Early last month, I discussedCleveland-Cliffs’ (NYSE:CLF) bull case by incorporating the war in Ukraine as well as recession risks. As expected, the stock quickly surged by 20% fueled by a broader upswing in global stocks. In this article, I want to do two things. First, to discuss new developments that make Cleveland-Cliffs an even more attractive investment than I previously thought. This includes rapid input price explosions in competing steel nations like Europe and China where production conditions have turned unfavorable. It also includes what I believe to be a commodity super cycle, which could put a floor under (in this case) steel prices for the foreseeable future, making it possible for CLF to get to the valuation it deserves. Related, I highlight the company’s top-tier supply chains and the benefits that come with that.

Second, I want to look into recession risks, which could hurt demand. Hence, I expect a bit more weakness before the next move is much higher for CLF shares.

So, let’s get to it!

Commodity Super Cycle

Commodities have been the cornerstone of my research for more than 2 years now. Agriculture, metals, energy, you name it. The pandemic has damaged supply chains, and the push for net-zero in 2050 (Paris Climate Agreement) is impacting every carbon-intensive supply chain and increasing demand for certain metals. On top of that, we need to incorporate the “usual” cyclical economic developments and the war in Ukraine, which is making everything even more complicated.

With that said, using the “super cycle” as a bull case sometimes feels like a snake oil salesman trick for two reasons:

The last super cycle started more than 20 years ago (I was too young to get it back then).

It sounds almost too good to be true when someone tells you the stocks you own will remain hot for many years to come.

So, let me explain why I’m using that argument.

But first, let’s look up the definition of “super cycle”. According to Schroders:

Commodities have achieved strong price gains recently, prompting speculation that we could be in the early stages of a so-called super-cycle; a sustained period of growing demand exceeding supply.

While there are many (similar) definitions, it’s basically a prolonged uptrend in commodity prices caused by demand outgrowing supply. This includes secular growth through cyclical waves. Some say it can take at least a decade. I’m not so sure about that and frankly not willing to forecast that far. If we get the super cycle even remotely right (2-3 years), we’ll be in a good place.

In this situation, it’s all about energy. Energy is the driving force of every industrial activity since the invention of the steam engine. Affordable energy is key in providing a foundation for successful industrial nations. That has changed in all key nations. Especially in Europe, where I live.

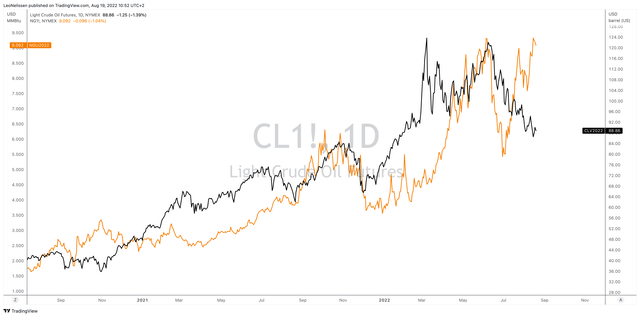

Energy prices are rapidly rising. Oil is trading close to $90, Henry Hub Natural Gas is trading close to $9.

TradingView (Black = WTI Crude, Orange = Henry Hub)

In Europe, natural gas is trading at an equivalent of more than $400 per barrel of oil. This is mainly due to the fact that Russia has massively reduced exports as a tool for economic warfare.

However, the roots of these problems are deeper as I have discussed in a number of articles, including the one below.

Seeking Alpha

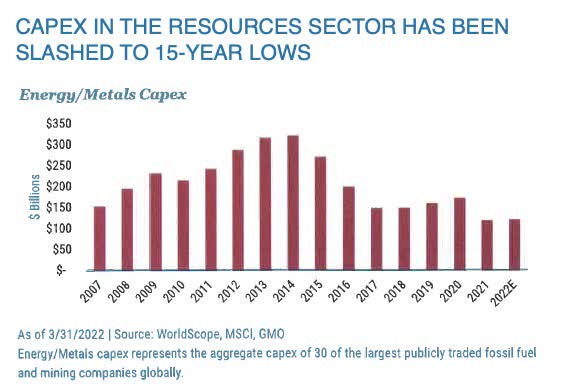

Because of political and economic reasons, both energy and metal companies have reduced capital expenditures. This improves their carbon footprint and cash flows (risk management and higher shareholder returns).

This year the largest 30 publicly traded fossil fuel and mining companies (a proxy for the entire industry) are expected to invest less than $150 billion in CapEx. That’s barely unchanged versus 2021 and nowhere close to the investment levels prior to the commodity crash of 2014/2015. One can imagine what this means in an environment where demand is coming back.

WorldScope, MSCI, GMO

Now, to return to the aforementioned energy crisis, I don’t expect supply to come back meaningfully anytime soon.

As Bloomberg reported (in this case via Mining.com) multiple commodity industries are buckling under the energy crisis. One of them is the steel industry:

The power cuts in China’s Sichuan have affected more than 70% of local steel mills, either through production halts or rationing. That’s putting pressure on prices of iron ore, used to make steel.

British Steel is among heavy industry firms hiking prices on the back of soaring energy costs. Though that has worked in the past due to the strength of Europe’s construction industry, it will be more of a challenge this time as a weaker economy darkens demand prospects.

In the US, at least two steel mills have started suspending some operations to cut energy costs.

It is headlines like the one below that perfectly encapsulate the devastating trend hitting industrial heavyweights like Germany – the world’s 7th-largest steel producer.

Bloomberg

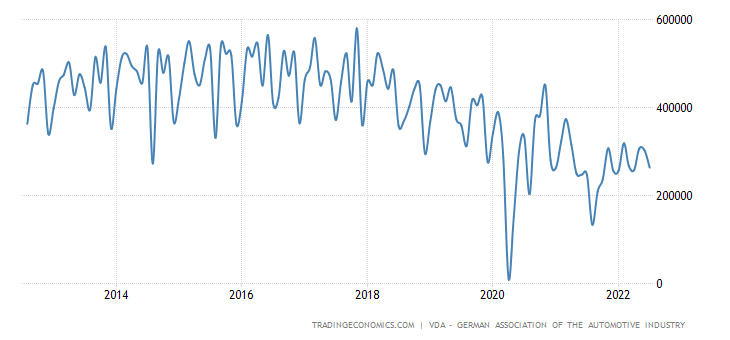

While energy prices will come down, I do not believe that Europe will experience pre-crisis conditions where it can compete with foreign steel. The same goes for industrial production. Remember, automotive production in Germany peaked in 2017, NOT in 2020 as most believe.

TradingEconomics (German Car Production)

CLF CEO Lourenco Goncalves hit the nail on the head in his 2Q22 earnings call when he mentioned the de-industrialization of Europe and the impact this has on North America.

So we are starting to see a reallocation of microchips and other things from Europe to the United States. And we’re also seeing the growth in orders as a consequence of that. So even though I’m not giving you a number Lucas I’m giving you a lot of good indications that things are starting to turn and we are ready for that.

European de-industrialization has been the cornerstone of my research for Intelligence Quarterly, where I covered these developments for institutional clients.

It’s also one of the reasons why I buy North American infrastructure stocks like railroads, trucking, and related.

There’s more to this super cycle, which I will explain now by incorporating Cleveland-Cliffs a bit more.

Cleveland-Cliffs Is In A Terrific Position

Cleveland-Cliffs is not immune to high energy prices. With an annual consumption of 200 million MMBtu, CLF is one of America’s largest natural gas customers. Higher costs related to inflation and some downtime caused adjusted steelmaking EBITDA to fall from $1.36 billion in 2Q21 to $1.11 billion in 2Q22.

After all, the company is now the number one producer of flat-rolled steel products in North America after buying AK Steel in March of 2020 and Arcelor Mittal USA in December of the same year.

Based on this context, there are a few factors that benefit CLF as America’s go-to spot for high-quality steel products.

First of all, its location. As I already highlighted in the first part of this article, energy inflation is an issue in almost every manufacturing nation in the world. However, it’s all about relative differences. The US is in a better spot than both Europe and China when it comes to energy security. If we go beyond the ongoing crisis, the US will continue to benefit from its ability to be a huge net exporter of liquified natural gas. Both Europe and China will need it. Don’t get me wrong, China is still a low-cost steel producer with the ability to dump cheap steel overseas, but its advantages are eroding. That’s what matters here.

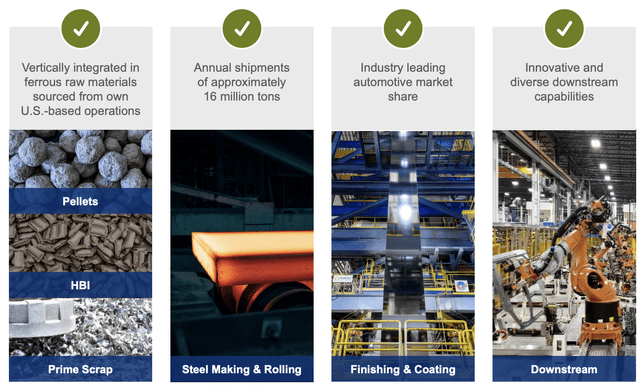

Second of all, CLF is a well-integrated producer thanks to strategic supply chain acquisitions. The company mines its own pallets, HBI, and provides its own scrap. This allows it to save on costs. After all, companies that do not have in-house iron ore sourcing have to pay more as mining companies need to make a profit.

Cleveland-Cliffs

In the case of CLF, the company can produce 27 million gross tons of pellets in its 5 mines. These pallets are 85% less CO2 intensive than sinter. On top of that, the company has the capacity to produce 1.9 million metric tons of HBI per year.

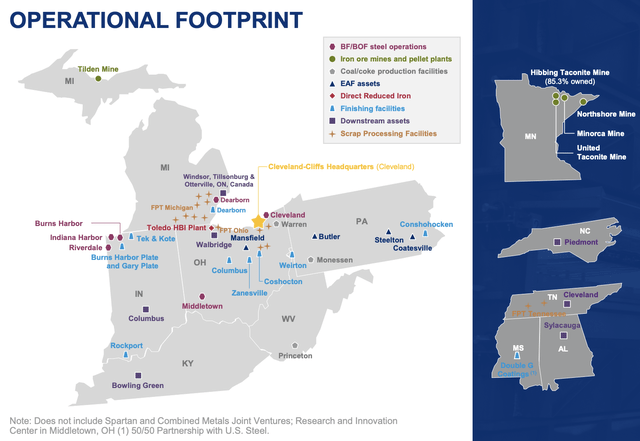

On top of that, and with regard to its supply chains, the company operates its own “ecosystem” in the Midwest, which also makes supply chains more reliable as it does not come with (for example) iron ore imports from Brazil.

Cleveland-Cliffs

Moreover, unlike its American competitors, the company does not rely on imported ferrous raw materials. In this case, both Russia and Ukraine exported 4 million tons of pig iron, 3 million tons of steel, and 2 million tons of semi-finished steel to the US. CLF is not impacted by the war. At least not directly.

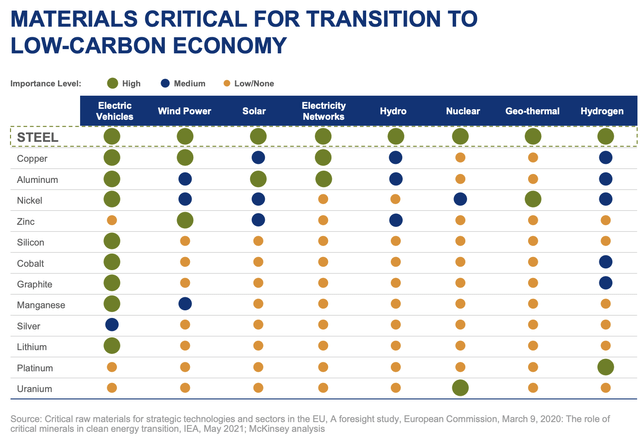

With regard to the aforementioned transition to net-zero, steel is much more important than one might think. While there are many great ways to benefit from higher metal demand related to new energies, steel is key in every single new energy technology. To give you one example, between 66% and 80% of the weight of a wind turbine comes from steel.

Cleveland-Cliffs

In most environmental reports, steel is excluded as the key focus is mainly on rare metals. However, I think that’s wrong – especially when looking at differences between countries. For example, the Chinese steel industry emits 2.5 billion tons of CO2 per year. The US steel industry emits 90 million tons. None of these sentences include a typo. While I am not going to bet any money on China enforcing strict environmental rules, we only need a very small shift in its willingness (or ability) to dump cheap steel overseas to get a much bigger bull case for American steel companies. After all, producing cheap steel for overseas countries has been a large driver of Chinese employment. That will be much harder to achieve when energy prices remain high – or when pollution remains a health hazard in many cities.

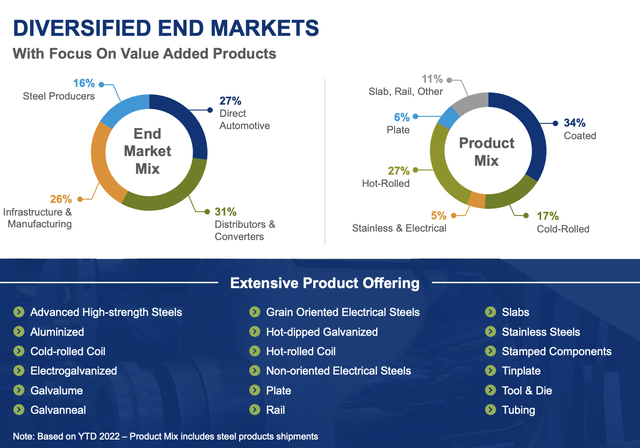

Moreover, and this is also key, CLF produces high-quality steel that goes up very high in various supply chains. That means higher margins (better products instead of what I like to call “generic steel”) and exposure in industries that will require more steel. For example, the company’s wide variety of steel products makes it possible to service the renewable technologies that were listed in the screenshot above.

Cleveland-Cliffs

Basically, is that I believe that CLF will benefit from a prolonged period of strong pricing and steadily rising demand (throughout cycles).

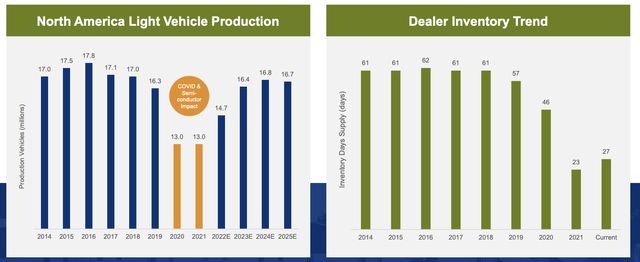

On top of that, the company is benefiting from rebounding auto production.

Because automotive production was lagging behind construction due to supply chain problems, the company believes that now is its time to shine given that the company has 27% direct automotive exposure. It’s also the leading automotive sector steel supplier in general.

In 2020 and 2021 automotive production was down to 13 million units per year. While demand was high, production was influenced by severe supply chain disruptions. This caused dealer inventories to fall to levels not witnessed in modern history. It was actually common that supply was below demand at various dealerships.

Cleveland-Cliffs

What this means is that even if economic growth remains slow, replenishing inventories will come with higher sales for all parties involved in the supply chain.

All of our automotive customers have indicated to us that their supply chain issues are easing, and we are seeing tangible proof of this trough on our own channel checks. The production pace of the first half of this year has been nowhere near its full potential, let along the prior decade average. Starting in the second half of 2022, we expect to get more automotive volume and with more volume and base load for our mills, our costs should naturally improve.

I’m getting a lot of confirmation of this trend. For example, Union Pacific (UNP), the nation’s largest stock-listed railroad shipped more than 228 thousand carloads of motor vehicles and equipment. That’s 6% higher compared to the prior-year period. Quarter-to-date, shipments are up 25%. So, that’s definitely a good sign for the entire industry – even if it is mostly backlog production and not strength based on new orders.

This brings me to recession fears.

Recession Fears

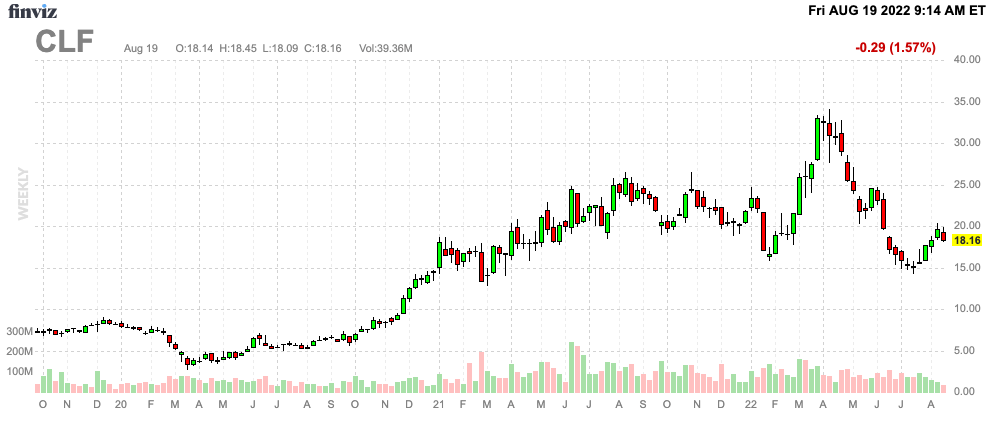

CLF shares have fallen roughly 10% in recent days. Shares are roughly 45% below their 52-week high.

There are two options here. Either the bull case is “garbage” or the bull case is for real but investors aren’t willing to bet on it yet.

Needless to say, I’m going with option 2 because it’s backed by data.

Despite all the bullish things I’ve written in this article so far, economic indicators are weakening.

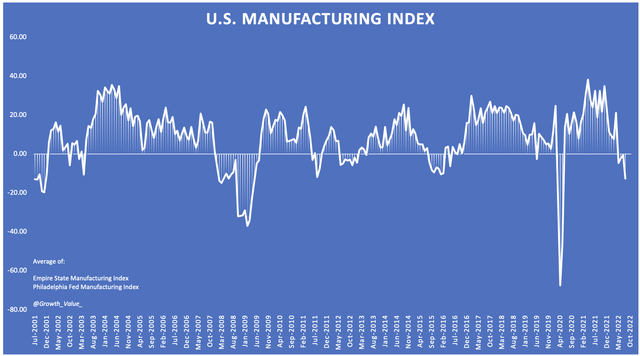

The average of the Empire State and Philadelphia Fed manufacturing surveys are now pointing at high risks of a manufacturing recession as my chart below shows.

Author (Empire State/Philadelphia Fed)

We’re witnessing the impact of high rates, high inflation, ongoing supply chain problems, and consumer weakness on demand. The Fed remains determined to aggressively hike rates as the market now expects the Fed to hike until at least 3.50% in 2023.

The problem is that the Fed cannot directly impact supply problems. It can, however, reduce demand in order to fight inflation. That’s a very toxic thing for the economy, but it’s almost required by the dire situation we’re in.

This is what I wrote in a recent article covering metals:

While falling leading indicators (like the ones above) will almost certainly lead to lower economic expectations, the outlook was already somewhat weak. Using Wells Fargo’s outlook, we see expectations that real gross domestic product growth will fall to a mere 1.7% in 2022 followed by 0.4% contraction in 2023 as inflation is expected to fall to 3.5% with core inflation still hovering at 2x the Fed’s target. While these are expectations, it perfectly shows the challenges facing the economy. Not just in the US, I need to add here.

Wells Fargo

Moreover (this quote also makes sense here):

While all of this is “annoying” for shareholders of cyclical companies, it’s good as it always comes with good buying opportunities.

And that’s what I care most about, buying quality companies at good prices.

CLF Shares Are Too Cheap

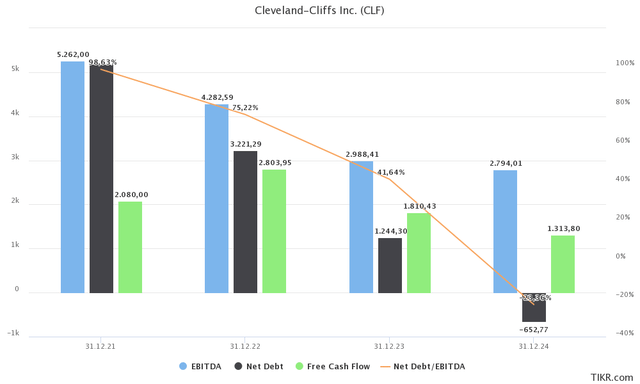

CLF is trading below 5.0x EBITDA. In this case, I’m using the $9.5 billion market cap, $265 million in minority interest, $2.84 billion in pension-related liabilities, and $1.24 billion in expected 2023 net debt to arrive at a $13.85 billion enterprise value. I used $2.8 billion in expected EBITDA as that is what the company should be able to do under normal circumstances. I think $3.0 billion is more likely given my view on metals, but for now, my estimate gives us a bigger margin of safety.

TIKR.com

Besides that the company has an expected net debt ratio of just 0.4x EBITDA using 2023E data, we’re dealing with a valuation that is too low.

For example, under “normal” circumstances, CLF can end up with $650 million in net cash in 2024 (more cash than gross debt. That would have a major impact on the valuation.

If I use 2024 net debt numbers, the valuation drops to roughly 4x EBITDA – all else equal.

Now, if we assume that the commodity super cycle lasts 5 years, the company enters a cycle of high prices, which allows for a long-term decline in net debt allowing for aggressive buybacks and dividends on the side.

It would pave the way for significant total returns on a long-term basis. Even without incorporating a super cycle, I would make the case that CLF is at least 40% undervalued.

So, the risk/reward is pretty good.

Takeaway

We’re in a new era of higher inflation. Forget what we witnessed between 2011 and 2020. It’s different now. Inflation is likely to remain above the Fed’s 2% target on a prolonged basis as supply chains are shifting. This includes new energy market fundamentals that have the ability to provide us with a commodity super cycle.

American steel producers are expected to benefit from tougher production conditions overseas that benefit “Made in the USA”. Cleveland-Cliffs is my favorite player in that space. The company has the best supply chain in North American steel, it has high-quality steel products that go well-beyond automotive applications. Moreover, the company is now in a position to generate high free cash flow, which will benefit investors tremendously thanks to a very healthy balance sheet.

Even without incorporating a super cycle, CLF is too cheap. The stock has at least 40% upside from current prices, I think.

However, it’s not unlikely that CLF dips further before ripping higher. Economic fundamentals are shifting as demand is weakening. The Fed needs to fight inflation and isn’t likely to ease despite slowing economic fundamentals.

Yet, I don’t mind that. These trends are mid-term trends that I expect to shift in our favor in early 2023 when the Fed is likely to pivot. The super cycle is a long-term development.

I am looking to buy CLF as close to $15 as I can. *If* it reaches $15, I will be buying aggressively (relatively speaking).

FINVIZ

However, please be aware that CLF is very volatile. Incorporate that in your decision-making if you’re considering buying CLF. Regardless of how good a bull case sounds, risk management is more important than anything else.

Other than that, I think it’s fair to say that CLF is a tremendous long-term opportunity that will trade nowhere close to where it is trading right now if the bull case is even remotely right.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment