Sports fans, where you at? If you’re like me, you’ve been in need of a competitive fix, and I have found mine most recently in Call of Duty: Warzone. This Activision (ATVI) title is taking the Battle Royale world by storm, so what better time than now to take a look at Activision Blizzard from an investment point of view?

Activision Blizzard and its consortium of video game brands are well-positioned to take on the up and coming Esports market. With World of Warcraft as a steady source of recurring revenue in its back pocket, the future looks quite bright.

Already Having Success in Esports

Activision Blizzard already sees great success across its brands, particularly when it comes to Esports. Overwatch has a highly watched professional league where the winner can take home $1.5M, and the StarCraft II World Championships sent the 2019 winner home with $700,000.

These high dollar winnings and an easy barrier to entry for young players are making Esports the dream of many. With traditional sports temporarily banned in the west, it may become a dream of many more who are turning to indoor activities.

Then there’s Activision’s golden child, Call of Duty. The first-person-shooter was first released in 2003 and has seen 16 releases since then. Breaking sales records almost every year, Call of Duty truly is a cultural phenomenon.

In February 2019, Activision announced the Call of Duty League. The league would follow in Overwatch’s path and have city-based teams, much like a traditional sports league. Players are guaranteed a minimum salary of $50,000, and there’s a $25M price tag to get a team into the league. While it may not be mainstream yet, Activision Blizzard is starting to capitalize on Esports.

Unfortunately, COVID-19 did put a bit of a damper on the league, forcing games to be postponed. Activision did say that they are exploring ways to get the games online and continue playing that way. Honestly, they should get this done sooner rather than later. If they can capitalize more on this lack of traditional sports, the future may end up being much brighter.

Video Game Interest Is Booming

While the current macro conditions are less than ideal, video games, and Activision Blizzard, stand to benefit. As most of the western world went on lockdown, Activision’s target audience became trapped at home with much more time to spend playing and watching video games.

{kind=link}

Call of Duty: Warzone, released on March 10th, fell perfectly in that window and was offered to gamers free of charge (similar to competing games in the Battle Royale genre). The timing of this release and the lack of cost associated with it allowed the game to jump to the top of streaming charts.

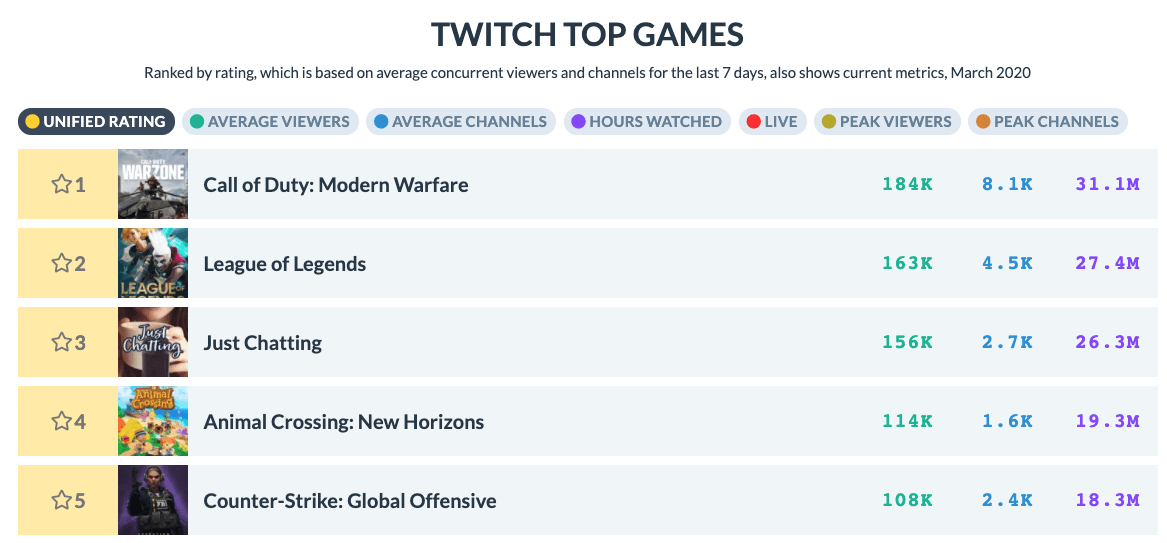

Image: Top games per TwitchTracker

Image: Top games per TwitchTracker

Checking Twitch at the time of writing (early evening) shows 350,000 streamers watching this game alone. The game as a whole does, however, fall short of peers on the number of followers on Twitch, but we are in the very early days yet (Call of Duty: 2.5M, Apex Legends: 7.9M, Fortnite: 54M).

