Bo Shen/iStock via Getty Images

Investment Thesis Summary

We firmly believe there’s an alpha opportunity in buying Alkermes plc (NASDAQ:ALKS) shares at $27 for an initial return objective of 22%, searching for more upside beyond this point. Underpinning the investment thesis is the company’s recent announcement that it hopes to carve out its oncology business from its neuroscience division to create two standalone companies.

The oncology business has a robust engineered cytokines pipeline that has potential to create a long-term compounder with interesting economics tied into the mix, and so we understand management’s rational behind the decision. Moreover, its quarterly top-line growth has stagnated in recent times [see: Exhibit 5] and it share price has traded in a sideways consolidation since peaking in FY21′ [Exhibit 1]. Consequently, this move could free up capital resources and allow the company to redirect capital to unlock medium-term value for shareholders. Details of the spinoff are set to be released soon, and FY23′ is the year where it is set to take place.

We’ve seen this kind of activity en masse over in Australia on the ASX in the resources, energy and mining domains these past few years. This has occurred as the ASX’s large resources/energy/mining players look to separate their ‘fossil-fuel’ and renewables arms into two standalone entities, listing on the exchange in doing so. We envision a similar setup here with ALKS in its forward-looking plans. Net-net, we rate ALKS a buy, initial price objective $33.

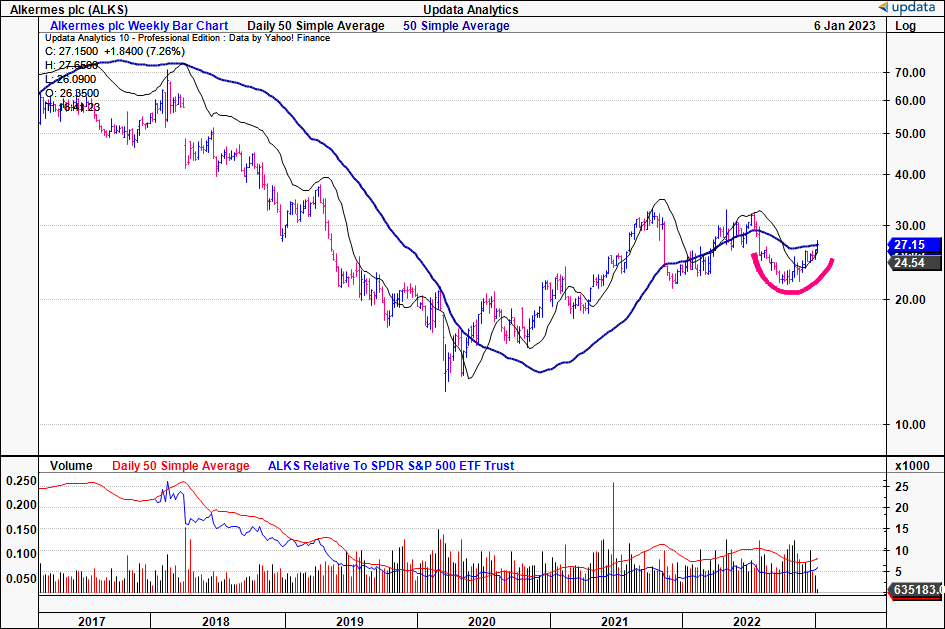

Exhibit 1. ALKS 5-year price action – shares are well below the longer-term ranges and need a catalyst to return to former glory.

Data: Updata

Breakdown of potential oncology business spinoff

In November, ALKS announced its plans to consider separating its commercial-stage neuroscience division from its development-stage oncology division. The company is exploring the possibility of creating a new, independent, publicly-traded company, tentatively named Oncology Co., as a strategic play to create corporate value for its oncology division.

The rationale behind the decision argues the spin-off would create a clear strategic focus for each business, establish separate and specialized management teams with niche therapeutic expertise, “simplify capital allocation decision-making and increase flexibility to pursue growth and investment strategies” that align with each respective end-market, and ultimately, drive long-term value creation for shareholders.

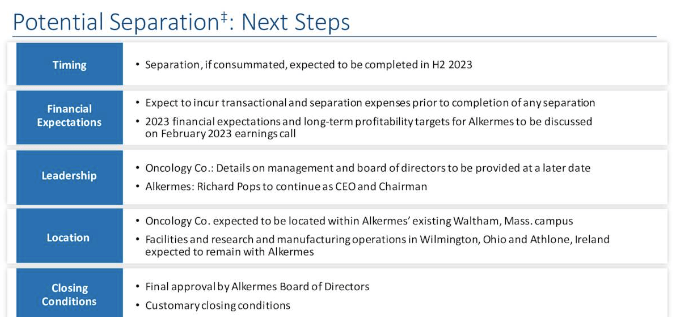

Exhibit 2. Journey for ALKS’ potential spinoff

Data: ALKS Q3 FY22′ Investor Presentation, pp.9

Investors can expect more information regarding the spinoff, including financials, within the early parts of FY23′. If completed, the separation is expected to be finalized in H2 FY23′, with Oncology Co. anticipated to be located within ALKS’ existing campus in Waltham, Massachusetts. The research and manufacturing operations in Wilmington, Ohio, and Athlone, Ireland, will remain with ALKS.

ALKS plans to continue prioritizing significant unmet needs within the realm of neuroscience and driving growth of its proprietary commercial products, such as Lybalvi, Aristada/Aristada Initio, and Vivitrol. In addition, the company intends to push ahead in progressing its pipeline assets addressing neurological disorders, including ALKS 2680, an orexin-2 receptor agonist intended for the treatment of narcolepsy.

Noteworthy is that ALKS expects to retain manufacturing and royalty revenues from its licensed products and 3rd-party products under its licensed proprietary technologies. Following the potential spinoff, it also anticipates increased profitability and sustained financial stability for its core enterprise. It’s also worth noting that Richard Pops will continue to serve as both CEO and Chairman of ALKS.

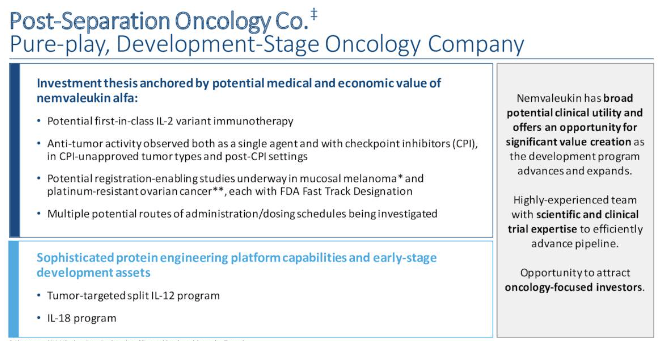

On the other hand, Oncology Co. is geared to be an oncology pure-play [Exhibit 3]. The development-stage oncology company will focus solely on researching and creating cancer therapies. This will include continuing the development of nemvaleukin alfa (“nemvaleukin”), a novel interleukin-2 (IL-2) variant immunotherapy that is currently being evaluated in the treatment of platinum-resistant ovarian cancer, and mucosal melanoma. Via it’s selective activation of the IL-2 pathway, nemvaleukin has the potential to be effective against a variety of tumour sub-types in our estimation, should safety and efficacy data hold up well. The pipeline assets that due to be carved out will likely be rolled into a single portfolio of pre-clinically engineered cytokines in our opinion, such as tumour-targeted split interleukin-12 (IL-12) and interleukin-18 (IL-18).

Exhibit 3. Oncology Co. descriptors

Data: ALKS Q3 FY22′ Investor Presentation, pp.8

Q3 earnings breakdown – benchmark for upcoming Q4, FY22′ numbers

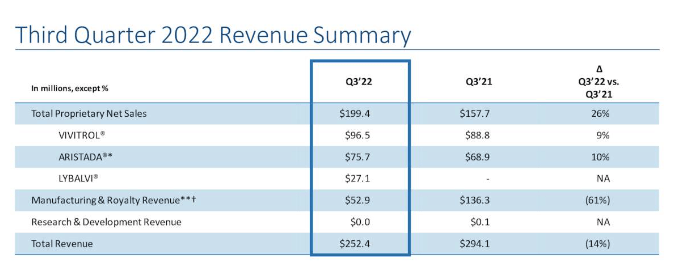

We saw the company booked turnover of $252.4mm in Q3, underlining the robustness in its proprietary commercial product offerings. With that, we made notes on each of the company’s segments. To list a few:

- Vivitrol contributed net sales of $96.5mm, reflecting a YoY increase of 9%. The third quarter saw gross-to-net adjustments of 51.2% for Vivitrol, consistent with the preceding quarter and with the company’s full-year guidance. ALKS has refined its projection for Vivitrol net sales for the current fiscal year to a range of $370mm-$380mm, and expects gross-to-net adjustments to remain at ~51% for the year.

- The Aristada product line saw net sales of $75.7mm, representing a YoY increase of 10%. The quarter’s gross-to-net adjustments for Aristada were 54.6%, also in-line with the preceding quarter. ALKS has revised its forecast for Aristada net sales for the current fiscal year to a range of $300mm-$310mm, and expects gross-to-net adjustments to remain at around 54%.

- We also saw that Lybalvi net sales increased 35% sequentially to $27.1mm, largely due to strong underlying demand growth of ~36%. Inventory levels increased in-line with demand, and lifted by approximately $2mm in the quarter, while gross-to-net adjustments remained unchanged at 26%.

Exhibit 4. ALKS Q3 revenue snapshot

Data: ALKS Q3 FY22′ Investor Presentation, pp.12

Shifting to the manufacturing and royalty division, the YoY decrease in turnover immediately stood out. Revenue in the segment pulled in to $52.9mm, a contrast to the $136.3mm recorded in the previous year. This downturn was primarily due to the termination of royalty payments by J&J for U.S. sales of Invega products. It should be noted that arbitration proceedings relating to this matter are still underway. It’s also worth mentioning that the company continues to receive royalty revenues from the ex-U.S. sales of long-acting Invega products.

It’s also worth mentioning that Vumerity royalties generated $26.3mm in turnover, and the company has made significant progress in addressing potential supply constraints, with plans to restart commercial production in the forthcoming weeks. Lastly, we feel it’s important to mention that Q3 results saw downsides of ~$21.5mm in royalty revenue following the conclusion of arbitration proceedings with Acorda Therapeutics, in relation to Ampyra.

Moving down the P&L, Q3 saw ALKS invest heavily in R&D, allocating a total of $100.4mm towards the nemvaleukin clinical program, and various early stage neuroscience and oncology initiatives. This included the preparation for the inaugural study of ALKS 268 involving human subjects. This amount represents a decrease from the $118.4mm designated for R&D in the same period of the prior year, which folded in the $25mm development milestone related to ALKS’ HDAC inhibitor platform.

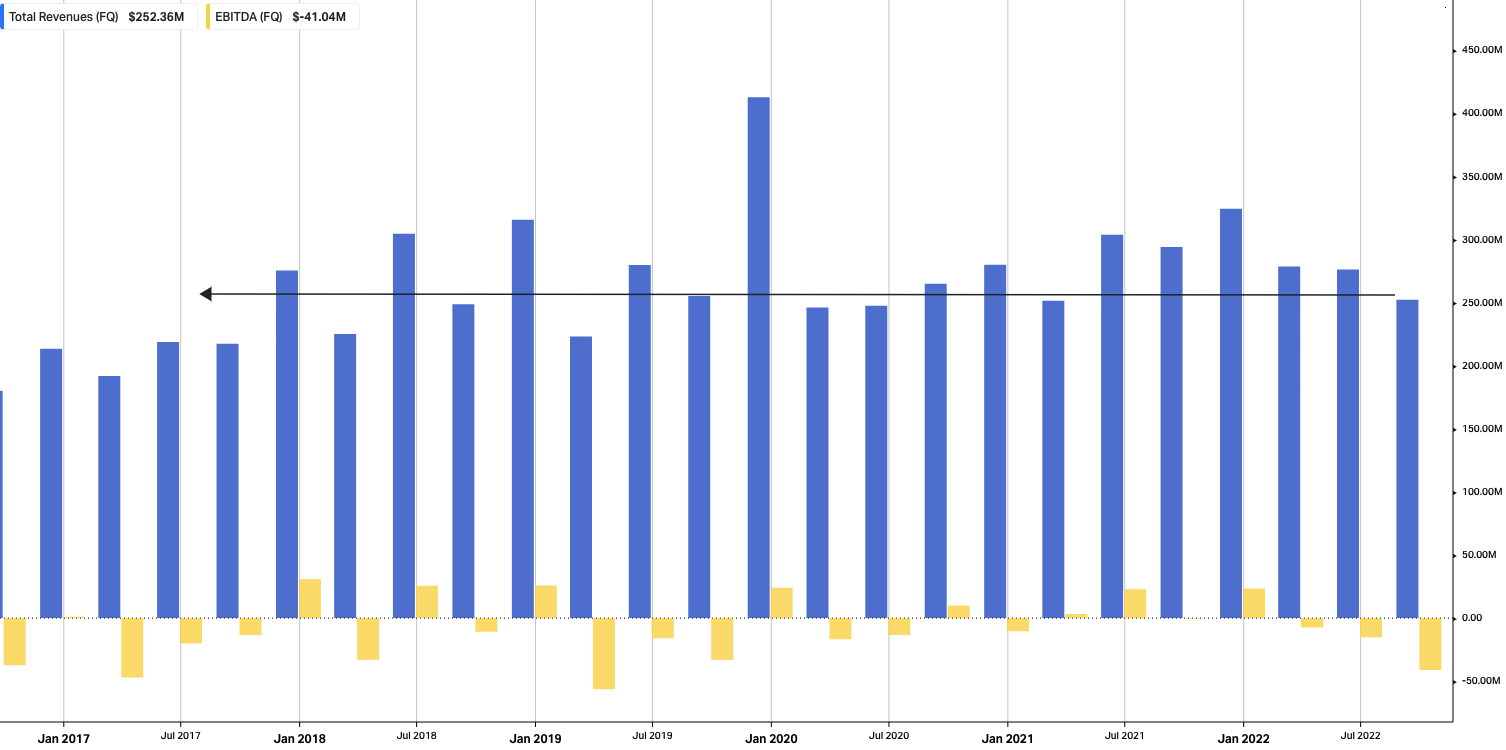

Exhibit 5. ALKS’ core revenue growth has stagnated in recent years, whilst core EBITDA is non-existent.

Data: HBI, Refinitiv Eikon, Koyfin

ALKS has revised its expectations for FY22′ total revenues for the fiscal year, now anticipating an increase in the range of $1.07 billion-$1.12 billion, a small increase at the midpoint of range. This change is largely due to improved projections for Lybalvi, as well as the updated assumption that the company will continue to receive royalty revenues from ex-U.S. sales of long-acting Invega products [as mentioned earlier] through the end of the year, and the previously mentioned reversal of Ampyra royalty revenue.

In terms of OpEx, management has raised its expectations for COGS by $5mm at the midpoint, underpinned by the higher projected revenue volumes. As the fiscal year approaches its conclusion, ALKS narrowed its predictions for R&D and SG&A expenses, both remaining within previously stated ranges. Noteworthy, the revised forecasts to the upside by ~$10mm at the midpoint for non-GAAP net income, now falling within the range of $25mm-$55mm [$0.33/share].

ALKS technical considerations for equity positioning

It is difficult to prescribe an accurate valuation for the two separate businesses in the planned spinoff without more details on the economics involved. Additionally, we feel there’s greater merit in looking at the market’s positioning in ALKS to guide price visibility looking ahead.

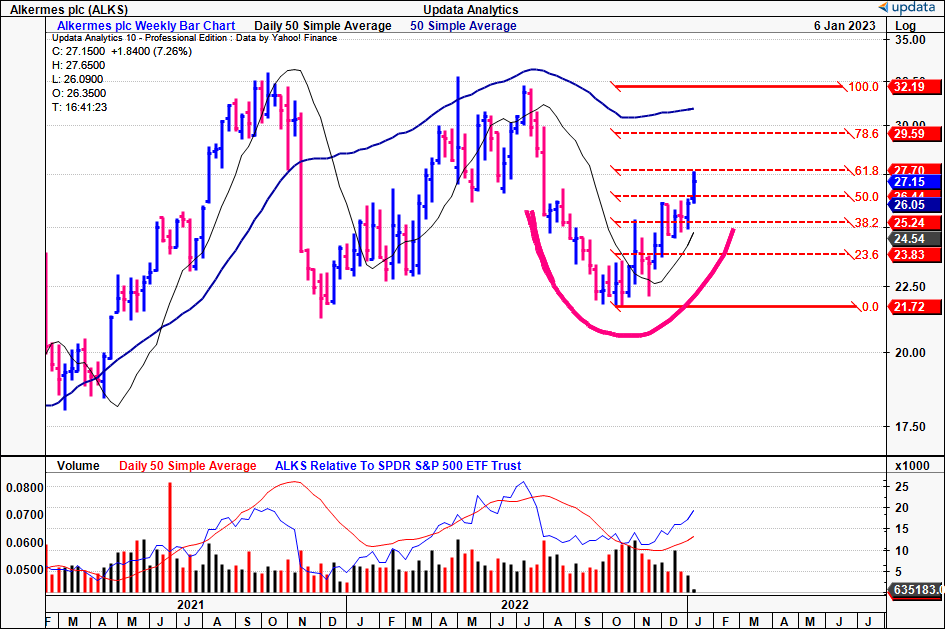

Looking at Exhibit 6, you can see the formation of a 23-week cup and handle that began its formation back in June FY22′. Since bouncing from its October lows, the stock has closed higher for the past 11-weeks to date, gathering further upsides post Q3 earnings. On this basis, there is grounds to suggest its Q4 numbers could provide an additional catalyst should they come in with an upside surprise.

Trading the fibs down from the previous highs to the October low demonstrates ALKS has already reclaimed ~62% of the entire down-leg. We are looking to $29.60 as the next key level at this trajectory, with $32.20 on the cards after that. Adding to this, weekly volume has begun to dry up, setting the stage for another breakout. Shares also trade above the 50DMA and are riding this as a line of support.

Exhibit 6. ALKS weekly price distribution and 62% retracement of Jun-Oct FY22′ lows

Data: Updata

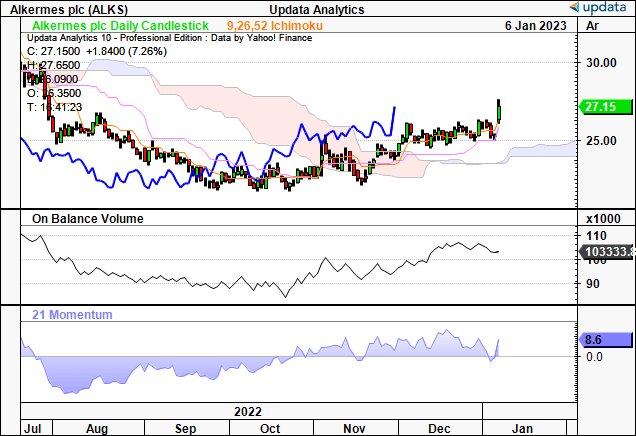

Adding further bullish weight to this, shares are firmly in bullish territory and are trading well above the top of the cloud shown in the Ichimoku chart below. The lagging line is also in hot pursuit, whilst the crossover of the cloud in December tells us there could be another spike to the upside coming.

Moreover, on-balance volume continues within its short-term rally after curling up from lows in October, right at the same point as the price reversal. Momentum indicators have also maintained an upward tilt as well.

Exhibit 7. Bullish confluence from cloud chart studies, with on-balance volume curling from lows in October.

Data: Updata

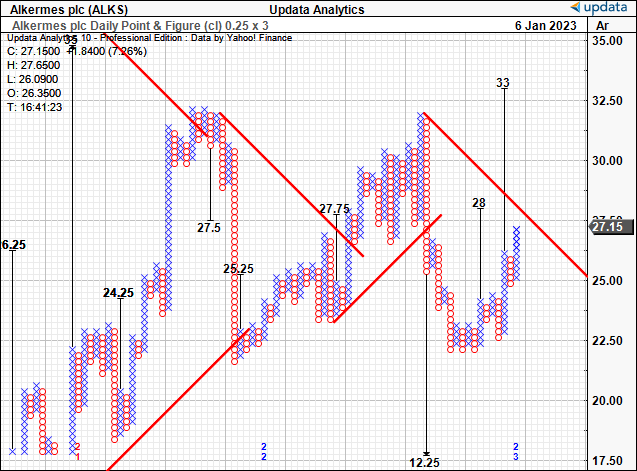

As another factor of confluence, we’ve got upside targets in the near-term to $33, in support of the numbers listed earlier. As an objective measure, this gives greater confidence on looking at $33 as the next price objective in this name. This would also mark a new high above the previous levels, and therefore warrants our buy thesis by estimation.

Exhibit 8. Upside targets to $33 which gives another factor of confluence to that level as an initial price objective.

Data: Updata

In short

ALKS’ decision to potentially carve out its oncology business from the neuroscience division provides an adequate springboard to bounce from in H1 FY23′ in our best estimation. There’s still some data to be revealed regarding the financial particulars of the transaction, and the newly formed entities, but we’re satisfied this could create another lock-step forward in generating shareholder value. As mentioned, we’ve seen plenty of this kind of activity in the resources, energy and mining space over in Australia on the ASX these past few years, as the large resources/energy/mining players there look to separate their fossil-fuel arms from their renewables arms to create two standalone entities. We envision a similar setup here with ALKS in its plans. Moreover, the market’s already taken notice, and is pricing in further upside downstream in our opinion. Net-net, we rate ALKS a buy and are searching for an initial price objective of $33.

Be the first to comment