JamesBrey

Recently, I made the case that 2023 offers the “Perfect Macro Setup For This High-Quality REIT,” with the high-quality REIT being the retail single-tenant net lease landlord Agree Realty Corporation (ADC).

ADC benefits from an environment of disinflation and falling long-term interest rates in multiple ways:

- The real (inflation-adjusted) value of its rental revenue streams rises.

- Its cost of debt falls.

- Cap rates stabilize or decline, lifting property values and thus ADC’s net asset value.

But what about the widely anticipated recession to come this year?

Here ADC shines as well through a rock-solid portfolio of investment grade tenants in fungible buildings, a fortress balance sheet, and a peer-leading cost of capital.

The downside of ADC’s strong cost of capital, though, is that it yields only 3.9%, which is on the low end for net lease REITs. So investors may instead want to consider ADC’s sole preferred stock:

- Agree Realty 4.25% Depositary Cumulative Preferred Series A (NYSE:ADC.PA)

In what follows, I want to make three points about ADC’s preferred stock:

- The dividend is ultra-safe

- It has an extremely low likelihood of being called

- It acts like a bond proxy

If you wanted to buy investment grade corporate bonds anyway, I would argue that ADC.PA’s 5.8% dividend yield is a better option, if only as a short-term bet on falling interest rates.

ADC.PA’s Dividend Is Ultra-Safe

There are two primary reasons why ADC.PA’s preferred dividend is ultra-safe:

- The REIT’s cash flows are extraordinarily stable due to a strong and recession-resistant portfolio

- The preferred stock capitalization is a tiny fraction of ADC’s enterprise value, and the preferred dividend is a tiny fraction of EBITDA

On that first point, ADC’s portfolio is overwhelmingly made up of strong, high-credit, recession-resistant retailers that are highly likely to continue paying rent through a recession.

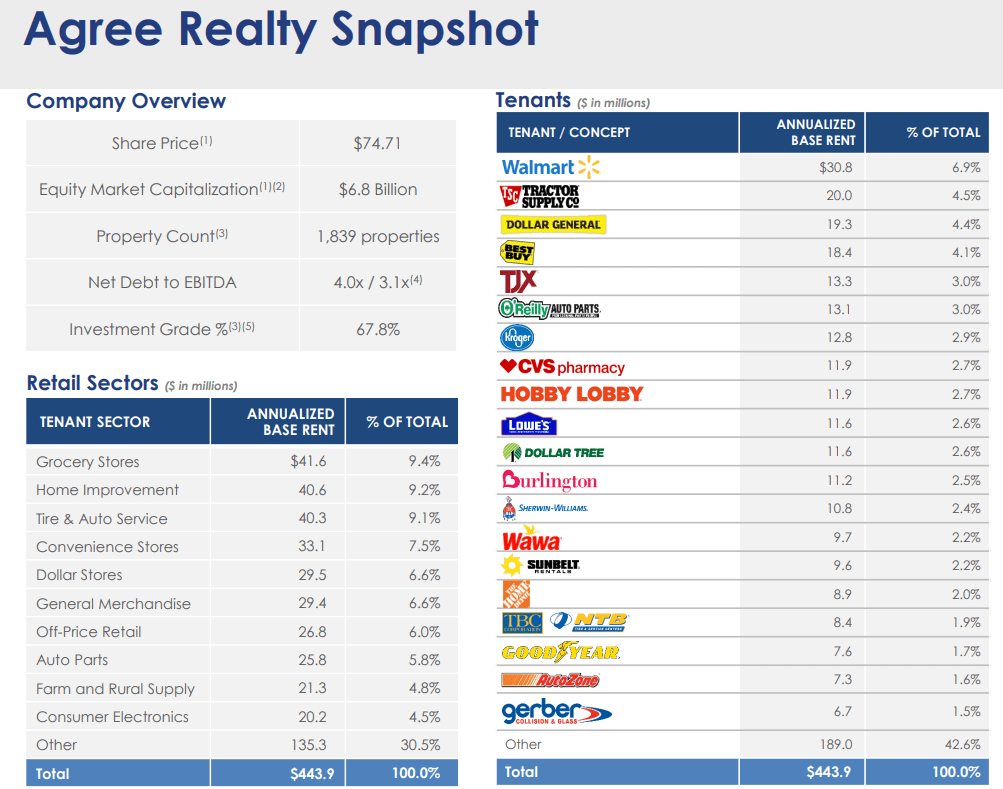

ADC February 2023 Presentation

What’s more, as you can see in the “company overview” box above, net debt to EBITDA is quite low for a REIT at 4.0x, and the REIT’s weighted average interest rate is quite low at less than 3.5%. And ADC’s weighted average debt maturity sits at around 8 years. In other words, interest expenses do not threaten to eat into the preferred dividend’s coverage much at all.

On the second point, ADC.PA represents $175 million of ADC’s enterprise value of $8.315 billion, or 2.1%. The ~$7.44 million in annual preferred dividends represents about 2% of trailing twelve-month EBITDA of ~$364 million.

ADC.PA Is Probably Not Going to Be Called – Ever

Given the perpetual nature of ADC.PA (no required redemption date), management almost certainly won’t call the preferred stock on its redemption date when it comes. Consider that ADC.PA is a very low-cost form of perpetual capital for ADC – the second lowest coupon yield for a REIT preferred. Only the A-rated Public Storage (PSA) has issued a lower-yielding preferred stock.

Though 4.25% is a higher rate than would’ve been paid if ADC had instead issued bonds in September 2021, it is significantly lower than the interest rate ADC could get on new debt today. So, if ADC.PA’s call date was today, it would make no sense to replace ADC.PA with debt.

But what if interest rates are back to ultra-low levels when ADC.PA’s call date arrives? What if ADC had the option of repaying ADC.PA with bonds sporting sub-3% coupon rates? Even in this case, it is still unlikely that ADC would replace the preferred with bonds, because it would almost certainly be more accretive to AFFO per share to buy properties with that newly issued debt. I find it highly unlikely that ADC would be unable to find net lease properties to buy at cap rates anywhere near 4.25%.

What about replacing the preferred stock with common stock? This would make no sense. Not only has ADC never traded at an AFFO yield anywhere near as low as 4.25%, even if it did, management would almost certainly be issuing shares to buy properties.

So, ADC.PA will probably never be called.

Does this mean that the ~36% upside to par value will never be achieved? No, not necessarily.

ADC.PA Is A Bond Proxy

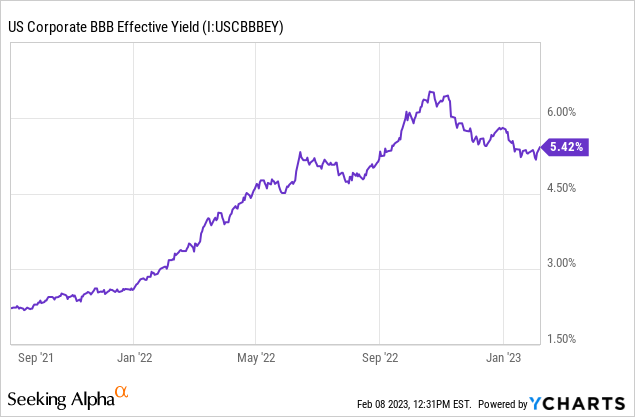

You might wonder why investors would bid ADC.PA back up to $25 if there’s little chance of the preferred stock being called. The answer is that ADC.PA basically acts like a bond proxy. Its yield moves up and down along with long-term corporate interest rates.

ADC.PA’s yield began, of course, at 4.25% at its IPO in mid-September 2021. At the time, the average corporate BBB bond yield was in the 2% territory. But yields didn’t stay there. They immediately began rising after ADC.PA’s IPO as the prices of both ADC.PA and corporate bonds slid.

By the end of 2021, ADC.PA’s yield reached about 4.5%, while BBB bonds yielded an average of around 2.5%. In June 2022, as BBB bond yields reached 5%, ADC.PA’s yield hit 6.1%.

Then, as BBB bond yields slid in July to around 4.8% at the beginning of August, ADC.PA’s yield slipped back down to 5.1%, only to subsequently surge all the way up to 6.75% in late October as BBB bond yields hit 6.5%.

As BBB bond yields have eased from their highs to about 5.4%, so also has ADC.PA’s yield declined to 5.8%.

Though the correlation between ADC.PA and corporate bond yields may not be one-to-one, it is pretty darn close.

ADC.PA’s ~36% upside, then, is dependent upon corporate interest rates falling.

Bottom Line

While preferred stocks are a hybrid between equity and debt, ADC.PA very much trades like a corporate bond, albeit one with a perpetual maturity.

Long-term interest rates have likely peaked for this cycle along with inflation, so the best-case scenario for ADC.PA is that the average BBB bond yield falls back to a 3-handle and the preferred stock achieves its full 36% upside to par value – on top of the 5.8% yield.

That would represent a total return of 41-42%, or about 15% annually over a four-year period.

But the most reasonable worst-case scenario for ADC.PA is that corporate bond yields (and ADC.PA’s dividend yield) continue to float around their current level, offering the preferred stock little upside. If we are indeed in a “higher for longer” environment, then buyers of ADC.PA today will get a total return of 5.8%, equal to the dividend yield.

So, the reasonable worst case is 5.8% annual returns, while the best case is 14-15% annual returns, depending on what interest rates do in the coming years.

Be the first to comment