PM Images/DigitalVision via Getty Images

Thesis

Aberdeen Income Credit Strategies Fund (NYSE:ACP) is a fixed income closed end fund. We have covered this fund before here and here, and our last piece was outlining how the fund could generate 30% returns over two years, if investors were comfortable with volatility. The CEF focuses on the riskiest components in the high yield space, namely CCC credits. As credit spreads and rates went up in 2022, all-in yields for CCC credits became extremely attractive. When you add leverage on top (as ACP does), you are guaranteed very high cash flows as long as default rates do not pick up substantially.

Recently we have seen a major downshift in investor expectations for rates to be higher for longer, with many market participants now expecting a Fed pivot. This has translated into a significant risk rally, especially for very duration sensitive securities such as tech equities and credit sensitive instruments such as CCC bonds. To that end ACP is now up an astounding 27% since October! That is a massive move that should not be taken in stride. Furthermore the CEF is now trading at a 7% premium to NAV, after selling at a discount during the risk-off move in October. We believe the market is now pricing in a Fed pivot, similar to the Fed Funds futures market where participants are seeing two rate cuts this year. A Fed pivot is positive for very risky assets, hence the massive rally in ACP.

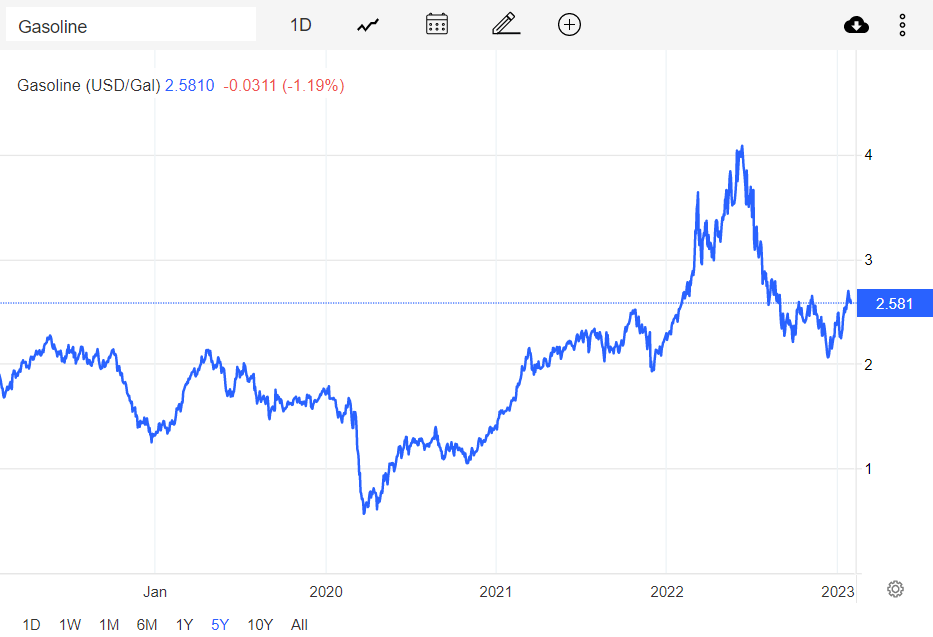

We are of the opinion that inflation is going to be much stickier than initially though, and the Fed will keep rates higher for longer to stamp out any inflationary pressures. While the bulk of rate hikes are behind us, we do not see any rate cuts in 2023. The market is not pricing that in, and ACP has front-run too much in our opinion the yield curve. Let us just have a look at gasoline prices:

Gasoline Prices (Trading Economics)

After a significant fall after hitting $4/gallon last year, gasoline is starting to climb back up again. It is up from $2/gallon to $2.5/gallon now. With the China re-opening and the firming up in energy prices, we think inflation is not going to disappear as fast as market participants think, and the Fed will not lower rates this year in order to avoid at all necessary costs a stagflation.

High rates for longer translate into slightly wider credit spreads from here for CCC bonds, and a flat market price versus NAV for ACP. We think the CEF has gone up too fast and it would be prudent to cut some exposure here after the significant rally in the share price.

Performance

ACP is up an astounding 27% since October:

Total Return (Seeking Alpha)

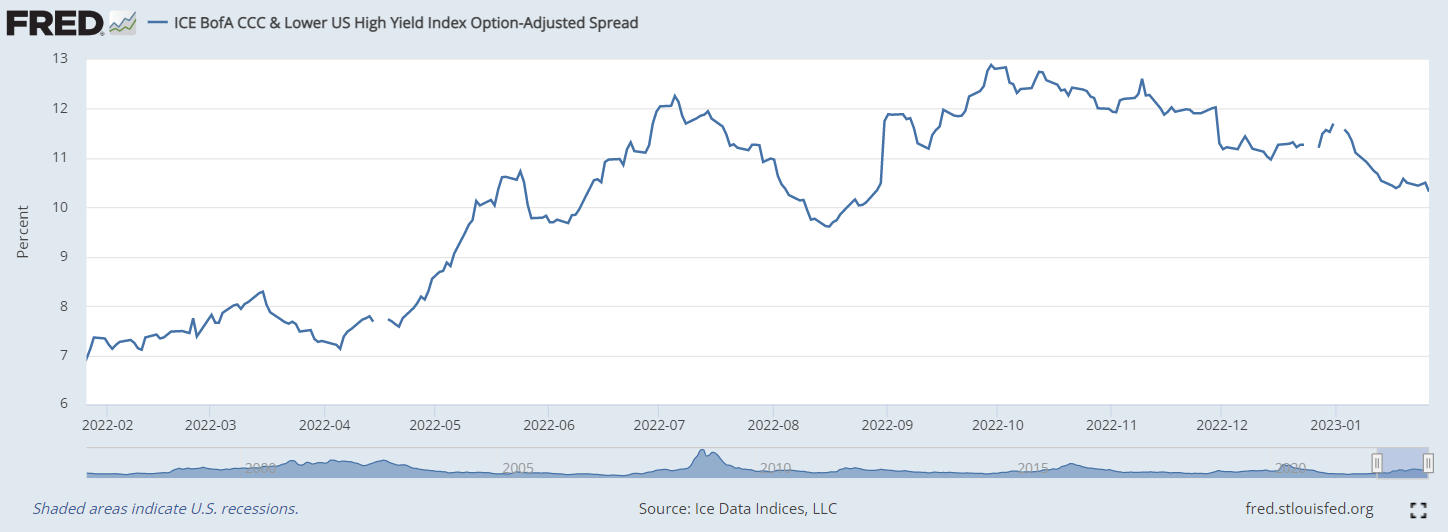

The fund is a high beta vehicle and has shot up as credit spreads have tightened:

CCC Spreads (The Fed)

We can see from the graph above, courtesy of the Fed, how CCC credit spreads have tightened from around 13% to almost 10% now. That is a pretty significant move, and not in line with the expected recession.

Premium / Discount to NAV

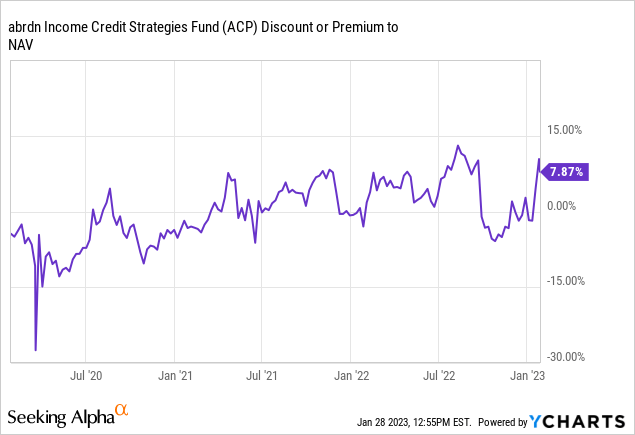

The fund is now trading at a premium to NAV:

We can see how the CEF has a nice range of -5% to +10% for its premium/discount to NAV in the past three years. During the September/October risk-off move the CEF started trading with a discount to NAV. It has now switched to a premium. This level is not sustainable unless the Fed does indicate it will pivot. We do not find that likely.

Conclusion

ACP is a fixed income CEF. The fund focuses on the riskiest corner of the high yield market, namely CCC credits. CCC spreads have tightened substantially during the latest market risk-on rally. The move has been driven by an implied Fed pivot in 2023, and has seen ACP move up 27% since October. The move has been driven by NAV as well as the fund now trading at a 7% premium versus a discount before. We feel inflation is going to be stickier than forecasted and rates are going to be higher for longer with no Fed pivot this year. ACP is now discounting too many good news and we feel a savvy investor would be well served to take some profits here.

Be the first to comment