halbergman

The superior man understands what is right; the inferior man understands what will sell.”― Confucius

Today we take a deeper look at an asset-lite logistic concern. The stock is down by more than half of macro and other concerns. However, the shares have seen insider buying and the company is executing well. An analysis follows below.

Seeking Alpha

Company Overview:

Headquartered in Greenwich, Connecticut, GXO Logistics, Inc. (NYSE:GXO) is the largest pure-play contract logistics provider in the world, offering warehousing, distribution, and order fulfillment across more than 950 facilities encompassing ~200 million square feet. The company’s chairman, Brad Jacobs, gained control of GXO’s former parent – less-than-truckload shipping, brokerage, and logistics concern XPO, Inc. (XPO) – in 2011, and as with his former successes in oil brokerage, trash hauling, and heavy equipment rentals, grew the business through acquisition. GXO went public when it was spun out of XPO in August 2021, with its first regular-way trade executed at $57 a share. Its stock trades just above $43.00 a share, translating to a market cap of just over $5.1 billion.

November Company Presentation

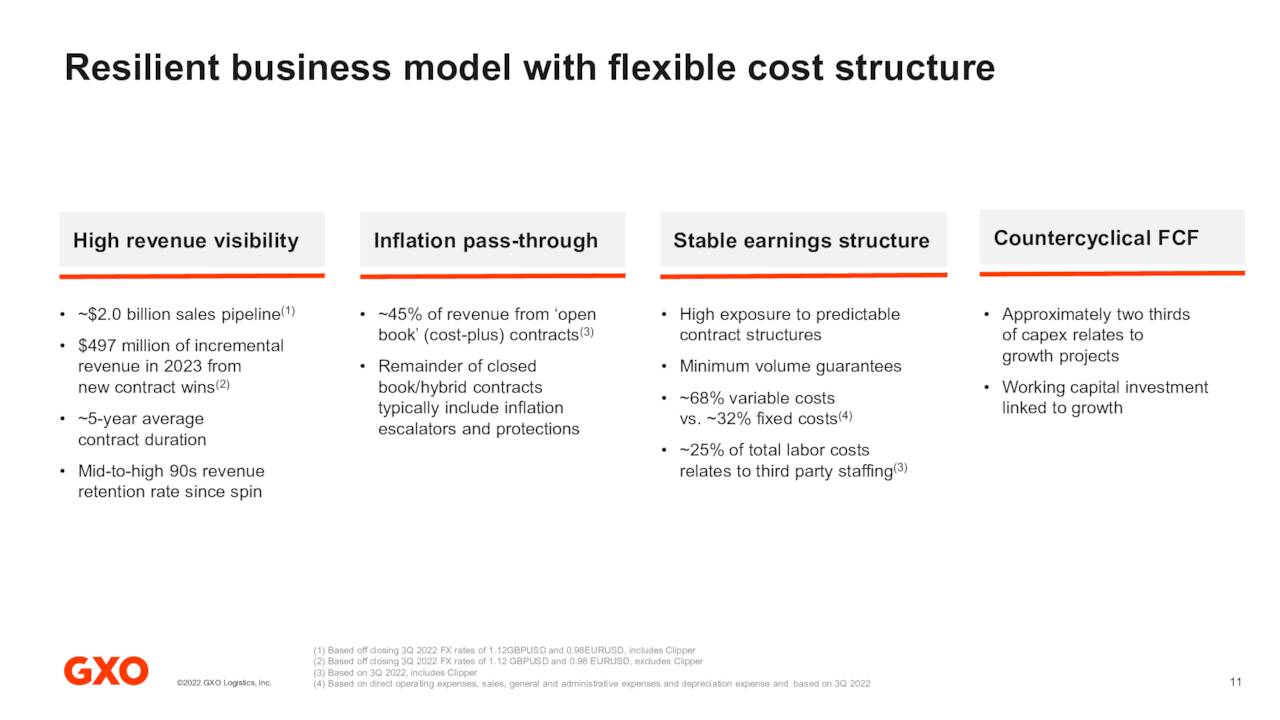

The company operates on an asset-light model, owning only seven of its warehouses. The balance are either leased by GXO or owned or leased by its customers, which comprise top companies in verticals such as omnichannel retail, food & beverage, technology & electronics, industrial & manufacturing, and consumer packaged goods. Its leases typically match multi-year (usually five-to-seven year) customer contracts with inflation pass-throughs and minimum volume guarantees. Capital outlays are concentrated on technology (think robots) to improve labor productivity, warehouse management, inventory management, demand forecasting, and automation. GXO enjoys a revenue retention rate north of 90% with its top 20 relationships averaging 16 years. The company also enjoys little concentration risk with its top five customers accounting for ~17% of its FY21 top line. Even before its recent acquisition of Clipper Logistics – more on that below – the majority of its revenue was derived outside the U.S. (32%), with the UK (36%), Netherlands (8%), France (8%), and Spain (6%) the largest contributors.

GXO is part of a North American and European logistics market valued at ~$130 billion, competing against the likes of Deutsche Post’s (OTCPK:DPSTF) DHL, DSV Panalpina, Kuehne + Nagel (OTCPK:KHNGF), Geodis, and ID Logistics, amongst others.

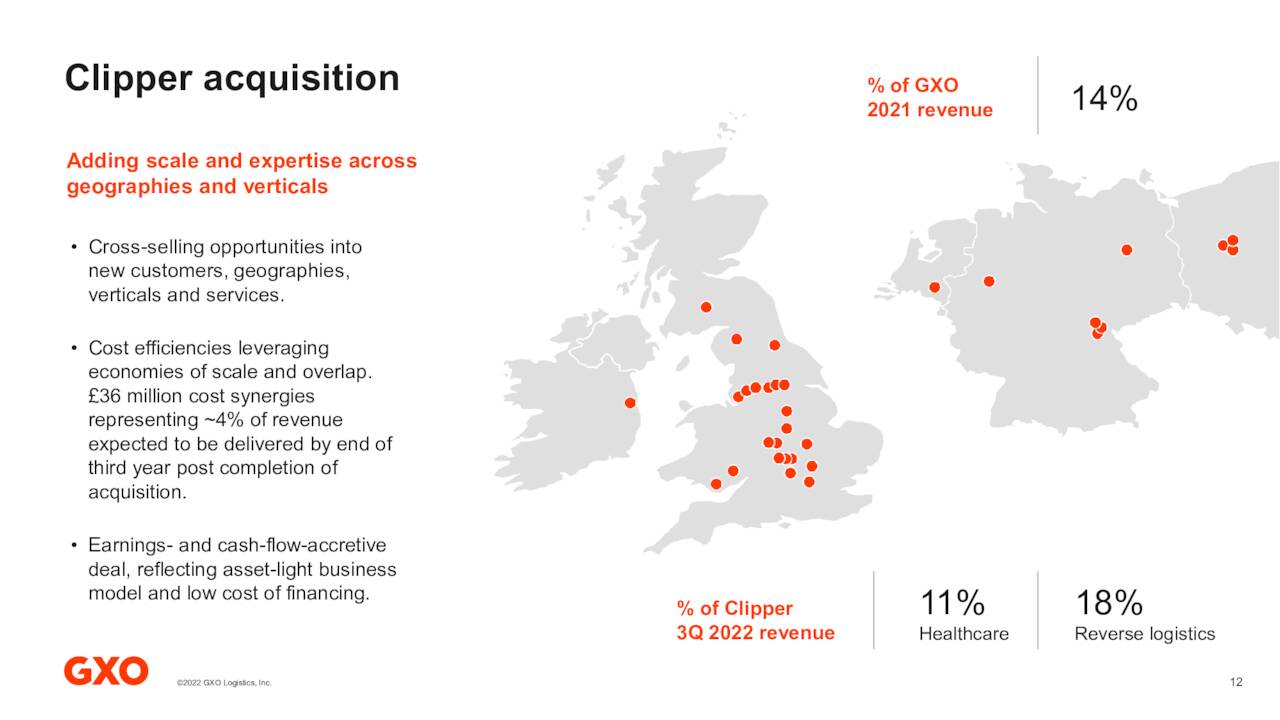

Clipper Logistics Acquisition

With serial acquirer Brad Jacobs as a beneficial owner and chairman – he has purchased over 500 companies in his career – it wasn’t a surprise to see GXO expanding its geographic reach with the acquisition of British omnichannel retail logistics specialist Clipper Logistics, a concern specializing in life sciences, reverse logistics (returns), and repairs. For a total consideration of $1.1 billion ($900 million cash, 3.75 million shares of GXO stock), the company expanded its European presence, opening markets in Germany and Poland, with cost synergies of ~$44 million expected three years post-close.

November Company Presentation

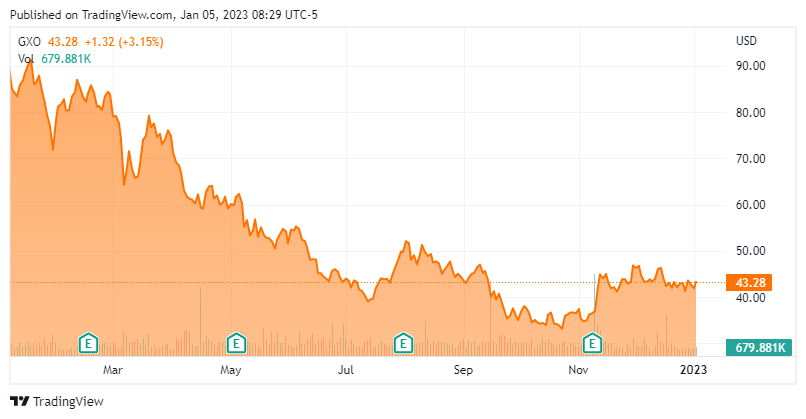

Share Price Performance

Under Jacobs’ stewardship, XPO was one of the best performing stocks during the past decade, up 1,457%. With 50,000 customers worldwide, including 69 of the Fortune 100, the rationale behind the splitting off GXO from XPO was to ‘unlock value’ by creating two significant pure-play companies with distinct investment identities. At the time of the split, the combined market cap of the two concerns was $12.1 billion. Their combined value is now $10.8 billion, or down 11% – comparing unfavorably with the S&P 500, which is off 5% during the same period. GXO has performed worse, with its market cap decreasing 16%. That wasn’t always the case. At one point in mid-November 2021, shares of GXO peaked at $105.92 as the market viewed the worldwide supply chain disruptions driving a secular trend towards outsourcing. However, after 11 months, its stock traded to an intraday low of $32.10 a share in mid-October 2022.

There are several reasons behind this 70% peak-to-trough downdraft. First, GXO is simply perceived as a cyclical stock. More importantly, with the war in Ukraine, the appraisal has been that exceptionally high energy prices in Europe will drive its economy into a much steeper recession versus the U.S. That estimation has acted as a double whammy against GXO, as it is hurt by both its majority exposure to Europe plus the potential for negative currency translations.

3Q22 Earnings & Outlook

Despite the pessimism regarding the macroeconomic backdrop, GXO bested earnings expectations in the two stanzas of 1H22, raising its top-line FY22 outlook after its 2Q22 report on the back of new business wins.

November Company Presentation

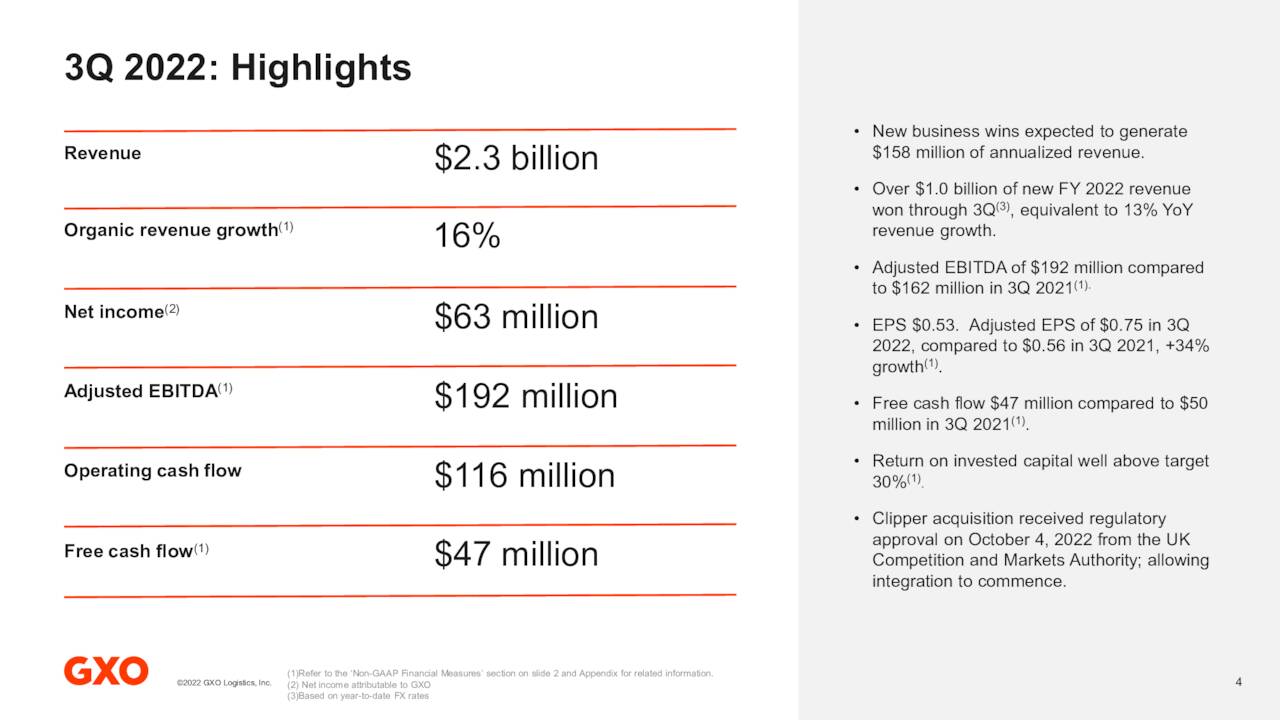

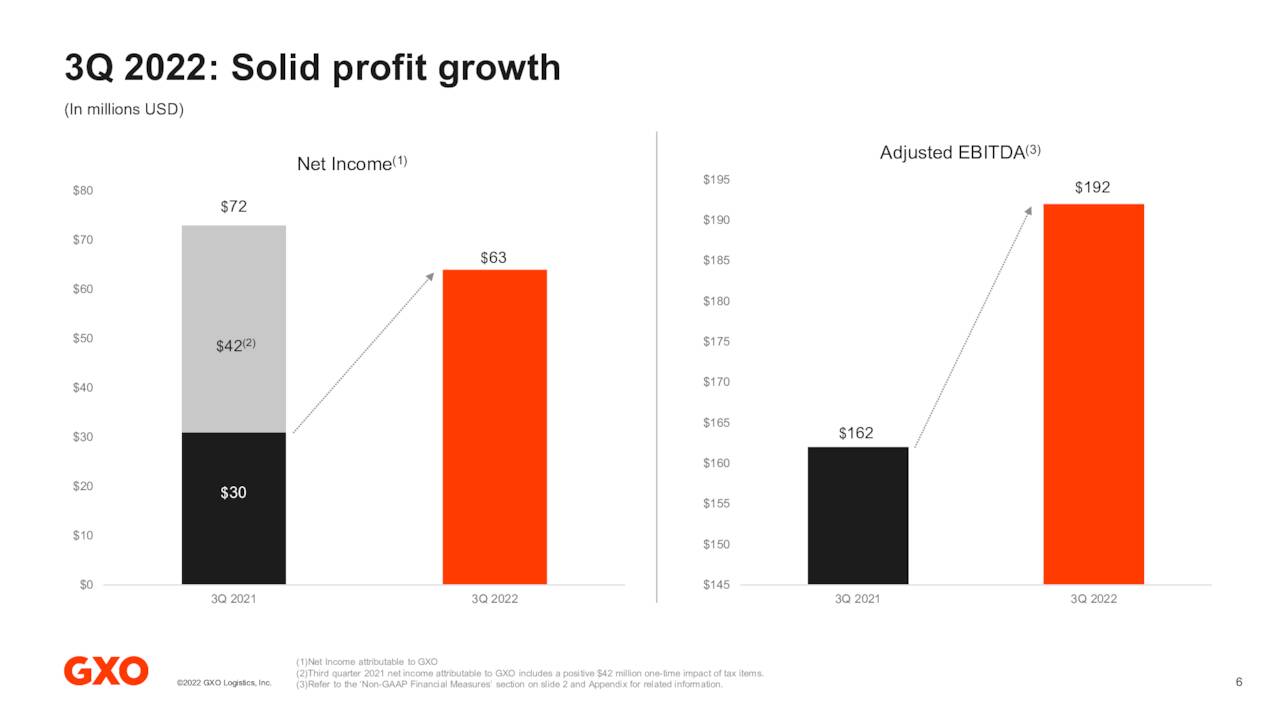

Announced on November 8, 2022, GXO’s 3Q22 was more of the same with the company posting earnings of $0.75 a share (non-GAAP) and Adj. EBITDA of $192 million on revenue of $2.3 billion versus $0.56 a share (non-GAAP) and Adj. EBITDA of $162 million on revenue of $2.0 billion in 3Q21, representing improvements of 34%, 19%, and 16% (16% organic). The bottom line beat Street consensus by $0.05 as the company won new customer contracts in the quarter that are expected to contribute incremental revenue of $158 million in FY23 ($497 million YTD). Revenue retention was characterized as “mid-to-high 90s”.

November Company Presentation

For the first nine months of FY22, non-GAAP earnings improved 49% to $2.02 a share, while revenue increased 15% to $6.5 billion.

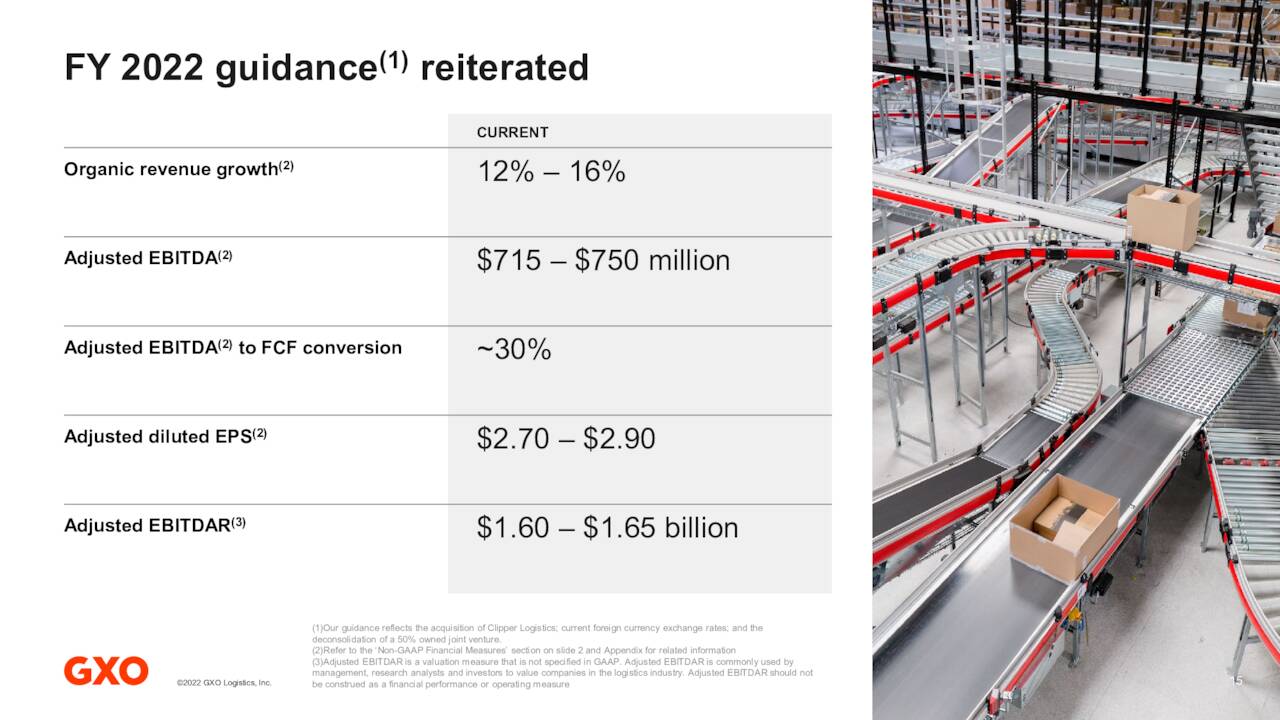

That said, management did not alter its guidance for FY22, which calls for non-GAAP earnings of $2.80 and Adj. EBITDA of $732.5 million on organic revenue growth of 14% (~$9.1 billion) – based on range midpoints – with free cash flow ~30% of Adj. EBITDA. And with all its investment in technology, it expected gross margin to improve 50 basis points year-over-year in 4Q22. The company also expressed confidence regarding FY23, with a new business pipeline of ~$2 billion.

November Company Presentation

The market more or less yawned at these results with the stock up a little more than 1% in the subsequent trading session to $36.99. It did not help that three Street analysts dampened any potential enthusiasm surrounding GXO’s financial report by lowering price targets.

However, an upbeat promotion by Steve Weiss of Short Hill Capital Partners on CNBC – calling shares of GXO, “compellingly cheap” – the following morning (November 10th) pulled the company’s stock out of the doldrums. It rallied 21% over the subsequent two trading sessions to $44.94 a share. The stock has come down around four percent since.

Balance Sheet & Analyst Commentary:

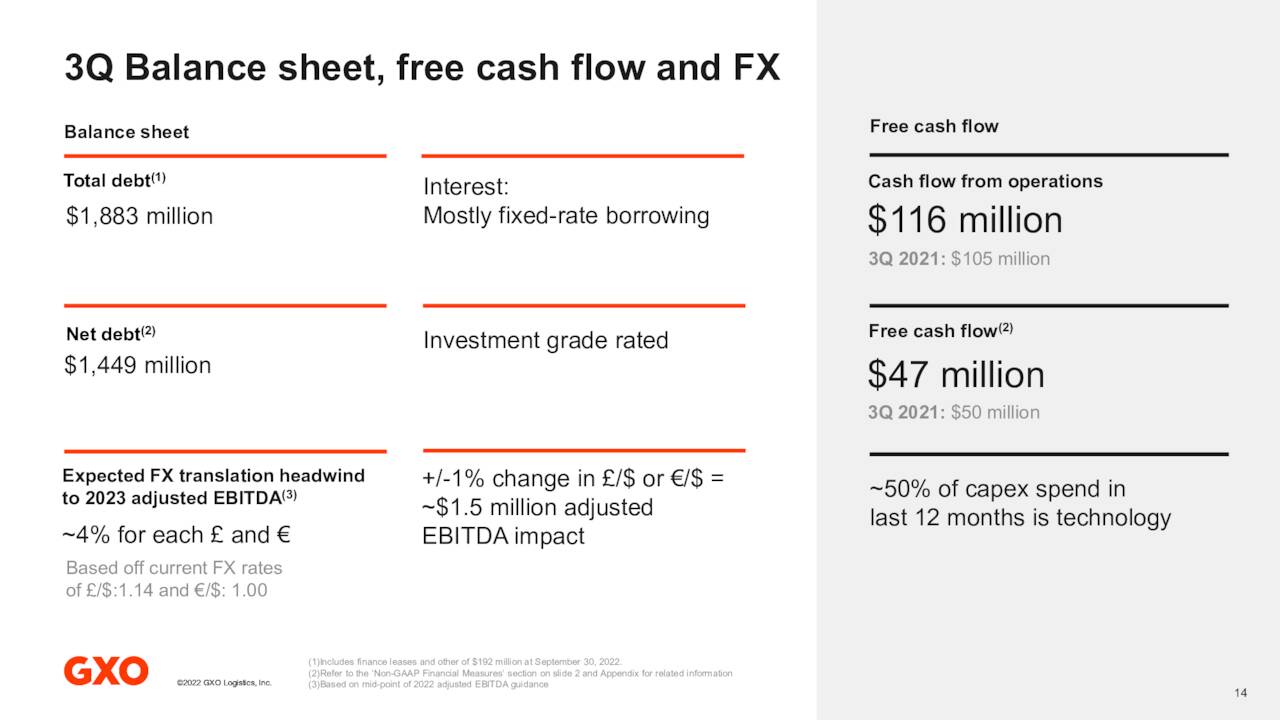

The balance sheet was certainly not the reason for GXO being compelling cheap. Even with the onboarding of ~$900 million of debt to pay for Clipper – bringing its total to $1.9 billion – with cash and equivalents of $434 million, the company’s net leverage was more than manageable at 2.1. That said, the recently birthed GXO does not return capital to shareholders, neither through a dividend nor share repurchases.

November Company Presentation

The Street, despite its recent spate of downward price target revisions – mostly due to multiple compression – leans bullish on GXO, with four buy and five outperform ratings versus three holds with a median twelve-month price objective of just over $50.00 a share. On average, they expect the company to earn $2.72 a share (non-GAAP) on revenue of $8.99 billion in FY22, followed by $2.45 a share (non-GAAP) on revenue of $9.55 billion in FY23.

CEO Malcolm Wilson took Mr. Weiss’ advise, purchasing 4,174 shares of GXO at $43.97 on November 25, 2022.

Verdict:

GXO operates a low EBITDA margin business (~8%) but based on the company’s wins YTD amounting to 6% growth (already) in FY23 and its robust pipeline, the thesis of a secular shift to outsourcing supply chain management appears viable, setting the table for growth far in excess of global GDP. Factoring in long-term contracts that include inflation pass-throughs and minimum volume guarantees, it would appear that the Street’s bottom-line estimate of $2.45 for FY23 is low. With the Fed likely to pump the brakes on rate hikes, perceptions regarding the macro backdrop should begin to improve, further raising GXO’s appeal. The company is not “compellingly cheap,” but it seems a solid covered call candidate.

Very few things make a fool feel smart better than negotiating.”― Mokokoma Mokhonoana

Be the first to comment