LeonU

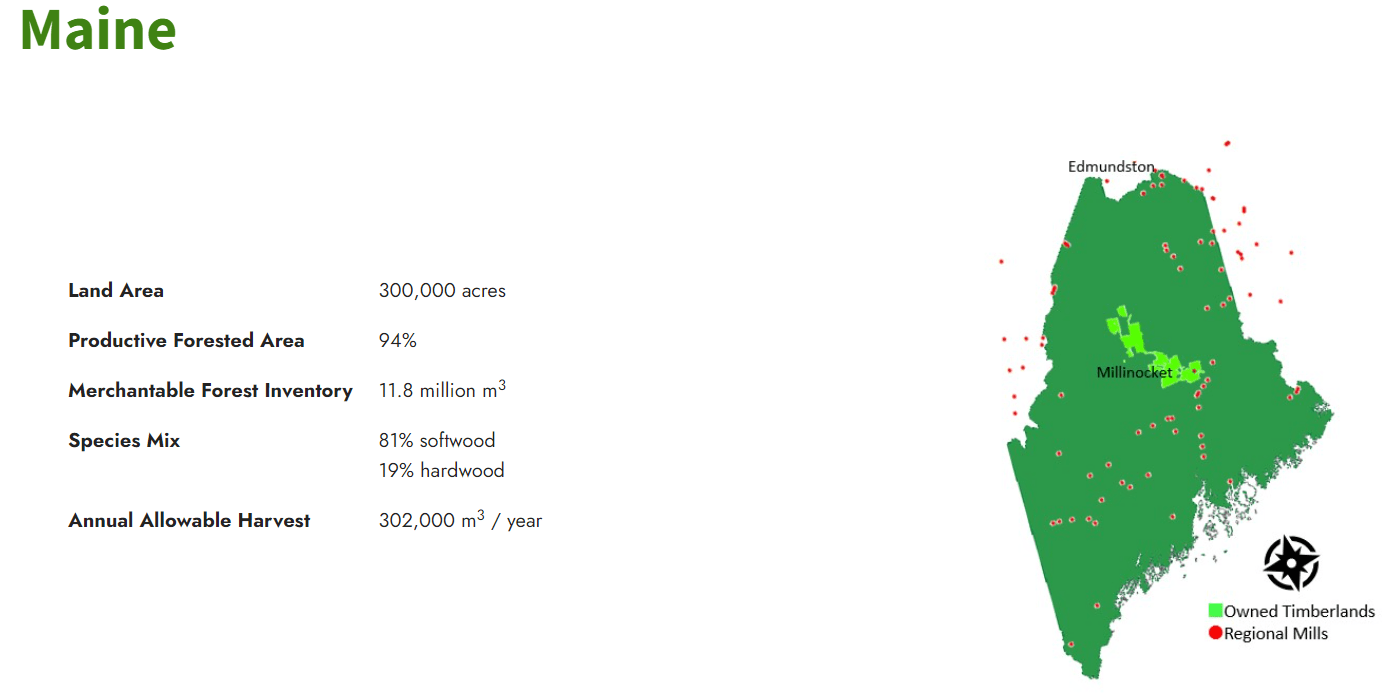

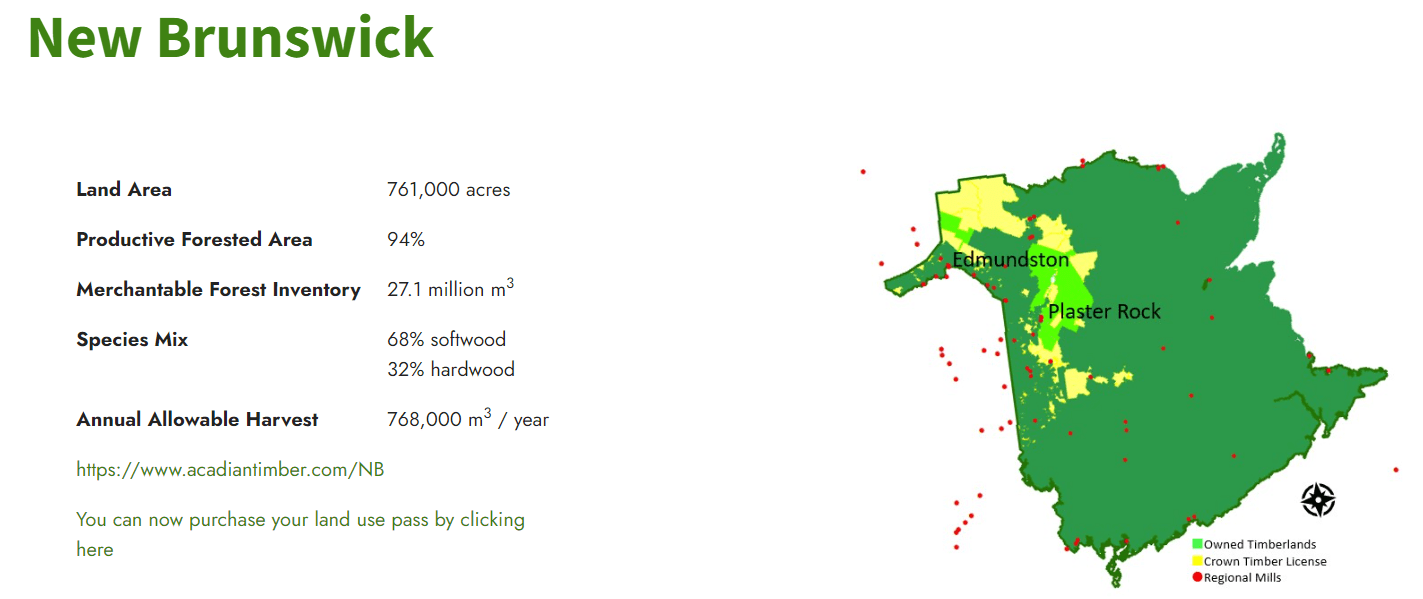

Acadian Timber Corp. (OTCPK:ACAZF) is a Canadian forest products supplier and engages its activities with two segments: Maine Timberlands (Fig. 1) and New Brunswick Timberlands (Fig. 2), managing approximately 1.1 million acres of land. Its product offering serves almost 90 regional clients and includes biomass by-products, pulpwood, hardwood & softwood sawlogs. In addition, the company also oversees 1.32 million acres of Crown licensed timberlands in the New Brunswick area.

Maine area and proximity to regional mills (Fig.1) (Acadian Timber Corp. Corporate Website) New Brunswick area and proximity to regional mills (Fig.2) (Acadian Timber Corp. Corporate Website)

To sum up Mare Evidence Lab’s investment thesis, we could say that the company is benefitting from a niche local exposure in a dynamic market with upside related to 1) carbon considerations and 2) stumpage rates (we should also include biomass value). Why are we confident? Here at the Lab, we are not focusing on the quarterly results (and today we are not providing comments on the Q2 company performance), whereas we are looking at the broader picture, focusing on two long-term values.

Carbon Credits

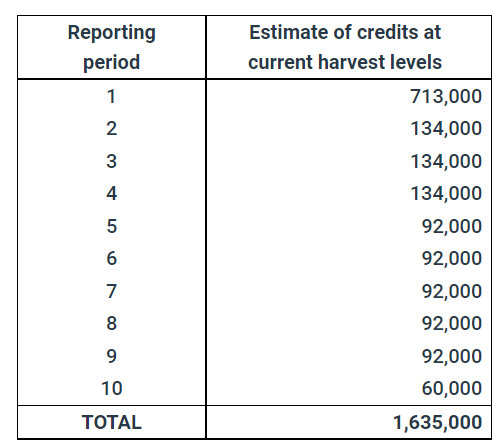

Starting from the carbon credits, they are now something real. It was a project that started in 2021 and now, Acadian is set to develop voluntary carbon credits to balance forest growth and harvest requirements. Financially speaking, the company released its project update communicating that it expects to collect “approximately 84% of gross revenues from any sale of carbon credits“. This model below represents an estimated carbon credit volumes for the next ten years:

Preliminary Credit Volumes (Global Newswire)

Price Increase Based on Higher New Brunswick Stumpage Rates

Related to our point 2), during the Q&A call with the investor community, it is vital to report some CEO’s words:

“We’re seeing some good price increases, obviously, with softwood sawlogs. As we’ve always said, demand will drive a fair bit of this, but with the stumpage rates coming up? I’m not sure we’re going to be able to capture it all, but we’re sure hoping to capture a lot of it in the same quarters“. Explaining also: “it has this sort of taking a little bit of a progressive stance where Congress rates will come up and then we’ll start to see, I suspect the prices for not only probably lots, but also for us to go up as well. So, we’re thinking, in the next few quarters, we’re going to start seeing prices increase due to the royalty rates going up“.

According to our research, higher rates in stumpage will translate into higher revenue figures for Acadian Timber Corp, positioning it to benefit over the medium-long term horizon.

Conclusion and Valuation

Cross-checking Q2 performance, Acadian reported numbers below Wall Street consensus estimates missing on volumes and EBITDA levels. However, unlike in the past, the Canadian company seems to benefit from supportive regulation and from carbon credits outcome. These positive circumstances coupled with a low stock price performance help us remain positive on Acadian Timber Corp’s valuation. Looking to the released Q2 results, we now forecast an EPS of CAD 1.02 and 1.1 respectively for 2022 and 2023(E), using a historical P/E multiple of 16.5x, we derive a target price of CAD 18 per share, implying a 9% upside from the current stock price. The 2023 implied dividend yield is set at 6.5% versus a Timber REIT average of 4.7%, so this likely provides a margin of safety that we are always looking for when we initiate new coverage with a buy rating. Risks to our buy rating include Canada and US house market weakness, interest rate development, FX, duties by the US, natural catastrophe, infestations & disease, and hardwood & softwood price dynamics.

Be the first to comment