Khanchit Khirisutchalual/iStock via Getty Images

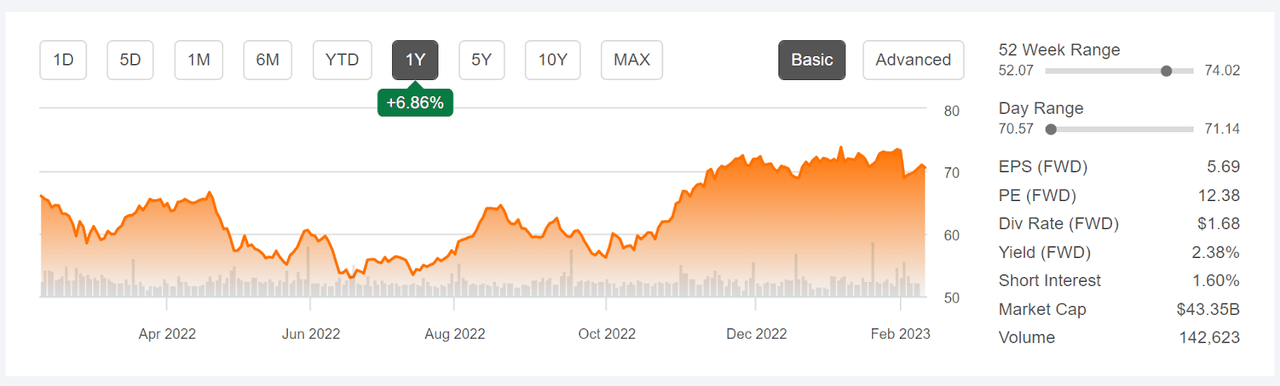

Aflac (NYSE:AFL) reported Q4 2022 results on February 1, 2023, beating expectations on earnings but missing on revenues. Exchange rates were a significant drag on results. While AFL stock dropped following the Q4 results, the shares have performed admirably over the past year, with 12-month total return of 9.1%, as compared to -1.4% for the life insurance industry group (as tracked by Morningstar), 8.3% for the iShares U.S. Insurance ETF (IAK), and -7.5% for the S&P 500 (SPY). AFL’s longer-term trailing total returns are remarkably stable, with 3-, 5-, and 10-year annualized total returns of 12.1%, 13.0% and 12.3% per year, respectively. AFL is currently trading at about 4.4% below the 12-month high closing price of $73.84 on January 6th.

12-Month price history and basic statistics for AFL (Seeking Alpha)

As I discussed in my last post on AFL, rising interest rates tend to be good for life insurance companies because of the corresponding decline in the net present value of liabilities (expected future payouts). Historically, AFL’s returns have a consistent positive correlation to increases in Treasury yields.

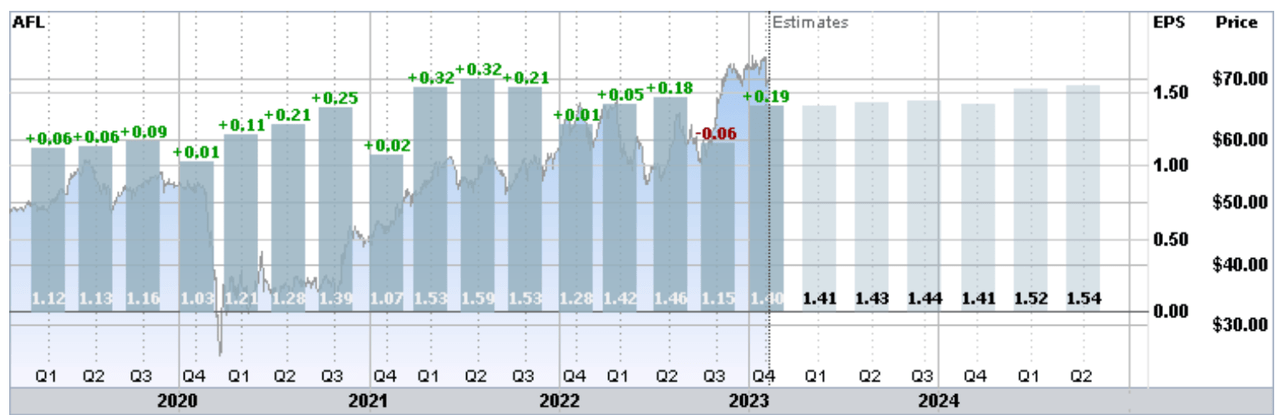

AFL has managed to grow earnings at a modest pace over the past 4 years, and the expectation is that the rate of growth will be modest over the next several years. ETrade reports that the consensus expected EPS for 2023, 2024, and 2025 are $5.69, $6.06, and $6.42, as compared to $5.67 in 2022.

Trailing (4 years) and estimated future quarterly EPS for AFL. Green (red) values are amounts by which EPS beat (missed) the consensus expected value (ETrade)

While AFL’s forward dividend yield is not especially high at 2.38%, the historical dividend growth rate is consistently high. The trailing 3-, 5-, and 10-year annualized dividend growth rates are 14.0%, 13.0%, and 9.1% per year, respectively. AFL has increased the dividend for a remarkable run of 40 consecutive years. Along with paying out $248 million in dividends in Q4, the company also spent $600 million on share repurchases.

I last wrote about AFL on August 18, 2022, about 5 ½ months ago, when I reiterated a buy rating. At the time, the Wall Street consensus rating was a hold and the consensus 12-month price target was 3% to 4% below the share price. Including dividends, consensus expected 12-month return was close to zero. The market-implied outlook, a probabilistic price forecast that represents the consensus view from the options market, was bullish for the 5.1-month period to January 20, 2023, with expected volatility of 24.6% (annualized). Considering the beneficial effects of rising rates and the company’s solid earnings, along with the analysts’ tendency to underestimate AFL, maintaining a buy rating was the clear choice. In the period since this post, AFL has performed well relative to the broader market.

Previous post on AFL and subsequent performance vs. the S&P 500 (Seeking Alpha)

For readers who are unfamiliar with the market-implied outlook, a brief explanation is needed. The price of an option on a stock reflects the market’s consensus estimate of the probability that the stock price will rise above (call option) or fall below (put option) a specific level (the option strike price) between now and when the option expires. By analyzing the prices of call and put options at a range of strike prices, all with the same expiration date, it is possible to calculate the probable price forecast that reconciles the options prices. This is the market-implied outlook. For a deeper discussion than is provided here and in the previous link, I recommend this outstanding monograph published by the CFA Institute.

As we have now passed the period for which the previous outlook was calculated, I have generated updated market-implied outlooks for AFL and I have compared these with the current Wall Street consensus outlook in revisiting my rating.

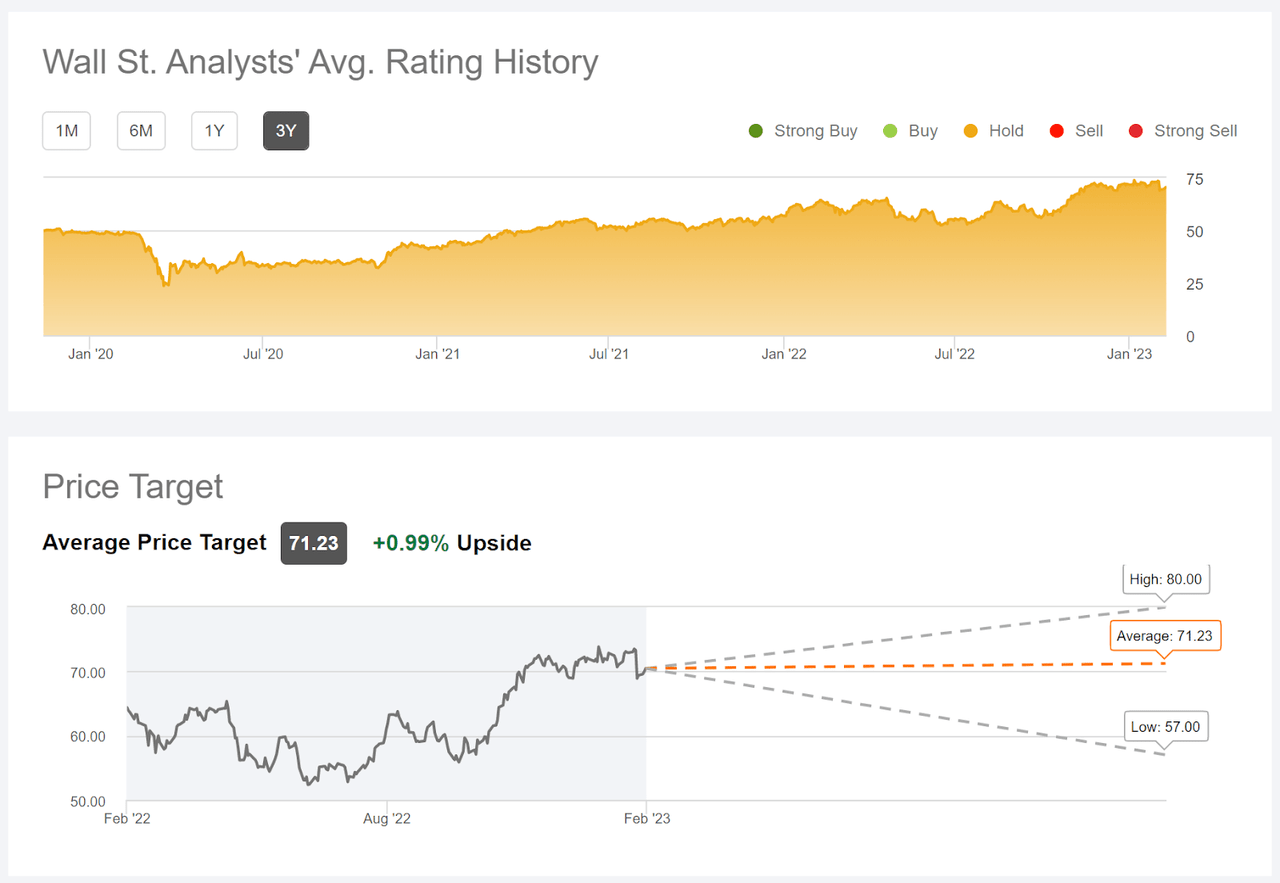

Wall Street Consensus Outlook for AFL

Seeking Alpha calculates the Wall Street consensus outlook for AFL by aggregating the views of 13 analysts who have published ratings and price targets over the past 90 days. The consensus rating is a hold, as it has been for all of the past 3 years. The consensus 12-month price target is 0.99% above the current share price.

Wall Street analyst consensus rating and price target for AFL (Seeking Alpha)

As I have noted previously, it appears that the analysts consistently underestimate AFL. The annualized total 3-year return for AFL is 12.1% per year, substantially higher than the 9.07% per year for the S&P 500 (SPY), a period during which the consensus rating has been a hold.

Market-Implied Outlook for AFL

I have calculated the market-implied outlook for the 4.2-month period from now until June 16, 2023 and for the 11.2-month period from now until January 19, 2024, using the prices of call and put options that expire on this date. I selected these specific expiration dates to provide a view to the middle of 2023 and through the entire year.

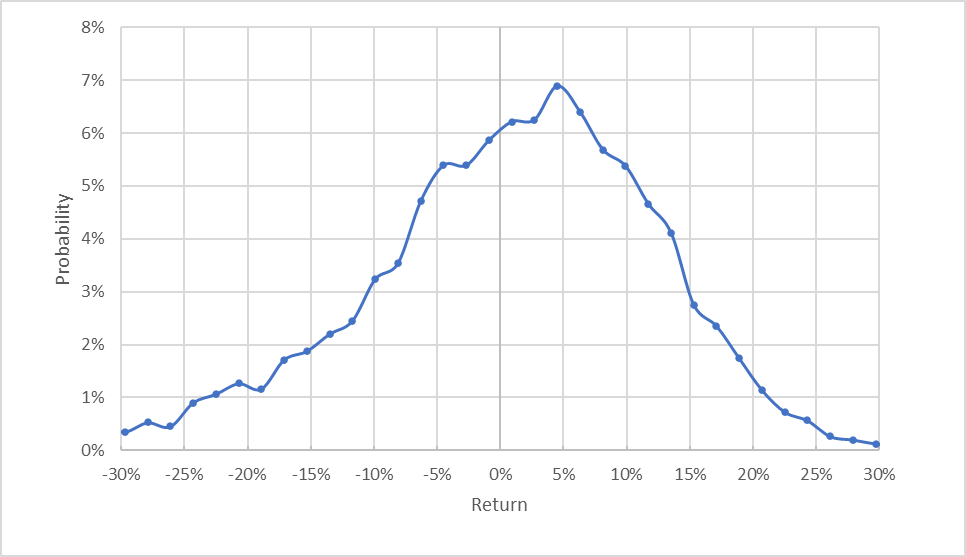

The standard presentation of the market-implied outlook is a probability distribution of price return, with probability on the vertical axis and return on the horizontal.

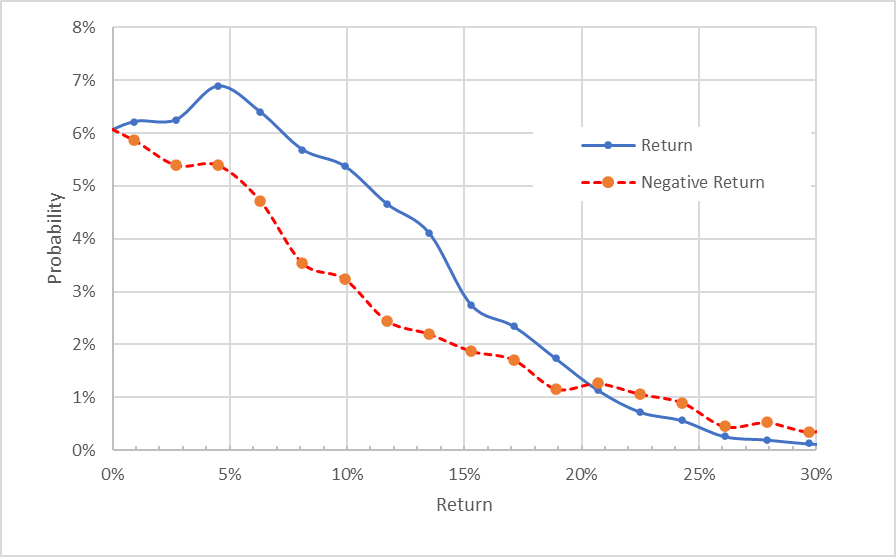

Market-implied price return probabilities for AFL for the 4.2-month period from now until June 16, 2023 (Author’s calculations using options quotes from ETrade)

The outlook to the middle of 2023 is tilted to favor positive returns. The maximum probability corresponds to a price return of 4.5%. The expected volatility calculated from this distribution is 21.9% (annualized). For comparison, ETrade calculates an implied volatility of 20% for the options expiring on June 16th.

To make it easier to compare the relative probabilities of positive and negative returns, I rotate the negative return side of the distribution about the vertical axis (see chart below).

Market-implied price return probabilities for AFL for the 4.2-month period from now until June 16, 2023. The negative return side of the distribution has been rotated about the vertical axis (Author’s calculations using options quote from ETrade)

This view shows the difference in probabilities for positive and negative returns of the same size, as measured by the vertical distance between the solid blue line and dashed red line on the chart above. The probabilities strongly favor positive returns over a wide range of the most-probable outcomes. This is a bullish outlook.

Theory indicates that the market-implied outlook is expected to have a negative bias because investors, in aggregate, are risk averse and thus tend to pay more than fair value for downside protection. There is no way to measure the magnitude of this bias, or whether it is even present, however. The expectation of a negative bias reinforces the bullish interpretation of this outlook.

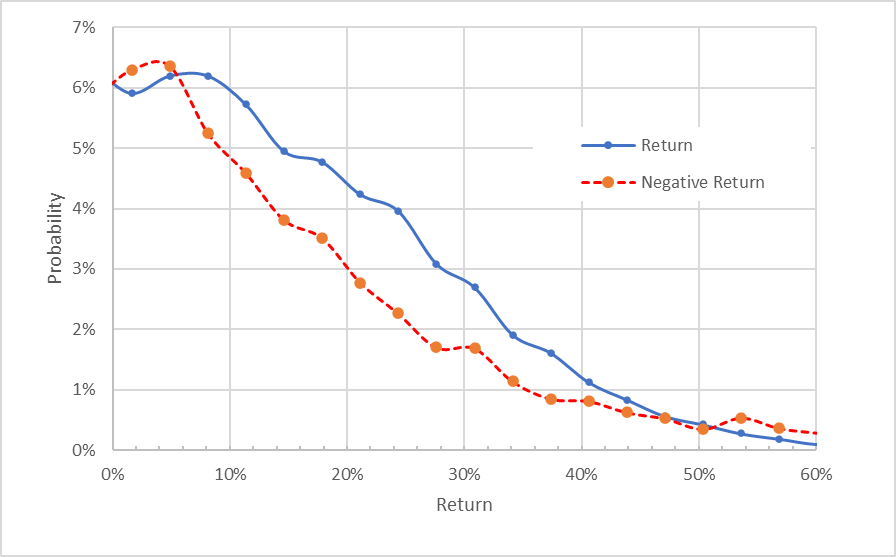

The market-implied outlook for the 11.2 months from now until January 19, 2024 is also bullish, although there is not a well-defined shift in the peak probability. Even so, the spread favoring positive returns is consistently high across most of this distribution. The expected volatility calculated from this distribution is 22.9% (23.6% annualized). This is a bullish outlook.

Market-implied price return probabilities for AFL for the 11.2-month period from now until January 19, 2024. The negative return side of the distribution has been rotated about the vertical axis (Author’s calculations using options quotes from ETrade)

For those who are concerned that the Wall Street analysts expect no price appreciation over the next year, as well as income-oriented investors, selling covered calls is worth considering. As I have been writing this post today, I purchased AFL at $70.43 and sold call options with a strike of $70, expiring on January 19, 2024, for $7.00. This net position has an option premium yield of 9.3% (having subtracted the $0.43 by which these options are in the money) over the next 11.2 months. In addition, this position is expected to provide 3 dividend payments of $0.42 each over this period, so the total income is 11.1%.

Summary

Aflac has outperformed over the past year, with contributing factors being rising interest rates and a broad rotation from growth to value. The company also delivered solid earnings, even with headwinds from exchange rates. So far in 2023, we are seeing a resurgence of growth stocks, so the question is how well AFL will hold up. The Fed is signaling that there will be further rate increases, albeit smaller than over the past year. The Wall Street consensus rating is a hold, with a consensus price target that corresponds to a total return of 3.4% over the next year. As I have noted, however, the Wall Street consensus has consistently underestimated AFL in recent years. The market-implied outlook for AFL is bullish to the middle of 2023 and into the start of 2024, with fairly low volatility. I am maintaining a buy rating on AFL.

Be the first to comment