Jeff Swensen

Introduction

It has been some time since my last article on Alcoa Corporation (NYSE:AA). The company has faced challenges since last year, evidenced by a 30% decline in the stock price over the past 12 months due to a combination of weak demand, declining pricing, and rising input costs.

However, my previous outlook on Alcoa remained optimistic, based on the belief that demand would recover as the Federal Reserve’s stance on inflation softened, while high energy prices would support a favorable supply growth environment. Since then, the stock has seen an increase of 12%.

In this article, I aim to provide a comprehensive update on my bullish stance toward Alcoa. Despite the mixed results reflected in the 4Q22 earnings report, with high inflation and slow demand, I believe the company is well-positioned for future growth. Now, let’s delve deeper into the current state of Alcoa and its prospects.

4Q22 – The Tricky Supply/Demand Picture

Managing high input costs and volatile demand

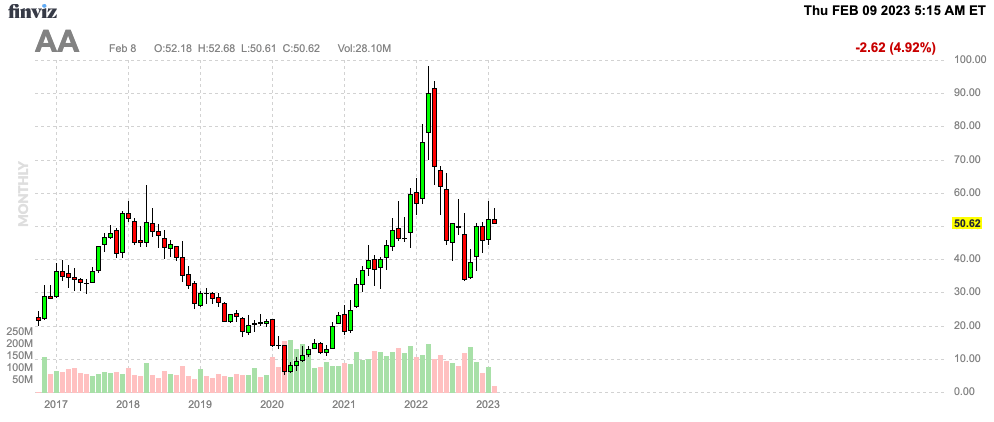

Since the company split in 2016, Alcoa hasn’t been a great source of shareholder wealth. The company has moved sideways with several steep drawdowns and rallies.

FINVIZ

The good thing is that this is what is expected. After all, Alcoa is a highly cyclical producer of alumina and aluminum. I would even make the case that the company’s cyclical stock price is terrific news for traders. After all, for investors who want steadily rising income and a business model that lets them sleep well at night, there are plenty of good alternatives.

I’m bringing this up as Alcoa is once again finding itself in a situation that could either lead to high returns or losses, depending on which of the two outcomes below turns out to be correct:

- High input costs remain an issue while slowing economic growth pressured demand. This is highly bearish for Alcoa.

- Demand improves, but input costs remain high enough to pressure global supply growth. This is very bullish for Alcoa, as it supports higher pricing power and demand growth.

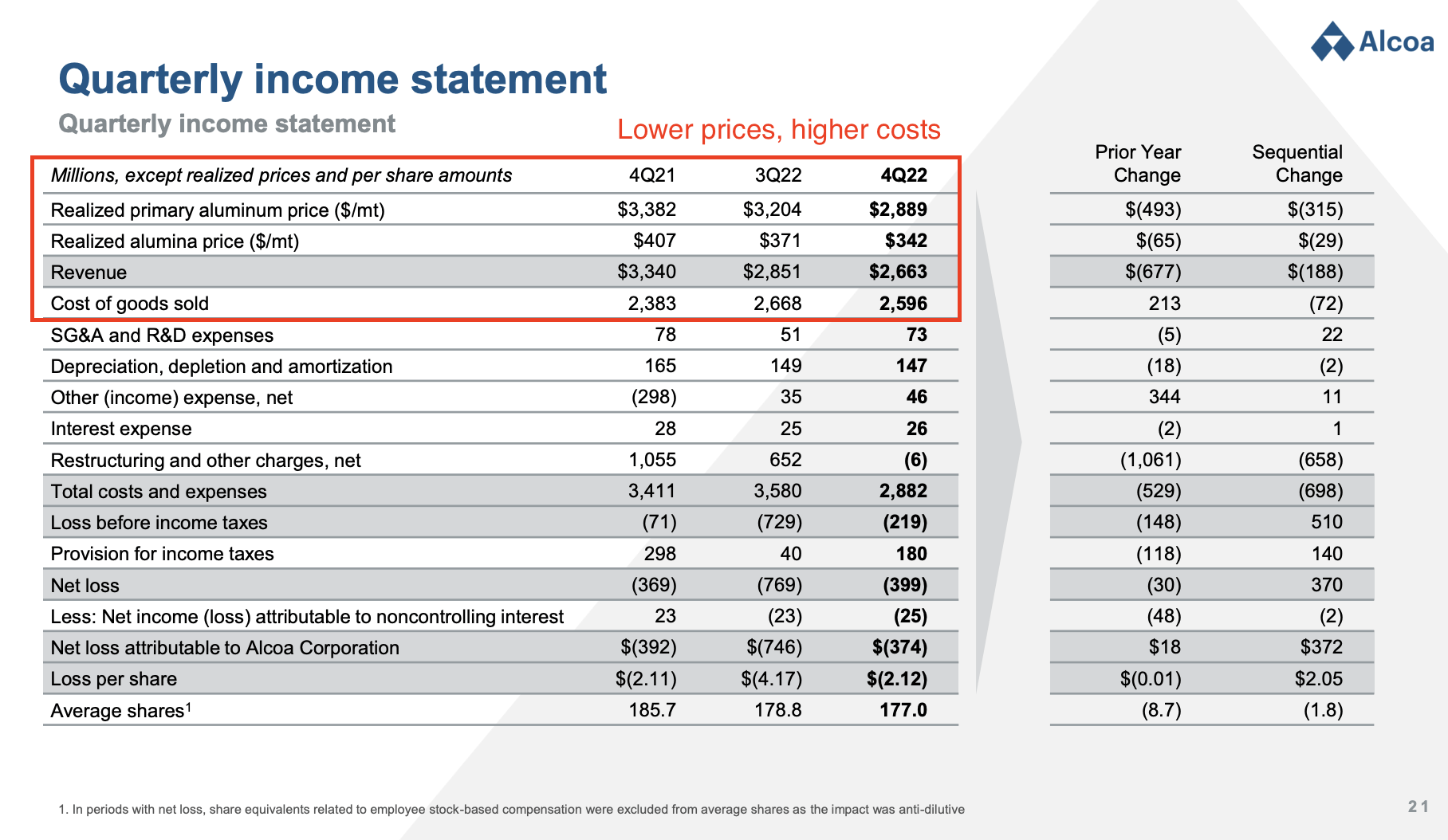

With that said, in 4Q22, Alcoa reported a 20.2% decline in revenue to $2.7 billion, which caused adjusted EPS of -$0.70 to fall into negative territory.

The problem was straightforward. The company saw a revenue decline to $2.7 billion as a result of lower realized aluminum and alumina prices. The realized alumina price fell from $407 to $342 per ton. The realized aluminum price dropped from $3,382 to $2,889 per ton. These are year-on-year numbers. Meanwhile, the cost of goods sold rose from $2.4 billion to $2.6 billion, causing an operating loss after incorporating SG&A and depreciation.

Alcoa Corp. (Author Annotations)

On a side note, people who are new to Alcoa need to know that it produces bauxite and aluminum, which are key elements in the aluminum production chain. It uses 92% of the bauxite it mines for its alumina production. 30% of its alumina goes towards its aluminum production. 100% of its aluminum is sold to outside customers. After all, after the 2016 spin-off, it does not have a business that further adds value to aluminum, which is fine, as we’re now dealing with a pure-play stock.

Alcoa Corp.

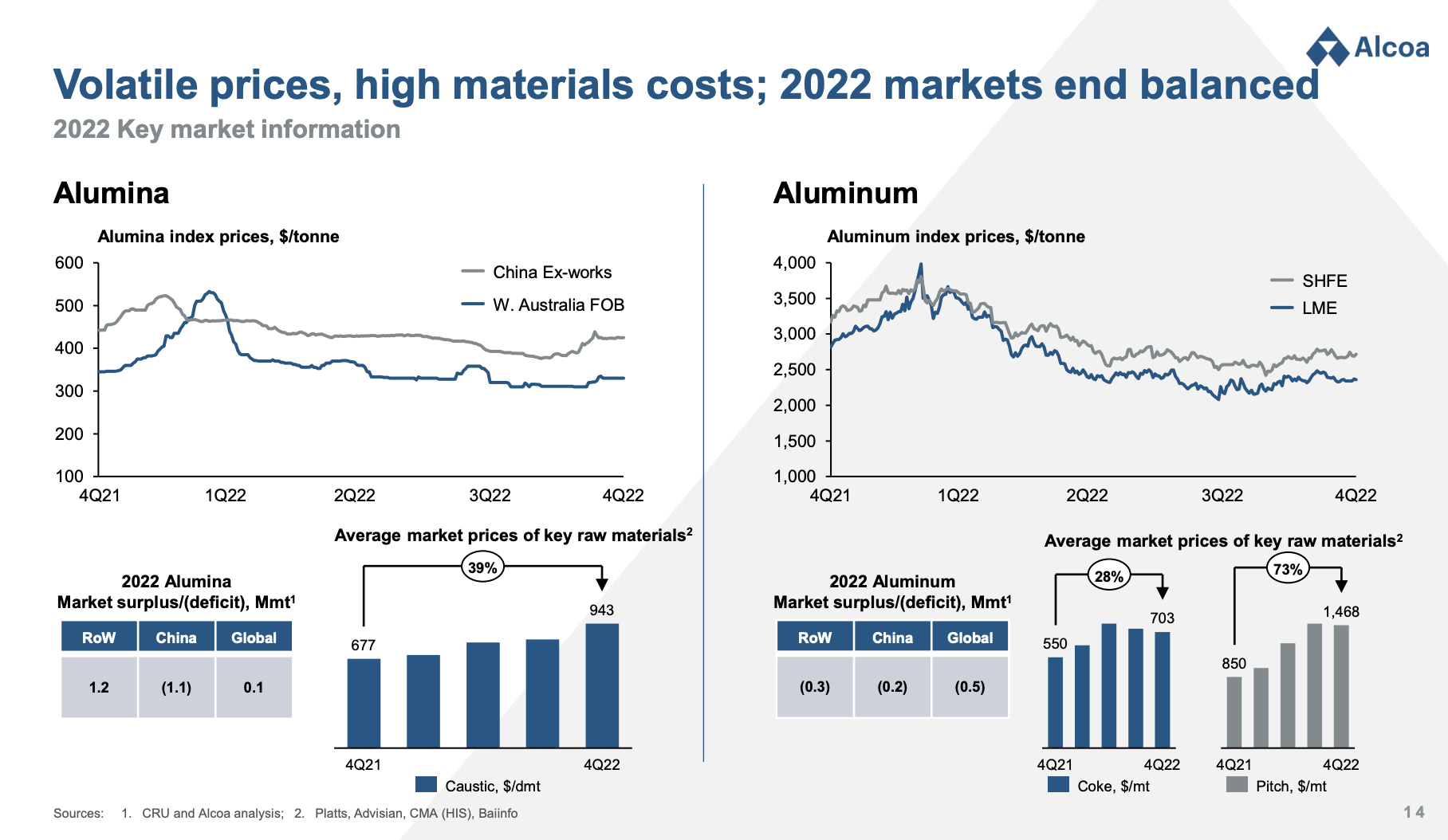

Alcoa has taken measures to mitigate the increasing costs of gas and electricity by reducing output at the San Ciprián alumina refinery in Spain and curtailing one-third of production at its Lista aluminum smelter in Norway. The company has also recently adjusted production at its smallest refinery in Western Australia due to ongoing natural gas shortages in the region. Despite these challenges, Alcoa has a strong foundation built on the knowledge and expertise needed to drive continuous improvement. The company remains focused on its future, where aluminum is expected to play an even more important role in the effort to decarbonize the world.

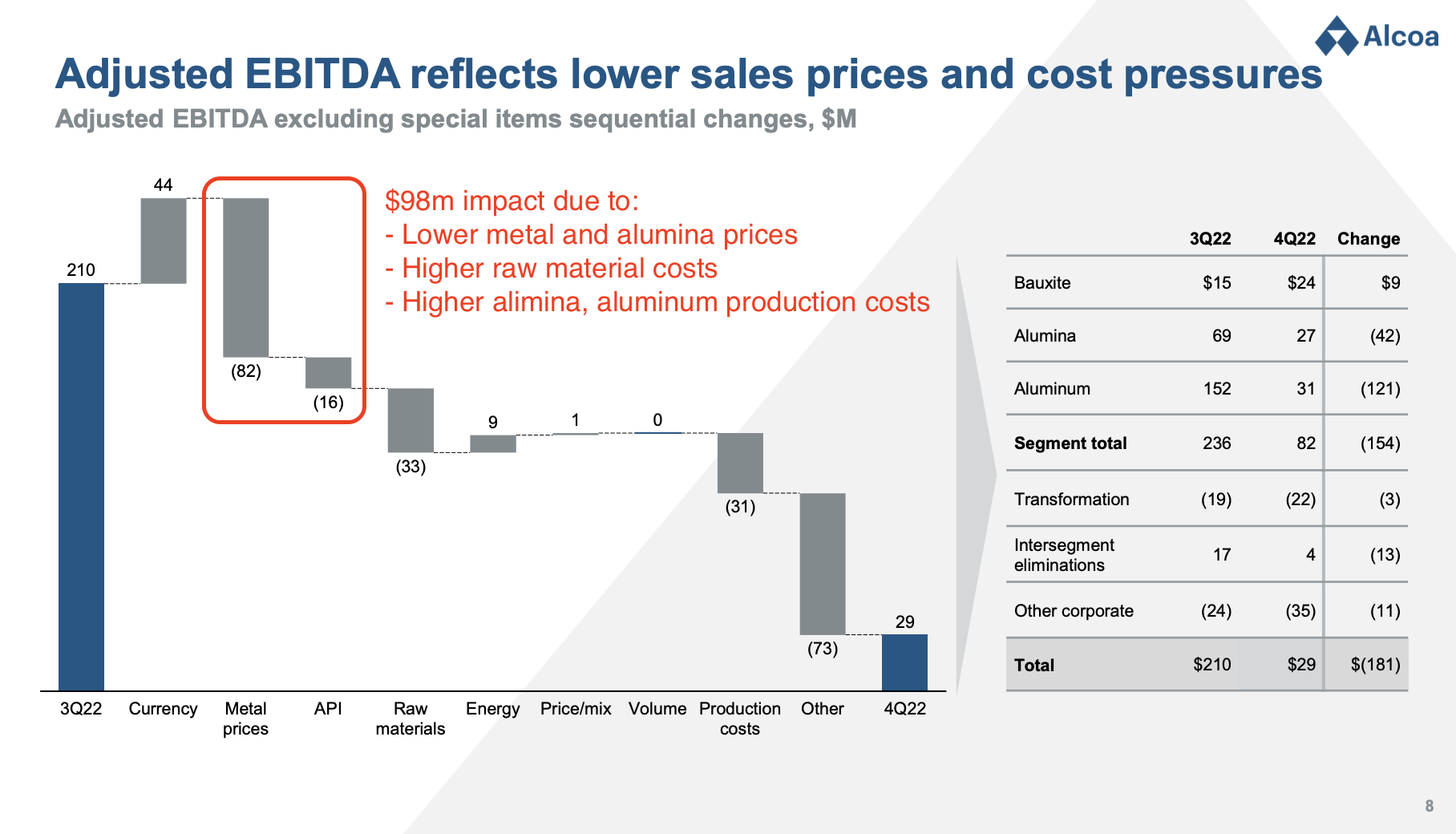

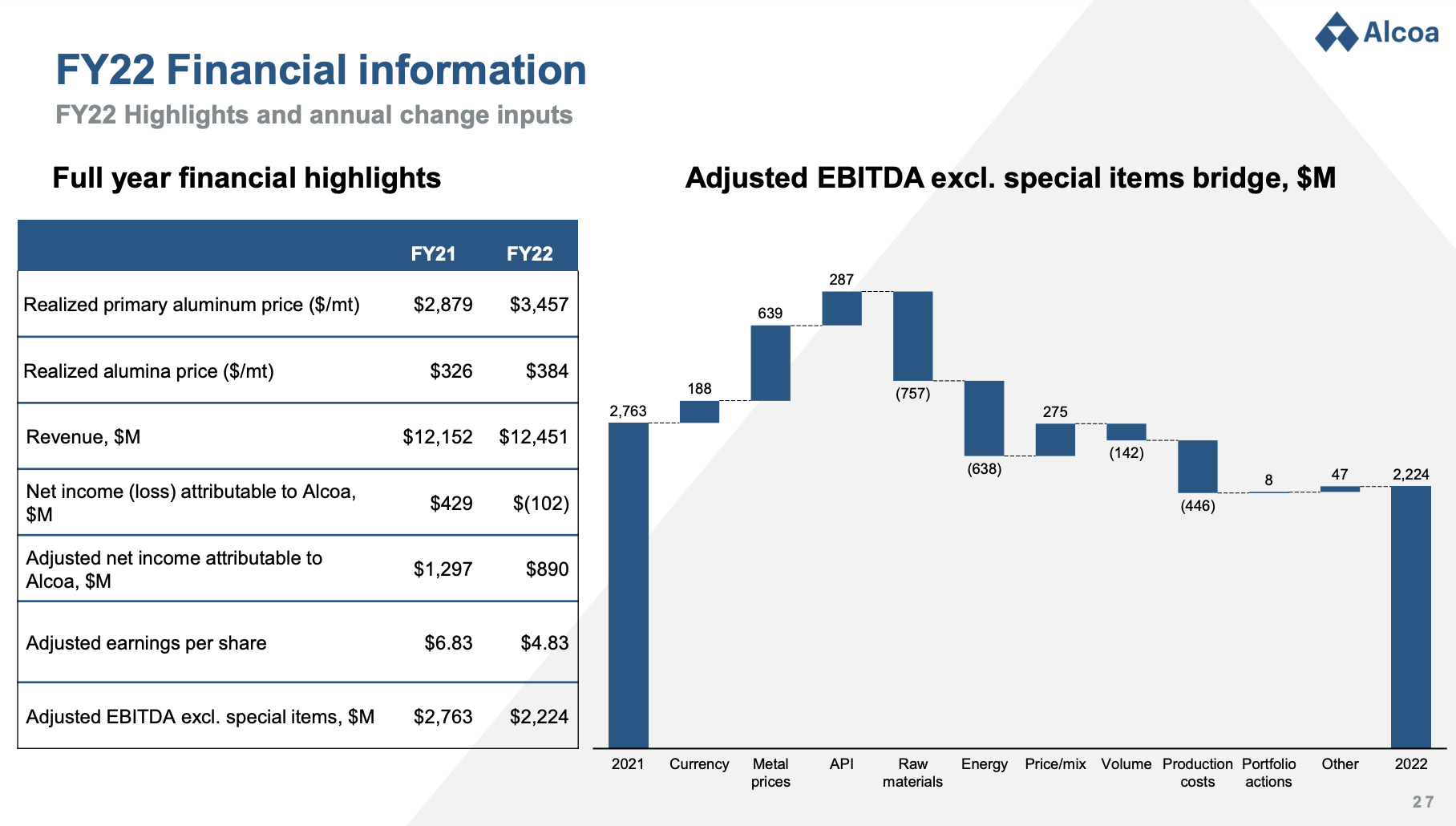

To put a number on it, the company mentioned $98 million in lower metal and alumina prices, including higher raw material costs and higher production costs in alumina and aluminum. This was the biggest driver of the quarter-on-quarter decline in EBITDA. I added this comment to the chart below to better visualize the impact.

Alcoa Corp. (Author Annotations)

Note that on a full-year basis, higher raw material and energy costs also more than offset gains from metal and alumina prices, as the overview below shows.

Alcoa Corp.

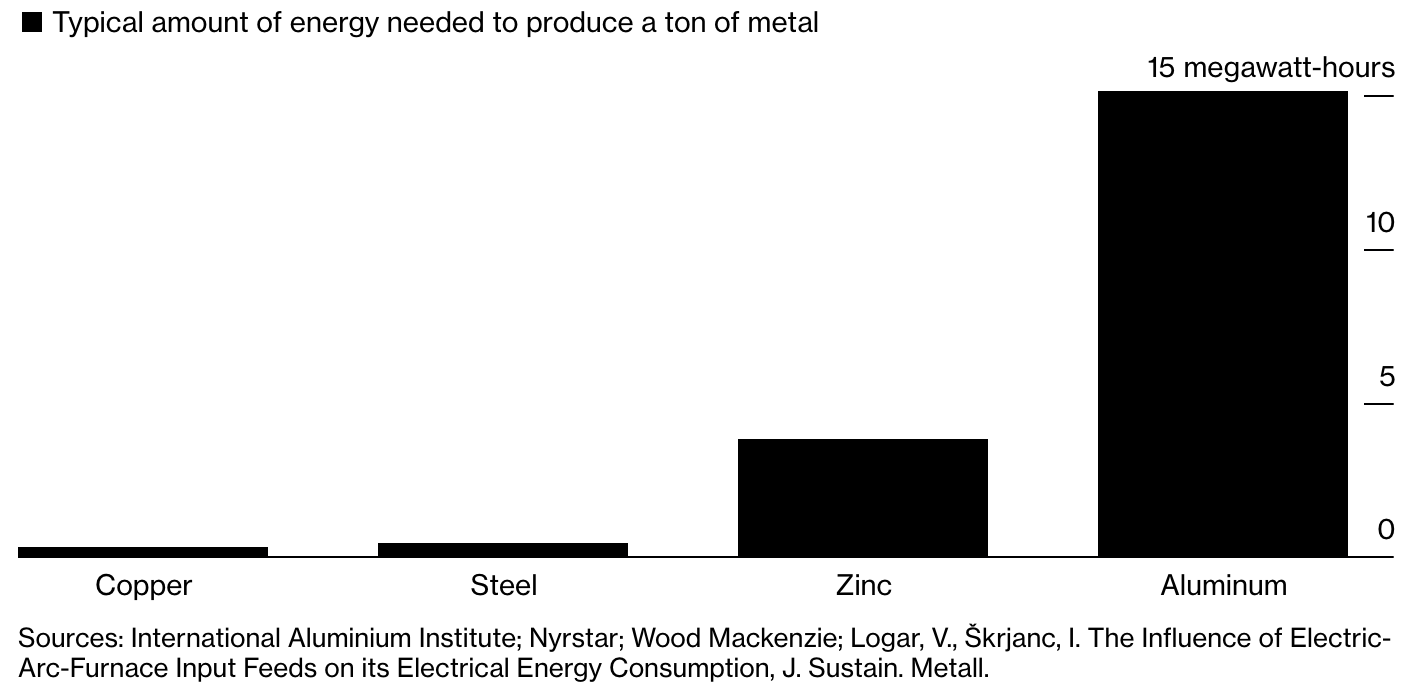

Bear in mind that 24% of aluminum smelting costs are power costs. The aluminum production process is the most energy-intensive among major metals like zinc, steel, and copper.

Bloomberg

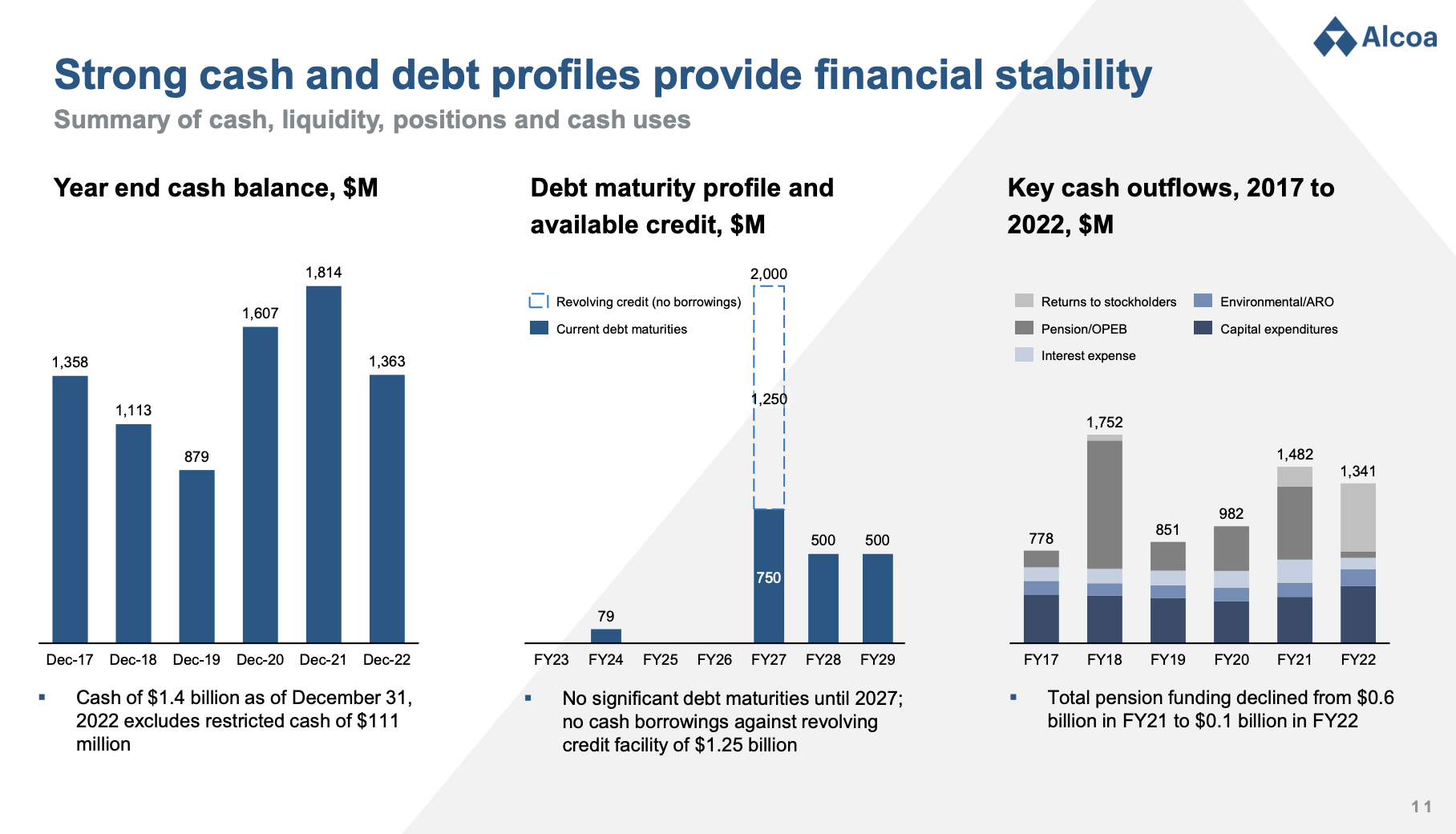

The good news is that the company improved its balance sheet in 2022.

At the end of 2022, Alcoa had a substantial cash balance of $1.4 billion, which is in line with the average level seen over the past five years. The company has redeemed its higher-rate debt with maturities in 2024 and 2026, resulting in a lower debt rate and inconsequential maturities until 2027, which buys the company a lot of time in the current environment of higher interest rates.

Additionally, the terms of its revolving credit facility have been improved, and it has been extended until 2027 with no outstanding borrowings. Alcoa’s pension and OPEB cash needs were low in 2022 and are expected to remain low in 2023 and beyond, with most of these costs now being OPEB, which is a pay-as-you-go system.

Alcoa Corp.

With that said, there’s more good news, especially with regard to the company’s outlook.

So, What’s Next?

In 2023, Alcoa is expected to maintain steady aluminum shipments of 2.5 to 2.6 million metric tons. In 2022, it shipped 2.6 Mmt. Alumina shipments are expected to come in between 12.7 and 12.9 Mmt, down from 13.1 Mmt in 2022.

Alcoa, which will put its bauxite and alumina segments under one roof in 2023, sees lower refinery production driven by the aforementioned partial curtailments in Spain and Australia.

With that said, Alcoa is very positive when it comes to future supply and demand dynamics.

Here are some of my bullet points from the company’s industry outlook:

- Alcoa remains bullish on the long-term fundamentals for aluminum despite the challenges faced in 2022.

- The transportation and packaging sectors are experiencing significant growth in demand for aluminum, driven by the growth of electric and hybrid vehicles and increased use of aluminum cans.

- China’s 45 million metric ton cap on aluminum production and recent actions to limit exports of primary aluminum are expected to support continued demand for aluminum.

- Inventories of aluminum are expected to remain near historically low levels in 2023, adding support to both the short and long-term outlook for aluminum.

- Alcoa continues to expect a balanced market for aluminum in 2023 and favorable underlying fundamentals for the metal in the long term.

The share of electric vehicles and hybrids is expected to rise by 7x by 2023 compared to 2016. EVs contain 40% more aluminum than conventional cars. China alone produced close to seven million EVs in 2022, with an outlook of nine million units in 2023.

ESG initiatives are also visible in other demand areas. Between 2016 and 2023, aluminum can demand is expected to rise by 41%.

Last month, Goldman Sachs (GS) came out, making a case for higher Chinese and European demand.

The metal will probably average $3,125 a ton this year in London, analysts including Nicholas Snowdon and Aditi Rai said in a note to clients. That’s up from the current price of $2,595 and compares with the bank’s previous forecast of $2,563.

Goldman sees the metal used to make everything from beer cans to plane parts climbing to $3,750 a ton in the next 12 months.

“With visible global inventories standing at just 1.4 million tons, down 900,000 tons from a year ago and now the lowest since 2002, the return of an aggregate deficit will quickly trigger scarcity concerns,” the analysts said. “Set against a far more benign macro environment, with fading dollar headwinds and a slowing Fed hiking cycle, we expect upside price momentum to build progressively into spring.”

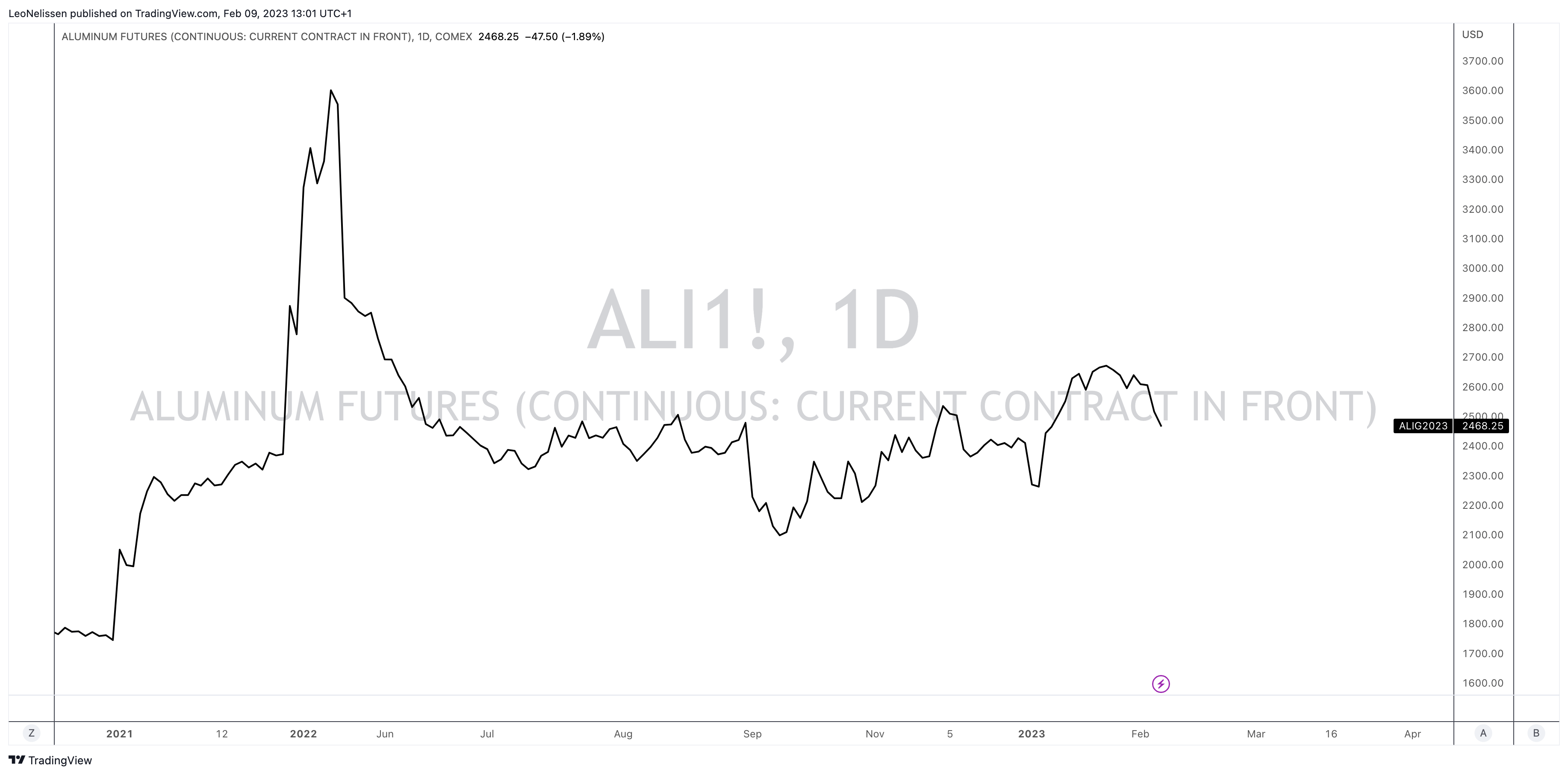

These factors have put a floor under aluminum prices. Using COMEX aluminum, we see that prices are consistently above $2,300 per ton. While this is well below the levels experienced after the Ukraine invasion last year, it is well-above pre-pandemic levels of roughly $1,500 per ton.

TradingView (COMEX Aluminum)

Speaking of Russia and supply, the supply side could become even tighter as a result of 200% tariffs on Russian aluminum exports.

According to Bloomberg:

Russia, the world’s largest aluminum producer after China, has been a significant source of material for the US market. Most of it is value-added items rather than in bulk product, with US buyers ranging from building and construction to automotive.

Such a steep tariff would effectively end US imports of the metal from Russia. While the country has traditionally accounted for 10% of total US aluminum imports, the amount has dropped to just more than 3%, according to US trade data.

Concerning demand, the company sees high demand in the US, yet more uncertainty in Europe, which struggles more with high inflation than the US.

We are still seeing a lot of strength in the U.S. market, particularly. And so when we look across the different product categories, and I would highlight transportation and packaging is the two places where we are just seeing – we continue to see more demand than probably we are able to fulfill. So, the U.S. market is still running very well. In Europe, I think there is a lot more uncertainty.

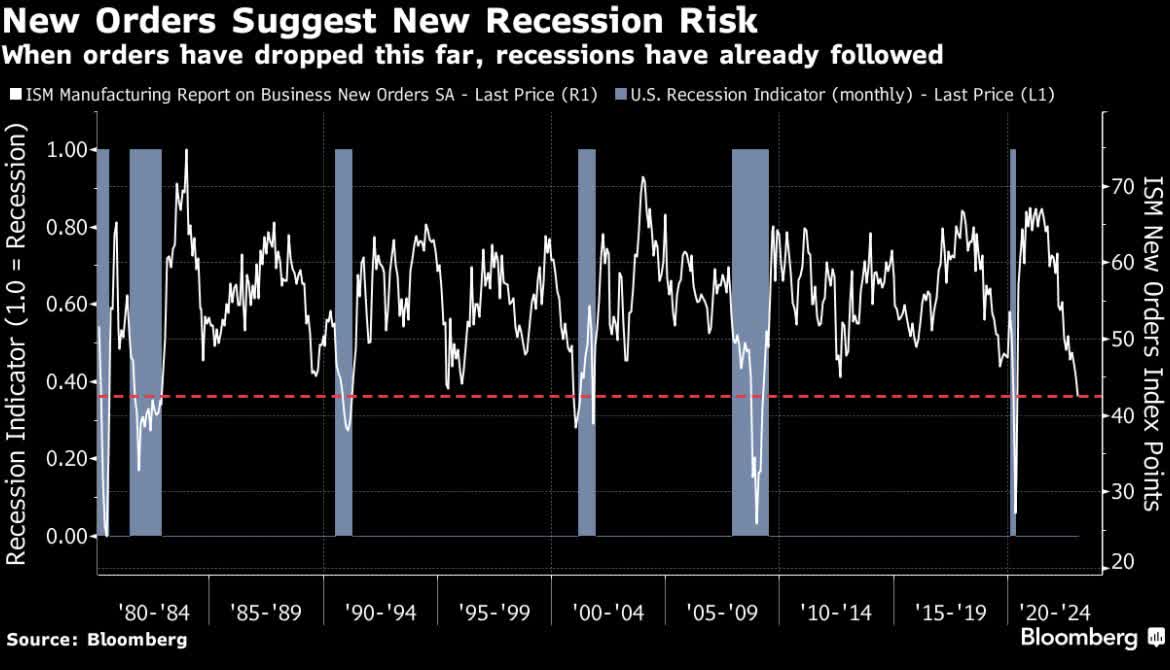

This is interesting as US manufacturing sentiment (like ISM new orders) has indicated high recession probabilities going into this year. The yield curve has indicated this since 4Q22.

Bloomberg

Therefore, it is my belief that Alcoa’s stock price will remain steady until the demand reaches its minimum point. At that point, a reduced supply and favorable pricing are expected to contribute to a substantial increase in the value of the stock. If conditions align, I anticipate that Alcoa’s shares will surpass the $90 mark.

For now, I believe that the company is fairly valued.

If a market correction were to provide us with a decline to $40, I would be a buyer.

Takeaway

Alcoa is facing challenges from elevated input costs and a slowing economy, which are impacting demand for its products. However, the company remains optimistic about future market dynamics, having strengthened its financial position in 2022 with a solid cash balance and minimal pension and OPEB obligations. Moving forward, Alcoa anticipates steady aluminum shipments and lower alumina shipments in 2023, with decreased refinery production in Spain and Australia. The company also has a positive outlook on the role of aluminum in the global effort towards decarbonization.

Given the timing uncertainties, it is recommended to closely monitor Alcoa as potential buying opportunities may arise in the event of a bottom in demand. The company’s shares have the potential to soar in this scenario, with expectations of subdued supply and elevated pricing benefits.

(Dis)agree? Let me know in the comments!

Be the first to comment