JohnFScott/E+ via Getty Images

Main Thesis And Background

The purpose of this article is to provide a broad review of 2022 – what went right, what went wrong, and some lessons learned. This was not entirely a year to forget. On the contrary, a lot of great things happened in my personal life. My wife and I bought a new house in the mountains, my twin brother made me an uncle, I resumed national tennis competitions, and I finally returned to my office after an almost two year hiatus from my company’s Charlotte headquarters.

Despite these positives, my investment portfolio was another matter! Yes, there were bright spots, but my domestic holdings and foreign ETFs were hit hard overall. Some timely purchases were made, but it was not enough to overcome the broader slide in equity markets – the S&P 500 especially. While we never want to “lose” on our investments, doing so often provides learning opportunities. This is a simple reality but one that can be overlooked. Whether in school, athletics, investment, or other parts of life, we should learn the most from our missteps. With this focus, I will recap some of the important takeaways from this past year that will hopefully make myself and others better investors in the future.

Leverage Should Not Be Taken Lightly

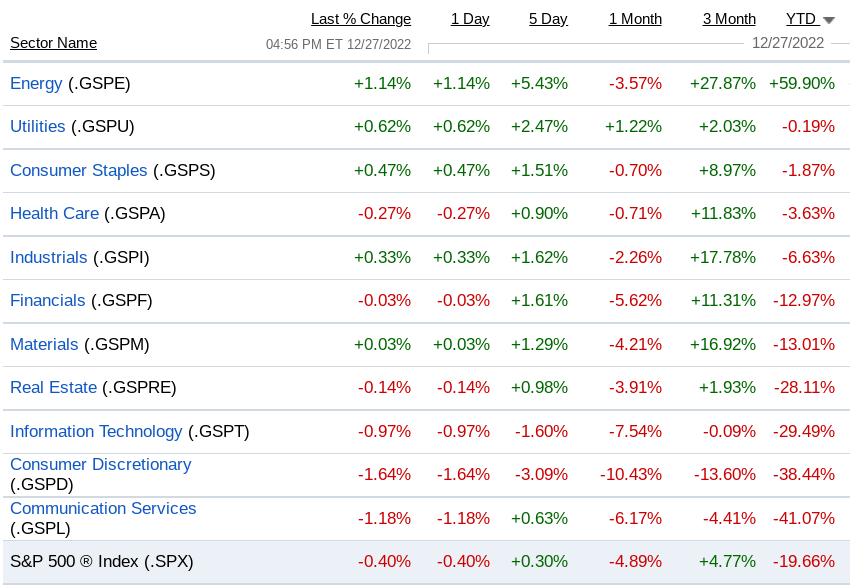

We the exception of Energy, most sectors across the S&P 500 didn’t have a very good year. Utilities held its own with a flat return and it is worth noting that defensive areas like Consumer Staples, Health Care, and Industrials only saw single digit losses:

Sector Performance (YTD) (Fidelity)

I’m sure it does not come as a surprise to readers that most of the market finished (or will finish) in the red this year. So losses are expected, and we have to accept this is a potential reality for investors with every new year. Further, it was not just U.S. indices that fell victim to inflation, geo-political tensions / war in Ukraine, and a continuing pandemic. The major economies in Europe and Asia will also see the indices that track market performance finish in negative territory.

But losses in the single digits, or even in the teens, is not what keeps investors up at night. Heavy losses, bear markets, and declines that show little sign of abating are what do. Unfortunately for those with a bullish take at the start of the year that worst case scenario could have become a reality. For example, if one was to take an amplified approach to the market in January, they would likely be nursing some very big losses as we wrap up December. This puts them in the position of tax harvesting at a potentially inopportune time or holding positions deep in the red that are an eyesore each time they look at their portfolio.

What I am referring to here as leverage. This can come in many forms. It could mean using margin in one’s investment account to buy more equity exposure than they could afford with just cash on hand. Or it could mean buying in to leveraged ETFs or CEFs that are managed by firms to borrow on an investor’s behalf to give larger exposure than an unleveraged/passive fund would. This use of borrowing can be pricey but often worth it during good times (or bad times for inverse funds!). The idea being that a fund’s borrowing costs should be dwarfed by the extra return earned through the leveraged assets, generating excess profit than would otherwise be earned.

The problem with this strategy is that when things go bad – they go bad in a big way. This was the case with leveraged positions in 2022 across the board. Whether it was U.S. equities, foreign equities, or debt and muni funds, leverage cost investors big time this year. To illustrate this point, I will highlight a few popular options that span the investment spectrum. Representing domestic equities there is the ProShares Ultra S&P 500 ETF (SSO), for corporate and mortgage debt is PIMCO Corporate & Income Opportunity Fund (PTY), for munis the Nuveen AMT-Free Quality Municipal Income Fund (NEA), for the Technology sector the ProShares UltraPro QQQ ETF (TQQQ), and for developed foreign equities I choose the Aberdeen Australia Equity Fund (IAF). These funds all have vastly different objectives but what they have in common is their heavy use of leverage and, as a result, heavy losses in 2022:

YTD Performance (Google Finance)

What is the common theme here? Losses, lots of losses. For leveraged plays the year was a brutal one and due to the nature of compounding losses it may take a very long time (if at all) for investors to recover their positions (if we assume one was initiated in January). Take, for instance, the 3X leveraged TQQQ – which returns three times what the NASDAQ offers on a given day. When losses stretch across days and weeks consistently the fund simply gets pummeled and the share price drops to a level that even if the underlying index doubles from here investors will not be able to recoup what they lost.

This is an inherent risk to these investments that may make them unsuitable as long-term holds. It is especially true for retail investors and/or others that cannot exit positions quickly. The takeaway for me and lesson learned here is we have to remember that bad times happen and leverage is not always appropriate. When times are great and markets are rising everyone who uses leverage looks like a genius. But without contemplating what can happen when things go wrong it may wind up making you a bag holder nursing unsustainable losses.

This year proves a lesson that even quality assets like investment grade municipal bonds or large-cap U.S. companies can suffer large drawdowns and that leveraged plays on those spaces means a major drag on portfolio performance. While my outlook is brighter for 2023, this should be a stark reminder to stay within one’s tolerance and approach any type of leverage with extreme caution.

The World’s Problems Are Our Problems

Another key point to consider out of 2022 is that global events continue to have an immediate and often outsized impact on the U.S. and U.S. equity markets. For support, let us consider some of the biggest stories (not considering celebrity gossip!) from this year that impacted stocks domestically. There were too many to list here, but I tried to capture some of the biggest ones:

Russian Invasion of Ukraine (Wall Street Journal) China “Zero Covid” Approach (NY Times) UK Government Changes (Bloomberg) Global Rate Increases (Fitch Ratings) China’s Election Results (The Guardian)

This is just a snapshot of some of the news stories out of this year, but the overriding theme is that they are global in nature. Yet, they all had an impact on U.S. equities, by varying degrees out course.

The conclusion here should be clear. What is going on across the globe is impacting U.S. investors in rapid, perhaps disproportionate ways. This has always been true to an extent, but I personally feel is has been amplified since my investment career began two decades ago because of the speed of information and travel, how spread out supply-chains have become, and how pandemics and natural disasters do not recognize borders.

The lesson learned here is we need to not only follow what is going on outside of the U.S. but understand the implications for our investments. Questions to consider when buying a U.S. company/fund that would help investors understand the risks they actually face:

- How much business does this company conduct overseas?

- Who are their primary customers?

- Where and how do they obtain their raw materials and other inputs?

- What global regulations may impact the revenue stream?

- Are competitors emerging outside the U.S.?

For those who may say this exercise is futile I would suggest that is precisely the point of this piece. We need to learn this lesson and not fall victim to the blinder effect. What is going on in the world absolutely impacts domestic holdings and U.S. companies. A classic example is Apple (AAPL) and their China woes. One might not have predicted that going in to 2022, yet it hurt the company all the same. My hope is that all investors, here and abroad, take more time to contemplate what is going on outside their own borders and bake that in to their investment predictions in both the short and long term.

Oil & Gas Still Drive The World

This lesson may seem obvious to some, but with all the “clean” energy and “ESG” talk coming out of news outlets, corporate boardrooms, and universities, among other places, it could be easy to have fallen trap to the idea that oil and gas companies are no longer investable and are soon to be relics of an era that is passing by. Well, clearly, 2022 proved that oil and gas are here to stay for quite a while and the investment implications are extremely important.

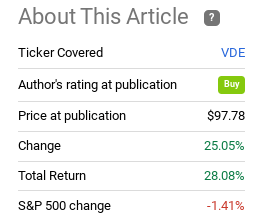

Personally, I saw the impact of global and domestic events as winners for the energy sector. The big drivers of gains in my view this year were the Russian-Ukraine War, a more hostile U.S. administration towards fossil fuels, and a rebound in consumer demand as lockdowns ended. Despite strong gains for energy funds in the first half of the year, I remained bullish on the sector for Q3 and Q4, as I indicated in July. Since then, profits continued to roll in for my preferred Energy holdings, the Vanguard Energy ETF (VDE):

VDE Performance (Seeking Alpha)

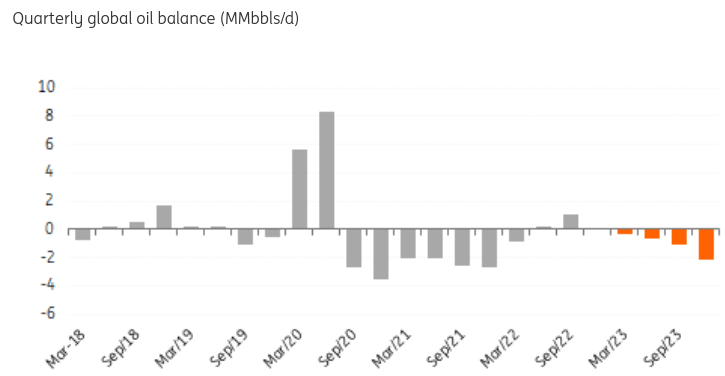

The lesson here is that fundamentally not much has changed in the global energy market. To be fair, the world is attempting to more to more electric, nuclear, and solar energy sources in the hopes of tackling the “cleaner” objective so many profess to want. But the reality on the ground is the world still moves on oil and gas. This change is not going to happen overnight and certainly not in 2023. Continuing to ignore this dynamic may keep investors under-performing next year as they would have this year had they ignored this sector. The global oil market has been under-supplied and that is a trend that is anticipated to continue for the foreseeable future:

Global Oil Supply Balance (EIA)

VDE and other energy funds have been a source of profit and I don’t see that changing just because the calendar reads January. The lesson is to focus on fundamentals, not marketing hype, and keep Energy top of mind going forward.

Inflation Drives The Fed and The Fed Drives Markets

My last lesson is one I should have learned already as someone who entered the workforce during the Great Recession. That is that the Fed – and perhaps more importantly interest rates – are a primary driver of equity returns. This may sound obvious, but after a strong run in 2021 many put their heads in the sand to the upcoming headwind that was Fed rate hiking. The Fed announced their intention well in advance and followed through, but market expectations continued to expect a more dovish policy. The result was panic selling on multiple occasions as the Fed disappointed. The lesson remains consistent since the Fed has taken a more active role in the economy – don’t fight it!

This is a valuable lesson for 2023 because market participants still may not have gotten the message. In Chairman Powell’s December address, he suggested rate hikes would continue in 2023 and that the idea of cutting rates next year is not one he was entertaining. Despite that, the market continues to believe the Fed will begin to reduce its benchmark rate next year:

Fed Futures Curve (Charles Schwab)

This looks to me like the lesson on not fighting the Fed has not been learned by many yet. The Fed has made its intention clear: until inflation is under control, rate hikes will continue and/or a higher than normal rate will be sustained. Inflation may have “peaked”, but it remains well above what Americans are used to:

Inflation Rate (Bureau of Labor Statistics)

What I hope readers will takeaway from this is the Fed will continue to impact equities in a big way in 2023. That means many of the same winners and losers from the current policy are probably going to keep on being winners and losers for the next few months, if not longer. The lesson of not fighting the Fed has been on full display to anyone paying attention this year. Don’t make the mistake of thinking this won’t be relevant in the year ahead.

Bottom-line

I had my share of losses in 2022 and I’m sure I will again in 2023. But I enter the year wiser and more prepared than I did last year because I was dealt a harsh dose of reality along with most investors. I believe the themes I laid out in this piece are well founded and the lessons learned will serve readers to avoid making fundamental errors in the new year. While we never know what the future will hold, we can control how we prepare. I enter 2023 with more cash on hand, a light touch of leverage, and meaningful energy exposure. It is my hope that this discussion will similarly prepare readers for what will hopefully be a fruitful new year for all.

Be the first to comment