider offers a significant edge to the business model.

Risk factors

Although the business has been producing ultrahigh profits from the last two years, various risk factors can drive down the stock price.

The company has over $23 billion in intangible assets. A significant part of these assets belongs to the news network segment; any deterioration in the business performance might cause substantial impairment charges, which can affect the business’s financial position. As consumer preference is shifting from T.V. cable to Streaming services, the revenue from the company’s network segment might be affected.

debt maturity (quarterly report )

Furthermore, over $5.1 billion of debt is going to mature in the next two years; due to its consistently dropping market cap, the company might face significant trouble refinancing the debt facilities. In such a case, the company might face the burden of high interest rates on its new facility, which can further affect business margins. Also, the company faces significant competition from Verizon Communications and Frontier Communications, which could affect the business model in the coming years.

Recent development

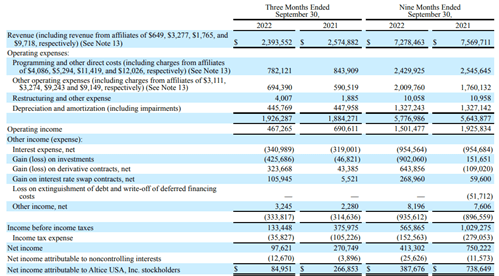

quarterly results (quarterly report )

In the recent quarter, revenue has dropped from $2.57 billion in the same quarter last year to about $2.39 billion now. Also, due to a loss in investment, the net profits have dropped to $84 million. The performance is primarily attributed to adverse economic conditions and rising competitive pressure. As the management focuses on improving customer experience, the company might effectively improve its results, but there seems to be significant uncertainty about future earnings due to the rising competition.

Currently, the company is trading for $2.1 billion, which gives it an earnings multiple of nearly five times its base on its last nine months’ earnings. The stock has been trading at a significantly lower valuation, but various risks can affect the business model. Therefore, I assign a sell rating.

Be the first to comment