Kosal Hor/iStock via Getty Images

The shares of Alcoa (NYSE:AA) are off by around 46% from its highest level seen in March, as declining macro indicators left a drag on the aluminum prices rally. However, not only do the strong growth drivers of aluminum demand remain intact, but they are becoming more prominent. I believe Alcoa, as a leading bauxite, alumina and aluminum producer, will benefit from secular tailwinds in the automotive, aerospace and packaging markets to drive future growth from its strong upstream production portfolio.

Moreover, the additional driver for the aluminum demand will be the easing of coronavirus restrictions and the move away from the zero-Covid policy in China. While potential sanctions against Russian aluminum imports could have an adverse impact on Europe’s industry and lead to a volatility in the metal’s price, overseas Alcoa would capitalize on the higher aluminum prices and will improve its profitability. From thus far I will try to elaborate my Strong Buy call on AA by examining its financial results, demand growth drivers, RUSAL’s headwinds and valuation.

Aluminum price and secular demand drivers

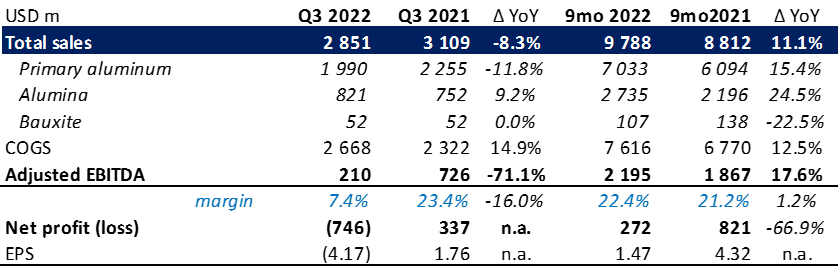

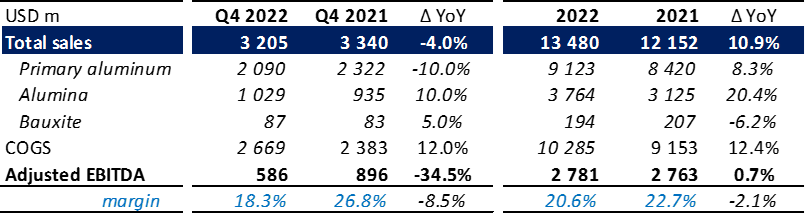

Following the strong sequential two quarters since the beginning of the year, third quarter results were not that positive. In the second half of the year aluminum prices declined from March peak levels and are consolidating around $2 300/mt. This was the main factor behind the decrease of Alcoa’s Adjusted EBITDA to $210 million in Q3, from $913 million in the previous quarter .

Q3 financial results (company reports)

Total revenue was down 6.8% YoY due to lower primary aluminum sales ($1.99 billion; -11.8% YoY) as a result of a 14% YoY decline in third-party shipment to 621k mt, and despite higher average selling price/mt of $3 204 (+2.56% YoY; -17.1% QoQ). Alumina sales ($821 million; +9.2% YoY), however, partially limited the top-line decline due to higher realized price during the quarter (+18.9% YoY), while on 7.5% YoY lower shipments. Below the EBITDA line, net loss attributable to Alcoa amounted to $746 million, or $4.17 per share, due to the higher input costs and restructuring charges during the quarter.

Looking forward, the secular growth drivers for aluminum demand will provide plenty of opportunities to drive future growth and wipe out the negative quarterly results. The growing demand for aluminum will be primarily associated with lightweighting megatrend in the automotive industry in order to increase the fuel efficiency of ICE vehicles, and the range capability of BEVs as much as possible. In the aerospace industry, demand for aluminum alloys should remain strong due to the rapidly growing use of composite materials, supported by passenger traffic and build rates recovery. Overall, the green transition and emission reduction rush will provide for increased demand for aluminum as a result of its endless recyclability, energy saving and waste reduction peculiarity. The green trends could also lead to a reduction in production capacity using coal-fired electricity, which is still the main source of aluminum electrolysis, and force aluminum in short supply. This will exhibit an upward pressure on the metal’s price and underpin Alcoa’s profitability.

Energy crisis

The European manufacturing sector remains under pressure amid a slowdown in economic growth, record inflation, geopolitical tension, as well as rising operating costs. This has led to the closure of more than a million tons of aluminum production in Europe since 2021.

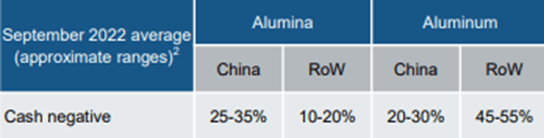

Profitability of aluminum production (Company presentation)

Alcoa calculations revealed that a significant portion (around 50%) of global producers of aluminum (without China) are experiencing negative profitability. However, the share of cash negative production in China is much lower, around 25%.

The energy crisis did not bypass Alcoa as well, which is evidenced by the following quote from Q3 report:

While the Company has overall limited exposure to spot energy costs, two of our operating locations in Europe, the Lista smelter in southern Norway and the San Ciprián refinery in Spain, experienced significant losses in the third quarter of 2022 primarily due to the volatility in the European energy market.

As a result, the company closed a portion of production at both operating facilities. However, despite production curtailments, the fact that such a big portion of production capacities world-wide are operating in red territory represents a good opportunity for Alcoa to extract more benefits from secular growth catalysts.

Sanctions against Russia? Not likely at this stage

A number of European industrial organizations called on the EU authorities not to impose sanctions against Russian aluminum, as this could endanger the European aluminum industry. RUSAL, which produces about 6% of the world’s aluminum, is not subject to Western sanctions, but the US is considering imposing restrictions on Russian aluminum imports. There are some options for restrictions: complete ban on imports; raising import tariffs or imposition of sanctions against RUSAL.

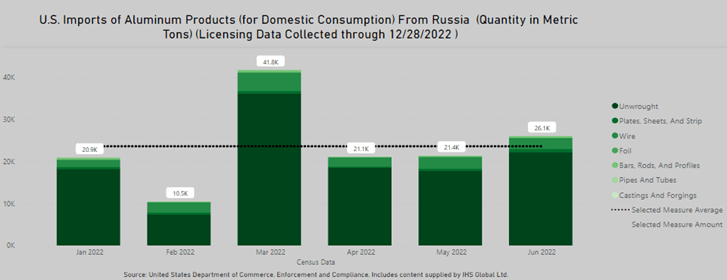

US import of aluminum from Russia (International Trade Administration)

For the 6mo 2022 period, aluminum imports to the US market from Russia amounted to 141.8k mt. This volume is 7.5% of the total aluminum production of RUSAL. With economic growth slowing down, this option to exclude volumes from the other markets will support domestic US producers. It is not surprising that Alcoa called to introduce a ban on the use of aluminum from Russia.

Back in 2018, after the US imposed sanctions on Rusal and the LME blocked its metal, aluminum prices jumped 35% in a matter of days. Thus, a complete ban on the supply of Russian aluminum by the US could lead to the metal prices skyrocketing back to $ 3 000/mt levels.

Undoubtedly, the US introduction of a ban on the supply of Russian aluminum will have a great impact on further development of the aluminum industry and would be a strong blow to the EU economy. However, Alcoa could benefit from this by increasing its own production, underpinned by eventual upside volatility of aluminum prices.

RUSAL has enough problems

By uniting all its Russian aluminum smelters, RUSAL actually represents almost the entire aluminum industry of the Russian Federation. Although the company’s products are not subject to sanctions thus far, it depends on the supply of alumina, as the Nikolaev alumina plant in Ukraine was stopped, and Australia banned the export of this raw material to Russia. However, the company seems to have managed to solve the problem of supplying its plants with raw materials, as the production of primary aluminum in H1 2022 increased by 1.2% YoY and amounted to 1 891k mt. Apparently, RUSAL managed to arrange the supply of the missing volumes of raw material from China, although this led to an increase in the cost of primary aluminum production.

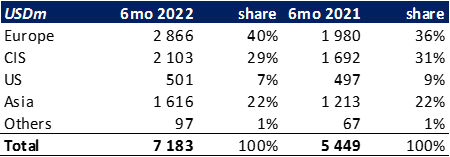

RUSAL H1 2022 revenue (company financial statements)

RUSAL’s revenue from exports to Europe in H1 grew by 44.7% YoY and the share of the European market in the revenue mix for the period was 40% compared to 36% a year earlier. The growth comes against the backdrop of a reduction in aluminum production at European plants due to the high cost of electricity. Under these conditions, the introduction of restrictions on the import of Russian aluminum into the EU looks unlikely.

Valuation and expectations

I expect a 4% YoY decrease in Q4 sales, mainly due to the lower aluminum prices compared to the Sep-Dec period of last year, where Alcoa was selling its aluminum at an average price of above $3 300/mt. For the full 2022 year, I assume total sales to reach $13.5 billion and register 10.9% YoY growth. Despite elevated input costs, I believe EBITDA should come in at $2.8 billion, remaining in a green territory, with a margin of 20.6%.

Q4 and 2022 expectations (company reports; author’s estimates)

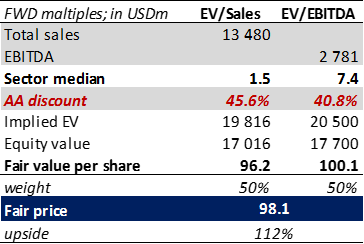

I valued Alcoa using a comparative method based on the above forecast for 2022. My valuation is determined by a weighted average of EV/Sales and EV/EBITDA forward trading multiples.

Valuation based on sector median multiples (seekingalpha data; author’s estimates)

AA is currently trading at EV/Sales and EV/EBITDA forward multiples of 0.8x and 4.4x, respectively, which represent a significant discount of more than 40% both to the sector’s median (derived from Seeking Alpha) multiples of 1.5x and 7.4x, respectively. Applying my financial estimates of 2022 Sales and EBITDA to the sector median multiples should yield an enterprise value of $20.2 billion. Net of interest-bearing liabilities and pension related obligations, the implied equity value should be $17.4 billion, which corresponds to $98 per share. The valuation implies significant upside potential of 112% from the current price and is in line with a Strong Buy rating.

Risk factors

Sky-high input prices are a major challenge for Alcoa, which could lead to further curtailments of production operations. Overall, stagnation in the automotive, aerospace and packaging industries due to ongoing recession fears could undermine demand for aluminum products and the company’s profitability at the same time.

Conclusion

The energy crisis in Europe keeps worsening, leaving the energy-intensive aluminum industry vulnerable, as elevated energy prices continue to halt production. The crisis did not bypass the company either, as Alcoa had to curtail part of its production capacity. However, Alcoa still commands a strong production portfolio, and could benefit from a significant share of unprofitable production around the world. If the US nevertheless decides to impose sanctions against Russian aluminum, nothing will prevent China from buying Russian aluminum at a big discount and reselling it to Europe and the US in order to close the deficit in the market. But that’s another matter for discussion. The point is that the secular tailwinds for aluminum products are, and will be intact, stipulating the company’s future growth. Despite considerable risks, I deem investment in AA stock represents an attractive opportunity.

Be the first to comment