Olemedia

Trying To Keep Up With Demand

The lithium market experienced a stagnant phase in the late 2010s and into 2020 as producers like Albemarle (NYSE:ALB) began to build capacity to meet demand from EVs that had not yet materialized. This led to several years of lithium carbonate prices hovering around their marginal cost of production, resulting in negative free cash flow for Albemarle. As I wrote in 2019, the company even idled its Wodgina spodumene mine and slowed down plans to add conversion capacity at Kemerton (Both sites are in Australia.)

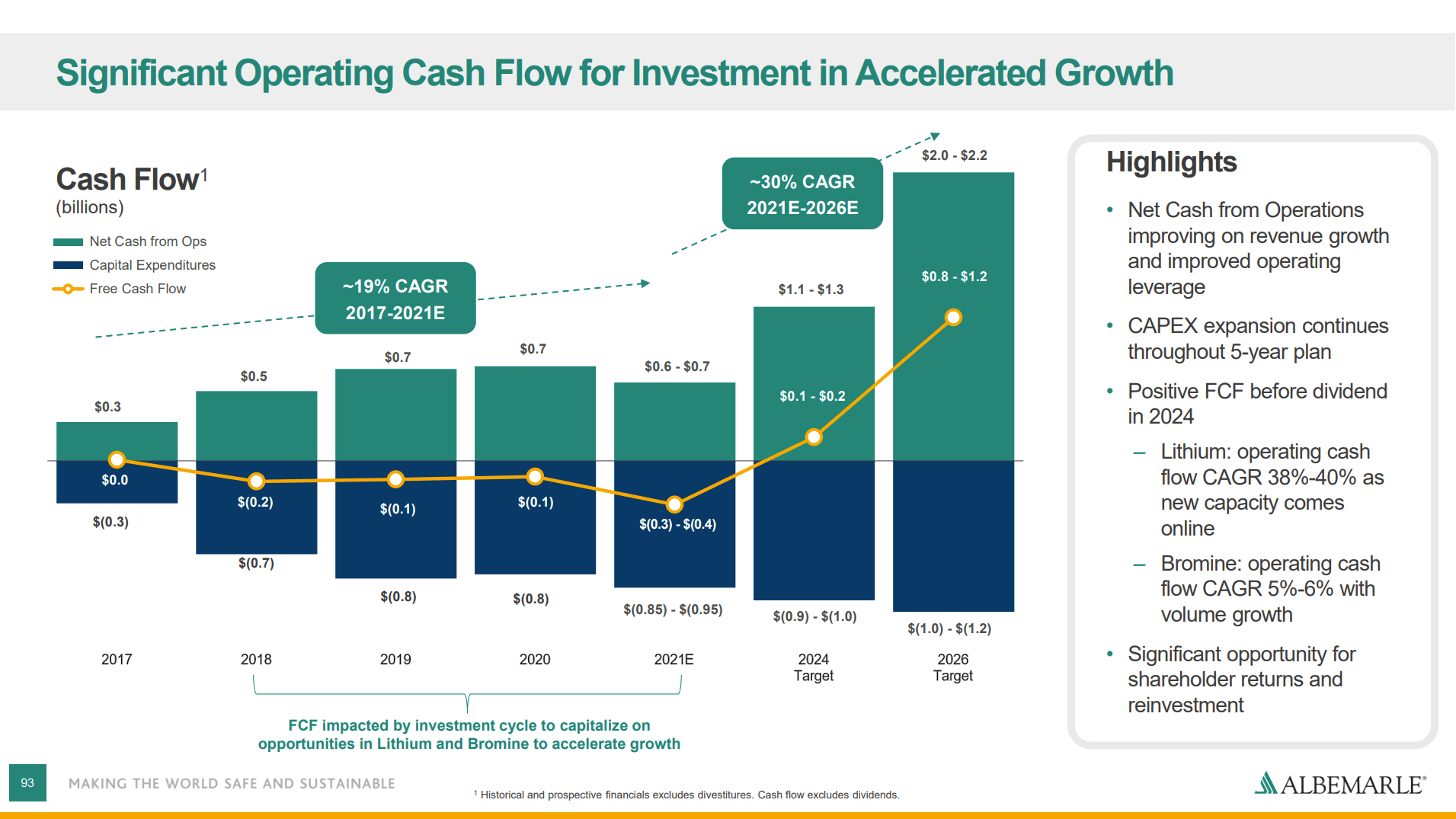

Albemarle September 2021 Investor Presentation

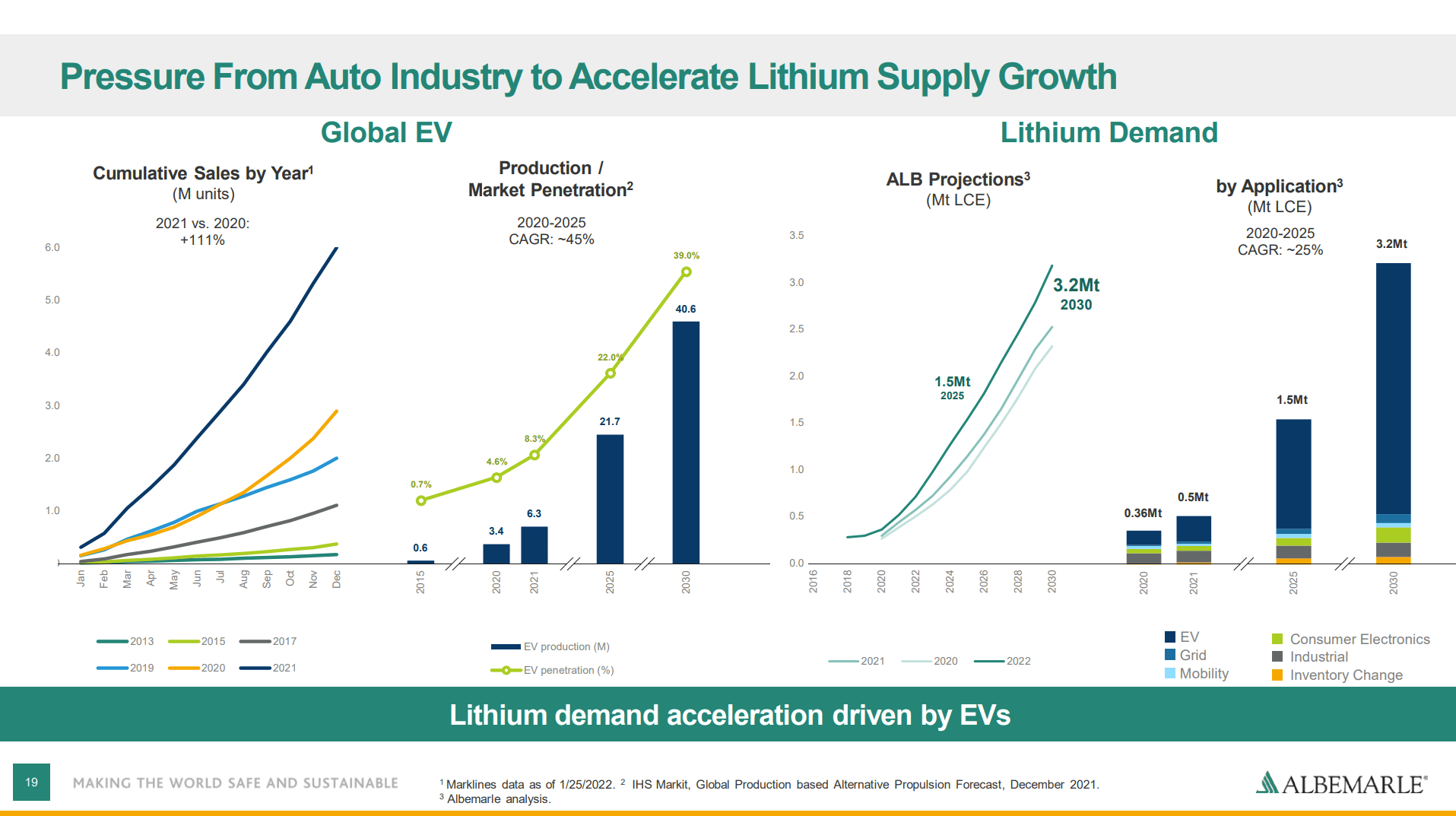

The demand inflection point came in 2021, as EV sales came in at double 2020 levels. Looking forward, worldwide lithium demand is now expected to increase from 0.5 million tons lithium carbonate equivalent to 1.5 million in 2025 and 3.2 million in 2030.

