Thomas Barwick

Ready, set, go: it’s time to invest in growth again. With the markets seeing signs of life in the first few weeks of 2023, growth-oriented investors have a fantastic opportunity to purchase iconic stocks that are still technically in bear market territory after deep corrections last year.

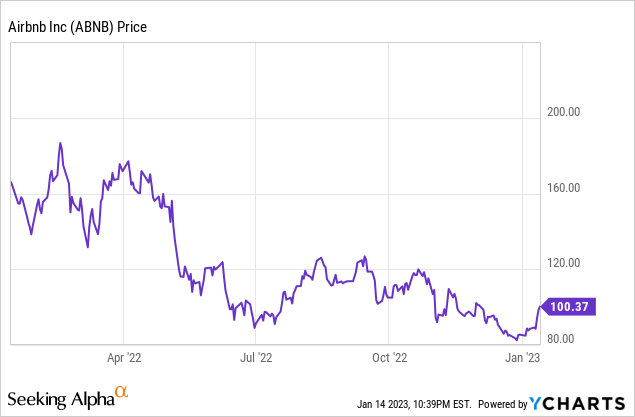

Airbnb (NASDAQ:ABNB), no doubt, is one of the most recognizable tech names in the internet sector. The lodging giant has seen a ~35% correction in its share price over the trailing twelve months, despite the fact that Airbnb has essentially fully recovered from the pandemic as a stronger, more profitable company. It’s a great time for investors to add this name to their portfolios.

A vibrant bull case for Airbnb

I am bullish on Airbnb and am holding onto the stock for the long haul. The company enjoys secular tailwinds from the growth in peer-to-peer markets, a growing appreciation for “authentic” travel experiences, and growth in supply/Hosts as more people chase side income in a post-pandemic world that has somewhat eschewed the normal 9-5 lifestyle. I find it difficult to imagine that in five to ten years down the line, Airbnb won’t become even more dominant as the largest lodging and travel brand than it is today.

Here is my full long-term bull thesis for Airbnb:

-

Pent-up travel demand. As people get back into the swing of travel, Airbnb is well-positioned to absorb that demand and gain market share, thanks to its growing pool of hosts, its broader network of availability in different regions, and its various “Experiences” offerings.

-

Airbnb may not just be for vacation anymore. With so many companies announcing permanent remote or hybrid work structures, many workers have leaped at the chance to become digital nomads and work from anywhere. In the spirit of this trend, even Airbnb itself has also announced that it is allowing its staff to work from any location (including up to 90 days internationally, limited for tax purposes). This trend may see Airbnb picking up not just travel demand, but essentially “rent” budgets from digital nomads as well. As a result of this trend, average trip lengths are increasing quite substantially.

-

Chance to absorb hotel business through promoted listings. It’s not a great time to be in the hotel game right now. After facing two years of heightened vacancy, hotels have always dealt with high third-party booking fees through platforms like Expedia (EXPE) and Booking (BKNG). Airbnb already allows boutique hotels to list on its platform for a fee; over time Airbnb could fully throw its hat in the ring to compete against the high-fee OTA giants.

-

Profitability in mind. During the immediate aftermath of the pandemic, Airbnb laid off about 20% of its staff. While it is now continuing to hire, this profit-centric mindset and the fact that Airbnb is structurally leaner than it was pre-pandemic has allowed the company to make sizable profitability gains.

We’ll dive into this last point in more detail.

Profitability wins above all

Here is something that may surprise investors who haven’t checked in on the stock in several years: Airbnb is now tremendously profitable. The stock suffered from a bit of a slump after it reported a deceleration in bookings in Q3 in early November, but the trade-off is that the company is throwing off healthy amounts of adjusted EBITDA and free cash flow. In today’s relatively risk-averse market, Airbnb’s rich bottom line distinguishes it against many other growth/tech names.

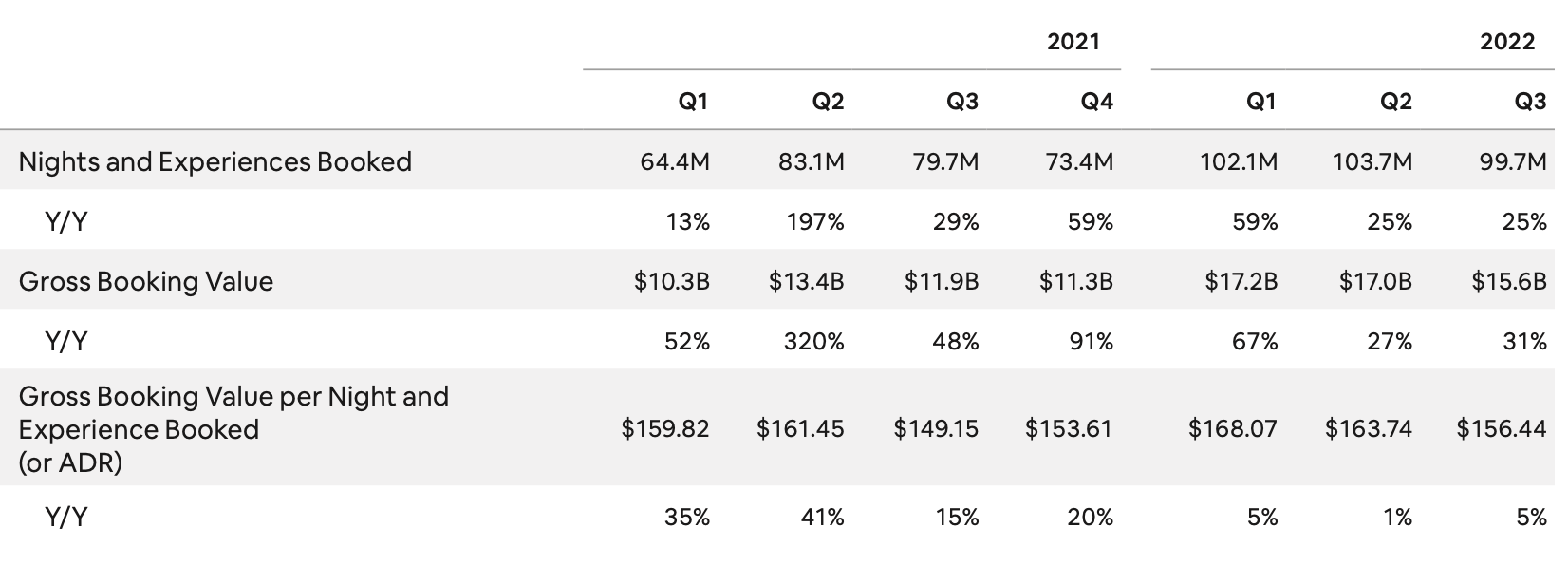

Airbnb bookings (Airbnb Q3 shareholder letter)

First, we’ll discuss bookings. As shown in the chart above, Airbnb is still showing strong double-digit growth in both booking nights and gross booking value, the latter of which grew 31% y/y to $15.6 billion. This is, of course, a slower pace than in 2021 and the early part of 2022, but this is largely due to comps becoming tougher as we move further away from the pandemic. There is also FX headwind to consider, as 55% of Airbnb’s revenue is generated in non-USD currencies. Airbnb’s revenue of $2.88 billion (representing an ~18% take rate, consistent with prior years) grew 29% y/y, but on a constant-currency basis growth would have been seven points stronger at 36% y/y.

Management has continued to cite robust travel demand, even in the face of macro headwinds. Per CEO Brian Chesky’s remarks on the Q3 earnings call:

First, guest demand on Airbnb remains strong. Globally, we exceeded 90 million guest arrivals during the quarter and this is another record. Now even with macroeconomic headwinds, Nights and Experiences Booked increased 25%. And during the quarter, we also continued to see longer lead times, supporting a stronger backlog for Q4. Second, guests are increasingly returning to cities and crossing borders. Both segments continue to accelerate. Cross-border gross nights booked increased 58% compared to a year ago. High density urban nights booked grew 27%. And now even as these two segments return, demand for domestic and non-urban travel remains strong.”

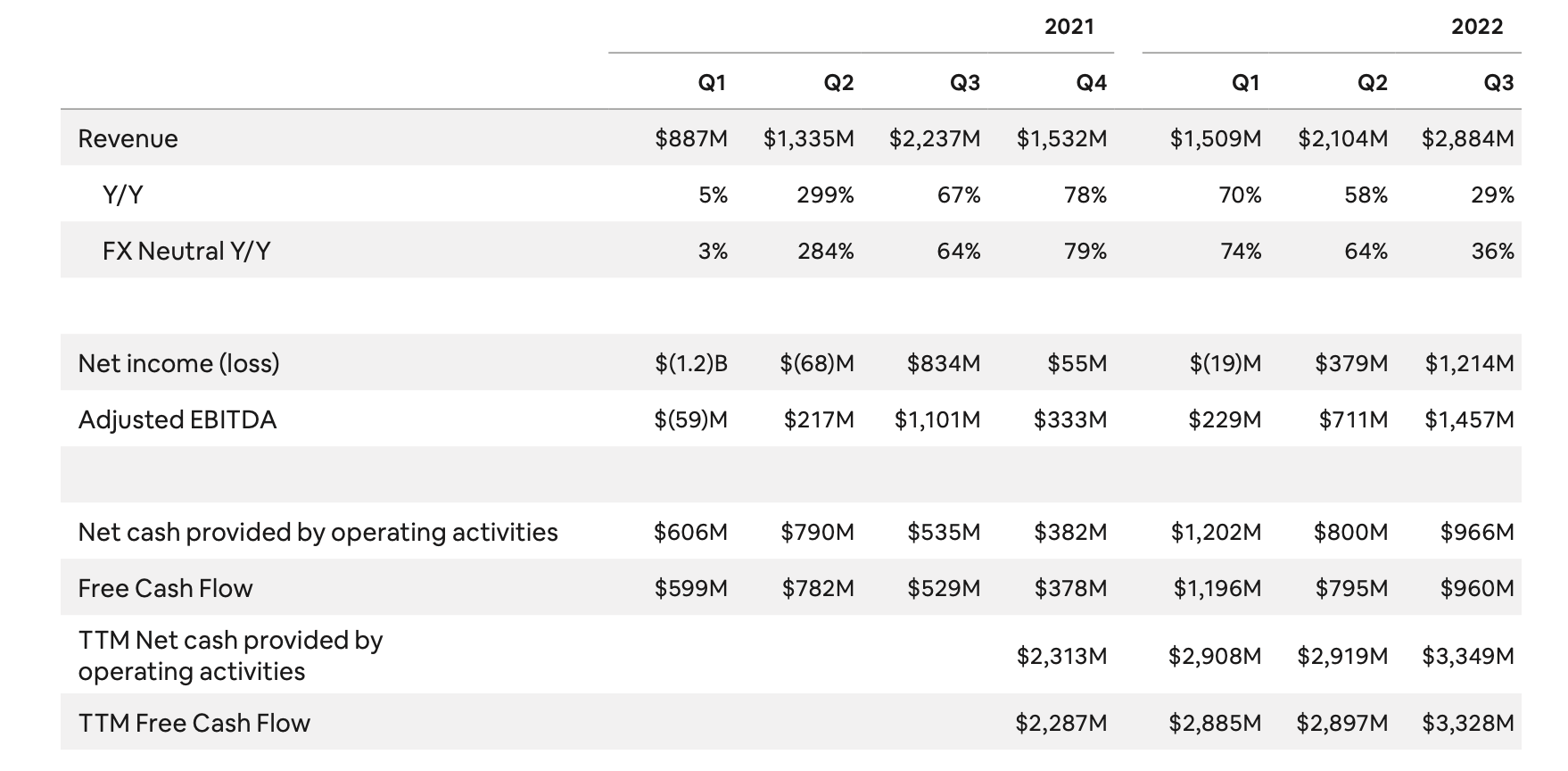

Most importantly, Airbnb’s growth – especially in longer-term stays – has helped the company achieve admirable economies of scale. The company hit $1.46 billion in adjusted EBITDA in Q3, up 32% y/y and representing a meaty 51% adjusted EBITDA margin: two points higher than the year-ago Q3. It’s worth noting that the company’s GAAP net margin of 42% (yes, Airbnb is one of the few prominent growth companies to actually report GAAP earnings!) showed five points of margin improvement versus 37% in the prior-year Q3.

Airbnb key financial highlights (Airbnb Q3 shareholder letter)

Valuation is incredibly modest; key takeaways

Despite its double-digit growth on top of significant margin expansion, Airbnb still trades at quite modest valuation multiples – not at all like the stock back in its IPO days.

At current share prices near $100, Airbnb trades at a market cap of $63.55 billion. After we net off the $9.63 billion of cash and $1.98 billion of debt on Airbnb’s most recent balance sheet, the company’s resulting enterprise value is $55.97 billion.

For the current fiscal year FY23, Wall Street analysts are expecting Airbnb to generate $9.34 billion in revenue, representing 12% y/y growth. Given the fact that Airbnb is currently growing revenue in the high 20s, I think this estimate is rather conservative. Nevertheless, if we conservatively assume Airbnb holds its current TTM FCF margin of 41% and its current adjusted EBITDA margin of 51% on this revenue profile, the company would generate $3.83 billion of FCF and $4.76 billion of adjusted EBITDA next year. This puts the company’s valuation multiples at:

- 14.6x EV/FY23 FCF

- 11.8x EV/FY23 adjusted EBITDA

By no means is Airbnb a value stock, but considering its current pace of growth plus the global dominance of its brand, I’d say these are rather safe multiples to buy into this stock.

The bottom line here: with travel demand healthy and Airbnb finally starting to generate healthy profits, don’t ignore this stock as you are building your 2023 portfolio.

Be the first to comment