Natali_Mis

Dividend growth investing doesn’t always have to be with popular names such as Microsoft (MSFT) or Apple (AAPL). That’s because the future is always full of unknowns, and it will take many years before an investor will achieve a healthy yield on cost from buying at today’s prices.

That’s why it may be helpful to buy into a stock that also has a tried-and-true business model combined with a high starting yield. This brings me to Advance Auto Parts (NYSE:AAP), which was a highflyer that’s now fallen on hard times.

As shown above, AAP has fallen by 38% since the start of the year, and in this article, I highlight why this presents an excellent opportunity for value investors, so let’s get started.

Why AAP?

Advance Auto Parts is a leading parts provider for the automotive aftermarket, serving both DIY customers and professional installers alike. At present, it operates over 4,747 stores and 313 WorldPac branches primarily in the U.S., Canada, and Puerto Rico. AAP also serves 1,335 independently owned Carquest branded stores, furthering its reach to more customers and markets.

AAP’s vast store network serves as a good defense against e-commerce players like Amazon (AMZN). That’s because customers are more likely to visit a location to buy their parts, where there is in-house expertise and installation services, which is hard to replicate with online manuals and videos. AAP also has a tool-loan program, which is helpful for a customer’s one-time specialized installation. This, combined with parts available on demand, is especially helpful when a customer needs a part quickly to regain their use of their personal or commercial vehicle.

Having said that, AAP is seeing some challenges, as its third quarter (ended in October) comparable sales were down by 0.7% YoY. AAP’s operating fundamentals have lagged its peers, as it still has an ongoing turnaround to improve part availability and service levels.

Moreover, inflationary product costs and unfavorable channel mix has pressured margins, as reflected by adjusted operating margin declining by 68 basis points YoY to 9.8%, down from 10.4% in the prior year period.

Nonetheless, AAP continues to be a free cash flow generating machine, returning $167 million to shareholders during the last quarter in the form of share dividends and buybacks (0.4 million shares repurchased), bringing total capital returns to $860 million for the first nine months of the year.

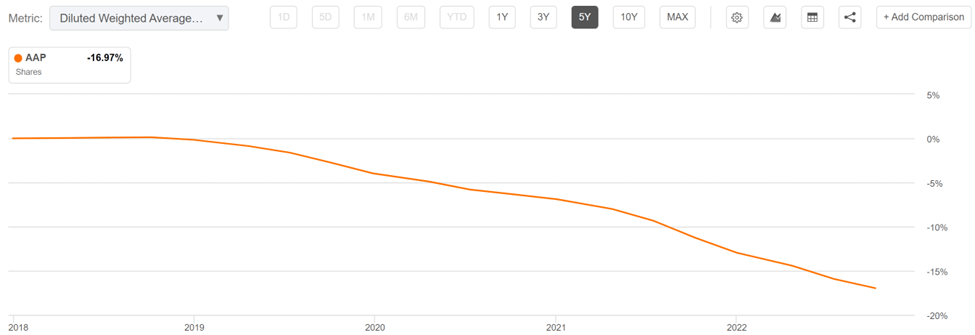

AAP has $1 billion in remaining authorization on this share repurchase program, and that’s rather significant for a company with an $8.4 billion equity market cap. As shown below, AAP has reduced its share count by a substantial 17% over the past 5 years alone.

AAP Shares Outstanding (Seeking Alpha)

Looking forward, management has expressed dissatisfaction with top line performance and announced strategic initiatives to put the business on firmer footing, as highlighted during the recent conference call:

As we develop plans for 2023 and beyond, we’ve done a deep dive on the competitive environment and the actions necessary to accelerate growth. From our analysis, two opportunities came to the forefront, particularly in the professional sales channel. First, we have opportunities on availability in certain categories, which require inventory investment to enable us to get more SKUs closer to the customer.

Secondarily, while our research has consistently indicated that price is not the most important driver of choice for professional customers, we’ve tested and will make surgical pricing actions in certain categories to enable us to better address changes in competitive pricing dynamics.

Meanwhile, AAP maintains a BBB- investment grade rated balance sheet, and pays an attractive 4.2% yield at the current price, that’s well-covered by a 45% payout ratio. Management is clearly prioritizing shareholder returns, as the $1.50 quarterly dividend rate this year was significantly ramped up from the $1.00 rate last year. Given that the dividend was last raised in February, I would expect to see another raise in the early months of 2023.

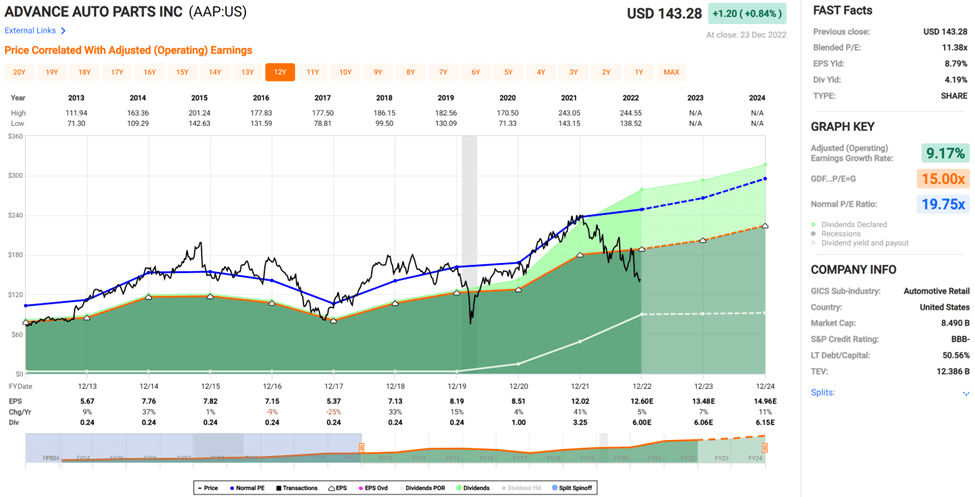

I also believe AAP’s headwinds have been more than baked into the current share price of $143 with a forward PE of 11.4. As shown below, this sits well below AAP’s normal PE of 19.8. Analysts have a consensus Buy rating on the stock with an average price target of $173, equating to a potential 25% total return from the current price.

AAP Valuation (FAST Graphs)

Investor Takeaway

AAP’s operating fundamentals have lagged its industry peers, and its share price performance is deeply in the red for the year. However, management is proactively taking steps to address its issues while prioritizing shareholder returns. It appears that AAP’s near-term headwinds have been more than priced into the stock, giving value investors a respectable starting yield over 4% and potentially strong total returns from here.

Be the first to comment