Albemarle May 2022 Investor Presentation

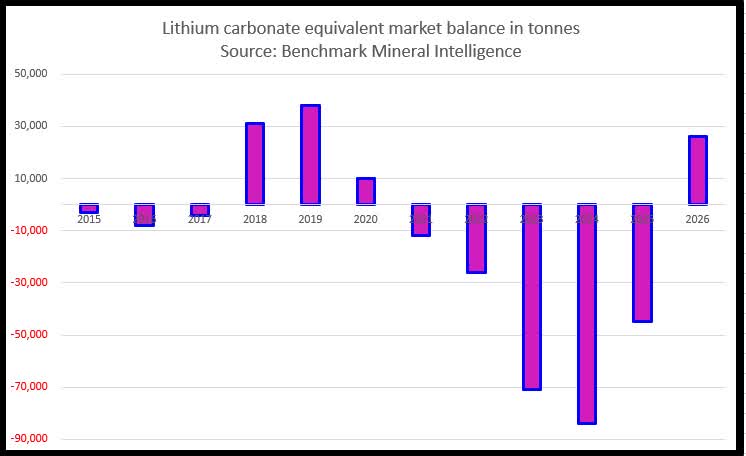

The market went from oversupplied in the late 2010s to undersupplied for at least the next several years. Lithium carbonate and hydroxide conversion plants take a couple of years to construct. This is followed by several months of startup until on-spec product is produced, followed by several more months of qualification for the product to be accepted by customers. Albemarle and others are now bringing on facilities as fast as they can to meet demand, but it will be a slow process. I suggest following Trend Investing here on Seeking Alpha for monthly lithium updates.

BMI

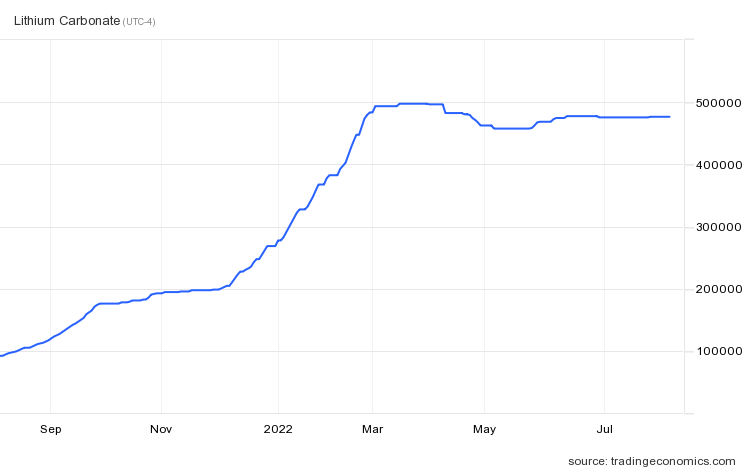

Albemarle has now started its Wodgina mine and has produced first product from the Kemerton I upgrader, with construction of Kemerton II almost complete. However, since product has barely started to hit the market, the supply/demand imbalance is reflected in the huge price increase this year for lithium carbonate. (476,500 CNY = ~$71,000)

Trading Economics

With prices at this level, Albemarle now expects to be free cash flow positive this year, 2 years earlier than the 2024 target on the first chart above. Looking forward, the market looks to be balanced to oversupplied again by 2026. Longer-term forecasts show a supply shortage returning soon after that and widening every year, but I do not place much confidence in them as markets have a way of adjusting in that time frame. More supply will be added beyond currently announced plans or substitutes for lithium may be developed. Nevertheless, the shortage over the next few years will be a cash generating opportunity for Albemarle, the magnitude of which depends on pricing. Conservatively, the company should be able to not only produce $1 billion per year of free cash flow in 2026 as shown on the first slide above but can deliver that in 2023. Using more recent optimistic forecast, Albemarle can generate $3-$4 billion of FCF. The company looks fairly valued in the conservative case and cheap in the higher-price case.

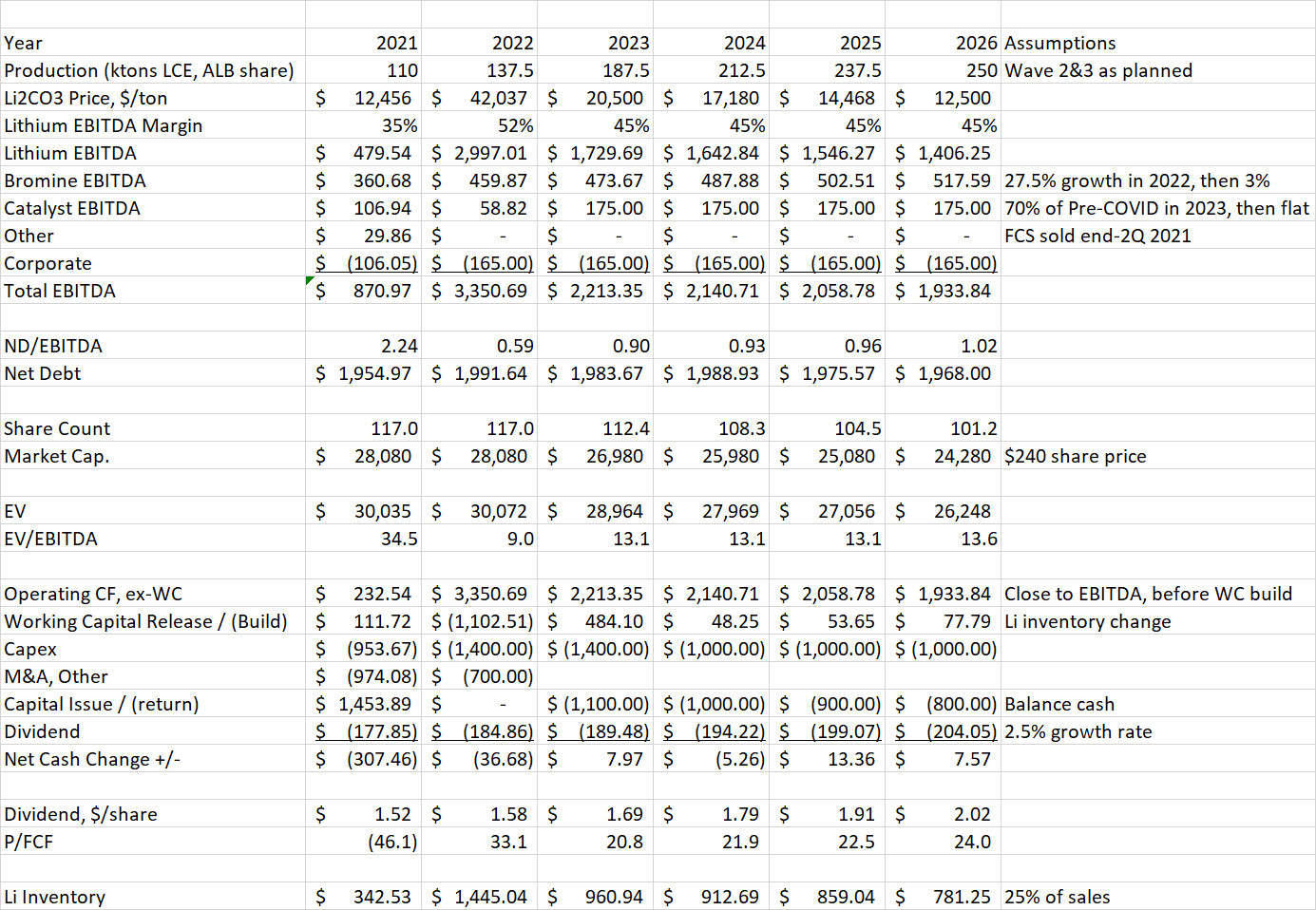

Volume And Price Assumptions

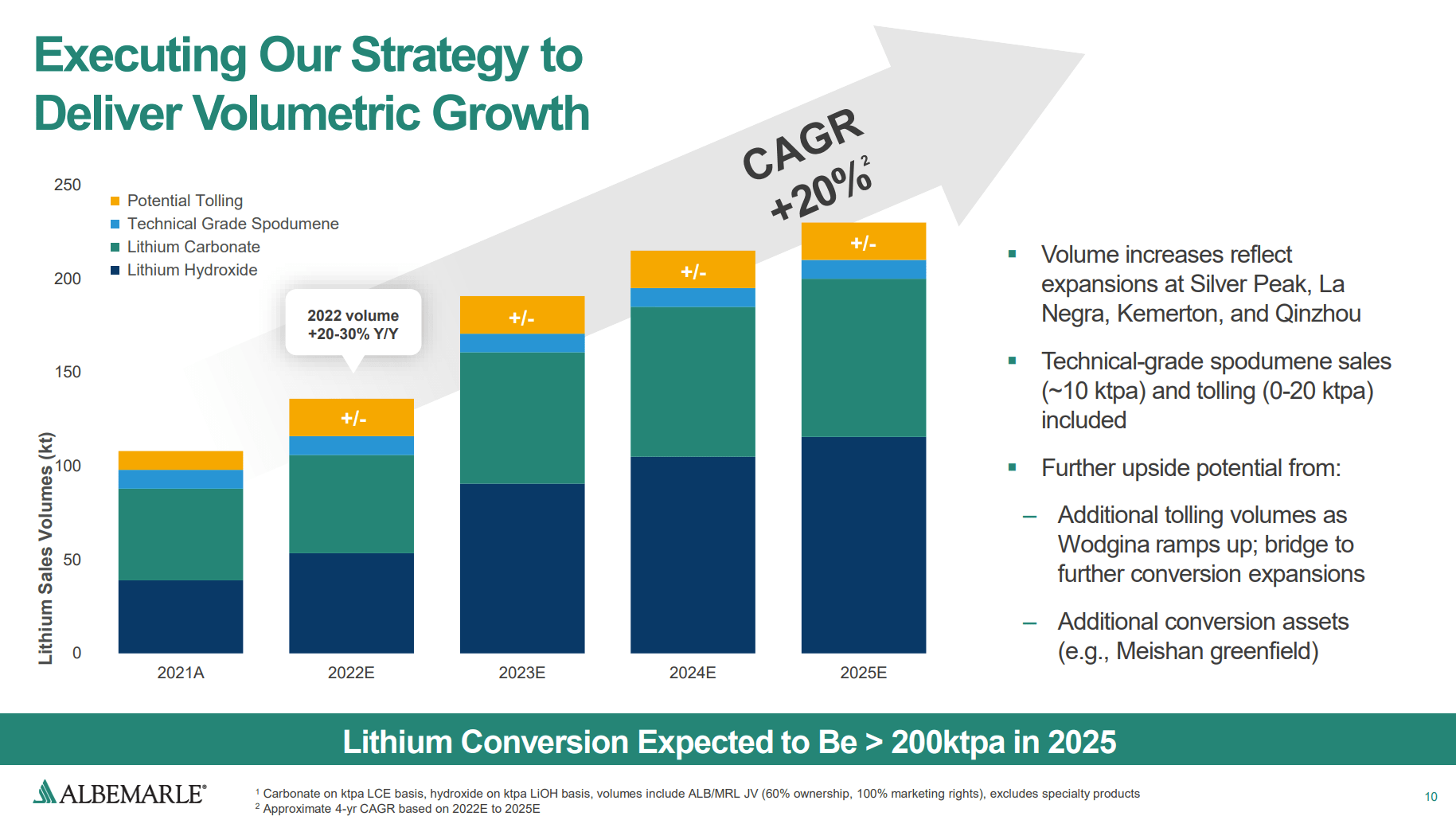

Albemarle sees their lithium sales increasing from 110,000 tons in 2021 to 250,000 tons in 2026. This includes completion of the La Negra brine facilities in Chile and Kemerton II in Australia, as well as the acquisition of the Qinzhou plant in China. Over the next few years, the company will complete two more units at Kemerton and a new lithium hydroxide plant in Meishan, China, as well as expanding Silver Peak in Nevada. I estimate the company will be spending about $1 to $1.4 billion per year of capex on these projects. Albemarle will also process up to 20 ktpa through tolling arrangements.

Albemarle 2Q 2022 Earnings Slides

Albemarle’s latest guidance of pricing up 225%-250% for 2022 implies around $42,000 per ton LCE. This is lower than the current spot price but is more representative of the first half average. Albemarle has done a great job of moving their customers from long-term fixed price contracts to index-based pricing, but there will still be some lag to catch up to spot prices. Management did note that there is upside to the current forecast “if prices stay at their current levels”. My interpretation is that 2H prices will look more like spot prices, bringing the year average price up to $57,000 per ton.

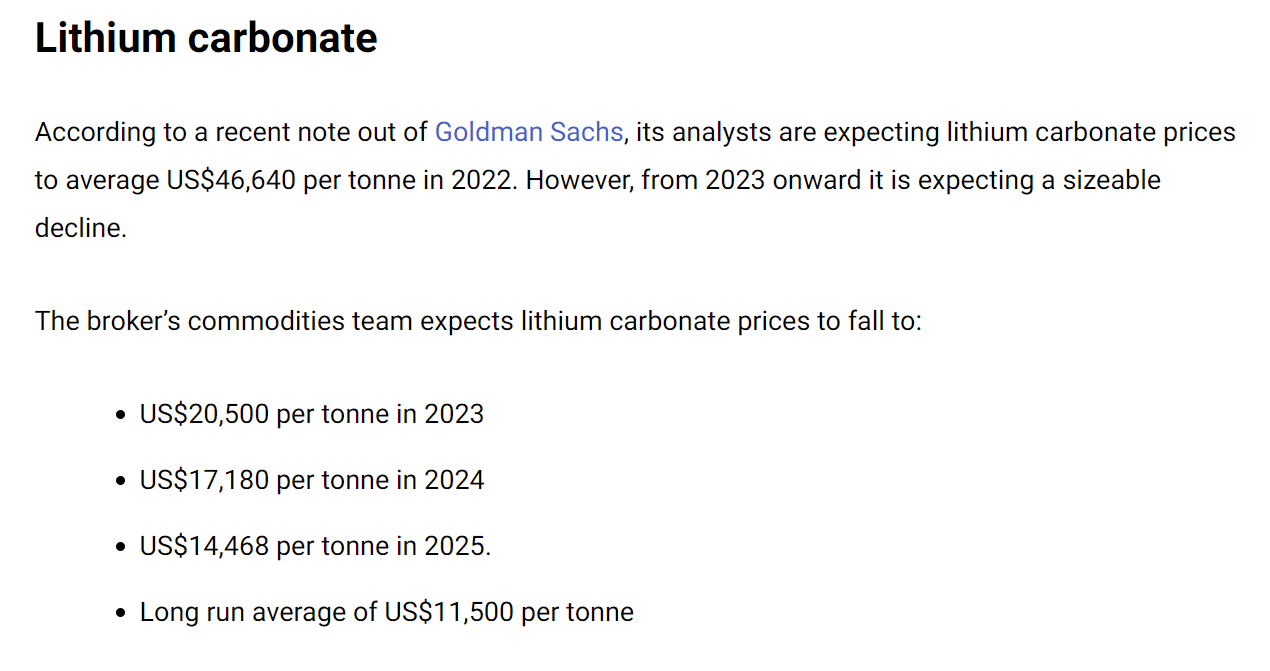

The company never discusses out-year pricing as it is extremely unpredictable, as we see from history and available forecasts from different analysts. For example, Motley Fool Australia published this forecast from Goldman Sachs (GS) in May 2022:

Motley Fool Australia

This forecast now seems very conservative as it did not seem to capture the extended stay at the $70,000 level this year. It also assumes a quick drop back down to $11,500/ton which was historically the marginal cost of production. As more capacity comes on at harder-to-produce sources, however, the marginal cost of production should be higher in the future.

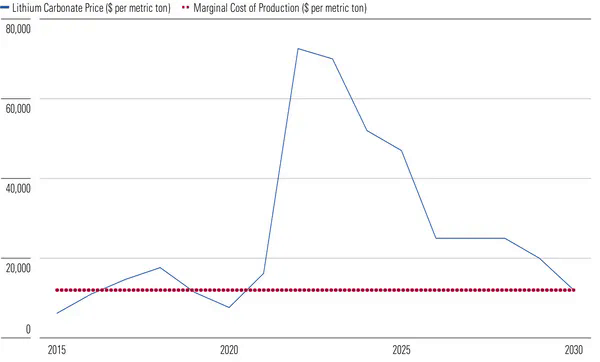

By early July, Morningstar published this forecast, which has much stronger pricing over the next couple years but still comes back down to a marginal cost of production around $12,000/ton by 2030.

Morningstar

These two forecasts produce free cash flow forecasts for Albemarle that differ by a factor of 3.

Conservative Case

For the conservative case, I use Goldman’s price forecast and assume Albemarle reaches its EBITDA margin goal of 45%, which it is already exceeding in 2022. I also include earnings from the company’s still-significant Bromine division as well as Catalysts, which is the smallest division and may be sold at some point.

Author Spreadsheet

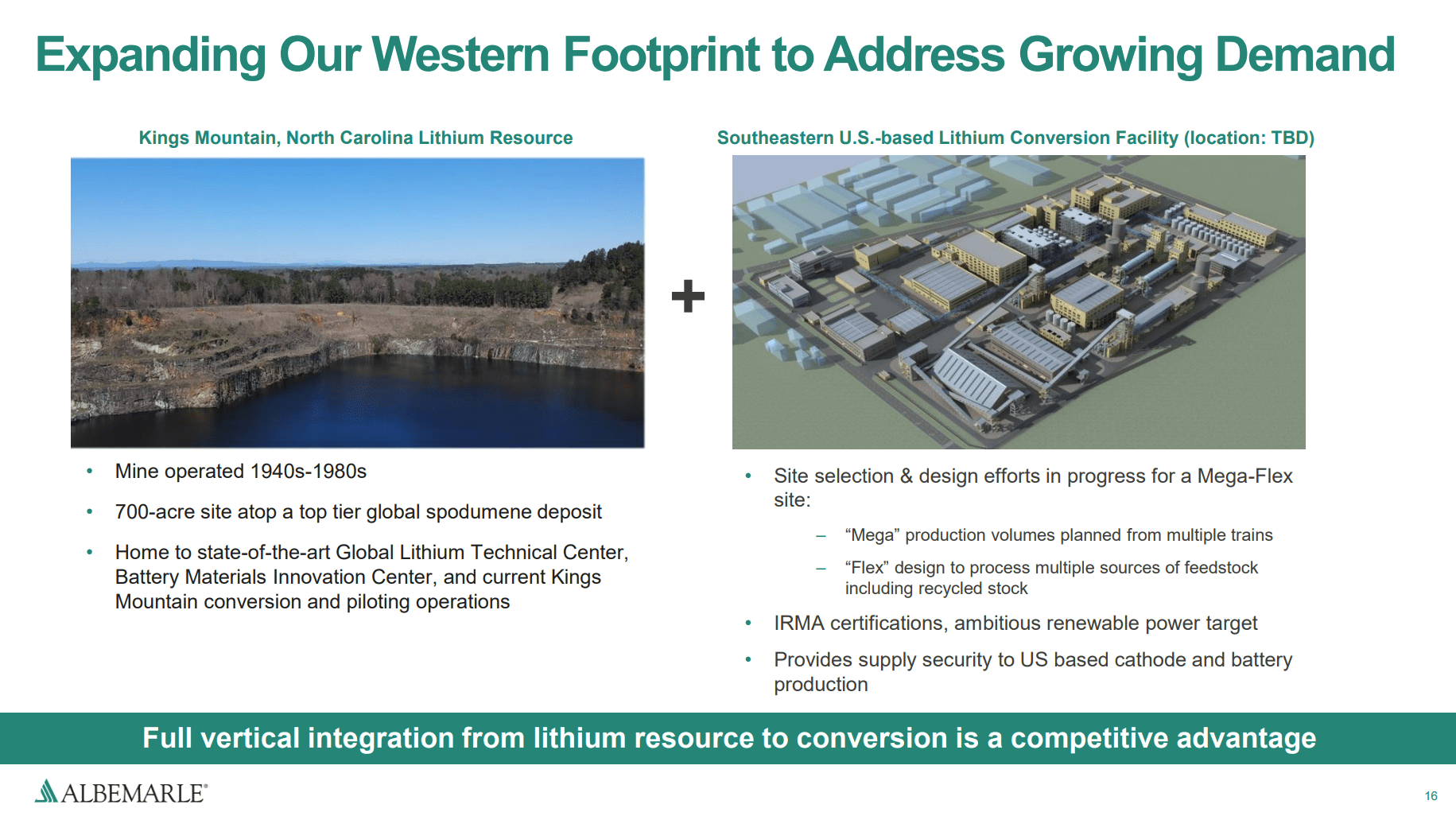

This model produces free cash flow of $1-$1.3 billion per year starting in 2023. I assume Albemarle continues to increase the dividend slowly by 2.5% per year and the excess cash is returned via buybacks. This would still increase the dividend more, as the payout would be spread over fewer shares. In this case, the dividend would grow to $2.02 by 2026, a 6% CAGR from current levels. Using a share price of $240, Albemarle would have an EV/EBITDA around 13 and a P/FCF in the low 20s based on 2023-2026 earnings. This is not super cheap and will require good growth prospects beyond 2026 to justify the share price. Albemarle has growth projects in the hopper, including a “mega flex” conversion plant in the Southeast US which would process 100 ktpa total of spodumene from Kings Mountain, NC plus recycled material.

Albemarle 2Q 2022 Earnings Slides

If the current forecasts pan out that show demand diverging upward from supply starting around 2030, prices will come back up and plants like these will get built.

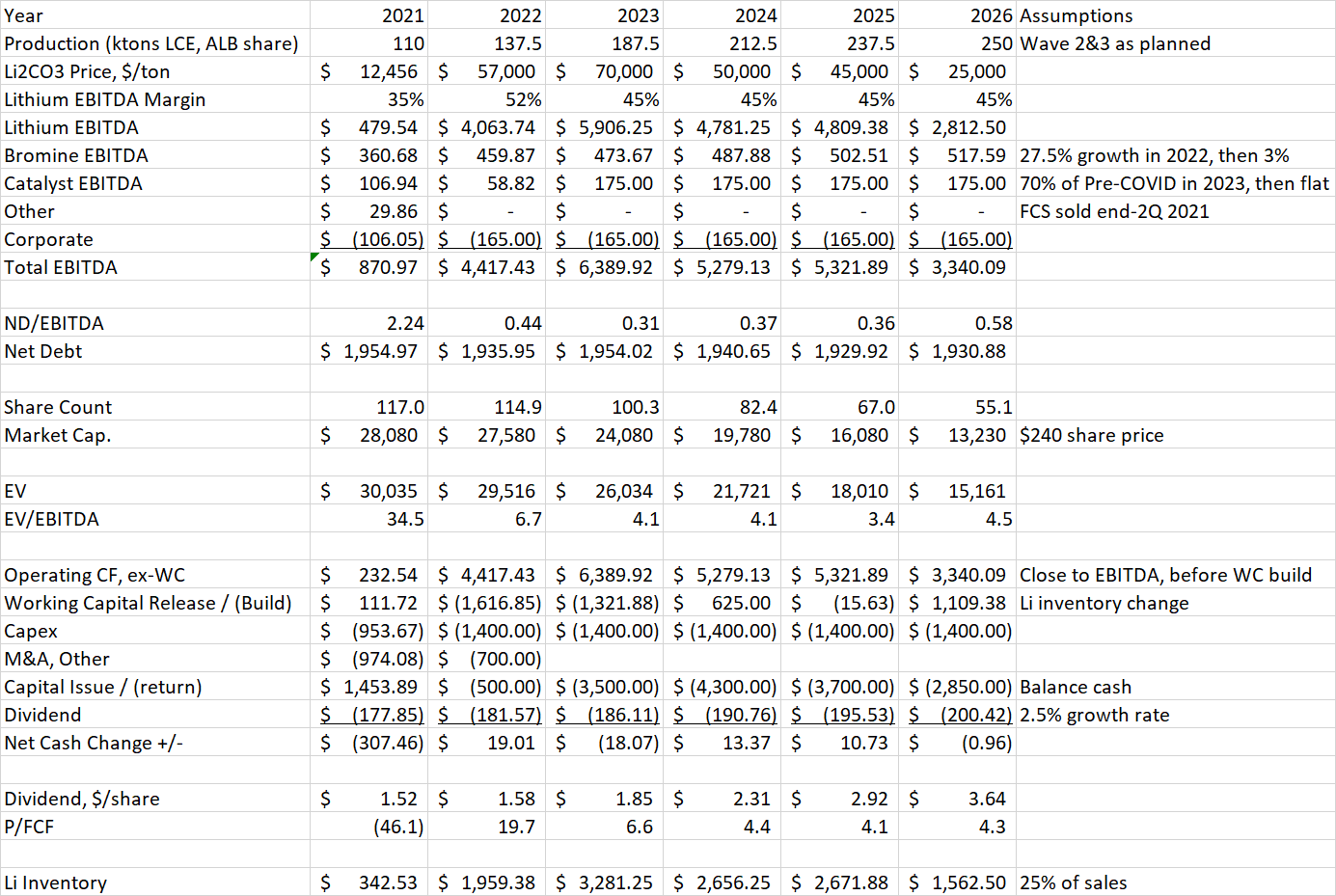

Optimistic Case

For the optimistic case, I use the Morningstar forecast above except for a blended 2022 value of Albemarle’s 1H actuals and the $72,000 shown in the graph for 2H, resulting in a year average price of $57,000/ton. Production ramps up at the same pace through 2026 although show the company spending more on capex each year to accelerate expansion in the second half of the decade. Bromine and Catalyst performance are the same as in the base case.

Author Spreadsheet

This case produces free cash flow of $3-$4 billion starting in 2023. If excess FCF beyond the dividend is applied toward buybacks, it would cut the share count of the company by more than half by 2026. This would grow the dividend to $3.64 in 2026 which represents a 23% CAGR from current levels. EV/EBITDA and P/FCF would be a very cheap multiple of around 4 times.

Conclusion

Albemarle can produce massive free cash flow at current high lithium prices. The catch is that these prices can’t last forever as Albemarle and other companies bring capacity online to meet demand. Even the optimistic forecast shows prices much lower by 2026. This explains the flat to slightly negative reaction in the market after the earnings release despite the massive beat and raise.

In the conservative case with prices dropping quickly under $20,000/ton by 2023, Albemarle should be able to return about $1 billion of capital per year to shareholders. The stock would not be a bargain in this case, although future supply/demand imbalances beyond 2026 would justify the current price. In the more optimistic case, Albemarle can throw off $3 to $4 billion in free cash flow and quickly cut share count in half if they do buybacks. In this case, the stock looks incredibly cheap at around 4x EV/EBITDA or P/FCF in 2024.

The market seems to be pricing in the conservative case, but that means Albemarle stock is no worse than fairly valued with plenty of upside if lithium prices fall more slowly.

Be the first to comment