Despite only being available for roughly three weeks, Warzone has already had a handful of high-dollar tournaments put on by the community. Internet personality Keemstar has started a $20,000 weekly tournament, Warzone Wednesdays featuring many of gaming’s biggest names including Ninja and NickMercs. This type of early interest is a fantastic sign that Activision has hit the jackpot with its landing in the Battle Royale genre.

Slowing Revenues, But Many Catalysts On The Horizon

Video game sales have now dropped for seven straight months. This is on the back of few significant software releases and a console refresh on the horizon. I should say, however, that I think we’ll see an up month on our next report thanks to an increase in quarantine related sales.

This overall slowdown in the video game market and some lackluster reporting from Activision Blizzard has resulted in pretty poor performance from the stock over the last 18-months. At its peak, Activision Blizzard traded at just over $83 a share. Today, it can be bought for 40% less than that high point.

So, how about those catalysts? Well, we’ve already discussed Esports, something I think will continue to grow over time for Activision Blizzard. I would also expect that the company forms its own Warzone tournaments or leagues once the mode is out of beta, which would be another boon for the company, especially if they could involve the community in some way (think Pros vs. Joes).

A second potentially much larger catalyst to software sales is the console refresh. Sony (SNE) will release the PlayStation 5, and Microsoft (MSFT) will release the Xbox Series X this fall. New hardware means new software, and fans looking to pick up the latest titles in well-known franchises like Call of Duty, Overwatch, or perhaps even a Tony Hawk Pro Skater 6 (hey, one can dream).

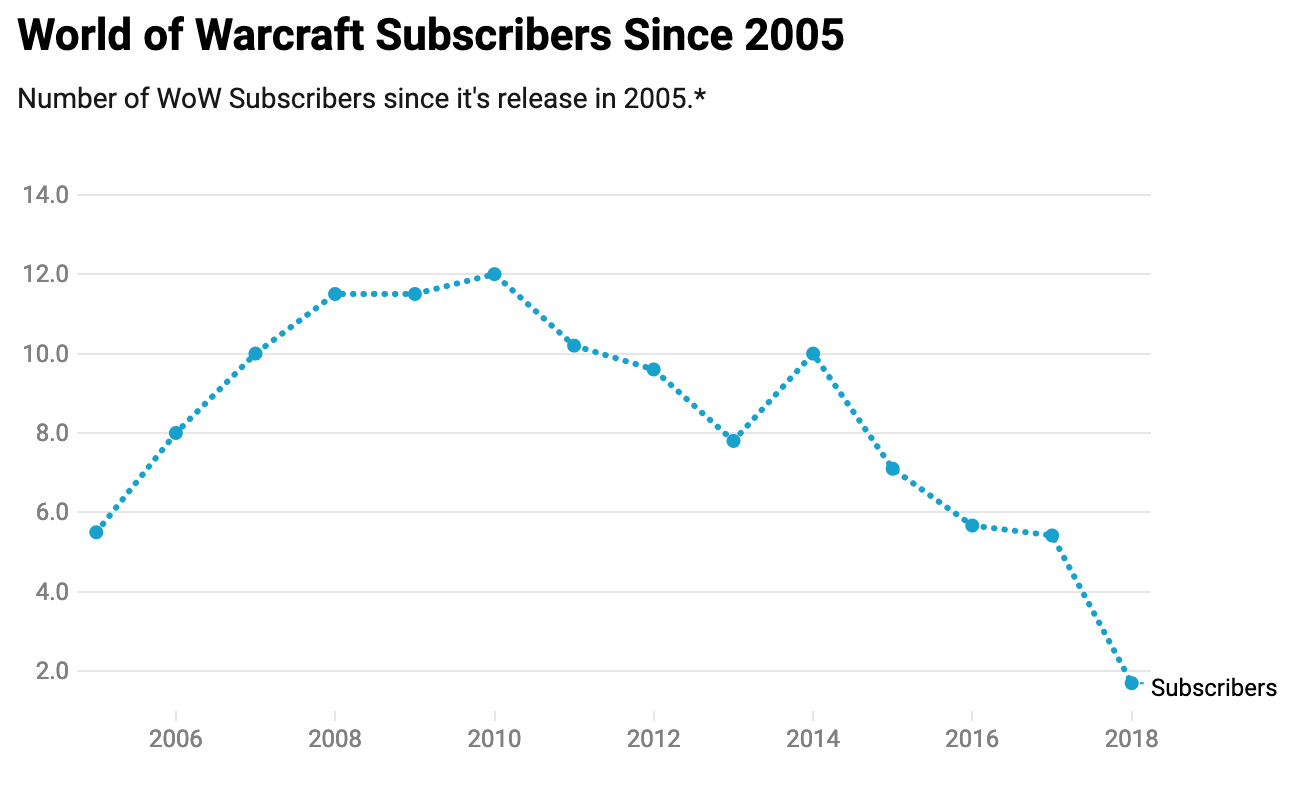

Then there’s World of Warcraft, the much-ignored cash cow at Activision Blizzard. During its heyday, WoW had 12M subscribers paying $15 per month to play. Over time, those numbers have steadily dwindled to the point that the company no longer shares a true count. Things might be getting back on a better track, however, as Newsweek, via SuperData, reports that Blizzard’s release of World of Warcraft classic saw the game grow subscribers by 223%. Without a starting number, that figure is entirely meaningless, but the consensus among those that play and track the game is that there were roughly 2M subscribers before WoW Classic being released.

Image: Estimated WoW Subscribers

World of Warcraft updates and expansions do tend to pull in new players, so an increase of 2M players will give Activision Blizzard a nice chunk of change to play around with and use to develop WoW expansions further. Speaking of expansions, World of Warcraft: Shadowlands will be released sometime this fall.

An Ever-changing Market May Be The Downfall

It is incredibly difficult to build and maintain a video game franchise, but Activision Blizzard has managed to do it numerous times. That said, the company’s most significant risk is that subsequent releases do not match competitors in terms of playability or quality.

Call of Duty: Warzone may be a hit today, but will it stand the test of time? Having played the game and its current competitors, I think so. It is fun, it has an err of realism, and the community appears to be backing it. With frequent updates to the title, Activision does seem to be listening to the community and giving them what they want in the game.

A similar point can be said about any of Activision Blizzard’s major games, which is why the diversity of offerings the company has is so important. Overwatch, for example, has a significant competitor on the horizon from Riot Games, a subsidiary of Tencent (OTCPK:TCEHY)(OTCPK:TCTZF). VALORANT, which will be released in 2020, is a 5v5 character-based FPS, much like Overwatch. This highly anticipated game will, no doubt, spawn leagues and tournaments.

Activision Blizzard’s backing of sports leagues gives them a significant advantage against insurgents. The Overwatch League, much like the Call of Duty League, provide these games with an elevated stature. There are teams of players committed to playing these games because of contacts that come with secure salaries and the potential for six-figure bonuses. Newcomers like VALORANT would have to offer significantly more to draw professional players away from their current game of choice.

Valuing Activision

Activision Blizzard trades at a premium to competitors today, but their place within the industry warrants it. Games like World of Warcraft offer several hundred million dollars in annual recurring income, and yearly franchises like Call of Duty are all but guaranteed to generate a billion dollars in sales per year.

While the leagues, at this time, are hard to value, I think they stand to see a big boost in viewership if they can capitalize on the lack of traditional sports at this time. At this time, I would consider the leagues auxiliary, and not value them, but instead consider them a huge margin of safety and a future “moonshot” project. Instead, let’s value what we do know.

We know that World of Warcraft saw a significant boost in users. We know that the game also has an expansion coming out this, and expansions keep players around. At $15/month, World of Warcraft will bring in, at least, $700M this year (1.7M estimated subs + 223% increase at $15/month allowing for significant churn). New games on consoles later in the year and a COVID-19 quarantine sales boost will, in my opinion, bring Activision Blizzard back up to the $7B in sales they had in FY2017.

Call of Duty: Warzone, despite being free, offers the company a high-margin income stream. With the game being so new, we do not yet know how it is performing, but we do have data on how Apex Legend’s performed in a similar situation. The EA (EA) title brought in $150M during its first month and continues to bring in $45M a month sometime later. Fortnite, a similar Battle Royale title made $1.8B in 2019, which would be a dream come true for Activision Blizzard shareholders if CoD: Warzone could emulate.

Being conservative, I estimate this new game brings in $50M per month over the next nine months of the year for a total of $450M in revenue, leaving my full-year Activision revenue at $7.45B.

Incremental World of Warcraft subscription revenue and a slight bump from Warzone in-game purchases should help give the net margin a little bump. The margin was 23.1% last year, but I think we conservatively see 23.5% this year. At 23.5%, the company will bring in $1.75B of net income. If there are significant price drops on big market down days, I’ll be picking up this stock for the long-term.

$1.75B means the company is trading today at 23x forward earnings and is thus, trading right around fair value.

I do consider Esports to be “valueless” today, but I think that it offers a significant hedge against a bad game or two for investors. If the company can develop a successful league out of one of their major brands, the sky is truly the limit, and that’s why I am bullish on this company.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in EA over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment