When we last spoke about Adobe Inc. (NASDAQ:ADBE), it was in the context of the largest bubble in the history of mankind. We did not mince any words on April 10, 2022, about the need to run for exit like the theatre was on fire.

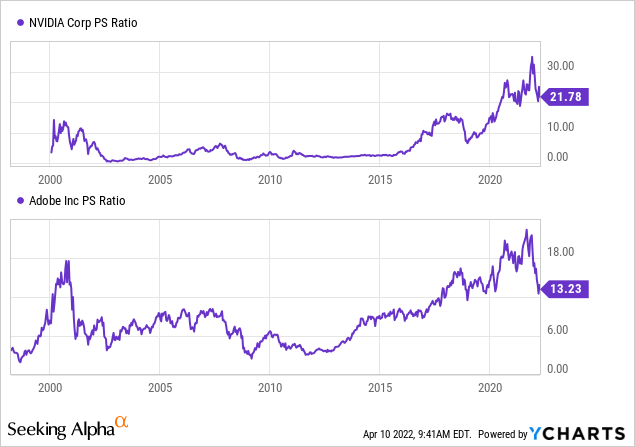

NVIDIA Corporation (NVDA) still trades at twice the price to sales multiple that it achieved at the NASDAQ peakin 2000.

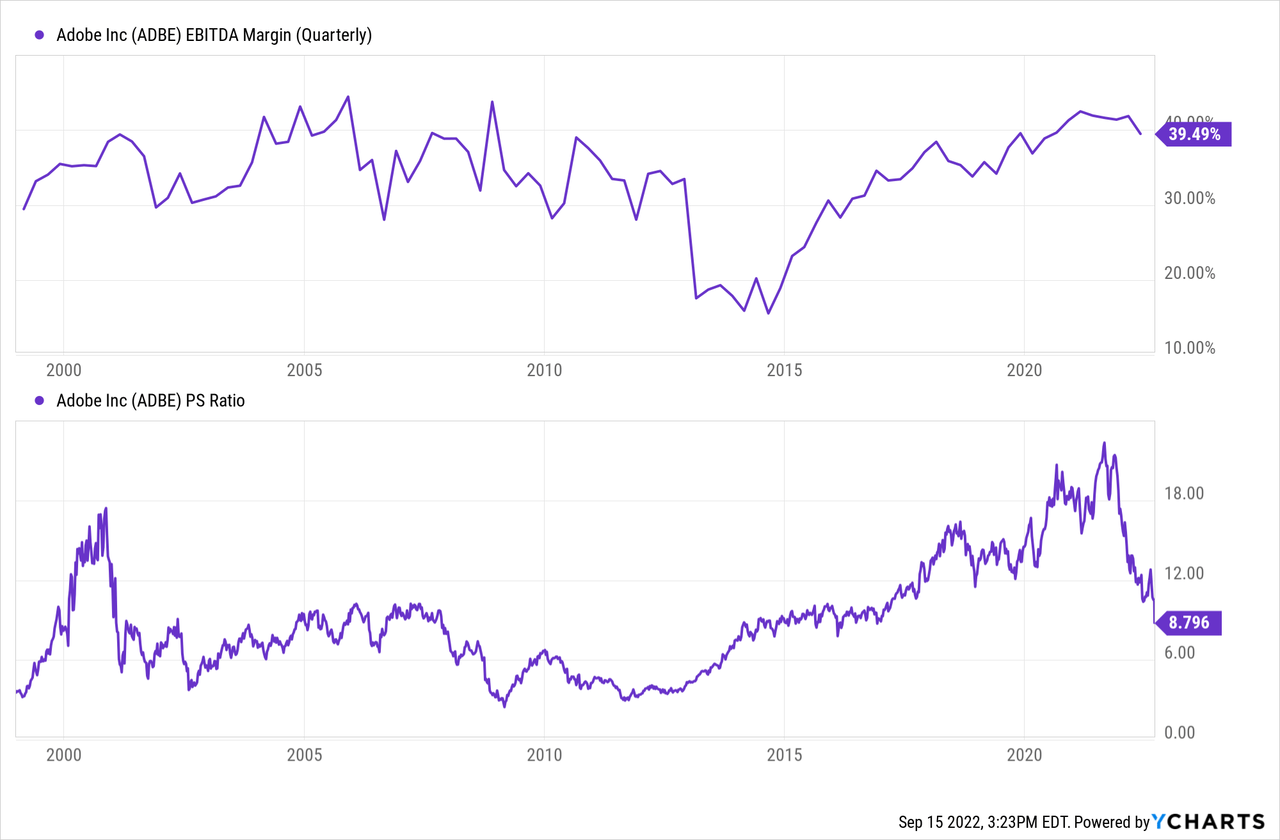

Y-Charts

Adobe Inc. is hovering right at that peak valuation level and trades at 40X GAAP EPS while expecting a 2.5% GAAP income growth for 2022. When this bubble fully deflates everyone will look back at this time fondly and wish they had sold more of these.

We look at the recent results and tell you it is not too late to start running for the hills.

The Results

At first glance the results were not too bad. The $3.23B in revenue for the Digital Media division was a13% increase over the prior year or a 16% increase in constant currency. Creative revenue was up about 14% in constant currency. Document Cloud was the star with a 25% in constant currency growth.

Adobe Results Press Release

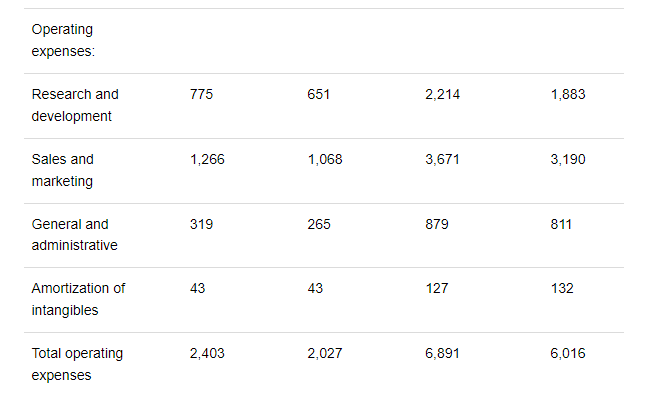

These are not numbers growth investors live for. Unfortunately, there was some other “growth” that was less than positive. Total operating expenses jumped 19% up to 2.407 billion. Outside of amortization of intangibles, every category was up strongly.

Adobe Results Press Release

This is salary inflation and it is flowing through with a vengeance.

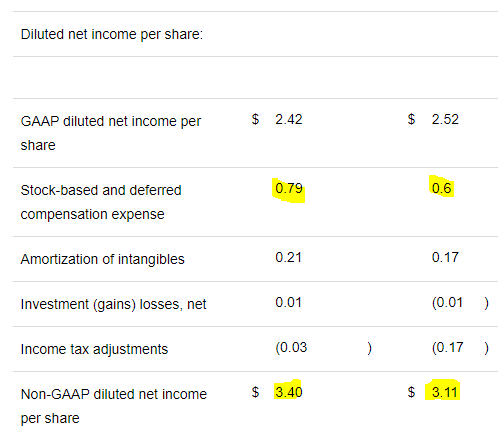

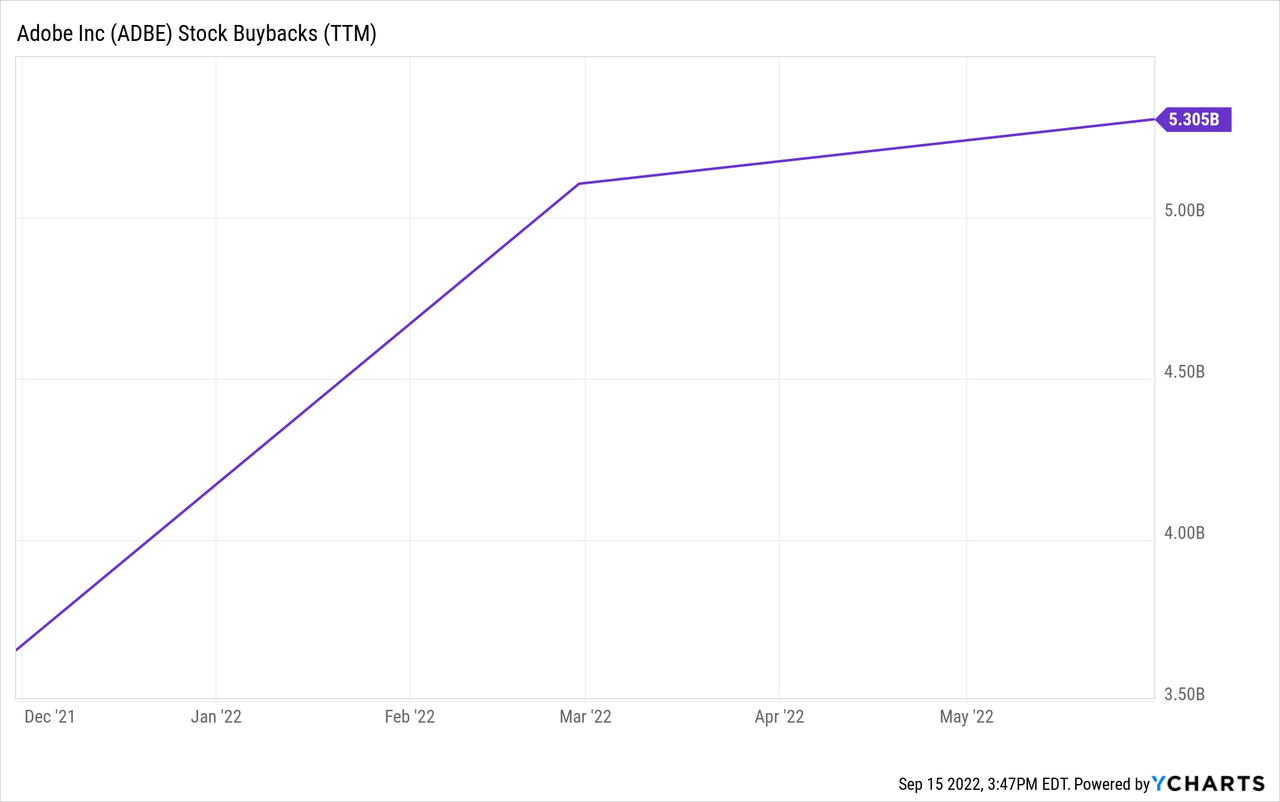

The impact was so bad that GAAP earnings were down 5% year over year($2.42 vs $2.52) per share. This is despite a monumental effort by the company to reduce shares outstanding. Adobe’s buying spree throughout the year reduced shares outstanding by about 8 million, and yet earnings per share declined. But wait, did the headlines not report growth in earnings per share?

That is true. We have all been brainwashed into looking for the Non-GAAP number, so yes that one was up. That would be like your doctor telling you that your cardiac health was up if we adjusted for the fact that you ate enough steak to put cows on the endangered species list. So if we ignore the 79 cents of stock based compensation in the quarter, we did get growth.

Adobe Results Press Release

But ignoring that stock based compensation number is plain wrong. ADBE is spending over $1.4 billion a year just to offset that dilution. You don’t see it as the total buyback is far higher and share counts actually move down year over year. But that is an expense and investors should ignore any analyst that throws in the Non-GAAP number as a way to call Adobe cheap.

Valuation

Adobe trades at close to 32X GAAP earnings. Price to sales has changed from the 13.23X we showed in our last coverage and now is under 9.0X.

Our outlook calls for a sharp drop in margins, some of which we saw this quarter, but has yet to reflect in the Y-Charts above. As to how far it gets is unknown, but we think technology sector is likely to experience continuing headwinds from rapidly rising labor costs and falling demand as the economy retrenches. This is exacerbated by an incredibly strong US dollar. In that environment the upper end of what anyone should pay would be 5X sales. That works out to close to a $100 billion market capitalization on a standalone basis for 2023 revenues of $19-20 billion.

So we have about another 30% drop, conservatively, based on that. Unfortunately, things are not just that bad…

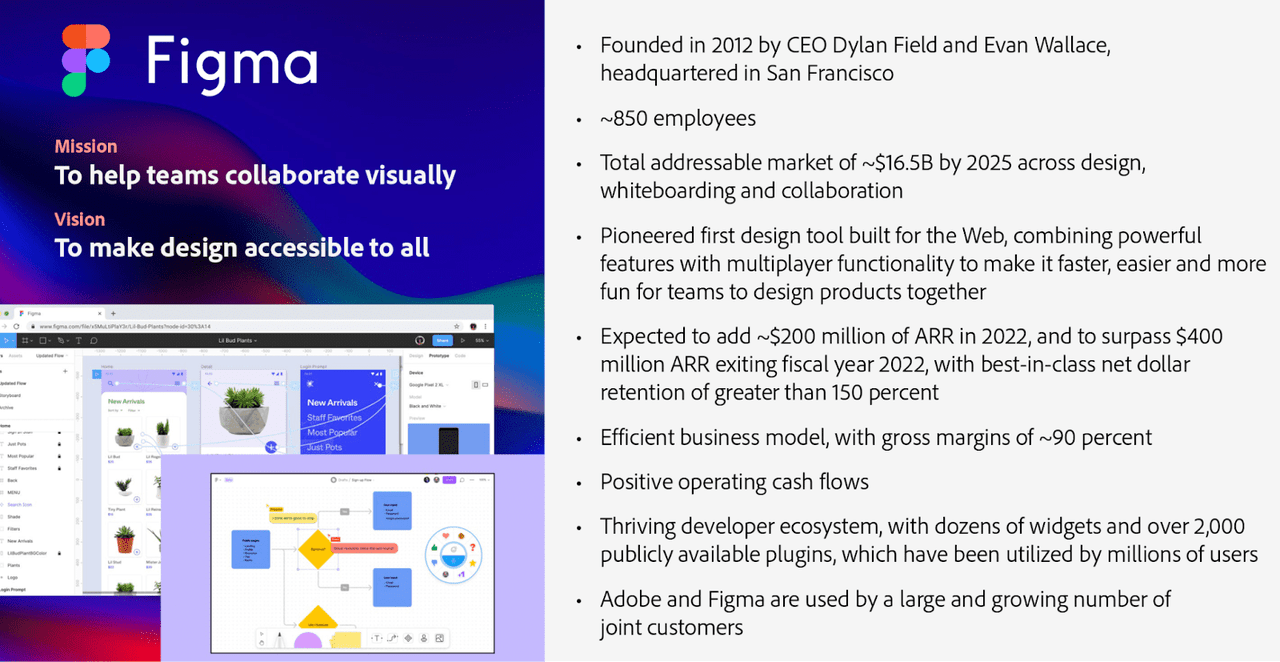

FIGMA

You tend to see this kind of silliness at the peak of the bubble, not when it is half way through imploding. Nonetheless, ADBE decided that there was no better time than to buy FIGMA, a competitor, for $20 billion. The stunning price here shows just how desperate ADBE was for growth. Half of the amount was in cash and the other half in ADBE stock.

That same stock that ADBE spent $5.33 buying back at all prices north of here, was being issued. Actually twice as much as that.

Despite a zero hurdle rate for the cash portion of the deal, and the extremely high multiple ADBE’s own stock trades at, the deal would be dilutive in both years 1 and 2. In fact we guarantee that this will see a gigantic deal related goodwill write-down within 2 years. ADBE just paid 50X sales at the worst possible time.

Adobe Presentation

Verdict

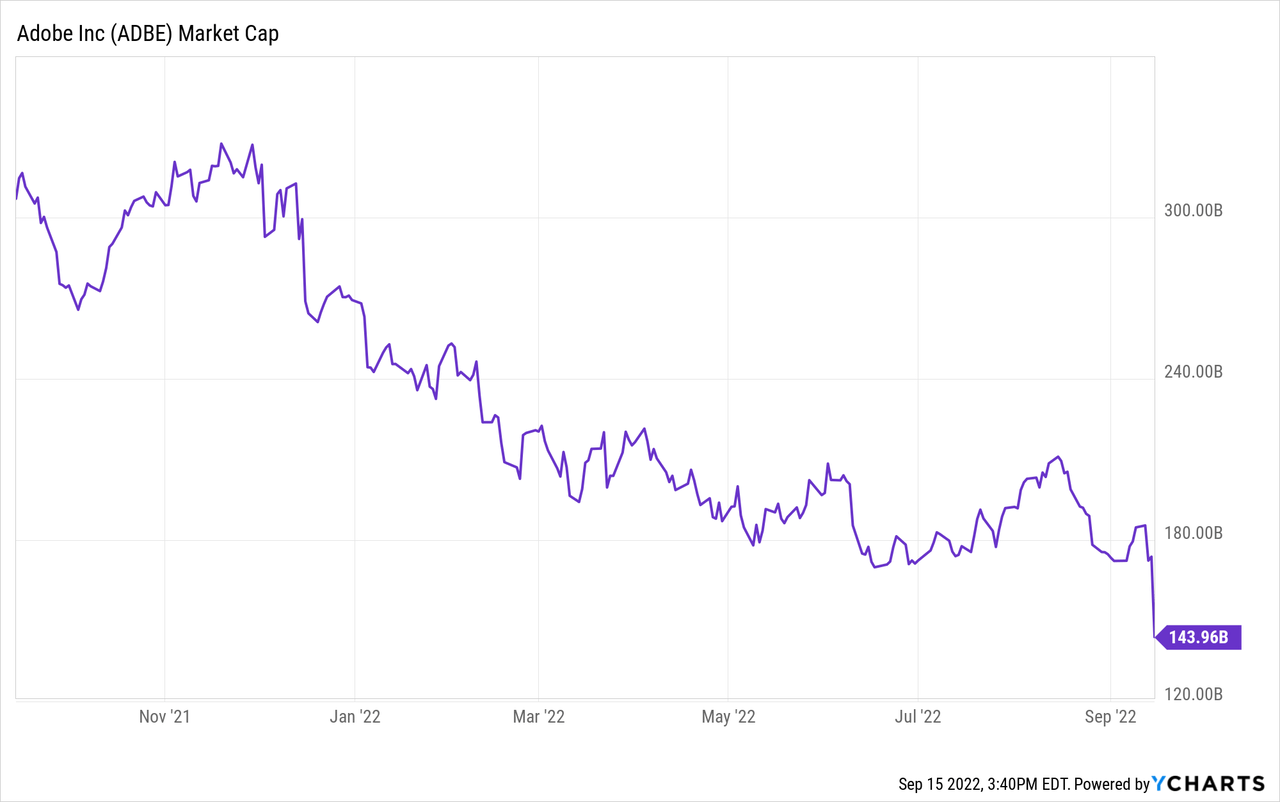

Perhaps a sign of the times that a stock can drop more than 50% off the highs and still trade at over 30X GAAP earnings. NVDA, which we mentioned earlier, is down 70% and still trades at over 45X GAAP earnings. These numbers are insane, to put it bluntly. Keep in mind that overvaluation extremes lead to undervaluation extremes. So whatever you think is fair value, cut that down by 20-40% before you think these get buyable. That drop from 13X to 9X revenues was 50% of the journey. So we are halfway there, and Adobe is still livin’ on a prayer.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment